Clinker (1)

advertisement

")

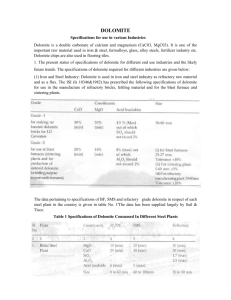

‘Small Talk’ – Small and Medium Market Cap Conference 26 February 2013 Presentation coverage Who we are and what we do • Diversified open cast miner and materials supplier • “Delivering consistent growth” Corporate activity • • • • What is happening in our environment Strategy & rationale • Focus on smaller Clinker sized projects Infrasors adds to Afrimat’s BEE sustainability How are we performing financially • Excellent cash conversion • Strong balance sheet • Consistent dividend payer The future and what lies ahead • Acquisitions paying off • Market remains under pressure • Diversification underpins sustained performance 2 Group overview Leading black empowered open cast miner and materials supplier Strategically diversified through location and product range 3 Afrimat’s products Products from mines: Aggregates (crushed stone) Metallurgical dolomite Metallurgical quartzite Agricultural lime Clinker Products from factories: Concrete blocks Concrete bricks Pavers 4 Afrimat’s products (cont’d) Products from readymix batch plants: Readymix concrete Readymix mortar Services by the contracting team: Contract crushing Mobile screening Drilling Blasting 5 Supply market segments Transport infrastructure: Road building materials Materials for railroads (e.g. ballast) Industrial minerals: Metallurgical dolomite Quartzite Energy infrastructure: Materials for power stations (e.g. Medupi) Materials for renewable energy projects Materials for distribution network 6 Supply market segments (cont’d) Building materials: Affordable housing (Government funded) Commercial building Residential (Privately funded) Agriculture: Agricultural lime Drainage stone Paving 7 Our diversification … portfolio … and footprint MINING & AGGREGATES Commercial quarries (24) Sand and gravel mines (8) Dolomite mine (1) Clinker (1) CONTRACTING Mobile Crushing Drilling and Blasting CONCRETE PRODUCTS Concrete brick & block factories (9) READYMIX Batching sites (17) … which generates a balanced consistent income stream 8 Strategic principles Diversified: Wide product range Across wide geographic markets Effective hedge against market volatility Competitive advantage: Geographic location Unique and scarce products or Operations with structural cost advantage Innovation and creativity Operational expertise 9 Corporate Activity 10 Acquisitions: The underlying strategy The goal Enhance sustainability, profitability and robustness Targets Acquisition purchase consideration below 15% of Afrimat market cap In our space of expertise High upside Compensate for our weaknesses Must fit strategically into our master plan 11 Infrasors transaction Acquired 50.4% (control) at 35 cps amounting to R32 million Competition Commission approved transaction Infrasors: Listed resources group involved in mining and beneficiation of minerals used in the industrial, metallurgical, mining and construction sectors Lyttelton Centurion Mine – opencast mining and beneficiation of a dolomite ore-body Marble Hall Mine – opencast mining and beneficiation of a limestone (metamorphosed dolomite) ore-body Delf Sand – sand extraction and beneficiation of alluvial silica sand Delf Silica Coastal – sand extraction and beneficiation of alluvial silica sand Conditions precedent ABSA (ring fenced) – no material changed to debt facilities, pricing or repayment terms 12 Infrasors transaction (cont’d) Rationale (product and assets) Augment Afrimat’s industrial minerals diversification strategy Add to the aggregates product offering Expand geographic footprint Operational involvement Afrimat manager appointed to oversee operations Take control of board Implement Afrimat’s proven management, marketing, product development and pricing strategies Implement a proper BEE scheme 13 Clinker Group acquisition Effective 1 March 2012 Purchase consideration R121 million (R95 million in cash and R26 million shares) F2012 PAT = R35.1 million Business with unique competitive advantage Already well integrated into Afrimat Life expectation of operation is 10 years Marketing and research drive shows possibility of extending life of mine 14 Clinker Group 15 Clinker Group (cont’d) 16 Impact of acquisitions Glen Douglas Open pit dolomite mine in Gauteng (metallurgical dolomite, aggregates, agricultural lime) R35 million purchase consideration Defensive product diversification Industrial minerals with vast applications Attractive margins and strong profitability Life of mine: >30 years Clinker Clinker Supplies and SA Block (brick & block manufacturing) in Gauteng Processor of clinker material – used in manufacture of concrete products R121 million purchase consideration Product diversification which adds