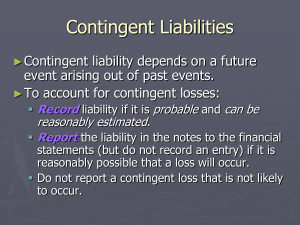

12 Provisions and contingencies

12.1

12.2

Identify, by indicating the relevant box in the table below, whether each of the following

statements about provisions and contingencies is true or false.

A company should disclose details of the change in

carrying amount of a provision from the beginning to

TRUE

FALSE

the end of the year.

Contingent assets must be recognised in the financial

statements in accordance with the prudence concept.

TRUE

FALSE

Contingent liabilities must be treated as actual liabilities

and provided for if it is probable that they will arise.

TRUE

FALSE

Which of the following statements about contingent assets and contingent liabilities are

correct?

A contingent asset should be disclosed by note if an inflow of economic benefits is

probable.

(2) A contingent liability should be disclosed by note if it is probable that a transfer of

economic benefits to settle it will be required, with no provision being made.

(3) No disclosure is required for a contingent liability if it is not probable that a transfer of

economic benefits to settle it will be required.

(14) No disclosure is required for either a contingent liability or a contingent asset if the

likelihood of a payment or receipt is remote.

1 and 4 only

2 and 3 only

2, 3 and 4

1, 2 and 4

12.3 A former director of Biss Co has commenced an action against the company claiming

substantial damages for wrongful dismissal. The company's solicitors have advised that the

former director is unlikely to succeed with his claim, although the chance of Biss Co

paying any monies to the ex-director is not remote. The solicitors' estimates of Biss Co's

potential liabilities are:

Legal costs (to be incurred whether the claim is successful or not)

Settlement of claim if successful

50,000

500,000

550,000

According to IAS 37 Provisions, Contingent Liabilities and Contingent Assets, how should this

claim be treated in Bliss Co's financial statements?

Provision of $550,000

Disclose a contingent liability of $550,000

Disclose a provision of $50,000 and a contingent liability of $500,000

Provision for $500,000 and a contingent liability of $50,000

BPP

Questions

69

12.1* Identify, by indicating the relevant box in the table below, the correct action to be taken in

the financial statements in respect of each item.

The company gives

warranties

on

its

products at no extra

cost to the customer.

CREATE A

DISCLOSURE

The

company's

NO ACTION

PROVISION

NOTE

ONLY

statistics show that

about 5% of sales give

rise to a warranty

claim.

The

company

has

guaranteed the overdraft

of another company. The

CREATE A

DISCLOSURE

likelihood of a liability

NO ACTION

PROVISION

NOTE ONLY

arising

under

the

guarantee is assessed as

possible.

12.5 Which of the following statements about the requirements of IAS 37 Provisions, Contingent

Liabilities and Contingent Assets are correct?

A contingent asset should be disclosed by note if an inflow of economic benefits is

probable.

(2) No disclosure of a contingent liability is required if the possibility of a transfer of

economic benefits arising is remote.

(3) Contingent assets must not be recognised in financial statements unless an inflow of

economic benefits is virtually certain to arise.

O All three statements are correct

O 1 and 2 only

O 1 and 3 only

O 2 and 3 only

12.6 Wanda Co allows customers to return faulty goods within 11+ days of purchase. At 30

November 20X5 a provision of $6,548 was made for a refund liability (sales returns). At 30

November 20X6 the provision was re-calculated and should now be $7,634.

What should be reported in Wanda Co's statement of profit or loss for the year to 31

October 20X6 in respect of the provision?

O A charge of $7,634

O A credit of $7,634

O A charge of $1,086

O A credit of $1,086

70

Financial Accounting (FFA/FA)

BPP

12.7 Doggard Co is a business that sells second hand cars. If a car develops a fault within 30 days

of the sale, Doggard Co will repair it free of charge.

At 30 April Doggard Co had made a provision for repairs of $2,500. At 30 April 20X5

Doggard Co calculated that the provision should be $2,000.

What entry should be made for the provision in Doggard Co's statement of profit or loss

for the gear to 30 April 20X5?

A charge of $500

A credit of $500

A charge of $2,000

A credit of $2,000

12.8 Which of the following best describes a provision according to IAS 37 Provisions,

Contingent Liabilities and Contingent Assets?

A provision is a liability of uncertain timing or amount

A provision is a possible obligation of uncertain timing or amount

A provision is a credit balance set up to offset a contingent asset so that

the effect on the statement of financial position is nil

A provision is a possible asset that arises from past events

12.9 Which of the following items does the statement below describe?

According to IAS 37 Provisions, Contingent Liabilities and Contingent Assets, 'A

possible obligation that arises from past events and whose existence will be confirmed

only by the occurrence or non-occurrence of one or more uncertain future events not

wholly within the entity's control'.

A provision

A current liability

A contingent liability

A contingent asset

12.10 Montague's paint shop has suffered some bad publicity as a result of a customer claiming to

be suffering from skin rashes as a result of using a new brand of paint sold by Montague's

shop. The customer launched a court action against Montague in November 20X3,

claiming damages of $5,000. Montague's lawyer has advised him that the most probable

outcome is that he will have to pay the customer $3,000.

What amount should Montague include as a provision in his financial statements for the

gear ended 31 December 20X3?

BPP

Questions

71

12.11 Mobiles Co sells goods with a one gear free warranty under which customers are covered

for any defect that becomes apparent within a year of purchase. In calendar year 20X4,

Mobiles Co sold 100,000 units.

The company expects warranty claims for 5% of units sold. Half of these claims will be

for a major defect, with an average claim value of $50. The other half of these claims will

be for a minor defect, with an average claim value of $10.

What amount should Mobiles Co include as a provision in the statement of financial

position for the year ended 31 December 20X4?

$125,000

$25,000

$300,000

$150,000

12.12 When a provision is needed that involves a number of outcomes, the provision is

calculated using the expected value of expenditure. The expected value of expenditure is

the total expenditure of:

Each possible outcome

Each possible outcome weighted according to the probability of each

outcome happening

Each possible outcome divided by the number of outcomes

Each possible outcome multiplied by the number of outcomes

12.13 X Co sells goods with a free one gear warranty and had a provision for warranty claims of

$64,000 at 31 December During the year ended 31 December $25,000 in claims were

paid to customers. On 31 December X Co estimated that the following claims will be

paid in the following gear:

Scenario

Probability

Anticipated cost

Worst case

5%

$150,000

Best case

20%

$25,000

Most likely

75%

$60,000

What amount should X Co record in the statement of profit or loss for the year ended 31

December 20X1 in respect of the provision?

72

$57,500

$6,500

$18,500

$39,000

Financial Accounting (FFA/FA)

BPP

0

0