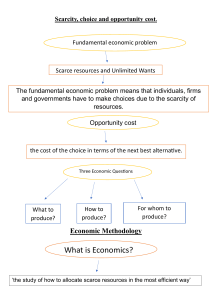

AP Microeconomics Unit Overview: What is Economics? Focus Sheets Page 1 of 6 Introduction to Economics Economics is the study of human behavior constrained by scarcity. It's not a field of business. Economics is used to predict how peoplebusiness owners and consumers behave when faced with scarcity. So, what is scarcity? We have scarcity because the world doesn't have enough resources, or "stuff," to make all the things people want. Scarcity means we have to make decisions. There are two broad types of economics: Microeconomics and Macroeconomics. • Microeconomics looks at individual behavior, or the "small picture." • Macroeconomics looks at the economy as a whole, or the "big picture." Resources are also called factors of production or inputs, because we use resources to create goods and services. Most economists divide resources into three categories: land, labor, and capital. • Land includes all the natural resources that come from the earth. • Labor includes all human effort, physical and mental. • Many people think of money when they hear the term capital. But in economics capital isn't money. It's all the machinery, equipment, buildings, and human skills used to manage and produce goods and services. Keep in mind that economists divide capital into two types: physical capital and human capital. • • Physical capital includes machinery, buildings, and equipment. • Human capital includes the knowledge and skill used to make goods and services, but not natural ability. For example, it includes the skills a ballet dancer developed through lessons, but it doesn't include the dancer's natural athletic talent. Some economists use a fourth category of resources: entrepreneurship. Entrepreneurs are people who come up with new ways of using the other resources to produce goods or services. They are the "risk takers." The United States and many other countries use an economic system called a market system to distribute goods and services. In a market system, the price of a good or service depends on its scarcity. Items with high prices are generally more scarce, and items with low prices are generally less scarce. The scarcity of a good or service depends on two things: availability and value. Scarcity can change if the availability of resources changes or if people's wantshow much they value an itemchange. The price of an item doesn't tell us how much people value an item. Some goods are called "free goods." When the amount of a good available exceeds the amount that people want, it's a free good. It has a zero price. ___________________ Copyright © 2021 Apex Learning. See Terms of Use for further information. AP Microeconomics Unit Overview: What is Economics? Focus Sheets Page 2 of 6 The economist's definition of a market is "a place where buyers and sellers exchange goods or services for a price they agree on." For economists, a market exists whenever and wherever an exchange takes place. Markets fall into two large categories: factor markets and product markets. Resources and semi-finished products are exchanged in the factor market. It's also called the resource market. Goods and services are exchanged in the product market. In the factor market, resource owners receive rent for their land, wages for their labor, and interest for their capital. These are the prices for each factor. In the product market, sellers receive the selling price for goods and services. Generally, sellers (or producers) take these factors of production and make something (it can be a good or service) then sell it to a buyer (or consumer) in a product market. Hopefully, the price the buyer pays is more than the cost to the seller in making the product. The difference between the price a seller receives and the cost a seller faces is profit. Profit is the total revenue of sales received minus the total cost of the resources used. The combined economic activity in factor and product markets is known as the circular flow of economic activity. Resource owners sell their resources to business owners in the factor market. In exchange they get rent, wages, or interest. The business owners then use the resources they bought to make goods or services. Finally, they sell these goods and services in the product market, to the resource owners. ___________________ Copyright © 2021 Apex Learning. See Terms of Use for further information. AP Microeconomics Unit Overview: What is Economics? Focus Sheets Page 3 of 6 Economic Tools: Graphs and Equations There are three main types of graphs: Pie Chart Line Graph Bar Chart Shows differences in relative size • Illustrates the statistical relationship between variables • Demand and Supply curves are line graphs • Shows trends over time (also called a time series graph) • Lets the reader quickly assess changes in a variable, such as inflation, over time. • Convenient when comparing different values of a single variable • Unemployment rates for each state are well represented on a bar chart. • Can also be used to compare the values of a single variable over time. You'll use line graphs most often in this course. The line graph called the supply curve helps economists study supply, whereas the line graph called the demand curve helps economists study demand. Price Independent Variable S (Supply) D (Demand) Quantity Dependent Variable A supply curve is a direct relationship between price and quantity. This means the variables both move in the same way. So, when price goes up, quantity supplied goes up. And when price goes down, quantity supplied goes down. A demand curve is an indirect relationship between price and quantity. This means the variables move in the opposite way. So, when price goes up, quantity supplied goes down. And when price goes down, quantity supplied goes up. Price is the independent variable, and quantity supplied is the dependent variable. It means that the dependent variable reacts to or is responsive to the independent variable. ___________________ Copyright © 2021 Apex Learning. See Terms of Use for further information. AP Microeconomics Unit Overview: What is Economics? Focus Sheets Page 4 of 6 Be aware that in economics, unlike in other disciplines, price is always on the vertical axis, whether it's independent or dependent. The vertical intercept is where the line graph intercepts the vertical axis. Another way to say it is