Review of Economic Studies (2005) 72, 707–734

c 2005 The Review of Economic Studies Limited

0034-6527/05/00290707$02.00

Monetary Policy and Exchange Rate

Volatility in a Small Open Economy

JORDI GALÍ

CREI, UPF, CEPR and NBER

and

TOMMASO MONACELLI

IGIER, Università Bocconi and CEPR

First version received November 2002; final version accepted October 2004 (Eds.)

We lay out a small open economy version of the Calvo sticky price model, and show how the

equilibrium dynamics can be reduced to a simple representation in domestic inflation and the output gap.

We use the resulting framework to analyse the macroeconomic implications of three alternative rulebased policy regimes for the small open economy: domestic inflation and CPI-based Taylor rules, and

an exchange rate peg. We show that a key difference among these regimes lies in the relative amount

of exchange rate volatility that they entail. We also discuss a special case for which domestic inflation

targeting constitutes the optimal policy, and where a simple second order approximation to the utility of

the representative consumer can be derived and used to evaluate the welfare losses associated with the

suboptimal rules.

1. INTRODUCTION

Much recent work in macroeconomics has involved the development and evaluation of monetary

models that bring imperfect competition and nominal rigidities into the dynamic stochastic

general equilibrium structure that for a long time had been the hallmark of real business

cycle (RBC) theory. In the resulting models—often referred to as New Keynesian—changes

in monetary settings generally have non-trivial effects on real variables. Monetary policy may

thus become a potential stabilization tool, as well as an independent source of economic

fluctuations. Not surprisingly, the study of the properties of alternative monetary policy rules (i.e.

specifications of how the central bank changes the settings of its policy instrument in response to

changes in macroeconomic conditions) has been a fruitful area of research in recent years and a

natural application of the new generation of models.1

In the present paper we lay out a small open economy version of a model with Calvotype staggered price-setting, and use it as a framework for analysing the properties and macroeconomic implications of alternative monetary policy regimes.2 The use of a staggered pricesetting structure allows for richer dynamic effects of monetary policy than those found in the

models with one-period advanced price-setting that are common in the recent open economy

literature.3 Most importantly, and in contrast with most of the existing literature—where monetary policy is introduced by assuming that some monetary aggregate follows an exogenous

1. The volume edited by Taylor (1999) contains several significant contributions to that literature. See, e.g.

Clarida, Galı́ and Gertler (1999) for a survey.

2. See, e.g. King and Wolman (1996), Yun (1996), and Woodford (2003, Chapter 4), for an analysis of the

canonical Calvo model in a closed economy.

3. See, e.g. Obstfeld and Rogoff (1995, 1999), Bacchetta and van Wincoop (2000), Betts and Devereux (2000),

and Corsetti and Pesenti (2001).

707

708

REVIEW OF ECONOMIC STUDIES

stochastic process—we model monetary policy as endogenous, with a short-term interest rate

being the instrument of that policy.4 For this very reason our framework allows us to model alternative monetary regimes. Furthermore, we believe that our approach accords much better with

the practice of modern central banks, and provides a more suitable framework for policy analysis

than the traditional one.

Our framework differs from much of the literature in that it models the small open economy

as one among a continuum of (infinitesimally small) economies making up the world economy.

Our assumptions on preferences and technology, combined with the Calvo price-setting structure

and the assumption of complete financial markets, give rise to a highly tractable framework and

to simple and intuitive log-linearized equilibrium conditions for the small open economy. In fact,

the latter can be reduced to a first order, two-equation dynamical system for domestic inflation

and the output gap whose structure, consisting of a new Keynesian Phillips curve and a dynamic

IS-type equation, is identical to the one associated with the workhorse sticky price model of

a closed economy, often used in monetary policy analysis.5 Of course, as we show below, the

coefficients in the open economy’s equilibrium conditions also depend on parameters that are

specific to the open economy (in our case, the degree of openness and the substitutability among

goods of different origin), while the driving forces also include world output fluctuations (which

are taken as exogenous to the small open economy). As in its closed economy counterpart, the

two equations must be complemented with a description of how monetary policy is conducted,

in order to close the model.

