Islamic Compliant FX Forwards

Jonathan Lawrence

Derivatives and Structured

Products Group Meeting

4 August 2011

Copyright © 2011 by K&L Gates LLP. All rights reserved.

Background

US regulatory issues for cash-settled FX business

i.e. non-deliverable currency forwards

Characterisation as swaps therefore potential

regulation as swap dealers

2

Recognition of Hedging in Islam

Important objective of Shariah is to preserve and

protect wealth

Many Quranic verses indicate importance of taking

strategic measure to minimise anticipated risk to

property

3

Conventional and Shariah Viewpoints on FX

Forward

Conventional views:

Shariah Views:

Used to manage/hedge

against risk of fluctuations in

exchange rates

Is a derivative instrument

conducting a sale in the future

at a price fixed today

Contract sealed today but

settlement & delivery in the

future

Problem with FX: parties

wish to exchange currency in

future but have already fixed a

rate today

Contravenes Shariah rules

of bay’ al-sarf: exchange

should involve transactions on

a spot basis

4

Structuring

Contracts and principles in accordance with Shariah

rules and principles

Not to be used as an excuse for practising the

charging of interest

Each contract to be separate

Each contract to be actual – not fictitious

Each contract to have its own effect

5

Execution

Each contract to be executed separately

Execution of contracts to follow correct and logical

sequence

A real transaction must occur each time

Independent and separate nature of each contract

6

Usage

Instruments only to be used for hedging and not

speculation

Must be an underlying “real” transaction and not

merely a sham

Must be a real need to undertake the transaction

7

Wa’dan

Two unilateral promises given by two parties to one

another

The two promises are not connected

Application depends on two different conditions

shown in diagram below

8

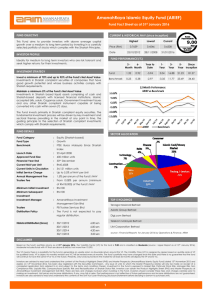

Islamic Currency Forward Based on Wa’dan

(two unilateral promises) at Dealing Date

1

Customer

Bank

Promises to sell USD1 million

at the rate of 3.5 if exchange

rate USD/MYR >3.5

2

Customer

Bank

Promises to buy USD1 million

at the rate of 3.5 if exchange

rate USD/MYR is below or

equal to 3.5

9

Islamic Currency Forward Based on Wa’dan

(two unilateral promises) at Value Date

Scenario 1: If USD/MYR > 3.50 (e.g. 3.60), bank

exercises its right under the first promise, to buy USD

for MYR at agreed rate of 3.50

Scenario 2: if USD/MYR< 3.50 (e.g. 3.40), customer

exercises its right under the second promise, to sell

USD for MYR at agreed rate of 3.50

10

Tawarruq contract

A financial institution, either directly or indirectly, will

buy an asset and immediately sell it to a customer on

a deferred payment basis. The customer then sells

the same asset to a third party for immediate delivery

and payment, the end result being that the customer

receives a cash amount and has a deferred payment

obligation for the marked-up price to the financial

institution. The asset is typically a freely tradeable

commodity such as platinum or copper.

11

FX Forward Based on Tawarruq

Payment of US$ 10 Million at

Value Date

Bank

Broker B

US$ 10 Million

Pay RM35

Million at Value

Date

RM35

Million

US$ 10 Million

Broker A

Customer

Payment of US$ 10 Million at

Value Date

Forward Rate:

US$/MYR =3.50

12

Conditions of Use

Approval given by Shariah committees only if the

instrument is exclusively for hedging purposes. This

means:

can only be used as insurance activity

cannot be used for funding and trading by means of

speculation

13