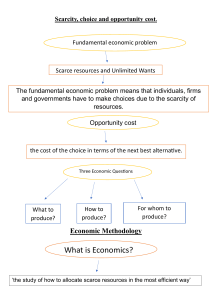

Economics is an Art and a Science i. Economics as an Art: Art is the practical application of knowledge for achieving goals. Economics provides guidance to the solutions to all the economic problems. A. C. Pigou, Alfred Marshall and others regard Economics as an art. ii. Economics as a Science: Science is a systematic study of knowledge. All its relevant facts are collected, classified, and analysed with its scale of measurement. Using these facts, science develops the co-relationship between cause and effect. Scientific laws derived are tested through experiments; and future predictions are made. These laws are universally applicable and accepted. Economists like Robbins, Jordon and Robertson argue that Economics is a science like Physics, Chemistry etc., since, it has several similar characteristics. Economics examines the relationships between the causes and the effects of the problems. Hence, it is rightly considered as both an art and a science. In fact, art and science are complementary to each other. Positive vs Normative Economics Parameters Positive Economics Normative Economics Meaning A part of economics grounded on information and certainty is positive economics. A part of economics grounded on values, perspectives, and discernment is normative economics. Outlook Objective Subjective Deals with What actually is? What has to be? Nature Illustrative Dictatorial Testing (Trial) Statements can be tested Statements cannot be tested Economic problems Evidently elucidates the economic concerns and issues Provides a solution for the economic concerns, based on the value. Examples: Normative Economics/or Positive Economics: 1. Income inequality should be reduced by raising taxes on high-income earners (Normative) 2. Most healthcare should be provided free at the point of use (Normative) 3. Women should be provided higher school loans than men. (Normative) 4. Laborers should receive greater parts of capitalist profits. (Normative) 5. Working citizens should not pay for hospital care. (Normative) 6. India should create more employment opportunities. (Normative) 7. Bio fuels and oil are substitutes in the energy industry (Positive) 8. An increase in indirect tax will impact the less well off more than the rich (Positive). 9. Monopolies have proved to be inefficient. (Positive) 10.The relationship between wealth and demand is inverse in the case of inferior goods. (Positive) Importance of Positive and Normative Economics: 1. Even though normative economics is a subjective study, it acts as a base or a platform for out-of-the-box thinking. 2. It provides a foundation for the innovative ideas that will ignite to reform an economy. 3. On the other hand, Positive economics is needed to provide an objective approach. 4. Positive economics is focused on the facts and analyses of the effects of such decisions in society and provides necessary information to make a sound economic decision. 5. Normative economics is useful in creating and generating newer ideas from another or different perspectives also. It cannot be the only basis for making decisions on important economic issues, and here the positive economics come into action thus complementing each other. 6. Positive economic theory can help the economic policymakers to implement the normative value judgments. Basic Concepts of Economics Needs wants and demands are a part of basic economics principles. Though they are 3 simple words, they hold a very complex meaning behind them along with a huge differentiation factor. In fact, A product can be differentiated on the basis of whether it satisfies a customers’ needs, wants or demands. Needs Human needs are the basic requirements and include food, clothing and shelter. Without these humans cannot survive. An extended part of needs today has become education and healthcare. Generally, the products which fall under the needs category of products do not require a push. Instead the customer buys it themselves. But in today’s tough and competitive world, so many brands have come up with the same offering satisfying the needs of the customer that even the “needs category product” has to be pushed in the customers mind. Example of needs category products / sectors – Agriculture sector, Real Estate (land always appreciates), FMCG, etc. Wants Wants are a step ahead of needs and are largely dependent on the needs of humans themselves. For example, you need to buy a car. But I am sure you want to buy a luxury car. Thus, wants are not mandatory part of life. You DONT need a luxury car. But you will try to buy it because it is your want. Example of wants category products / sectors – Hospitality industry, Electronics, Consumer Durables, Automobile, Formula Bikes, FMCG, etc. Desire 1. Desire simply refers to the mere wish of a person to have a particular commodity, irrespective of the fact whether one can buy it or not 2. There are no limitations for a desire. A person can desire anything at any point of time 3. Desire has no relation with price, place and time 4. Desire has a narrow scope as it includes demand. Demand 1. Demand refers to a desire backed by the ability to pay and willingness to pay for a particular commodity 2. There are several limitations for a demand such as ability to pay, willingness to buy etc 