2. Canadian Housing - Carson Dunlop Inspections

advertisement

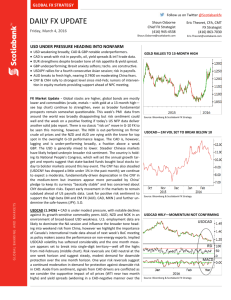

Canada’s Strained Housing Markets March 7, 2013 Derek Holt Vice-President, Scotiabank Economics Outline 1. Macro backdrop & the Bank of Canada 2. Canadian Housing: a) Strains b) Mitigating Factors c) Why It’s (Somewhat) Different From the United States d) Pockets Of Concern The Macro Backdrop – BoC On Hold Throughout 2013-14 Spare Capacity Will Prevent The BoC From Hiking Through 2013-14 Will Canadian Spare Capacity Narrow Or Widen? 3 2 1 % Scotia's Output Gap BoC's output gap post-GDP revision 0 -1 -2 -3 -4 Source: Bank of Canada, Statistics Canada, Scotia Economics. Even The BoC’s Output Gap Doesn’t Go Into Excess Demand By 2014 Canada’s Current CPI Softness Could Be Returning Us To The Past CDN CPI: Back To The 1990s? 8 CPI, y/y % change 7 6 US 5 Canada 4 3 2 1 0 -1 90 91 92 93 94 95 96 97 98 Source: Statistics Canada, BLS, Scotiabank Economics. 99 Among The World’s Best Corporate Balance Sheets Source: Statistics Canada, Quarterly Survey of Financial Statements, Scotia Economics 2. Canadian Housing a. The Strains Canada Is At A Cycle Top In Housing Home Ownership Rate 72 % 70 Australia 68 U.S. U.K. 66 Canada 64 62 60 1991 1996 2001 2006 2011e Source: Statistics Canada, Census of Population, U.S. Census Bureau, Housing Vacancy Survey, U.K. Office for National Statistics, Census of Population, Australian Bureau of Statistics, Census of Population and Housing. Canada Is At An Exhausted Point In The Consumer Cycle 115 Real consumer spending indexed to 2007Q1 = 100 110 Canada US 105 Euro zone 100 Japan U.K. 95 07 08 09 10 11 Source: OECD, Eurostat, UK National Statistics, Scotiabank Economics. 12 Canadian Renovation Spending At A Record High Canadian Renovation Spending 14 1.4 C$ bns, nsa, 4-quarter moving average % of personal disposable income, nsa, 4-quarter moving average 12 1.2 10 1.0 8 0.8 6 0.6 4 0.4 2 0.2 0 1971 0.0 1971 1979 1987 1995 2003 2011 Source: MLS, Statistics Canada, Scotiabank Economics. 1979 1987 1995 2003 2011 Sharply Cooling Canadian Housing Resale Markets Canadian Resale Transactions Edmonton Windsor St. Catharines % share of mkt, Jan 2013 volume of transactions, y/y % change, January 2013 4.6 1.5 0.6 Winnipeg 2.4 Saint John 0.3 Kitchener-Waterloo 1.5 Calgary* 6.7 St. John’s 0.9 Saskatoon 1.2 London 1.9 25 Major Markets 67.9 Canada 100.0 Hamilton 3.0 Quebec City 1.9 Sudbury 0.5 Ottawa 2.6 Durham Region 2.1 Halifax 1.3 Montreal 8.9 Thunder Bay 0.4 Toronto* 18.6 Victoria* 1.2 Regina 0.8 Vancouver* 5.8 -40 -30 -20 -10 0 10 20 Source: CREA, QFREB, Scotiabank Economics. *February data. Canadian House Prices In Early Decline Phase Canadian Home Prices Canadian Home Prices Thunder Bay Regina Halifax St. John’s Quebec City Saskatoon Calgary* Winnipeg Regina Calgary* Durham Region Edmonton Hamilton St. John’s Vancouver* Saskatoon Halifax London 25 Major Markets Montreal Sudbury Sudbury Ottawa 25 Major Markets Hamilton Toronto* Toronto* Canada Canada Edmonton Kitchener-Waterloo St. Catharines Victoria* Windsor Saint John Winnipeg Durham Region Victoria* London Kitchener-Waterloo St. Catharines Ottawa Vancouver* Saint John Thunder Bay y/y % change, January 2013 -10 -5 0 5 10 15 20 Source: CREA, QFREB, Scotiabank Economics. *February data. 25 Windsor 30 cumulative % change from December 1999 0 50 100 150 Source: CREA, Scotiabank Economics. *February data. 200 250 Home Price Indices – Repeat Sales Metric 240 Canada – Teranet National Bank House Price Index index:Jan 2000=100 220 200 180 160 140 US – Case-Shiller Home Price