to current product line with geographic diversification Vast applications Attractive margins and strong profitability Life of project: 10 years + 17 BEE update BEE ownerships is 26.1% (including 6.4 million shares purchased) Mega Oil SPV’s 7-year lock-in period expires November 2013 Afrimat BEE Trust purchased 6.4 million shares from Mega Oils Afrimat provided funding (R40 million) Purchased shares prior to expiry date to eliminate any BEE risk to mining rights 21.25% owned by black employees 18 Business Environment 19 Macro environment Slower growth: European economic woes continue China and India showing signs of slower growth USA – slow growth at best In South Africa: Increasingly exposed to a more uncertain China Internal growth dynamic is fragile Downgraded by credit agencies Government’s focus on infrastructure backlog will act as economic stimulus when implemented Excellent opportunities continue to present themselves 20 Trends in Afrimat’s markets Difficult time for aggregates business Western Cape slow and under pressure Diversification strategy has assisted Afrimat performance Strong increase in tender activity in most market segments Industrial markets stable, not as competitive as construction Action against incompetent government departments (e.g. Provincial roads to SANRAL) Strong pipeline, specifically government infrastructure (small to medium sized projects) Exciting opportunities 21 GDP by sector % y/y 20 15 10 5 0 -5 -10 -15 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Mining Manufacturing Construction Wholesale and retail trade Transport, storage and communication Finance, insurance and real estate Source: SARB, Standard Bank 22 Financial Overview 23 Financial highlights Revenue Operating profit 900,000 20,000 64 609 45,268 42,336 2010 2011 2012 75,623 40,000 65,521 506,717 455,874 15.4% 60,000 64,329 100,000 392,517 200,000 100,000 80,000 400,000 300,000 120,000 66,588 500,000 32.5% 671,349 600,000 398,622 700,000 385,499 800,000 489 420 140,000 0 2010 2011 2012 1st half 2nd half 2013 2013 1st half 2nd half 24 Segmental contributions to revenue 80% 71% 70% 67% 60% 50% Returning to previous levels 40% HY2011 HY2012 30% 17% 20% 19% 14% 12% 10% 0% Mining & Aggregates Readymix Concrete Products 25 Headline earnings per share HEPS for the six months 40.0 17.4% Cents per share 35.0 30.0 25.0 29.6 29.9 29.8 2009 2010 2011 35.0 24.5 20.0 15.0 10.0 5.0 2008 2012 26 Net cash from operating activities 100,000 86,860 90,000 80,000 64.8% 77,378 Rands 70,000 60,000 52,712 51,305 50,000 39,337 40,000 34,222 30,000 20,000 10,000 0 2007 2008 2009 2010 2011 2012 Net cash at end of period: R106.4m (2011: R63.7m) 27 Dividends Interim dividend Cents per share 9.0 8 8.0 7.0 7 6.0 6 6 6 2010 2011 2012 Afrimat remains a consistent dividend payer 5 5.0 4.0 2008 2009 2013 28 What differentiates us? Operating margin 13,2% vs. industry average 6,4% Strong financial position: Healthy cash flow Strong balance sheet Industry leading margins throughout economic cycle Active innovative strategic positioning: Good market intelligence and expertise Continuously identifying and evaluating opportunities Track record of successful acquisitions Successful greenfield projects Operational competence: Flexible Reliable quality supplier Superior reaction time 29 Risk mitigation Risk Mitigating action Slow delivery on Government infrastructure projects Widely diversified over markets, products and locations Construction companies under financial pressure No single dominant debtor, all less than 4% Macro-economic threats Constant strategic management (avoiding threats, exploiting opportunities) Actively seeking and exploiting opportunities Strict efficient credit control Entrepreneurial culture and creative innovative solutions Strong balance sheet Country risk in South Africa Seeking opportunities outside South Africa 30 What does the future hold? Prospects Short term outlook: Clinker group exciting Glen Douglas a real gem Remainder of the market conditions remain under pressure Integration of Infrasors acquisition Momentum drivers: Power stations Low cost housing Roads – SANRAL, provinces Renewable energy Industrial minerals Afrimat will pursue a conservative growth strategy preserving the status of the balance sheet 32 Take away Afrimat will pursue a conservative but strategic diversified growth strategy Preserve the status of the balance sheet Continue to deliver high cash conversion rates Final results due to be released during week of 6 May 2013 33 Q&A Thank you for your attendance and participation www.afrimat.co.za For any further Investor Relations questions please contact: Andries van Heerden (CEO): 021-917-8840 or Vanessa Rech (Keyter Rech Investor Solutions): 011-447-8656 34