We then address the issue of a welfare evaluation of alternative policy regimes. Under

a particular parameterization of household’s preferences we can derive a second order

approximation to the consumer’s utility, which can be used for policy evaluation purposes.6 In the

particular case considered (which entails log utility and a unit elasticity of substitution between

bundles of goods produced in different countries), we show that the optimal policy requires that

the domestic price level is fully stabilized.

We employ our framework to analyse the macroeconomic implications and the relative

welfare ranking of three simple monetary policy rules for the small open economy. Two of the

simple rules considered are stylized Taylor-type rules. The first has the domestic interest rate

respond systematically to domestic inflation (i.e. inflation of domestic goods prices), whereas the

second assumes that CPI inflation is the variable the domestic central bank reacts to. The third

rule we consider is one that pegs the effective nominal exchange rate.

We show that these regimes can be ranked in terms of their implied volatility for the

nominal exchange rate and the terms of trade. Hence, a policy of strict domestic inflation

targeting, which in our framework can achieve a simultaneous stabilization of the output gap and

domestic inflation, implies a substantially greater volatility in the nominal exchange rate and

4. See Lane (2001) for a survey of the new open economy macroeconomics literature. The introduction of price

staggering in an open economy model follows the lead of Kollmann (2001) and Chari, Kehoe and McGrattan (2002),

though both papers specify monetary policy as exogenous, restricting their analysis to the effects of a monetary shock. A

recent exception is given by Obstfeld and Rogoff (1999), who solve for the optimal money supply rule in the context of a

model with one-period sticky wages. A more similar methodological approach can be found in Svensson (2000), in which

optimal policy is derived from the minimization by the central bank of a quadratic loss function. His model, however,

differs from the standard optimizing sticky price model analysed here in that it assumes a predetermined output and

inflation (resulting from their dependence on lagged variables, with a somewhat arbitrary lag structure), and introduces

an ad hoc cost-push shock in the inflation equation (which creates a trade-off between the output gap and inflation).

Since we wrote and circulated the first version of the present paper there have been many significant contributions to the

literature on monetary policy regimes in open economies, including McCallum and Nelson (2000), Corsetti and Pesenti

(2001, 2005), Clarida, Galı́ and Gertler (2001, 2002), Schmitt-Grohé and Uribe (2001), Kollmann (2002), Parrado and

Velasco (2002), and Benigno and Benigno (2003), among others.

5. See, e.g. Clarida et al. (1999) and Woodford (2003, Chapter 4) among others.

6. Benigno and Benigno (2003) obtain a similar result in the context of a two-country model.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

709

terms of trade than the one achieved under the two Taylor rules and/or the exchange rate peg. The

excess smoothness in the nominal exchange rate implied by those simple rules (relative to the

optimal policy), combined with the assumed inertia in nominal prices, prevents relative prices

from adjusting sufficiently fast in response to changes in relative productivity shocks, causing

thus a significant deviation from the first best allocation. In particular, a CPI-based Taylor rule

is shown to deliver equilibrium dynamics that allow us to characterize it as a hybrid regime,

somewhere between a domestic inflation-based Taylor rule and an exchange rate peg.

The ranking based on the terms of trade volatility translates one-for-one into a welfare

ranking. Thus, and for a broad range of parameter configurations, a domestic inflation-based

Taylor rule is shown to dominate a CPI-based Taylor rule; the latter in turn dominates an

exchange rate peg. More generally, we show that, across regimes, the higher the implied

equilibrium terms of trade volatility, the lower the volatility of inflation and output gap, and

therefore the higher the resulting welfare score.

The remainder of the paper is organized as follows. In Section 2 we lay out the basic model.

Section 3 derives the equilibrium in log-linearized form, and its canonical representation in terms

of output gap and inflation. Section 4 analyses the macroeconomic implications of alternative

monetary policy regimes. Section 5 analyses optimal monetary policy in both the world and the

small economy under a particular parameterization in the latter, and conducts a welfare evaluation

of the alternative monetary policy regimes. Section 6 concludes.

2. A SMALL OPEN ECONOMY MODEL

We model the world economy as a continuum of small open economies represented by the unit

interval. Since each economy is of measure zero, its domestic policy decisions do not have any

impact on the rest of the world. While different economies are subject to imperfectly correlated

productivity shocks, we assume that they share identical preferences, technology, and market

structure.