3. Demand has relation with price, place and time 4. Demand has a wider scope as it is part of desire The basic difference between wants and demands is desire. Note: Needs are more physiological whereas wants and desires are more psychological. Example of demands – Cruise, BMW, 5 star hotel etc. Market >> Identify needs wants and demands >> Offer products to satisfy either needs, wants or demands. (In this conversation Mother is wishing her son (Mukund) on his birthday and giving him Rs.1000 as the birthday gift. Mother is suggesting many options to spend money and trying to teach him, that he has limited money and he can only go for single or combination of options, but he cannot go for all options as money with Mukund is limited.) Mother: Many Happy return of the day, Son. May God bless you. Mukund: Thanks Mummy for wishing me on my birthday. But first tell me, where is my birthday gift? Mother: Take this 1000 rupees note as birthday gift. Mukund: WOW! Thank you mummy Mother: Okay Mukund, Tell me where you are going to spend this 1000 rupees. Mukund: I don’t know right now. Mother: You have many options to spend, like: 1. 2. 3. 4. You can give party to your friends. You can buy clothes for yourself for Rs.1000. You can go for movie with your friends. You can buy books and stationery for you and save some money. Mukund: Mummy you have given me lot of choices. Now I am confused for which must go. Mummy, Can I opt combination of options? Mother: Yes you can go for more than on option but you cannot go for all. Mukund: Why? Mother: Because you have limited amount with you i.e. Rs. 1000 Only. Because If you go for more than one option it cost much more than what you have. Mukund: I think it is my bad luck Mother: No Mukund, It is not your bad luck because similar problem (dilemma) is faced by every individual, every society and even every country in this world. Mukund: What is the reason behind this shortage of money or other resources? Mother: Mukund, Resources are the inputs used in the production of the things we desire. Therefore, the goods produced by these resources are also scarce Mukund: I want to solve this problem of scarcity. Please tell what I have to do? Mother: Dear Mukund, This problem of scarcity is universal and unavoidable. The problem can never be solved but can only be managed. Mukund: So what should we do to manage the problem of scarcity? Mother: We should make efficient use of resources in order to satisfy unlimited wants and desires. LETS UNDERSTAND (1) SCARCITY Scarcity is the most basic economic problem (or limited resources), that every country (Economy) faces. Economy runs into scarcity as resources are scarce to satisfy unlimited wants and desires of the society. Problem of scarcity can never be solved or avoided, it can only be managed. (2) ALTERNATIVE USE OF RESOURCES Resources of Alternative uses of scarce resources can be understood with the help of given example. Government has to decide where it can use the tax revenue collected, whether for defence goods or for the construction of shelters for homeless people of the country. In a similar manner a farmer having a single piece of land has to decide whether to produce rice or wheat. (3) ECONOMICS Economics is the study of optimum utilization of scarce resources with the objective to satisfy unlimited wants and desires. (4) ECONOMIC PROBLEM Economic Problem is the problem of allocation and optimum utilization of scarce resources An economic problem arises because o Resources are short in supply in relation to needs and wants of the society. o Resources have alternative uses 5. Opportunity Cost This concept goes hand in hand with scarcity. Commonly known as the basic relationship between scarcity and choice, opportunity cost is a benefit someone gives up in order to gain something else. For example, if you have $10 to spend but you must choose between spending it on food and spending it on a book, you must give up one to attain the other. The opportunity cost of buying food is the book, since you no longer reap the benefits of owning the book. On the contrary, the opportunity cost of purchasing the book would be your inability to satisfy your hunger. 6. Incentives People respond to incentives. Governments offer them because they can motivate individuals to act a certain way, which can be a good thing. For example, if a government offers subsidies to firms who reduce their pollution to a specified amount, firms will want to minimize their pollution so they can take advantage of the subsidy. Here's another example: if your boss offers you recognition for a project you worked hard on, you'll be motivated to work just as hard next time — if not, even harder — so you can receive the same recognition again. 7. Purchasing Power If you have a dollar one year, it's still worth the same as a dollar in the future, isn't it? Wrong. While it may still be defined as a single dollar, inflation has caused it to be worth less than it was before. Explanation: say that your dollar can buy you a candy bar. One year later, you go back to the convenience store to purchase that same candy bar, but you notice the price has now risen to $1.10. Inflation pushed the price up, indicating that you need more than a dollar to purchase the same candy bar. Thus, your purchasing power has declined.