tio

to valua

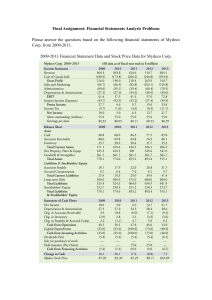

FIN 5203 Notes

Valuing Stocks with Multiples

Textbook Chapter 9, Section 4

↓

similaestate

r

1. Core Idea: Analogy from Home Valuation

• In real estate, one of the most common metrics to use is price per square foot:

Home Price ->

Price per Sq. Foot =

Square Feet

• The ratios are averaged from a bunch of homes near each other and then the average (or median) is

used to estimate the value of another house.

• So, if homes in the area average about $176.67 per square foot and I find an unpriced 1,500 square

foot home, then I estimate it is worth $176.67 ⋅ 1,500 = $265,005.

ellingpresen

-

if the entire mkt is misplaced,this

method wont find of

2. The Original Multiple: Price-to-Earnings

• There are many different firm characteristics that are used in ratios (e.g., value-to-number of

subscribers, value-to-number of scientists employed at a startup).

• Some ratios involve Enterprise Value and earnings before interest and taxes, for example: EV-toRevenue, EV-to-EBITDA, and EV-to-EBIT.

• Other ratios use equity-specific characteristics such as earnings per share (EPS) and book equity per

share.

• By far the oldest and most popular ratio is the price-to-earnings or P/E ratio, which is price per share

divided by EPS, or earnings per share (= Net Income / Shares Outstanding)

• Detail: We often use “diluted” EPS, to reflect the fact that insiders own options that can (and will

eventually) be exercises to create additional shares.

s

.

3. Lots of Options for What Earnings to Use futurearnings

•

•

•

•

•

Analysisfor comparabee

We think of prices as forward-looking, i.e., they reflect what is coming in the future (not the past). ①industry

princtivita

For mid-size to large public firms, forecasted earnings are available from public sources, such as

③

Yahoo! Finance.

↳

implicit

the

When you use a forecasted EPS to calculate P/E, we call that a forward P/E ratio.

Another way to calculate P/E is to use the most recent twelve months (trailing twelve months or

&

“TTM”) EPS. This is called a trailing P/E ratio.

Analysts often adjust EPS (forward or trailing) to remove any one-time or unusual items.

S

②geography

Example 1: Using a P/E Ratio

Suppose a firm as trailing twelve month EPS of $3.50 and forecasted EPS of $4.00. You average similar

firms to find that their trailing P/E is 15 and forward P/E is 17. Use this data to value the firm’s stock

(you’ll get two estimates).

Trailing Price to Earnings = 15

Trailing EPS = $3.50

Value of Stock = 15 ⋅ 3.50 = $52.50

Page 1

theres an

summeverythin

Forward Price to Earnings = 17

Forward EPS = $4.00

Value of Stock = 17 ⋅ 4.00 = $68.00

hunters. "

4. Two Basic Philosophies: Value vs. Growth"bargain

1. Value Investing learnings for the cheapest price. )

• Searches for low P/E stocks on the idea that the market may be undervaluing a firm.

• Very Simplified Thought Process: “Earnings are earnings, so I want the earnings for the cheapest

price possible”

• Low P/Es are good.

2. Growth Inves�ng

• Searches for high P/E stocks with the idea that the market is signaling future growth.

• Very Simplified Thought Process: “If the market is paying 100 times that stock’s earnings, it

must mean that the firm’s earnings are expected to grow at a really high rate.” (more faith in the market)

• High P/Es are good.

.

•

For much of the 20th century, value stocks (low P/Es) earned higher returns than growth stocks, but

that relationship has reversed in recent years.

5. Using Theory to Go Beyond the Growth vs. Value Debate

• Think back to our old friend: the growing perpetuity model. Apply it to a dividend-paying stock.

