budget - finishingschool

advertisement

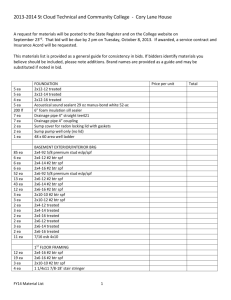

Scarcity leads to Innovation BUDGETING & Forecasting The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget is called budgeting. 2. The use of budgets to control an organization’s activity is known as budgetary control. Planning and Control Planning – involves developing objectives and preparing various budgets to achieve these objectives. Control – involves the steps taken by management that attempt to ensure the objectives are attained. Advantages of Budgets Budgets Goals and Objectives Advantages of Budgets Compels managers to think ahead Aids managers in coordinating their efforts Provides definite expectations that are the best framework to evaluate performance Advantages of Budgeting Define goal and objectives Communicate plans Think about and plan for the future Advantages Coordinate activities Means of allocating resources Uncover potential bottlenecks BMB Bhaag Milkha Bhag Case 31/2 years in Making. Innovations to enhance the audience base which led to increase in revenues and reduction in costs. Human Factors in Budgeting The success of budgeting depends upon three important factors: 1. 2. 3. Top management must be enthusiastic and committed to the budget process. Top management must not use the budget to pressure employees or blame them when something goes wrong. Highly achievable budget targets are usually preferred when managers are rewarded based on meeting budget targets. Budgeting Example Royal Company is preparing budgets for the quarter ending June 30. Budgeted sales for the next five months are: April 20,000 units May 50,000 units June 30,000 units July 25,000 units August 15,000 units. The selling price is $10 per unit. The Sales Budget The individual months of April, May, and June are summed to obtain the total projected sales in units and dollars for the quarter ended June 30th Sales Forecasting Step 1: Create the ROLL Out Plan Planning the Number of Doors/outlets Step 2: Find the Sales for each outlet A. On the basis of SPF for (EBO/LFRS): SPF= Sales /Area in square ft. 1) Find out the benchmark SPF ( Find for atleast two competitors and calculate average SPF) 2) Forecast Organization’s SPF in different scenarios. Sales Forecasting Different scenarios can be: Pessimistic Scenario: 10% to 30% of Benchmark SPF Normal Scenario: 40% to 70% of Benchmark SPF Optimistic Scenario: 80% to 100% of Benchmark SPF Sales Forecasting 3) Forecast Sales= SPF * Area Step 3: Cumulate the Sales of all the Outlets. Sales Forecasting B. On the basis of Quantities for (MBOs) 1) Find out the benchmark Quantity sold per month ( Find for atleast two competitors and calculate average quantities sold) 2) Forecast Organization’s Quantity sold in different scenarios. Sales Forecasting Different scenarios can be: Pessimistic Scenario: 10% to 30% of Quantity sold Normal Scenario: 40% to 70% of Quantity sold Optimistic Scenario: 80% to 100% of Quantity sold. Sales Forecasting 3) Forecast Sales= ASP * Quantity Sold. Step 3: Cumulate the Sales of all the Outlets. Computation of ASP Step 1 Identify key product categories Step 2 Decide the pricing of each category ( Competitive Benchmarking) Step 3 Indentify the Weightage of each category Computation of ASP Computation of ASP: Year 1 Key Product Categories/Business Verticals Q1 ( Say T-Shirts) Q2 ( Say Gift Items) Q3 ( Say Accessories) Q4 ( Say Bags) Weights Price 20% 40% 20% 20% 10000 15000 20000 5000 ASP= SUM of (W*P)= W*P 2000 6000 4000 1000 13000 Purchases Budget Budgeted purchases = Desired ending inventory +Sales– Beginning inventory