Next we describe in detail the problem facing households and firms located in one such

economy. Before we do so, a brief remark on notation is in order. Since our focus is on the

behaviour of a single economy and its interaction with the world economy, and in order to lighten

the notation, we will use variables without an i-index to refer to the small open economy being

modelled. Variables with an i ∈ [0, 1] subscript refer to economy i, one among the continuum of

economies making up the world economy. Finally, variables with a star superscript correspond

to the world economy as a whole.

2.1. Households

A typical small open economy is inhabited by a representative household who seeks to

maximize

X∞

E0

β t U (Ct , Nt )

(1)

t=0

where Nt denotes hours of labour, and Ct is a composite consumption index defined by

η

η−1

η−1 η−1

1

1

η

η

η

η

Ct ≡ (1 − α) (C H,t )

+ α (C F,t )

where C H,t is an index of consumption of domestic goods given by the CES function

! ε

Z

1

C H,t ≡

0

C H,t ( j)

ε−1

ε

ε−1

dj

(2)

710

REVIEW OF ECONOMIC STUDIES

where j ∈ [0, 1] denotes the good variety.7 C F,t is an index of imported goods given by

! γ

Z

1

C F,t ≡

(Ci,t )

γ −1

γ

γ −1

di

0

where Ci,t is, in turn, an index of the quantity of goods imported from country i and consumed

by domestic households. It is given by an analogous CES function:

! ε

Z

1

Ci,t ≡

Ci,t ( j)

ε−1

ε

ε−1

dj

.

0

Notice that parameter ε > 1 denotes the elasticity of substitution between varieties

(produced within any given country).8 Parameter α ∈ [0, 1] is (inversely) related to the degree

of home bias in preferences, and is thus a natural index of openness. Parameter η > 0 measures

the substitutability between domestic and foreign goods, from the viewpoint of the domestic

consumer, while γ measures the substitutability between goods produced in different foreign

countries.

The maximization of (1) is subject to a sequence of budget constraints of the form

Z 1

Z 1Z 1

PH,t ( j)C H,t ( j)d j +

Pi,t ( j)Ci,t ( j)d jdi + E t {Q t,t+1 Dt+1 } ≤ Dt + Wt Nt + Tt (3)

0

0

0

for t = 0, 1, 2, . . ., where Pi,t ( j) is the price of variety j imported from country i (expressed in

domestic currency, i.e. the currency of the importing country whose economy is being modelled).

Dt+1 is the nominal pay-off in period t + 1 of the portfolio held at the end of period t (and which

includes shares in firms), Wt is the nominal wage, and Tt denotes lump-sum transfers/taxes.

All the previous variables are expressed in units of domestic currency. Q t,t+1 is the stochastic

discount factor for one-period ahead nominal pay-offs relevant to the domestic household. We

assume that households have access to a complete set of contingent claims, traded internationally.

Notice that money does not appear in either the budget constraint or the utility function:

throughout we specify monetary policy in terms of an interest rate rule (directly or indirectly);

hence, we do not need to introduce money explicitly in the model.9

The optimal allocation of any given expenditure within each category of goods yields the

demand functions:

PH,t ( j) −ε

Pi,t ( j) −ε

C H,t ( j) =

C H,t ;

Ci,t ( j) =

Ci,t

(4)

PH,t

Pi,t

R

1

1−ε

1

for all i, j ∈ [0, 1], where PH,t ≡ 0 PH,t ( j)1−ε d j

is the domestic price index (i.e. an

R

1

1−ε

1

is a price

index of prices of domestically produced goods) and Pi,t ≡ 0 Pi,t ( j)1−ε d j

index for goods imported from country i (expressed in domestic currency), for all i ∈ [0, 1]. It

R1

R1

follows from (4) that 0 PH,t ( j) C H,t ( j)d j = PH,t C H,t and 0 Pi,t ( j) Ci,t ( j)d j = Pi,t Ci,t .

7. As discussed below, each country produces a continuum of differentiated goods, represented by the unit

interval.

8. Notice that it is irrelevant whether we think of integrals like the one in (2) as including or not the corresponding

variable for the small economy being modelled, since its presence would have a negligible influence on the integral itself

(in fact each individual economy has a zero measure). The previous remark also applies to many other expressions

involving integrals over the continuum of economies (i.e. over i) that the reader will encounter below.

