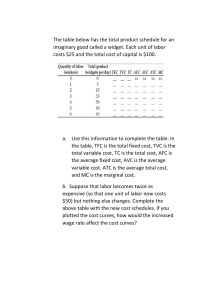

ECO Assignment 4 Wednesday, 27 November 2024 11:16 AM 1 a. B. It exhibit diminishing returns to labor because any additional amount of workers result to a decrease in the number of output which is the number of chairs. This is seen from the decrease of MPL from 10 to -3. C. The marginal product of labor become negative because the extra number of worker is making the production of chairs inefficient as the workplace may be too small to accommodate more than 5 worker which hinder the production rather than help. 2a. Flight Time Average cost per passenger 7 AM $50,000 / 240 = $208.33 10 AM $50,000 / 120 = $416.67 1 PM $50,000 / 120 = $416.67 4 PM $50,000 / 240 = $208.33 B. As a newly hired marketing consultant, I would focus on attracting off-peak customers as the flights are only half full which mean there is still space to increase revenue and sales while the rush-hour flights are fully filled. I would recommend the airline to provide a promotional activity by lowering the price of the airline ticket to increase sales as consumer’s willingness to pay for the off-peak flights might be in the lower range compared to the rush-hours. 3a. Total cost = Fixed cost + Variable costs TC = 300 + 55(q) TC = 300 + 55 (0) TC = 300 The fixed cost is $300,000 B. TC = 300 + 55(100) TC = 300 + 5500 AVC = VC / q AVC = 5500 / 100 AVC = 55 (thousand dollar per thousand units) C. MC = 55(100) - 55(99) / 100-99 = 55 Marginal cost of production at 100 thousand units is 55 (thousand dollar per thousand units) D. AFC = FC / q AFC = 300,000 / 100,000 AFC = 3 (thousand dollar per thousand units) E. TC = 350 + 45(q) + 3(i) 4a. 5a. Fixed cost = $50 Variable cost = $0.5q^2 B. Average total cost = Total cost / Quantity C. Average total curve is at its minimum when quantity is at 10. The marginal cost is 10 and the average total cost is also 10. D. QS = p|p≥10 E. QS = 9P F. G. H. In the short run, there is incentive for forms to enter since profit is bigger than zero. However, in the long run, profit will return to zero since supply increases due to firms entering the market. I. In the long run, profit always equal to zero J. 6a. Qd = Qs B. I would expect to see entry into the industry because TR > TC which shows economic profit. This shows that it gives an incentive for firm to enter. The effect is it will shift short run supply curve to the right, decrease price and minimize profit. Eventually, it will lead to zero economic profit and slow down incentive for firms to enter. C. P=ATC ATC=MC D. P=AVC The lowest price the firm would sell its output is at 0.005 because it is the shutdown price, firm will keep on producing as long as price is bigger or equal to the average variable cost. Therefore at that price, firm is experiencing a negative of 722 in profit. 7a. B. The price ceiling imposed by the government reduces the degree of monopoly from 29.4% to 14.3%. This regulation increases output and lower prices paid by the consumer which improves consumer welfare due to increased consumer surplus and quantity supplied to the market. But this limits monopolists’s ability to exploit its market power. C. The price ceiling that will lead to the largest level of output is when price is equal to ac which is at $ 8a. B.