Subject Name: Financial Accounting - V-SECT

advertisement

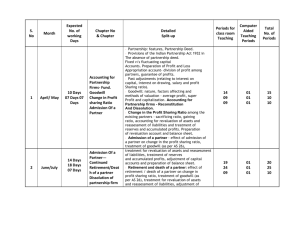

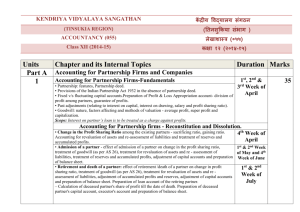

Syllabus Course Semester Subject Title Subject Code : : : : MCA 1st Financial accounting MCA14 Financial Statements Financial Statements, Meaning Of Financial Statements, Usefulness Of Financial Statements, Trading Account, Manufacturing Account, Profit And Loss Account. Balance Sheet, Distinction Between Tangible Assets And Intangible Assets, Distinction Between Fixed Assets And Current Assets, Distinction Between Trading And Profit And Loss Account And Balance Sheet, Distinction Between A Trial Balance And A Balance Sheet , Methods Of Presenting The Final Accounts, Treatment Of Some Items Which May Be Direct Items/Indirect , Items/Incomes/Expenses Classification Of Capital And Revenue, Rationale Of Making Adjustments At The Time Of Preparing The Final Accounts, Distinction Between Prepaid Expenses And Outstanding Expenses, Distinction Between Accrued Income And Unaccrued Income, Treatment Of Items Of Adjustments Appearing In The Trial Balance, Treatment Of Items Of Adjustments Appearing Outside The Trial Balance. Accounting Of Partnership Firms Consignment Accounts, Distinction Between Consignment And Sale, Terms Used In Consignment, Valuation Of Unsold Stock Lying With The Consignee, Treatment Of Abnormal Loss, Treatment Of Normal Loss, Distinction Between Normal Loss And Abnormal Loss In Consignment , Accounting Entries In The Books Of Consignor, Accounting Entries In The Books Of Consignee Accounting For Partnership Firms – Fundamentals Meaning, Essential Elements And Nature Of A Partnership, Partnership Deed , Methods Of Maintaining Capital Accounts Of Partners, Treatment Of Interest On Capital, Calculation Of Interest On Capital , Calculation Of Interest On Drawings, Treatment Of Interest On Partner’s Loan To The Firm, Calculation Of Commission To A Partner, Division Of Profit Among Partners, Calculation Of Capital Ratio, Past Adjustments, Guarantee Of Minimum Profit To A Partner, Goodwill, Change In Profit Sharing Ratio Accounting For Partnership Firms – Admission Of A Partner New Profit Sharing Ratio And Sacrificing Ratio, Treatment Of Goodwill, Calculation Of Hidden Goodwill, Revaluation Of Assets And Liabilities, Memorandum Revaluation Of Assets And Liabilities, Adjustment For Reserves And Accumulated Profits/Losses, Adjustment Of Capital Accounting For Partnership Firms – Retirement/Death Of Partner New Profit Sharing Ratio And Gaining Ratio, Distinction Between Sacrificing Ratio And Gaining Ratio, Treatment Of Goodwill, Revaluation Of Assets And Liabilities, Adjustment For Reserves And Accumulated Profits/Losses, Adjustment Of Capitals, Disposal Of The Amount Due To The Retiring Partner, Joint Life Policy, Death Of A Partner Shares And Debentures Accounting For Share Capital, Meaning, Nature And Characteristics Of A Company, Meaning And Categories Of Share Capital, Distinction Between Reserve Capital And Capital Reserve, Distinction Between Authorized Capital And Issued Capital, Meaning, Nature And Classes Of Shares, Distinction Between An Equity Share And Preference Share, Issue Of Shares , Minimum Subscription, Distinction Between Over-Subscription And Under-Subscription, Issue Of Shares At Par, Issue Of Shares At A Premium, Issue Of Shares At A Discount, Calls-In Arrears And Calls-In-Advance, Issue Of Shares For Consideration Other Than Cash, Forfeiture Of Shares, Re- Issue Of Shares, Forfeiture And Re-Issue Of Shares Allotted On Pro-Rata Basis In Case Of Over-Subscription. Issue Of Debentures Meaning And Nature Of Debenture, Distinction Between A Share And A Debenture, Kinds Of Debentures, Issue Of Debentures, Issue Of Debentures For Cash, Issue Of Debentures For Consideration Other Than Cash, Issue Of Debentures As Collateral Security, Accounting For Issue Of Debentures Considering The Terms And Conditions Of Redemption, Treatment Of Discount On Issue Of Debentures, Treatment Of Loss On Issue Of Debentures, Interest On Debentures. Ratio Analysis Meaning Of Ratio Analysis, Meaning Of Ratio, Liquidity Ratios, Solvency Ratios, Activity Ratios, Profitability Ratios, Importance Of Ratio Analysis, Precautions To Be Taken, Limitations Of Ratio Analysis Funds Flow Statement Meaning Of Funds Flow Statement, Objective Of Funds Flow Statement, Distinction Between Funds Flow Statement And Position Statement, Distinction Between Funds Flow Statement And Income Statement, Uses Of Funds Flow Statement, Limitations Of Funds Flow Statement, Preparation Of Funds Flow Statement, Preparation Of Schedule Of Changes In Components Of Working Capital, How To Determine Whether An Asset Is A Current Asset Or Non-Current Asset, Distinction Between Funds Flow Statement And Schedule Of Changes In Working Capital, Analysis Of Changes In Non-Current Items, Treatment Of Provision For Taxation, Treatment Of Financing And Investing Activity Not Affecting The Working Capital, Meaning Of Funds From Operations, Methods Of Computation Of Funds From Operations, Preparation Of Fund Flow Statement, Is Depreciation A Source Of Funds?