9. That modelling strategy has been adopted in much recent research on monetary policy. In it money can be

thought of as playing the role of a unit of account only.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

711

Furthermore, the optimal allocation of expenditures on imported goods by country of origin

implies

Pi,t −γ

Ci,t =

C F,t

(5)

PF,t

R

1

1−γ

1

for all i ∈ [0, 1], and where PF,t ≡ 0 Pi,t 1−γ di

is the price index for imported goods,

also expressed in domestic currency. Notice that (5) implies that we can write total expenditures

R1

on imported goods as 0 Pi,t Ci,t di = PF,t C F,t .

Finally, the optimal allocation of expenditures between domestic and imported goods is

given by

PF,t −η

PH,t −η

C H,t = (1 − α)

Ct ;

C F,t = α

Ct

(6)

Pt

Pt

1

where Pt ≡ (1 − α) (PH,t )1−η + α(PF,t )1−η 1−η is the consumer price index (CPI).10

Notice that, when the price indexes for domestic and foreign goods are equal (as in the

steady state described below), parameter α corresponds to the share of domestic consumption

allocated to imported goods. It is also in this sense that α represents a natural index of

openness.

Accordingly, total consumption expenditures by domestic households are given by

PH,t C H,t + PF,t C F,t = Pt Ct . Thus, the period budget constraint can be rewritten as

Pt Ct + E t {Q t,t+1 Dt+1 } ≤ Dt + Wt Nt + Tt .

(7)

In what follows we specialize the period utility function to take the form

U (C, N ) ≡

C 1−σ

N 1+ϕ

−

.

1−σ

1+ϕ

Then we can rewrite the remaining optimality conditions for the household’s problem as follows:

Wt

Pt

which is a standard intratemporal optimality condition, and

Ct+1 −σ

Pt

β

= Q t,t+1 .

Ct

Pt+1

ϕ

Ctσ Nt =

(8)

(9)

Taking conditional expectations on both sides of (9) and rearranging terms we obtain a

conventional stochastic Euler equation:

(

)

Ct+1 −σ

Pt

β Rt E t

=1

(10)

Ct

Pt+1

where Rt =

1

E t { Q t,t+1 }

is the gross return on a riskless one-period discount bond paying off one

unit of domestic currency in t + 1 (with E t Q t,t+1 being its price).

For future reference it is useful to note that (8) and (10) can be respectively written in loglinearized form as:

10. It is useful to note, for future reference, that in the particular case of η = 1, the CPI takes the form

1

Pt = (PH,t )1−α (PF,t )α , while the consumption index is given by Ct =

C 1−α C F,t α .

(1−α)(1−α) α α H,t

712

REVIEW OF ECONOMIC STUDIES

wt − pt = σ ct + ϕ n t

1

ct = E t {ct+1 } − (rt − E t {πt+1 } − ρ)

σ

(11)

where lower case letters denote the logs of the respective variables, ρ ≡ β −1 − 1 is the time

discount rate, and πt ≡ pt − pt−1 is CPI inflation (with pt ≡ log Pt ).

2.1.1. Domestic inflation, CPI inflation, the real exchange rate, and the terms of

trade: some identities. Before proceeding with our analysis of the equilibrium we introduce

several assumptions and definitions, and derive a number of identities that are extensively used

below.

We start by defining the bilateral terms of trade between the domestic economy and country

Pi,t

i as Si,t = PH,t

, i.e. the price of country i’s goods in terms of home goods. The effective terms

of trade are thus given by

St ≡

PF,t

PH,t

Z 1

=

0

!

1

1−γ

1−γ

Si,t di

which can be approximated (up to first order) by the log-linear expression

Z 1

st =

si,t di.

(12)

0

Log-linearization of the CPI formula around a symmetric steady state satisfying the

purchasing power parity (PPP) condition PH,t = PF,t yields11

pt ≡ (1 − α) p H,t + α p F,t

= p H,t + α st

(13)

where st ≡ p F,t − p H,t denotes the (log) effective terms of trade, i.e. the price of foreign goods

in terms of home goods. It is useful to note, for future reference, that (12) and (13) hold exactly

when γ = 1 and η = 1, respectively.

