Welfare Reform

Changes to Benefits

BT Benevolent Fund – June 2013

Presentation Outline

• To provide an overview of the Welfare

Reform Act and the proposed changes to the

Welfare Benefits system.

• To show a time line for the benefit changes

• To provide an overview of the criteria for the

new benefits.

Welfare Reform

Why The Change?

• Too complicated

• Too costly

• To provide the right incentives to get people

into work.

Aims of the Reform

• To provide a system that is fairer, more

affordable, and better able to tackle poverty.

• To create the right incentives to get more

people into work, whilst supporting those

who cannot.

• To be fair to both those claiming benefit, and

to the tax payer.

Current system

Contributory benefits (for

those who cannot work –

based on NI contributions)

Non-contributory benefits (for

specific circumstances –

“needs based”)

Means-tested benefits (for

those whose income is still

low)

Changes Already

Implemented

HOUSING BENEFIT

• LHA rates capped

• Bedroom allowances & removal of 5 bedroom

rate

• Rates set at 30th percentile – no longer 50th

• Removal of excess payment

• Non dependent deductions increased

• Extra bedroom for non resident carer

• Discretionary Housing Payments Budget

increased

• Age threshold for shared room rate raised to 35

Housing Benefit

One bedroom is allowed for:

• Every adult couple

• Any other adult aged 16 or over

• Any 2 children of the same sex under 16

• Any 2 children of either sex under 10

• Any other child

LHA RATES

LHA national weekly rates capped at:

-

£250 for 1-bed

£290 for 2-beds

£340 for 3-beds

£400 for 4-beds or more

(mainly affecting London)

Changes Implemented

continued

Tax Credits

• 50+ element removed from Working Tax

Credits (WTC)

• new applications and changes only

backdated for one month.

• a couple with at least one child must work

least 24 hours a week between them, with

one working at least 16 hours per week.

• Falls in income of up to £2500.00 will not be

re-assessed.

Changes Implemented

Employment & Support Allowance

• People in the work related activity group

who are on contribution based ESA will have

their benefit limited to one year.

• Those still on Incapacity Benefit to be moved

to ESA by 2014.

Income Support

• Lone parents with a child aged 5 and over

will be moved to JSA.

Welfare Reform Act –

Main Changes

• Child Benefit – taxable for high earners

from January 2013

• Benefit Cap – from April 2013

• Housing Benefit changes – April 2013

• Council Tax changes – April 2013

• Personal Independence Payments – from

April 2013

• Changes to Social Fund

• Universal Credit – from October 2013

January 2013

Child Benefit – from 7 January 2013

• Income tax charge to be applied to any taxpayer

who has an adjusted net income of over

£50,000, where they or their partner receives

Child Benefit.

• Rate of 1% of the child benefit for every £100 of

income between £50,000 and £60,000.

• For earnings above £60,000 the income tax

charge will be their total child benefit.

• People can decide to opt out of child benefit.

• Will be included in the “benefit cap” from April 13

and Universal Credit from October 13.

HB changes

From April 2013

• LHA rates reviewed and increased in line

with CPI, rather than actual rents

• Social tenants of working age will have HB

reduced:

– By 14% if they have 1 spare bedroom

– By 25% if they have 2 or more spare

bedrooms

Personal Independence

Payment

• Personal Independence Payment (PIP) will

replace DLA for eligible working age (16 –

64) claimants from 8 April 2013.

• Children under 16 will remain on DLA

• DLA recipients over 65 will not be migrated

onto PIP

• AA remains for all those over 65.

• No automatic transfer to PIP. Existing DLA

recipients will be invited to make a claim for

PIP – from October 2013. All on PIP by

2017.

• If PIP not awarded, DLA will cease.

Features of PIP

•

•

•

•

•

•

•

•

3 month qualifying period remains

New 9 month “forwards” test

Special rules for terminal illness remain

Remains non means tested and non taxable

Payable both in and out of work

Assesses individual needs

More consistent use of supporting evidence

Based on how a claimants condition affects

them, not on the actual condition

• Reviews at appropriate intervals – no

lifetime awards

Personal Independence

Payment

Made Up of Two Components:

• Daily Living Component

• Mobility Component

Awards will be made up of one or both

Components

Each component will have two rates:

• Standard

• Enhanced

PIP Criteria

The criteria DWP will use to assess people

against for PIP will:

• Assess disabled people as individuals

• Focus on the impact that their health

condition or impairment has on their daily

lives

• Consider the individual’s ability to carry out

key everyday activities

• Take account of physical, sensory, mental,

intellectual and cognitive impairments and

developmental needs

• Reflect variable and fluctuating conditions

PIP Criteria

They take into account whether activities can

be carried out:

• Reliably

• Repeatedly

• Safely, and

• In a timely manner

Areas of assessment

Daily living component

1. Preparing food and drink

2. Taking nutrition

3. Managing therapy or monitoring health conditions

4. Bathing and grooming

5. Managing toilet needs or incontinence

6. Dressing and undressing

7. Communicating

8. Engaging socially

9. Making financial decisions

Mobility Component

10. Planning and following a journey

11. Moving around

Scores required for benefit

• Daily living component payable if points

scored under activities 1-9

Standard rate = 8 points

Enhanced rate = 12 points

• Mobility component payable if points scored

under activities 10-11

Standard rate = 8 points

Enhanced rate = 12 points

Variable conditions

• If one descriptor in an activity applies for more than

50% of the time, then that descriptor should be

chosen.

