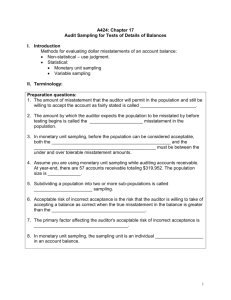

Audit Sampling: Concepts and Techniques

advertisement

Audit Sampling Slide 9-1 © The McGraw-Hill Companies, Inc., 2006 Audit Detection Risk (DR) Detection Risk - Auditors’ planning and tests cause them to reach incorrect conclusion about management assertions. Sampling & Nonsampling Portions Nonsampling - Auditor Deficiencies or Mistakes Sampling - Probability that sample will NOT yield same result as 100% test; causing auditor to draw incorrect conclusion. Slide 9-2 © The McGraw-Hill Companies, Inc., 2006 Population Variability Increases Sampling Error since it increases risk that sample may not be representative of the entire population of balances or transactions. Called “Standard Deviation” Most common way to minimize impact: Population Stratification Slide 9-3 © The McGraw-Hill Companies, Inc., 2006 Population Variability Item Population A 1 2 3 4 5 Mean Standard Deviation Slide 9-4 Population B 2,100 2,100 2,100 2,100 2,100 8,000 25 2,000 400 75 2,100 2,100 -0- 3,395 © The McGraw-Hill Companies, Inc., 2006 Advantages of Statistical Sampling Design efficient samples Measure sufficiency of evidence Objectively evaluate sample results Can project sample results so that you can draw a conclusion about the entire universe or population from which sample was taken. Slide 9-5 © The McGraw-Hill Companies, Inc., 2006 Selection of Statistical Samples Random number (tables, generators) Systematic selection Probability Proportional to Size(PPS) A form of automatic stratification (all items > sampling interval are sampled) Slide 9-6 © The McGraw-Hill Companies, Inc., 2006 Types of Statistical Sampling Attributes Variables Sampling Sampling Discovery Slide 9-7 Sampling © The McGraw-Hill Companies, Inc., 2006 Requirements of Audit Sampling Plans • Consider specific audit objective being tested. • Establish Materiality: Maximum Tolerable: Deviation rate (testing internal controls) or Misstatement (substantive tests) • Set Allowable sampling risk (what auditor will accept) • Consider population characteristics (variability, etc.) • Select items in such a manner (statistical) so that they can be expected to be representative of the population. • Project sample results to the entire population. • Treat items that cannot be audited as misstatements or deviations in evaluating the sample results. Unless... • Evaluate nature and cause of deviations/misstatements. Slide 9-8 © The McGraw-Hill Companies, Inc., 2006 Determining Tolerable Deviation How Important is the Control Activity? Are There Other Compensating Controls? Rules of Thumb per AICPA Study: Planned CR Tolerable Deviation Low 2% - 7% Moderate 6% - 12% Slightly < Maximum 11% - 20% Maximum No Testing Slide 9-9 © The McGraw-Hill Companies, Inc., 2006 Projecting Deviations Number of exceptions or deviations from compliance with internal controls found divided by Number of opportunities sampled = Deviation % Notes: If sample deviation % less than tolerable, then CR is lower than planned & vice versa. Reliability is based on sampling +precision & CL. Slide 9-10 © The McGraw-Hill Companies, Inc., 2006 Sampling Risks Tests of Controls Auditors’ Conclusion From the Sample Is: Deviation Rate Is Less than Tolerable Rate Deviation Rate Exceeds Tolerable Rate Slide 9-11 True State of Population Deviation Rate Deviation Rate Is Less Than Exceeds Tolerable Rate Tolerable Rate Correct Decision Incorrect Decision (Risk of Assessing Control Risk Too High) Incorrect Decision (Risk of Assessing Control Risk Too Low) Correct Decision © The McGraw-Hill Companies, Inc., 2006 Substantive Tests of Details Tolerable Misstatement Based on overall F.S. materiality threshold and that for the particular account. For the particular test (with sampling or not) the tolerable misstatement would be lower than either of the overall because of: Misstatements which could occur in other accounts. Misstatements in same account from other tests/ assertions. At account level, normally no more than 75% of overall materiality threshold. Slide 9-12 © The McGraw-Hill Companies, Inc., 2006 Sampling Risks Substantive Tests of Details Auditors’ Conclusion From the Sample Is: True State of Population Misstatement in Misstatement in A/C is Less Than A/C Exceeds Tolerable Amount Tolerable Amount Misstatement in A/C is Less Than Tolerable Amount (not materially misstated) Correct Decision Misstatement in A/C is Exceeds Tolerable Amount (materially misstated) Incorrect Decision Slide 9-13 (Risk of Incorrect rejection) Incorrect Decision (Risk of Incorrect acceptance) Correct Decision © The McGraw-Hill Companies, Inc., 2006 What Effects Sample Size? Population Size Little impact, except very small populations Expected Error Rate Direct Relationship Actual Error Rate Direct Relationship Standard Deviation Direct Relationship Auditor’s Tolerable: Deviation/Misstatement Opposite Relationship Risk of Incorrect Acceptance/Rejection Opposite Relationship Slide 9-14 © The McGraw-Hill Companies, Inc., 2006 Projecting Misstatements Classical variables sampling » Mean-per-unit estimation » Ratio estimation » Difference estimation Probability-Proportional-to-Size (PPS) sampling Slide 9-15 © The McGraw-Hill Companies, Inc., 2006 Projecting Misstatements-Classical Population: 1,000, $200,000 (average/mean = $200) Sample: 50, $9,000 (mean = $180) Audited sample value: $8,500 (mean = $170) Mean-per-unit estimation (used in universe $ unknown) Audited value = Audited mean ($170) X items in population (1,000) = $170,000 . Misstatement = $30,000 ($200,000 - $170,000) Ratio estimation Sampled misstatement of $500 ($9,000-8,500)/ Sample $ (9,000) = 5.56% X Population ($200,000) = $11,200 misstatement Difference estimation Sample book mean ($180) – Audited mean ($170) = $10 difference. Misstatement = $10,000 (1,000 X $10) Note: These are point estimates within + precision at CL. Slide 9-16 © The McGraw-Hill Companies, Inc., 2006 Projecting Misstatements-PPS Computation is by sampled item and then is totaled for all items sampled to get total misstatement per audit. For items > sampling interval (generally = or < materiality threshold), misstatement is NOT projected to the entire population (just like stratified classical sampling). For items < sampling interval, misstatement is projected to the entire population (just like unstratified classical sampling). Note: These are point estimates within + precision at CL. Slide 9-17 © The McGraw-Hill Companies, Inc., 2006 Projecting Misstatements-PPS Sampling Interval = $3,000 (number of $/sample size) Sampled item (trans or subaccount) book value = $100 Sampled Item Audit-determined value = $95 Item misstatement = Tainted % ($100-95=$5/$100 = 5%) X sampling interval ($3,000) = $150 __________________________________________________ Sampling Interval = $3,000 (number of $/sample size) Sampled item (trans or subaccount) book value = $4,000 Sampled Item Audit-determined value = $40 Item misstatement = $4,000 - $40 = $3,960 Slide 9-18 © The McGraw-Hill Companies, Inc., 2006