It follows that domestic inflation—defined as the rate of change in the index of domestic

goods prices, i.e. π H,t ≡ p H,t − p H,t−1 —and CPI inflation are linked according to

πt = π H,t + α 1st

(14)

which makes the gap between our two measures of inflation proportional to the per cent

change in the terms of trade, with the coefficient of proportionality given by the index of

openness α.

We assume that the law of one price holds for individual goods at all times (both for

i ( j) for all i, j ∈ [0, 1], where E

import and export prices), implying that Pi,t ( j) = Ei,t Pi,t

i,t

is the bilateral nominal exchange rate (the price of country i’s currency in terms of the domestic

i ( j) is the price of country i’s good j expressed in the producer’s (i.e. country

currency), and Pi,t

i’s) currency. Plugging the previous assumption into the definition of Pi,t one obtains Pi,t =

R

1

1 i

i , where P i ≡

1−ε d j 1−ε . In turn, by substituting into the definition of P

Ei,t Pi,t

P

(

j)

F,t

i,t

i,t

0

11. Below we discuss the conditions under which PPP holds in our model.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

713

and log-linearizing around the symmetric steady state we obtain

Z 1

i

p F,t =

(ei,t + pi,t

)di

0

= et + pt∗

R1

R1

i ( j)d j is the (log)

pi,t

R1 i

domestic price index for country i (expressed in terms of its currency), and pt∗ ≡ 0 pi,t

di is the

(log) world price index. Notice that for the world as a whole there is no distinction between CPI

and domestic price level, nor for their corresponding inflation rates.

Combining the previous result with the definition of the terms of trade we obtain the

following expression:

where et ≡

0

i ≡

ei,t di is the (log) nominal effective exchange rate, pi,t

0

st = et + pt∗ − p H,t .

(15)

Next, we derive a relationship between the terms of trade and the real exchange rate. First,

E Pi

we define the bilateral real exchange rate with country i as Qi,t ≡ i,tPt t , i.e. the ratio of the two

R1

countries’ CPIs, both expressed in domestic currency. Let qt ≡ 0 qi,t di be the (log) effective

real exchange rate, where qi,t ≡ log Qi,t . It follows that

Z 1

qt =

(ei,t + pti − pt )di

0

= et + pt∗ − pt

= st + p H,t − pt

= (1 − α) st

where the last equality holds only up to a first order approximation when η 6= 1.12

2.1.2. International risk sharing. Under the assumption of complete securities markets,

a first order condition analogous to (9) must also hold for the representative household in any

other country, say country i:

!−σ

!

!

i

Ct+1

Pti

Eti

= Q t,t+1 .

(16)

β

i

i

Cti

Pt+1

Et+1

Combining (9) and (16), together with the real exchange rate definition, it follows that

1

Ct = ϑi Cti Qi,t σ

(17)

for all t, and where ϑi is a constant which will generally depend on initial conditions regarding

relative net asset positions. Henceforth, and without loss of generality, we assume symmetric

initial conditions (i.e. zero net foreign asset holdings and an ex ante identical environment), in

which case we have ϑi = ϑ = 1 for all i. As shown in Appendix A, in the symmetric perfect

foresight steady state we also have that C = C i = C ∗ and Qi = Si = 1 (i.e. purchasing power

parity holds), for all i.

h

i 1

1−η 1−η

12. The last equality can be derived by log-linearizing PPt = (1 − α) + α St

around a symmetric

H,t

steady state, which yields

pt − p H,t = α st .

714

REVIEW OF ECONOMIC STUDIES

Taking logs on both sides of (17) and integrating over i we obtain

1

qt

σ

1−α

= ct∗ +

st

σ

ct = ct∗ +

(18)

R1

where ct∗ ≡ 0 cti di is our index for world consumption (in log terms), and where the second

equality holds only up to a first order approximation when η 6= 1. Thus we see that the

assumption of complete markets at the international level leads to a simple relationship linking

domestic consumption with world consumption and the terms of trade.13

2.1.3. Uncovered interest parity and the terms of trade. Under the assumption

of complete international financial markets, the equilibrium price (in terms of domestic

currency) of a riskless bond denominated in foreign currency is given by Ei,t (Rti )−1 =

E t {Q t,t+1 Ei,t+1 }. The previous pricing equation can be combined with the domestic bond

pricing equation, (Rt )−1 = E t {Q t,t+1 } to obtain a version of the uncovered interest parity

condition:

E t {Q t,t+1 [Rt − Rti (Ei,t+1 /Ei,t )]} = 0.

