Chapter 6

advertisement

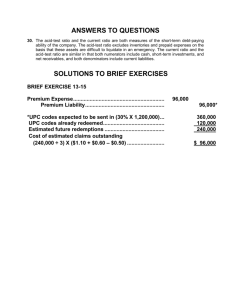

Chapter 6 How Much Health Insurance Should Everyone Have? Chapter Overview Questions: What is an optimal insurance plan, i.e., what should we insure? How are insurance premiums determined? Should employer provided insurance be tax exempt to the employee? Why are so many people without health insurance in the US? 1. How is a premium calculated? a. Pure premium for a group of people is the average cost of covering their medical expenses. b. Pure premium = probability of loss * loss = average expected loss c. E.g., if loss is $50,000 and probability of it occurring is .01 (1 of 100), then pure premium is .01 * $50,000 = $500. If the company insures 100 people and charges them $500 each, it’ll collect enough money to meet cost of medical services. d. Load = administrative, marketing costs + profit e. Premium = Load + pure premium f. Medical loss ratio is Pure Premium/ Premium or Medical Expenses/Premium 2. Decision to purchase insurance a. Should I buy insurance and put risk on other for a certain loss (=premium) or should I take the chance and self-insure? b. Individual will buy if MB of insurance > MC of insurance c. Economists assume that Marginal Utility of Income decreases as you acquire more of it making individuals risk averse. A loss of $1000 is more painful than a gain of $1000 (e.g., IRS) d. If load is large relative to pure premium, individuals will not buy insurance but would rather self-insure. e. Losses that have either very high probabilities (routine) or very low probabilities(remote) or are small in $ amount are likely to have high loads relative to the pure premium = average expected loss, so MB of insuring likely to be < MC of insuring. Better not to insure. f. E.g., no sense to have OTC drug insurance g. Buy insurance for big $ losses and less than routine events, e.g., hospitalization, big $ Rx drugs. h. Key Point: Quality of insurance plan is not how much it covers but whether it covers all risks whose MB > MC. Mandating a more comprehensive plan would decrease happiness. 3. Why do most Americans have insurance for risks that are routine or small $ then? Answer: employer paid and tax exempt to the employee insurance. a. Tax-free, employer-purchased health insurance provides a financial incentive to purchase health insurance for small claims. If an employee saves 40 percent when the employer buys health insurance, the price of insurance to that employee has been reduced by 40 percent. Given health insurance demand elasticity of -1, a 40% decrease in price leads to a demand for 40% more coverage. b. High income groups with highest tax brackets most responsive. c. Consequence: overinsurance in America where MB < MC = wasteful. d. Employees have little concern with getting extra services, so extra testing, services, tech prescribed by MDs meets little resistance from patients = lots of spending 4. Should tax-exemption of employer purchased HI be eliminated? A. Subsidy costs a lot of lost tax dollars (shifted to others). $270 billion in 2010 in forgone federal, Social Security, and state taxes. B. Huge subsidy for high income earners. (see table below) C. Employees have less incentive to select lower-cost health plans. D. Eliminating tax-exemption would end subsidy to well-to-do, increase insurer competition by making employees think about premium and services and improve efficiency by making MB vs. MC coverage decisions relevant. E.g. is the Lexus plan worth the extra tax bill vs. the Hyundai plan? E. Ending tax-exemption would make health insurance less comprehensive. Unlikely to pay for routine and low cost care (because individuals will choose not to pay the load for these kinds of coverage). 5. More on premiums and insurance features: A. Experience Rating is like auto collision/comprehensive insurance, i.e., make more claims & you’ll pay more premiums. No cross-subsidy, i.e., what you use is what you pay for. B. Most company insurance is experience rated. C. Community Rating is where all individuals in a particular class pay the same premium regardless of claims history. Some states (like NY) mandate community rating but most (until the Affordable Care Act) allowed experience rating. D. Cross-subsidization by low-users to high-users. All pay same average premium. No incentive to limit use or risky behaviors that affect health. E. Coinsurance, deductibles, indemnity plans (pay a certain amount for care) & service benefit plans (pay for services less copay). Many have both service benefit (within panel) and indemnity plan(out of network with deductible & coinsurance). Out of pocket costs are used to limit medical care demand. 6. Moral Hazard a. Moral hazard – lower out of pocket costs lead to increased medical care demand, ignoring true costs, which leads to waste (MB<MC) and higher premiums, which in turn leads to fewer people demanding health insurance (more uninsured). Estimated cost to GDP is 3%. b. Problem magnified with employer HI being tax-exempt 7. Adverse Selection a. Higher use individuals will disproportionately choose policies with generous coverage if premiums are community rated (= cross-subsidized). Will not be able to afford insurance if experience rated. b. Lower use individuals will balance type of plan with cost of plan. If experience rated, could opt for Lexus or Hyundai plan depending on preferences. If community rated, will invariably choose more limited coverage because generous plans will have premiums far in excess of expected benefit. c. If insurers have to community rate, problem will arise where best plans will disproportionately attract high users, leading to high average premiums, which will promote exit of low-users leading to even higher premiums. Race to bottom will occur as the most comprehensive plans will invariably be eliminated & population will move to the next lower rung in terms of coverage. d. Undesirable effects: excess turnover from plan to plan leading to gaps in coverage, losses for insurers with comprehensive plans and lack of choice eventually in plan type. 8. Preferred Risk Selection: Insurers will attempt to limit the effects on them of adverse selection by a. excluding pre-existing conditions or delay of benefits (won’t cover for 1 year) conditions b. offering discounts for long-time insures c. imposing high deductibles & copays and low annual/lifetime limits d. Limit choice of MD or hospital or limit specialists in panel and Rx to generics. e. imposing strict utilization review, prior authorization & second-opinions f. structure benefits to attract healthy and discourage sick, i.e., wellness benefits (gym, diet clubs, etc.) g. Hyundai plans will attract healthy and won’t attract ill NOTE: if insurer can avoid the few high users, it’ll make a lot more money (see table of use) 9. How could we increase insurance coverage of the population & deal with adverse selection? a. subsidies for those w/o sufficient income to buy insurance b. Allow experience rating but then high-users will be uninsured. c. Under community rating, everyone must buy insurance (=mandate). The vast majority of people under such a mandate would be good risks (low users) when they bought insurance and wouldn’t be uninsurable once they became ill (& needed insurance). d. Problem: many low users don’t want to pay when their use is low (MB < MC) and don’t want to cross-subsidize the older/wealthier population. e. Uninsured include many who can’t buy (not enough income vs. premium) and those who don’t want to buy (could be 50% of uninsured) 10. Impacts of Affordable Care Act a. ACA will make premiums higher in the individual market because: Mandates “essential” benefits package (which is more comprehensive) Mandates community rating Eliminates preexisting condition exclusions Many young/healthy people will pay the penalty tax and not buy insurance; will only buy insurance if they get sick (which is adverse selection problem) Higher taxes on insurers, drug firms and medical device makers will be passed on to insurees Insurers are anticipating that adverse selection will occur, biased toward those who are older and have higher risks. To control utilization and to lower their costs, insurers are using narrow provider networks and high coinsurance to discourage enrollees from using out-of-network providers that are likely to be more expensive. b. After ACA the uninsured rate dropped significantly, from 16.2% in the last quarter of 2013 to 10.7% in the first quarter of 2015 for nonelderly population. Adding in elderly (who are largely covered by Medicare + Medicaid) yields a 9.2% uninsured rate. Table of Use Distribution of Health Care Expenditures in US Tax Savings: Distribution of Employer-Paid Health Insurance Tax Exclusion, by Income, 2010