Index 120 100 00 03 06 09 12 Source: Teranet National Bank House Price Index, S&P/Case-Shiller Home Price Index, Scotiabank Economics. Canadians Have Higher Debt… But Stronger Balance Sheets Canadians’ Debt-To-Income Now Higher… … But Less Debt Used To Buy Assets 30 household credit liabilities as % of disposable income household debt as % of assets 160 US 145 US 26 130 22 115 Canada* 100 Canada* 18 85 70 1990 1995 2000 2005 2010 14 1990 1995 * Includes households, non-profits and unincorporated business. Source: U.S. Federal Reserve, Statistics Canada, Scotiabank Economics. 2000 2005 2010 Canada’s Debt Service Burden Is At An All-Time High Distorted by accounting change 30 25 Canada's Household Debt Service Burden interest payments on all debt + mortgage principal payments (% share of after-tax PDI) Total 20 Principal 15 10 Interest 5 0 1982Q1 1986Q1 1990Q1 1994Q1 1998Q1 2002Q1 2006Q1 2010Q1 Source: Bank of Canada, Statistics Canada, Scotiabank Economics. Source: Bank of Canada, Statistics Canada, Scotia Economics. No Leverage Apart From Household Debt? Think Again • Condos have driven all of the rise in housing starts for years… • …estimated 45-60% of Toronto of new condo sales over recent years have gone to investors not for primary occupancy…. • …5-15% down payments at sales office openings imply +/- 10 times gearing… • …then flip when the project goes live • Leveraged equity has been behind this Will Canadian Housing Starts Follow Sales Like They Did In The US? Housing Starts & Resales Declined Simultaneously in the U.S. 2.5 unit millions unit millions 8 7 2.0 6 Resales (RHS) 1.5 5 4 1.0 3 Housing Starts (LHS) 2 0.5 1 0.0 0 04 06 08 10 Source: U.S. Census Bureau, NAR, Scotiabank Economics. 12 Scenarios For Housing Starts Canadian Housing Starts 260 000s 240 forecast 220 History 200 Base Case 180 160 140 Risk 120 100 05 06 07 08 Source: CMHC, Scotiabank Economics. 09 10 11 12 13 Weakest Household Debt Growth Since The 1990s… Residential Mortgage Growth Household Credit Growth 18 20 %, 3-month moving average 18 16 14 %, 3-month moving average 16 y/y % change 12 14 y/y % change 12 10 10 8 8 6 6 4 2 m/m % change, seasonally adjusted 0 4 2 m/m % change, seasonally adjusted 0 90 92 94 96 98 00 02 04 06 08 10 12 Source: Bank of Canada, Scotiabank Economics. 90 92 94 96 98 00 02 04 06 08 10 12 Source: Bank of Canada, Scotiabank Economics. …Especially For Consumer Loans Consumer Loan Growth 20 15 %, 3-month moving average y/y % change 10 5 0 m/m % change, seasonally adjusted -5 90 92 94 96 98 00 02 04 06 08 10 12 Source: Bank of Canada, Scotiabank Economics. 2. Canadian Housing b. Mitigating Factors After Ottawa Eased The Most Since 1954 NHA and 1967 Bank Act… • 1999: Introduction of 5% down payment insured mortgage • 2003: Price ceiling on insured mortgages lifted • 2005: Introduction of insured mortgage with 30-year amortization period • 2006: Introduction of insured mortgage with 35-year & 40-year amortization periods • 2006: Introduction of 0% down payment insured mortgage …CDN Macroprudential Rules Clamped Down • After sharply easing mortgage lending standards in 2006-07, the federal government has since reversed its position • October 2008: Max 35 year amortization for insured mortgages; minimum 5% down for insured mortgages; consistent minimum credit score; new loan doc standards for property value and incomes • February 2010: Qualify at 5 yr posted rate instead of 3 yr; lower refi ceiling to 90% from 95%; min 20% down required to get mortgage insurance on non-owner occupied properties • January 2011: Max 30 year amortization for insured