Log-linearizing around a perfect foresight steady state, and aggregating over i, yields the

familiar expression14

rt − rt∗ = E t {1et+1 }.

(19)

Combining the definition of the (log) terms of trade with (19) yields the following stochastic

difference equation:

∗

st = (rt∗ − E t {πt+1

}) − (rt − E t {π H,t+1 }) + E t {st+1 }.

(20)

As we show in Appendix A, the terms of trade are pinned down uniquely in the perfect

foresight steady state. That fact, combined with our assumption of stationarity in the model’s

driving forces and a convenient normalization (requiring that PPP holds in the steady state),

implies that limT →∞ E t {sT } = 0.15 Hence, we can solve (20) forward to obtain

nX∞

o

∗

∗

st = E t

[(rt+k

− πt+k+1

) − (rt+k − π H,t+k+1 )]

(21)

k=0

i.e. the terms of trade are a function of current and anticipated real interest rate differentials.

We must point out that while equation (20) (and (21)) provides a convenient (and intuitive)

way of representing the connection between terms of trade and interest rate differentials, it does

not constitute an additional independent equilibrium condition. In particular, it is easy to check

that (20) can be derived by combining the consumption Euler equations for both the domestic

and world economies with the risk sharing condition (18) and equation (14).

Next we turn our attention to the supply side of the economy.

13. A similar relationship holds in many international RBC models. See, e.g. Backus and Smith (1993).

14. This abstracts from the presence of a risk premium term. See Kollmann (2002) for a specification which

includes an exogenous stochastic risk premium.

15. Our assumption of PPP holding in the steady state implies that the real interest rate differential will revert to

a zero mean. More generally, the real interest rate differential will revert to a constant mean, as long as the terms of

trade are stationary in first differences. That would be the case if, say, the technology parameter had a unit root or a

different average rate of growth relative to the rest of the world. In those cases we could have persistent real interest rate

differentials.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

715

2.2. Firms

2.2.1. Technology. A typical firm in the home economy produces a differentiated good

with a linear technology represented by the production function

Yt ( j) = At Nt ( j)

where at ≡ log At follows the AR(1) process at = ρa at−1 + εt , and j ∈ [0, 1] is a firm-specific

index. Hence, the real marginal cost (expressed in terms of domestic prices) will be common

across domestic firms and given by

mct = −ν + wt − p H,t − at

where ν ≡ − log(1 − τ ), with τ being an employment subsidy whose role is discussed later in

more detail. h

i ε

R1

1

ε−1

Let Yt ≡ 0 Yt ( j)1− ε d j

represent an index for aggregate domestic output, analogous

to the one introduced for consumption. It is useful, for future reference, to derive an approximate

aggregate production function relating the previous index to aggregate employment. Hence,

notice that

Z 1

Yt Z t

Nt ≡

Nt ( j)d j =

At

0

R 1 Yt ( j)

where Z t ≡ 0 Yt d j. In Appendix C we show that equilibrium variations in z t ≡ log Z t

around the perfect foresight steady state are of second order. Thus, and up to a first order

approximation, we have an aggregate relationship

yt = at + n t .

(22)

2.2.2. Price-setting. We assume that firms set prices in a staggered fashion, as in Calvo

(1983). Hence, a measure 1 − θ of (randomly selected) firms sets new prices each period, with an

individual firm’s probability of re-optimizing in any given period being independent of the time

elapsed since it last reset its price. As we show in Appendix B, the optimal price-setting strategy

for the typical firm resetting its price in period t can be approximated by the (log-linear) rule

X∞

p H,t = µ + (1 − βθ )

(βθ)k E t {mct+k + p H,t }

(23)

k=0

ε

where p H,t denotes the (log) of newly set domestic prices, and µ ≡ log ε−1

, which

corresponds to the log of the (gross) mark-up in the steady state (or, equivalently, the optimal

mark-up in a flexible price economy).

Hence, we see that the pricing decision in our model (as in its closed economy counterpart)

is a forward-looking one. The reason is simple and well understood by now: firms that are adjusting prices in any given period recognize that the price they set will remain effective for a (random) number of periods. As a result they set the price as a mark-up over a weighted average of

expected future marginal costs, instead of looking at current marginal cost only. Notice that in the

flexible price limit (i.e. as θ → 0), we recover the familiar mark-up rule p H,t = µ + mct + p H,t .