𝑃𝑃 =

•

𝐷𝐷1

𝑟𝑟𝐸𝐸 − 𝑔𝑔

𝐷𝐷1 /𝐸𝐸1 Dividend Payout Ratio

𝑃𝑃

=

=

𝑟𝑟𝐸𝐸 − 𝑔𝑔

𝐸𝐸1 𝑟𝑟𝐸𝐸 − 𝑔𝑔

•

•

divicle

Now, construct the forward P/E ratio by dividing by forecasted earnings 𝐸𝐸1 .

E

sides

botherning

.

yearscastings

The “Dividend Payout Ratio” is simply what percentage of a firm’s earnings it pays out in dividends.

How would each piece affect the ratio individually, holding the other parts constant?

o Dividend Payout Ratio: as this ratio goes up, what happens to P/E? (P/E goes up)

o Risk (Required Rate of Return on Equity): as this goes up, what happens to P/E? (P/E goes

down)

o Growth (Growth Rate of Dividends per Share): as this goes up, what happens to P/E? (P/E goes

up)

higherationusingherErato

6. Using Enterprise Value Multiples

• Enterprise Value multiples are less affected by the capital structure of the firms (i.e., comparing

firms with different amounts of debt).

• Enterprise Value measures the business activity (i.e., the “enterprise”) of a firm, ignoring unused

cash that the firm might have.

• Example: Dry Cleaners with a billion dollars in the bank

Value of Firm = Total Equity + Total Debt

Enterprise Value = Total Equity + Total Debt − Excess Cash

Enterprise Value = Value of Firm − Excess Cash

Page 2

•

•

•

•

When we discount the Free Cash Flows using the appropriate discount rate (the Weighted-Average

Cost of Capital (WACC)), we get the Enterprise Value, e.g.,

𝐹𝐹𝐹𝐹𝐹𝐹1

𝐸𝐸𝐸𝐸 =

𝑊𝑊𝑊𝑊𝐹𝐹𝐹𝐹 − 𝑔𝑔

where 𝑔𝑔 is now the growth of FCF (not growth of dividends)

We typically use EBITDA, EBIT, or even Revenue as the numerator in Enterprise Value multiples.

One Drawback: It’s often harder to find analyst forecasts of those numbers.

The same “levers” still are true, holding the other parts constant:

𝐹𝐹𝐹𝐹𝐹𝐹1 /𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐷𝐷𝑊𝑊1

𝐸𝐸𝐸𝐸/𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐷𝐷𝑊𝑊 =

𝑊𝑊𝑊𝑊𝐹𝐹𝐹𝐹 − 𝑔𝑔

o Higher FCF as a % of EBITDA: Higher EV/EBITDA

o Higher Risk (meaning higher WACC): Lower EV/EBITDA

o Higher Growth: Higher EV/EBITDA

Example 2: Using an Enterprise Value Multiple

Suppose a firm has forward EBITDA of $120,000. The firm has 10,000 shares outstanding and

$500,000 of debt. The firm also has $150,000 of excess cash. You average similar firms to find that the

typical forward EV/EBITDA multiple is 8.5. Using that multiple, estimate the price-per-share of the

stock.

Forward EBITDA = 120000

Forward EV to EBITDA Multiple = 8.5

Estimated EV = 120000 ⋅ 8.5 = 1,020,000

Equity Value = EV + Excess Cash − Total Debt

= 1,020,000 + 150,000 − 500,000 = 670,000

Equity Price Per Share =

7.

•

1.

2.

3.

670000

= $67.00

10,000

Pros and Cons of Multiples Valuation

Pros (simple using the MK+ to value.

No need to specify a complicated model or estimate rates of return. Just find similar firms.

Uses market participants’ forecasts and valuations, which are very good in an efficient market.

Harder to manipulate, for example, by using unrealistic inputs or an overly complicated model.

,

• Cons Completely useless if you have no comparable firms)

1. Only as good as the firms are comparable. Can often give very bad results if comparing dissimilar

firms.

2. Relies heavily on the market being efficient (you’re using one market valuation to estimate another).

3. More difficult to do sensitivity analysis. In a detailed cash flow forecast, you can adjust profit

margins, growth rates, etc. to see impact on value.

Page 3

0

0