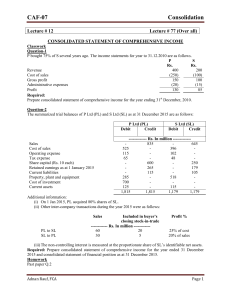

Group Statements Vol 1: Consolidated Financial Statements Textbook

advertisement