mortgages; refi ceiling for primary occupancy homes dropped to 85% from 90%; withdraw gov’t insurance on HELOCs • November 2011: Accounting changes to hold more on balance sheet • June 2012: Max 25 year amortization for insured mortgages; insurance dropped for mortgages on homes valued over $1 million (ie: now minimum 25% down); refinancing ceiling dropped to 80% from 85%; mortgage payments and total debt payments capped at 39% and 44% of income respectively. • 2012-13 Federal Budget: OSFI oversight of CMHC • Spring 2012: Insurance lifted from covered bonds, portfolio caps at the CMHC, new OSFI lending guidelines to banks • January 2014: Basel III A key difficulty lies in evaluating the opaque forms of non-rules-based tightening being applied through moral suasion by regulators to lenders and GSEs. Assessing Mortgage Rule Tightening Evaluating Amortization Compression $400 $362 Increase in Monthly Mortgage Payments, $ $350 $300 $250 $200 $166 $150 $100 $50 $0 40 down to 25 Source: Scotia Economics. 30 down to 25 Good Reasons For Rising High-Rise Housing Demand? Housing Starts 70 % share of total • Better affordability • Favourable demographics Single-detached 60 • Lifestyle choices 50 • More selection • Urban renewal / intensification 40 • Tight rental vacancy rates • Investor purchases 30 Apartment 20 10 00 02 04 06 Source: CMHC, Scotia Economics. 08 10 Canadians Have More Home Equity & More Real Estate in their Portfolio Canadians Have More Home Equity… 80 … and More Real Estate Assets 45 Real estate equity as % of real estate assets Real estate as % of total household assets Canada Canada 40 70 35 60 30 50 US US 25 40 20 30 1990 15 1995 2000 2005 2010 1990 1995 Includes households, non-profits and unincorporated business. Source: U.S. Federal Reserve, Statistics Canada, Scotiabank Economics. 2000 2005 2010 2. Canadian Housing - c. Why It’s (Somewhat) Different From The U.S. What Makes Canada’s Mortgage Market Different? • Explicit GSE guarantees – unlike the US GSEs • Strongly capitalized banks & captive dealers, far less shadow banking • Totally different funding model: deposit funding & large held-on-book component, versus reliance upon revolving door financing • Financial institutions less reliant upon short-term lines • No strategic defaults, outside of Alberta & Saskatchewan (and limited there) • Tougher bankruptcy rules • Less outsourcing of sales force in Canada • Generally more conservative products, but not entirely • No option ARMs in Canada, but entire book resets within 5 years • No mortgage interest deductibility (with exceptions) • Stricter underwriting criteria including independent appraisals & hair-cuts • Canada has already taken steps to tighten mortgage rules… • …and is pursuing further financial reforms (Basel III, OSFI oversight etc) Canadians Usually Don’t Default When House Prices Correct Large House Price Corrections Toronto 198995 Vancouver 1990-91 Vancouver 1995-96 0 Vancouver 2008 Mortgage Arrears During House Price Corrections Toronto 200809 0.7 peak to trough change in provincial mortgages in arrears, bps trough to peak in provincial mortgages in arrears, bps 0.6 0.5 -5 0.4 -10 0.3 -15 0.2 -20 0.1 -25 0.0 -30 % change Source: CREA MLS, Scotia Economics. Toronto 1989- Vancouver Vancouver Vancouver 95 1990-91 1995-96 2008 Source: Canadian Bankers Association, Scotia Economics. Toronto 200809 Canada has witnessed some big price corrections since the late 1980s that corresponded with big shifts in the macro environment, notably in Toronto and Vancouver, and yet each time mortgage arrears barely