Topic 8: Accounting for

Employee Benefits

Financial Accounting BFA201

BFA201_13

Readings & references

• Read Deegan Chapter 12

• AASB 119 Employee Benefits

BFA201_13

2

Learning Objectives

• Understand the various forms of benefits

employees can receive from employers

• Be able to account for the various forms

of employee benefits

• Understand whether particular employee

entitlement obligations should be

recorded at their nominal value or at their

discounted present value

• Be able to provide the necessary

disclosures in conformity with AASB 119

Employee Entitlements

3

Topics

1. Overview of employee benefits

2. Salaries and wages

3. Annual leave

4. Personal leave

5. Long service leave

BFA201_13

4

Overview of Employee Benefits

• AASB 119 - Purpose and Scope

• ‘Employee’ = a natural person appointed

under a contract of service

• ‘Employee benefits’:

– All forms of consideration given by an

entity in exchange for service rendered

by employees (para 7)

BFA201_13

5

Overview of Employee Benefits

Wages & salaries

Annual leave

Personal leave

Long service

leave

Superannuation

Share

entitlements

Bonuses

Other entitlements

BFA201_13

6

Regulation of employee

benefits

• National Employment Standards (NES)

sets minimum conditions. Individual

awards and agreements add extra.

• Annual leave accumulates, 4 wks per yr,

accumulates, vesting.

• Personal leave (includes carer’s leave,

sick leave) 10 days per yr, accumulates.

• Long service leave not specified – rely on

awards & agreements & State laws.

BFA201_13

7

AASB 119: Employee Benefits

.

Short term

benefits

Postemployment

benefits

Categories

Termination

benefits

BFA201_13

Other long-term

employee

benefits

8

Short term benefits: para 10

BFA201_13

9

.

Salaries and Wages

Payable after

12 months or

more

• Discount to

PV

Payable within • No need to

12 months

discount

• Only when

Liability arises

services

rendered

BFA201_13

Wages expense may

include:

* PAYG tax; medical

benefits

10

Salaries & wages

1. Entry at Reporting date

Dr

Salaries & wages expense

Cr

PAYG tax payable

Cr

Medical benefits payable

Cr

Salaries & wages payable

2. Entry when paid after Reporting date

Dr

Dr

Salaries & wages expense (incurred since reporting)

Salaries & wages payable (owing at reporting date)

Cr

PAYG tax payable

Cr

Medical benefits payable (since reporting date)

Cr

Cash (payment to employees)

3. Remittance to ATO & medical fund

Dr

Dr

PAYG tax payable

Medical benefits payable

Cr

Cash

11

See Handout

Lecture Example 1

BFA201_13

12

Example 1

Vege Ltd employs Iva Bean on a one-year contract

at an annual salary package of $52,000. Income tax

of $350 per week is deducted from Bean’s salary.

Vege Ltd also deducts $65 per week for health

insurance premiums payable to Medibank Private.

• What would the journal entry be each week to record

and pay Bean’s salary?

• What would the journal entry be when the amounts

collected on behalf of others are remitted?

• What would be the journal entry if on reporting date

four days wages are owing?

BFA201_13

13

Compensated absences para 11

Annual Leave

• Vacation

Personal (sick) Leave

• Short-term disability

Service

• Jury duty

• Military service

Parental Leave

• Maternity

• Paternity

BFA201_13

14

Compensated absences

2 categories

Nonaccumulating

entitlement

OR

Use it or lose it!

Recognise only when

the absence occurs

BFA201_13

Accumulating

entitlement – yr 3

year 2

year 1

Carry

forward

unused leave

15

Accumulating

compensated absences

2 Types

Vesting

BFA201_13

Non-vesting

16

Annual leave entitlement

4 weeks

Leave loading (17.5%)

If payable within 12

months – no PV calc

Expense & liability accrues DAILY

BFA201_13

17

Accounting for annual leave

•

To recognise annual leave obligation throughout

the year:

Dr

•

Annual leave expense

Cr

Provision for annual leave

When annual leave taken:

Dr

Provision for annual leave

Cr

PAYG tax payable

Cr

Cash at bank

BFA201_13

18

See Handout

Lecture Example 2

BFA201_13

19

Example 2

Iva Bean’s annual salary of $52,000 comes with an

entitlement to 4 weeks’ annual leave with a 17.5%

annual leave loading.

• What is the cost of the leave to Vege Ltd?

• What entry is required each non-leave week?

What is the entry required each week when Bean

is on leave?