the vertical intercept is the value of the independent variable when the dependent variable is 0. The slope is the rise over the run and tells us how much the variable on the y-axis changes for some change in the value of the variable on the x-axis. More precisely, the slope equals the change in the y-axis divided by the change in the x-axis. A positive slope shows direct relationship between the variables, so our supply curve has a positive slope. A negative slope shows an indirect relationship between the variables, so our demand curve has a negative slope. There are two methods of calculating specific numbers in a problem. If we use the supply curve as an example you'll see that the two methods to determine the quantity supplied at a certain price level are: • • to use an equation; or to draw a line from the price level over to the supply curve, and then down from there to the quantity axis. Example: First we calculate the slope. As you can see from the graph below, the rise or change in the y-axis or price variable is $1 ($2 - $1 = $1) and the run or the change in the x-axis or quantity variable is 2 units (4 units 2 units = 2 units). Therefore the slope of this supply curve is the rise/run or ½. So this means there's a $2 change in the quantity when there's a $1 change in the price. Therefore, given this slope, the equations to determine the price and quantity are: P= ½ Q or Q = 2P, where Q is quantity and P is price. Price S (Supply) Independent Variable $2 $1 D (Demand) 2 4 Quantity Dependent Variable ___________________ Copyright © 2021 Apex Learning. See Terms of Use for further information. AP Microeconomics Unit Overview: What is Economics? Focus Sheets Page 5 of 6 You can use the above graph to determine quantity by drawing a line from the price over to the supply curve and then down to the quantity axis. You can see when you do this that when price is $2, producers are willing to supply 4 units of a good. If you use the equation instead, you would obtain the same result because Q=2(2)=4 units. Economic Systems No economic system can satisfy all the wants of all its members. Remember the concept of scarcity? Societies develop economic rules and institutions to choose which wants get satisfied. Because of their different value systems, different societies distribute goods and services among people differently. All economies are designed to answer three fundamental questions: • What goods and services will be produced? • How will those goods and services be produced? • Who will get those goods and services? In every economic system the answers to these questions determine the production and allocation of resources, goods, and services. There are three principal types of economiestraditional, command, and market: • In a traditional economy, decisions are based on the decisions, customs, or religious practices of ancestors. Traditional economies were common in the past, and we can still find them in some parts of the world. • Command economies are centrally planned. The country's resources and means of production are publicly owned, and government officials make the economic decisions. • In market economies buyers and sellers use prices as a medium to exchange goods in free markets. In other words, price is used to indicate the value that buyers and sellers place on goods and services in unregulated markets. In a pure-market economy, people act in their own best interest, producing whatever gives them the most profit, buying whatever gives them the most satisfaction. ⇒ In his 1776 book Wealth of Nations, Adam Smith claimed that the market economy structure was the best market structure. His book still serves as a "blueprint" for pure market economies. In a pure-market economy, government stays out of the economy, letting producers and consumers do what they want. Smith wrote about an "invisible hand," defined as the forces of a free-market economy. He claimed that when people within a free market economy act in their own self-interest, the overall effect directs resources to where they produce the greatest benefit for all. It's just as if an "invisible hand" guided them. ___________________ Copyright © 2021 Apex Learning. See Terms of Use for further information. AP Microeconomics Unit Overview: What is Economics? Focus Sheets Page 6 of 6 Here's how the three principal types of economies address the three fundamental questions noted above: Type of Economy Economic Question Market Command Traditional 1. What goods and services will be produced? Determined by market. Determined by government. Determined by society's traditions and values. 2. How will those goods and services be produced? Determined by producers. Determined by government. Varies. 3. Who will get those goods and services? Whoever can pay for them. Determined by government. Varies. Most modern economic systems (including the United States economy) are mixed economies; that is, they're somewhere in between these three market structures. • For example, the U.S. economy is based on the idea of a market economy. It promotes the ideas of capitalism and free markets, and most of the means of production are privately owned. It also includes aspects of both command and traditional economies (i.e., the U.S. Postal Service and the custom of tipping). Government regulation of private businesses is another command element in the U.S. economy. Most economic systems try to achieve the same four economic goals: • People want to use their resources as efficiently as possible. When people try to satisfy their unlimited wants with scarce resources, they don't want to waste those resources. • People want to maintain stable price levels for goods and services. People want stable prices because it's much easier to make decisions if they have a good idea of what prices will be in the future. The most common form of price instability is inflation. Inflation is an increase in prices over time. • People want to have full employment. Societies want full employment because when people have jobs they add to the productivity of the economy. On the other hand, when they don't have jobs they detract from the economy's productivity. • People want growth. Economists usually measure economic growth by the increase in the value of goods and services an economy produces. ___________________ Copyright © 2021 Apex Learning. See Terms of Use for further information.