1. What is Linear Programming?

Linear programming is a solution of a mathematical problem concerning maximum

and minimum values of a first-degree (linear) algebraic expression, with variables

subject to certain stated conditions (restraints). This problem class is broad enough

to encompass many interesting and important applications, yet specific enough to

be tractable even if the number of variables is large.

In mathematics, linear programming (LP) problems are optimization problems in

which the objective function and the constraints are all linear. Linear programming is

an important field of optimization for several reasons. Many practical problems in

operations research can be expressed as linear programming problems. Certain

special cases of linear programming, such as network flow problems and

multicommodity flow problems are considered important enough to have generated

much research on specialized algorithms for their solution. A number of algorithms

for other types of optimization problems work by solving Linear Programming

problems as sub-problems. Historically, ideas from linear programming have

inspired many of the central concepts of optimization theory, such as duality,

decomposition, and the importance of convexity and its generalizations.

2. History

Linear programming was developed as a discipline in the 1940's, motivated initially

by the need to solve complex planning problems in wartime operations. Its

development accelerated rapidly in the postwar period as many industries found

valuable uses for linear programming. The founders of the subject are generally

regarded as George B. Dantzig, who devised the simplex method in 1947, and John

von Neumann, who established the theory of duality that same year. The Nobel prize

in econonmics was awarded in 1975 to the mathematician Leonid Kantorovich

(USSR) and the economist Tjalling Koopmans (USA) for their contributions to the

theory of optimal allocation of resources, in which linear programming played a key

role. Many industries use linear programming as a standard tool to allocate a finite

set of resources in an optimal way. Examples of important application areas include

airline crew scheduling, shipping or telecommunication networks, oil refining and

blending, and stock and bond portfolio selection.

3. Forms

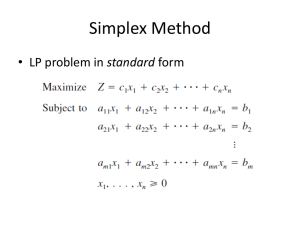

Standard form

Standard from is the usual and most intuitive form of describing a linear programming problem.

It consists of the following three parts:

A linear function to be maximized

e.g. maximize

Problem constraints of the following form

e.g.

Non-negative variables

e.g.

The problem is usually expressed in matrix form, and then becomes:

maximize

subject to

Other forms, such as minimization problems, problems with constraints on alternative forms, as

well as problems involving negative variables can always be rewritten into an equivalent problem

in standard form.

Example

Suppose that a farmer has a piece of farm land, say A square kilometers large, to be planted with

either wheat or barley or some combination of the two. The farmer has a limited permissible

amount F of fertilizer and P of insecticide which can be used, each of which is required in different

amounts per unit area for wheat (F1, P1) and barley (F2, P2). Let S1 be the selling price of wheat,

and S2 the price of barley. If we denote the area planted with wheat and barley with x1 and x2

respectively, then the optimal number of square kilometers to plant with wheat versus barley can

be expressed as a linear programming problem:

maximize

(maximize the revenue - revenue is the "objective function")

subject to

(limit on total area)

(limit on fertilizer)

(limit on insecticide)

(cannot plant a negative area)

Which in matrix form becomes:

Maximize

subject to

Augmented form (slack form)

Linear programming problems must be converted into augmented form before being solved by

the simplex algorithm. This form introduces non-negative slack variables to replace

non-equalities with equalities in the constraints. The problem can then be written on the following

form:

Maximize Z in:

where xs are the newly introduced slack variables, and Z is the variable to be maximized.

Example

The example above becomes as follows when converted into augmented form:

maximize

(objective function)

subject to

(augmented constraint)

(augmented constraint)

(augmented constraint)

where

are (non-negative) slack variables.

Which in matrix form becomes:

Maximize Z in:

Duality

Every linear programming problem, referred to as a primal problem, can be converted into an

equivalent dual problem. In matrix form, we can express the primal problem as:

maximize

subject to

The equivalent dual problem is:

minimize

subject to

where y is used instead of x as variable vector

.

4. Theory

Geometrically, the linear constraints define a convex polyhedron, which is called the

feasible region. Since the objective function is also linear, all local optima are

automatically global optima. The linear objective function also implies that an

optimal solution can only occur at a boundary point of the feasible region.

There are two situations in which no optimal solution can be found. First, if the

constraints contradict each other (for instance, x ≥ 2 and x ≤ 1) then the feasible

region is empty and there can be no optimal solution, since there are no solutions at

all. In this case, the LP is said to be infeasible.

Alternatively, the polyhedron can be unbounded in the direction of the objective

function (for example: maximize x1 + 3 x2 subject to x1 ≥ 0, x2 ≥ 0, x1 + x2 ≥ 10), in which case

there is no optimal solution since solutions with arbitrarily high values of the

objective function can be constructed.

Barring these two pathological conditions (which are often ruled out by resource

constraints integral to the problem being represented, as above), the optimum is

always attained at a vertex of the polyhedron. However, the optimum is not

necessarily unique: it is possible to have a set of optimal solutions covering an edge

or face of the polyhedron, or even the entire polyhedron (This last situation would

occur if the objective function were constant).

5. Algorithms

Figure 1.

Figure 1 is showing how a series of linear constraints on two variables produce a feasible region in

a linear programming problem.

A series of linear constraints on two variables produces a region of possible values

for those variables. Solvable problems will have a feasible region in the shape of a

simple polygon.The simplex algorithm, developed by George Dantzig, solves Linear

Programming problems by constructing an admissible solution at a vertex of the

polyhedron, and then walking along edges of the polyhedron to vertices with

successively higher values of the objective function until the optimum is reached.

Although this algorithm is quite efficient in practice, and can be guaranteed to find

the global optimum if certain precautions against cycling are taken, it has poor

worst-case behavior: it is possible to construct a linear programming problem for

which the simplex method takes a number of steps exponential in the problem size.

In fact for some time it was not known whether the linear programming problem was

NP-complete or solvable in polynomial time.

The first worst-case polynomial-time algorithm for the linear programming problem

was proposed by Leonid Khachiyan in 1979. It was based on the ellipsoid method in

nonlinear optimization by Naum Shor, which is the generalization of the ellipsoid

method in convex optimization by Arkadi Nemirovski, a 2003 John von Neumann

Theory Prize winner, and D. Yudin.

However, the practical performance of Khachiyan's algorithm is disappointing:

generally, the simplex method is more efficient. Its main importance is that it

encouraged the research of interior point methods. In contrast to the simplex

algorithm, which only progresses along points on the boundary of the feasible region,

interior point methods can move through the interior of the feasible region.

In 1984, N. Karmarkar proposed the projective method. This is the first algorithm

performing well both in theory and in practice: Its worst-case complexity is

polynomial and experiments on practical problems show that it is reasonably

efficient compared to the simplex algorithm. Since then, many interior point methods

have been proposed and analysed. A popular interior point method is the Mehrotra

predictor-corrector method, which performs very well in practice even though little is

known about it theoretically.

The current opinion is that the efficiency of good implementations of simplex-based

methods and interior point methods is similar for routine applications of linear

programming.

LP solvers are in widespread use for optimization of various problems in industry,

such as optimization of flow in transportation networks, many of which can be

transformed into linear programming problems only with some difficulty.

0

0