BFA201_13

20

‘On-costs’

‘

Workers’

comp

Payroll tax

Superannuation contributions

BFA201_13

21

Example of Tasmanian on-costs

Total

18.72%

http://www.flinders.edu.au/hr-files/documents/TAS%20Oncosts%201-Jul-2013.pdf

BFA201_13

22

Accounting for personal leave

Accumulating:

• obligation arises as service is rendered

• Vesting: accrues daily (as per annual leave)

• Non-vesting: Only paid upon a valid claim for

personal leave by the employee

• Journal entry each week:

Dr Personal leave expense

Cr

Provision for personal leave

Provision should be based on past experience

23

Accounting for personal leave

• If employees are sick:

Dr Provision for personal leave

(wages during personal leave)

Dr Salaries and wages

(wages for rest of period)

Cr PAYG tax payable

Cr Cash at bank

BFA201_13

24

Question:

How does your employer

account for sick leave?

See Handout

Lecture Example 3

BFA201_13

25

Example 3

Vege Ltd has a weekly payroll of $70,000. A normal

working week is Monday to Friday. Its employees

are entitled to 10 working days’ non-vesting

personal leave each year. Experience suggests that

85% of its employees will take their full personal

leave entitlement each year.

• Calculate the annual personal leave expense and the

weekly amount of the expense.

• Show the journal entry required each week to account

for the personal leave.

• Show the journal entry if Iva Bean, who has a weekly

salary of $1,000, takes personal leave of two days.

BFA201_13

26

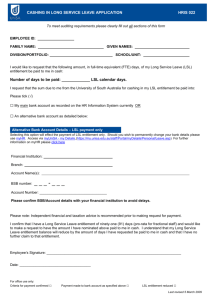

Long service leave

Extended leave after working for an

employer for a specific number of

years

Employer must recognise an expense

and an associated liability as LSL

accrues

Measured at its present value

BFA201_13

27

LSL entitlement categories

Pre-conditional

Conditional

No

entitlement

Entitlement Unconditional

under certain

circumstances Entitlement

Years of service

BFA201_13

28

Long service leave

• Many judgements required

• For example:

– probability employee will stay

until such time as they have a

LSL entitlement

– salary being earned at the time

of receiving the LSL entitlement

(inflation, promotion prospects

etc.)

BFA201_13

29

Accounting standards for LSL

• AASB119 (para 128) requires the

recognition of a liability for LSL to equal

the net total of:

– The present value of the defined benefit

obligation at the reporting date

– Minus the fair value at the reporting date of

plan assets (if any) out of which the

obligations are to be settled directly

BFA201_13

30

Calculating LSL liability:

need to calculate…

Projected

salary

current

salary ×

(1 + inflation

rate)n

BFA201_13

A

c

c

u

m

u

l

a

t

e

d

L

S

L

b

e

n

e

f

i

t

Present

value of

LSL

obligation

Probability

LSL

benefit will

be paid

LSL

liability

= TOTAL to be shown on financial position statement

Calculating LSL liability

– Projected salary

• current salary × (1 + inflation rate)n

– Accumulated LSL benefit

• Projected salary multiplied by

• Years worked / total years to be served before leave

can be taken multiplied by

• weeks of LSL entitlement / 52

– Present value of LSL obligation

• accumulated LSL benefit/(1 + appropriate bond rate)n

– Probability that LSL will be paid (experience

based)

– LSL liability = PV of LSL obligation x probability

BFA201_13

32

Appropriate bond rate

PV calculated by discounting the liability

using extrapolated yields on Fixed Rate

Commonwealth bonds with maturities

matching the term to settlement (rates

available on the Reserve Bank website

http://www.rba.gov.au/finservices/index.html under the Small

Investor Bond Facility – Quarterly Bond

Prices, CGS Valuation – Bond Prices, for

valuation purposes).

BFA201_13

33

BFA201_13

34

Accounting entries for LSL

• Entry to recognise the LSL expense:

Dr

Long service leave expense

Cr

Provision for long service leave

NOTE:

LSL liability = Balance required in provision

account;

Expense = Difference between existing balance

& required balance

– provision broken up into current and non-current

portion

Entry when LSL is subsequently taken:

Dr

Provision for long service leave

Cr

Cash at bank

BFA201_13

35

See Handout

Lecture Example 4

BFA201_13

36

Example 4

Inflation rate is 2% and wages are expected to keep

pace with inflation. The interest rate on bonds on

with 2 & 6 yrs to maturity is 6%. 13 wks LSL for

15 yrs service, 10 yrs pro-rata.

37

Calculating projected

salaries

BFA201_13

38

Calculating accumulated

LSL benefit

BFA201_13

Calculating LSL liability

Total

LSL expense 80 288

Provisions for LSL

BFA201_13

80 288

80 288

40

Next Week

Week 9 - Accounting for Income Taxes

Copyright notice

© Copyright University of Tasmania, School of Accounting & Corporate

Governance

All rights reserved.

Commonwealth of Australia Copyright Regulations 1969 - WARNING

This material has been reproduced and communicated to you by or on behalf of the University

of Tasmania pursuant to Part VB of the Copyright Act 1968 (the Act). The material in this

communication may be subject to copyright under the Act. Any further reproduction or

communication of this material by you may be the subject of copyright protection under the Act.

Do not remove this notice.

BFA201_13

41