• If more than one descriptor in an activity applies for

more than 50% of the time, then the descriptor

chosen should be the one which applies for the

greatest proportion of the time.

• Where one single descriptor in an activity is not

satisfied for more than 50% of the time, but a

number of different descriptors in that activity, when

added together, are satisfied for more than 50% of

the time, the descriptor satisfied for the highest

proportion of the time should be selected.

Claims for PIP

•

•

•

•

•

“Tell Story” form

Assessment of claim against descriptors

Medical evidence

Account taken of Aids

Most will have face to face meetings and can

be accompanied

• Health professional will provide evidence to

DWP decision maker

• No change for terminally ill

Benefit ‘cap’

From April 2013 income from means tested

benefits will be capped for some people.

The level of the cap will be:

•£500 a week for couples (with or without

children living with them)

•£500 a week for single parents whose

children live with them

•£350 a week for single adults who don’t have

children, or whose children don’t live with

them

Benefit ‘cap’

The cap will not apply where if anyone in the

household (excluding non – dependents):

• Is entitled to Working Tax Credit

• In receipt of IIB, DLA, AA or PIP

• In receipt of War widows/widowers

pensioners

• In receipt of the ESA support component

• Claimants who have been in employment

for at least 12 months before their job

ends (only for the first 39 weeks)

Benefits Included in the

Cap

•

•

•

•

•

•

•

•

•

•

•

•

•

Bereavement Allowance

Carers Allowance

Child Benefit

Child Tax Credit

Employment & Support Allowance

Guardian’s Allowance

Housing Benefit

Incapacity Benefit

Income Support

Jobseekers Allowance

Maternity Allowance

Severe Disablement Allowance

Widowed Parent’s Allowance

Benefit Cap

The following benefits are not included:

•

•

•

•

•

Council Tax benefit

Pension Credit

State Retirement Pension

Statutory Sick Pay

Statutory Maternity / Paternity/ Adoption

Pay

Benefit Cap

From April 2013, any excess deducted from

Housing Benefit

Options:

• Apply for discretionary housing payment

( £75 million allocated from 2013)

• Check benefits

• Consider trying to increase working hours

Likely Impact

•

•

•

•

•

•

•

•

•

•

56,000 households will be affected by the cap in 2013/14

The average benefit reduction is £93 a week per household

46% of households affected by the cap are in the social

rented sector

54% of households affected by the cap are in the private

rented sector

74% of households affected by the cap have 3 or more

children

28% of households affected by the cap have 5 or more

children

50% of households affected are lone parents

34% of households affected receive jobseekers allowance

25% of households are in receipt of ESA

39% of households are in receipt of Income Support

Council Tax Benefit

• Local Authority budget for C. Tax support cut by 10% in RBC this equates to £1.2 million.

•Local Authorities must decide on their own scheme of

Council Tax Support – must be in place by 31 Jan 2013

Money not ring fenced, but some principles apply:

• Local authorities will have a duty to run a scheme

of council tax support

• There should be no change to the current scheme

for pensioners

• Local authorities should consider support for other

vulnerable groups

• Local schemes should support work incentives

RBC Proposals

• Council Tax support to be based on 85% of

council tax bill, not 100%

• Working age claimants who have £3000.00

and over in savings will not be eligible for

any support in that tax year.

• Abolition of Second Adult Rebate scheme.

• Automatic switch to new scheme for those

already in receipt of CTB.

• No Backdating of benefit.

• Proposing discretionary hardship fund.

Social Fund

Current DISCRETIONARY system of:

• Community Care Grants

• Crisis Loans

• Budgeting Loans

No change to regulatory Payments, e.g. winter

fuel payments, cold weather payments,

maternity grants, funeral payments.

Social Fund

From April 2013:

• Community care Grants abolished from April

2013 – replaced by “local welfare assistance”

from Local Authority for emergency

situations.

• Crisis Loans abolished. Replaced by scheme

of short term advances – administered by

DWP.

• Budgeting Loans remain for those not on UC.

• From October 2013 – 2017 Budgeting Loans

will be replaced by payments in advance for

claimants on Universal credit.

Local Welfare Assistance

“The Government is committed to removing

burdens and controls from local government,

and so there will be no new statutory duty

requiring local authorities to deliver the

service. Local Authorities will have the

flexibility to design new locally based

support to meet local needs in the best way

that they see fit.”

Universal Credit

• National roll out from October 2013 for new

claimants

• A single benefit to top up income of working

age people ( whether in or out of work)

• From April 2014 all existing claimants start

to be transferred to UC

• All to be transferred by 2017

Universal Credit features

A single benefit to “top-up” income for people

of working age

Can be claimed whether working or not as long

as claimant is working age.

