Shortage vs. Surplus

advertisement

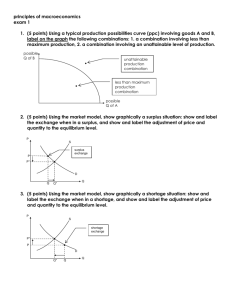

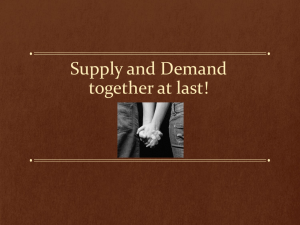

Shortage vs. Surplus Shortage vs. Surplus Let’s start with some basic concepts… • “A shortage exists at a market price when the quantity demanded exceeds the quantity supplied.” (i.e., excess demand) • “A surplus exists at a market price when the quantity supplied exceeds the quantity demanded.” (i.e., excess supply) (Dodge 62) Increase in Demand P S 17 2.79 Shortage D1 D q q1 Q Winter Blizzard! The price of rock salt “skyrockets” to $17/bag. Initial equilibrium price was $2.79/bag. “With the forecast of a blizzard, consumers expect a lack of future availability for” rock salt. Result = an increase in the demand for rock salt creating a shortage. Market cure = a higher equilibrium price $17/bag (Dodge 63) Decrease in Demand P Surplus S 18,000 p1 D D1 q1 q Q Recession caused a decrease in the demand for cars (a normal good) Manufacturers discounted sticker prices and offered a zero interest rate, along with other incentives. When the demand fell there was a surplus of cars at the original price. Market cure = lower the equilibrium price; resulting in fewer cars being purchased and sold. (Dodge 63) Remember! • “When demand increases, equilibrium price and quantity both increase.” P & Q • “When demand decreases, equilibrium price and quantity both decrease.” P & Q (Dodge 64) Increase in Supply P S “Advancement in computer technology and production methods” Increased the supply of laptop computers = surplus of laptops Market cure allow the price to fall = more demand. Surplus 4000 S1 p1 D q q1 Q (Dodge 64) Decrease in Supply P S p1 S1 20 D Shortage q q1 Q “Geopolitical conflict in the Middle East usually shows the production of crude oil.” A decrease “in the global supply of oil” = “a shortage of crude oil in the global market” Result = higher prices (Dodge 64) Remember! • When supply increases, equilibrium price decreases and quantity increases. P & Q • When supply decreases, equilibrium price increases and quantity decreases. P & Q Works Cited • Dodge, Eric R. “5 Steps to a 5 AP Microeconomics/ Macroeconomics”. New York, NY: McGraw-Hill. 2005.