budged. Implication? Revenues are at greater risk than charge-offs. 2. Canadian Housing – d. Pockets Of Greater Concern Canadian Households More Heavily Leveraged Than Most Toronto Condo Construction: 97k Units on the Way 350,000 300,000 Under Construction Existing Condo Stock 250,000 200,000 150,000 100,000 50,000 0 Q1-05 Q1-06 Q1-07 Q1-08 Q1-09 Source: Urbanation, Scotiabank Economics Q1-10 Q1-11 Q1-12 Toronto Condo Investors Under Water Toronto Condos: Monthly Rent vs. Monthly Carrying Cost $2,000 Assumptions: • 20% mortgage down payment; • 25 year amorization in 2004-05, 30-year am. from 2006-Q2 2012, 25-year am. from Q3 2012 onwards; • Mortgage is fixed rate @ 3.5% from from 2009 onwards, 5% beforehand; • Property taxes = 1% of condo purchase costs; maintenance & condo fees = $250/month; • The 'shrinking new condo' starts at 650 Sq. Ft. in Q4 2004 and 'shrinks' 10 sq. ft. per year to reflect falling condo sizes; • The shrinking codo's cost = its size * Urbanation's average $PSF condo cost estimate. $1,800 $1,600 $1,400 $1,200 $1,000 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q1 Q2 Q3 Q4 2004 2005 2006 2007 2008 2009 2010 2011 2012 2012 2012 2012 700 Sq. Foot Condo (Resale) Carrying Cost Central Toronto 1-Bdrm Condo Rent 700 Sq. Foot Condo (New) Carrying Cost Sources: MLS, TREB, Urbanation Toronto’s Luxury Condos Adding To The Overhang Opening Date: January 2012 August 2012 Summer 2012 April 2011 • 25 storeys • 101 residences Trump International Hotel & Tower Shangri-La Toronto Four Seasons Private Residences (East & West Towers) Residences at the Ritz-Carlton • 65 storeys • 66 storeys • 55 storeys • 53 storeys • 118 residential units • 202 hotel rooms • 253 hotel rooms • 267 hotel suites • 261 hotel rooms • 287 residential units • 103 residences • 159 condo units Source: Andrew Barr/National Post, THERESIDENCESTORONTO.COM, TRUMPTORONTO.CA, SHANGRI-LATORONTO.COM, YORKVILLERESIDENCES.COM. Contacts Economics Derek Holt, Vice-President, Scotia Economics derek.holt@scotiabank.com Dov Zigler, Financial Markets Economist dov.zigler@scotiabank.com Disclaimer & Legal Notices This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor its affiliates accepts any liability whatsoever for any loss arising from any use of this report or its contents. Trademark of The Bank of Nova Scotia. Used under license, where applicable. Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including Scotia Capital Inc., Scotia Capital (USA) Inc., Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V., Scotiabank Colombia S.A., Scotiabank Brasil S.A. Banco Multiplo – all members of the Scotiabank Group and authorized users of the mark. The Bank of Nova Scotia is incorporated in Canada with limited liability. Scotia Capital Inc. is a Member of the Canadian Investor Protection Fund. Scotia Capital (USA) Inc. is a registered broker-dealer with the SEC and is a member of FINRA, the NYSE and SIPC. The Bank of Nova Scotia, Scotiabank Europe plc, and Scotia Capital Inc. are each authorized and regulated by the Financial Services Authority (FSA) in the U.K. Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities. TM The ScotiaMocatta trademark is used in association with the precious and base metals businesses of The Bank of Nova Scotia. The Scotia Waterous trademark is used in association with the oil and gas M&A advisory businesses of The Bank of Nova Scotia and some of its subsidiaries, including Scotia Waterous Inc., Scotia Waterous (USA) Inc., Scotia Waterous (UK) Limited and Scotia Capital Inc. - all members of the Scotiabank Group and authorized users of the mark.