Claimants and partners must sign a “claimant

commitment”

Universal Credit

Will replace:

• Income Support

• Income Based JSA

• Income Based ESA

• Child Tax Credit

• Working Tax Credit

• Housing Benefit

DWP is now calling these “Legacy Benefits”

UC - Eligibility

•

•

•

•

•

Aged 18 or over (some exceptions)

Resident in Great Britain

Not in Education

Savings and Capital not more than £16,000.

Income not too high

Income rules

• Capital limit £16000

• Minimum assumed income for self-employed

• Generous earnings disregards:

– more of earnings are disregarded if

housing costs are low or if there is a

disability

– Only 65% of earnings after the disregard

are taken into account (incentive to work)

Work Related Conditions

• Most people will have to show that they are

taking steps to prepare themselves for work

Those exempt from work preparation:

• Those in Support Group of ESA

• Those with a child under the age of 1

• Those already earning the equivalent of a

full time job

• Those who are the victim of recent domestic

violence

How does it work?

Universal Credit includes set amounts for:

• Claimant and partner

• Children

• Housing costs

• Additional needs (e.g. disability/carer)

• Childcare costs (for working claimants)

If income is less than the total of the amounts calculated

for the above, then Universal Credit is payable

Transitional protection for existing claimants upon

migration

No changes to capital limits.

Universal Credit

Standard Allowances

Set allowances are given for:

• A standard rate for a single person or a couple

• An amount for each child

• An amount for each disabled child (2 rates)

• An amount for a sick or disabled adult (2 rates)

- limited capability for work

- limited capability for work related activity

• An amount for housing costs

• An amount if claimant or partner is a carer

• An amount for a carer

• An amount for childcare costs

The total of all appropriate allowances = claimants

potential maximum benefit.

Disability elements –

problems?

• Disability elements dependent on client

receiving ESA (adults) or DLA (children);

– WRAG or DLA low/mid for children £28.15

– SG or DLA high for children £77

• No enhanced disability premium

• No severe disability premium

• Cannot get carer premium and disability

premium together

Income

• If no income or capital, claimant will receive

maximum benefit (total of all applicable

allowances).

Income deducted from maximum benefit

• Earned income (less disregard)

• Income from an occupational pension is

deducted.

• Income from contributory benefits – C-ESA,

C-JSA, Incapacity Benefit, SSP, SMP etc

• Assumed income from savings

Earnings Disregards

• Minimum and maximum amounts of

earnings disregards

• Clients not receiving any housing costs in UC

will have the maximum disregard applied

• Clients receiving housing costs in UC will

have the maximum disregard reduced by

1.5x the amount of their housing costs

• No-one will get less than the minimum

earnings disregard

Earnings Disregards

Min

Max

Single person

No children

£13.46

£ 13.46

Couple no children

£36.92

£57.69

Lone Parent

£43.46+

£173.08

Disabled Person

£40.00

£134.62

Claimant Commitment

• Signed commitment outlining the steps

people must take when in receipt of the

benefit.

• Applies to partners as well claimant.

• Lists work related requirements whilst

receiving UC

• Sanctions for failure to comply

Claimant Commitment

4 Work related Requirements:

•

•

•

•

Work

Work

Work

Work

Focused Interview

Preparation

Search

Availability

Exemption from

Commitment

No work-related requirements

• People in support group

• Child under 1

• Carers

• Earning over 35 x NMW

• Recent victims of domestic violence

Sanctions

If conditions of claimant commitment not met:

• UC can be reduced

• Period of sanction can vary from 4 weeks to

3 years

• UC will be reduced by the amount of the

adult standard allowance

Can apply for a hardship payment

Claiming

Administered and paid MONTHLY by DWP

Payments to claimant

Claims made and managed online

Couples claim jointly

Extra components within UC in respect of

‘passported’ benefits

Pensioners on Pension

Credit

• Pension credit will remain outside UC

• Those on pension credit will receive a

Housing credit element in their benefit to

cover rent.

• Council Tax rebates will be awarded by Local

Authorities in line with their new strategy.

Overpayments

From 8 March 2012 – 6 year limitation rule does not

apply to recovery by deduction from benefit

From 8 May 2012 – Extension of admin penalties

From 1 July 2012? – Overpayments can be recovered by

deduction from earnings

From 1 October 2012 – A civil penalty (£50) for

‘negligent misrepresentation’ or ‘failure to provide

information’

From April 2013? – All overpayments of UC, JSA and

ESA to be recoverable. No right of appeal against

decision to recover

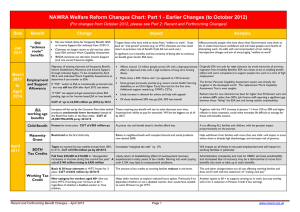

Govt estimates when Bill first

published as to savings

(in £millions)

Measure

2012/13

2013/14

2014/15

Lone parent conditionality

£70

£220

£300

HB restrictions social

sector

£0

£470

£470

Uprating LHA by CPI

£0

£40

£240

DLA reform to PIP

£0

£350

£1040

Benefit cap

£0

£220

£260

Time limiting ESA

£860

£1130

£1430

Abolishing ESA (youth)

£10

£10

£10

Other

£20

£60

£110

Total

£960

£2510

£3870