HEALTH INSURANCE MARKETPLACE & Medicaid transition

advertisement

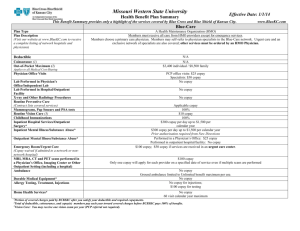

HEALTH INSURANCE MARKETPLACE & MEDICAID TRANSITION KEVIN R. HAYDEN Chief Executive Officer Group Health Cooperative of South Central Wisconsin CHANGING LANDSCAPE In 2014, there will be three main ways for Americans to get insurance coverage. Through: an employer (roughly 85% of Americans today) government programs (Medicaid/Medicare) the Health Insurance Marketplace (for individual consumers & small businesses) Individual Mandate & Expanded Coverage: everyone who can have insurance must have insurance or receive a tax penalty more opportunities for people to gain coverage The US House voted 219-212 to pass health care reform. Four votes the other way, and we wouldn’t be here today. IMPACT ON WISCONSIN Most Wisconsinites are insured through work: Employees of large group businesses (51+ full time workers) won’t see major changes in 2014 These employee plans must now cover preventive service at 100% (without a copay, deductible, etc.) Examples: screenings for blood pressure, colorectal cancer, depression, and others Remaining Wisconsinites face bigger changes: Changes to individual policy plans State didn’t accept funding for Medicaid expansion State didn't create a state-run exchange The Health Insurance Marketplace will be a new CURRENT WI COVERAGE Groups in bold face the most changes heading into 2014: Medicare 15% Uninsured 10% Medicaid (BadgerCare) 16% Individual 6% Employer 54% The actual universe of potential health insurance buyers in Wisconsin is at least 638,000. WISCONSIN CHANGES IN MEDICAID ELIGIBILITY CURRENT COVERAGE ELIGIBILITY BASED ON INCOME Pregnant Women Children Parents and Caretakers Childless Adults 0-100% FPL 100-200% FPL 200-250% FPL 250-300% FPL 300-400% FPL 400% + FPL Does Not Qualify for BadgerCare FUTURE COVERAGE ELIGIBILITY BASED ON INCOME Pregnant Women Children Parents and Caretakers Childless Adults 0-100% FPL 100-200% FPL 200-250% FPL Marketplace Eligible for tax credit and cost-sharing subsidies 250-300% FPL 300-400% FPL 400% + FPL Marketplace Eligible for tax credit subsidy Marketplace Not eligible for subsidies HEALTH INSURANCE MARKETPLACE 22 DAYS Until open enrollment! NOW OPEN For Enrollment! WELL, KIND OF… There are significant technical issues with the Marketplace website due to overwhelming demand. We anticipate these issues will be resolved in the coming weeks. In the meantime, there are other ways to access the Marketplace. MARKETPLACE GOALS Offer insurance coverage to individual consumers, folks transitioning off BadgerCare (92,000), and small group businesses Provide the best coverage at an affordable price Help qualifying individuals pay for coverage Guarantee Issue: prohibit insurance carriers from denying coverage to sick individuals. Create a competitive environment among health insurance companies to lower cost trends. Due to technical issues with the website, the Individual Mandate may be postponed by six weeks. WHAT WE KNOW TODAY Available online at healthcare.gov, by phone, and in-person. User keys in their personal information about household and income, then the website determines eligibility results. At this point: subsidies (financial help paying for coverage) is determined eligibility for Medicaid and other governmental programs is determined December 15, 2013: Deadline to enroll for coverage beginning January 1, 2014 The Marketplace website is comparable to online tax service, Turbo Tax. The user is guided through multiple steps to customize the shopping expereince. WHAT'S IN THE HEALTH INSURANCE MARKETPLACE? See our Health Insurance Marketplace handout for additional details. ESSENTIAL HEALTH BENEFITS METAL PLANS Monthly Premium Platinum 90% Gold 80% Silver 70% Bronze 60% Catastrophic Plan Out-of-Pocket Expense WHAT’S IN A PLAN? Platinum 90% Gold Difference between plans not based on benefit offerings; difference based on cost sharing between insurance company and consumer 80% Silver 70% Bronze 60% Catastrophic Plan Almost all plans offered in the Marketplace cover the 10 Essential Health Benefits Most plans have deductibles and may have office visit copays PLAN EXAMPLES Individual PLATINUM Plan Individual GOLD Plan Individual SILVER Plan Individual SILVER Plan without cost-sharing with cost-sharing Individual BRONZE Plan Deductibles $500 member $1000 family $1500 member $3000 family $2000 member $4000 family $0 $2000 member $4000 family Maximum Out-ofpocket $1500 member $3000 family $3000 member $6000 family $6350 member $12700 family $2115 member $4320 family $6350 member $12700 family Primary Care Visits $20 copay $30 copay $40 copay $40 copay $80 copay Specialty Care Visits $20 copay $60 copay $80 copay $80 copay $150 copay ER Visits $100 copay $500 copay $500 copay $0 copay $1000 copay $0 Tier 1 $30 Tier 2 $60 Tier 3 $100 Tier 4 $0 Tier 1 $40 Tier 2 $80 Tier 3 $150 Tier 4 $20 Tier 1 $40 Tier 2 $80 Tier 3 $150 Tier 4 $0 Tier 1 $40 Tier 2 $40 Tier 3 $40 Tier 4 $50 Tier 1 $120 Tier 2 $200 Tier 3 30% with Max of $300 Tier 4 Rx Please note these plans are for example only and are subject to change. SUBSIDIES Consumers can get financial help paying for insurance coverage in two ways: advanced premium tax credits • helps reduce monthly premiums • for individuals between 100-400% of FPL • examples: single person making approx. $46,000/year or a family of four making approx. $95,000/year cost-sharing reduction • helps pay out-of-pocket costs for: copays, deductibles, coinsurance, etc. • for individuals between 100-250% of FPL • examples: single person making approx. $29,000/year or a family of four making approx. $59,000/year Subsidies are only available through the Marketplace. An individual may qualify for one or both kinds of subsidies. HEALTH CONNECT In Dane County, individuals at 100-133% FPL are eligible to apply for: https://www.unitedwaydanecounty.org/healthconnect/ Financial assistance to help pay for insurance premiums with plans purchased through the Marketplace. PARTNERING FOR SUCCESS Success depends on insurance providers playing an active role Consumer education Consumer enrollment outreach Impetus for GHC Better Together Project A public service of Group Health Cooperative We’re on a mission to inform you about what health care reform means, without spin or politics The government will have to partner with health care systems throughout the country to make this program successful. Effective outreach and enrollment efforts are key.