3. EQUILIBRIUM

3.1. Aggregate demand and output determination

3.1.1. Consumption and output in the small open economy.

the representative small open economy (“home”) requires

Goods market clearing in

716

REVIEW OF ECONOMIC STUDIES

Yt ( j) = C H,t ( j) +

Z

0

=

PH,t ( j)

PH,t

1

C iH,t ( j)di

(24)

−ε "

Z 1

PH,t −η

(1 − α)

Ct + α

Pt

0

PH,t

i

Ei,t PF,t

!−γ

i

PF,t

Pti

!−η

#

Cti di

for all j ∈ [0, 1] and all t, where C iH,t ( j) denotes country i’s demand for good j produced

in the home economy. Notice that the second equality has made use of (6) and (5) together

with our assumption of symmetric preferences across countries, which implies C iH,t ( j) =

−γ i −η

PF,t

PH,t

PH,t ( j) −ε

α PH,t

Cti .

i

Ei,t PF,t

Pti

hR

i ε

1

ε−1

1

Plugging (24) into the definition of aggregate domestic output Yt ≡ 0 Yt ( j)1− ε d j

,

we obtain

!−η

!−γ

Z 1

i

PF,t

PH,t −η

PH,t

Yt = (1 − α)

Ct + α

Cti di

i

Pt

Ei,t PF,t

Pti

0

!γ −η

#

"

Z 1

i

Ei,t PF,t

PH,t −η

η

i

=

(1 − α) Ct + α

Qi,t Ct di

Pt

PH,t

0

"

#

Z 1

γ −η η− 1

PH,t −η

i

σ

(25)

=

Ct (1 − α) + α

St Si,t

Qi,t di

Pt

0

where the last equality follows from (17), and where Sti denotes the effective terms of trade of

country i, while Si,t denotes the bilateral terms of trade between the home economy and foreign

country i. Notice that in the particular case of σ = η = γ = 1 the previous condition can be

written exactly as16

Yt = Ct Stα .

(26)

R1 i

More generally, and recalling that 0 st di = 0, we can derive the following first order

log-linear approximation to (25) around the symmetric steady state:

1

yt = ct + αγ st + α η −

qt

σ

αω

= ct +

st

(27)

σ

where ω ≡ σ γ + (1 − α) (σ η − 1). Notice that σ = η = γ = 1 implies ω = 1.

A condition analogous to the one above will hold for all countries. Thus, for a generic

i

country i it can be rewritten as yti = cti + αω

σ st . By aggregating over all countries we can derive

a world market clearing condition as follows:

Z 1

∗

yt ≡

yti di

(28)

0

Z

=

0

1

cti di ≡ ct∗

16. Here one must use the fact that under the assumption η = 1, the CPI takes the form Pt = (PH,t )1−α (PF,t )α

P α

= Stα .

thus implying PPt = P F,t

H,t

H,t

GALÍ & MONACELLI

SMALL OPEN ECONOMY

717

where yt∗ and ct∗ are indexes for world output and consumption (in log terms), and where the

R1

main equality follows, once again, from the fact that 0 sti di = 0.

Combining (27) with (17) and (28), we obtain

yt = yt∗ +

where σα ≡

σ

(1−α)+αω

1

st

σα

(29)

> 0.

Finally, combining (27) with Euler equation (11), we get

αω

1

(rt − E t {πt+1 } − ρ) −

E t {1st+1 }

σ

σ

α2

1

= E t {yt+1 } − (rt − E t {π H,t+1 } − ρ) −

E t {1st+1 }

σ

σ

1

∗

= E t {yt+1 } −

(rt − E t {π H,t+1 } − ρ) + α2E t {1yt+1

}

σα

yt = E t {yt+1 } −

(30)

where 2 ≡ (σ γ − 1) + (1 − α)(σ η − 1) = ω − 1.

t

3.1.2. The trade balance. Let nxt ≡ Y1 Yt − PPH,t

Ct denote net exports in terms

of domestic output, expressed as a fraction of steady state output Y . In the particular case of

σ = η = γ = 1, it follows from (25) that PH,t Yt = Pt Ct for all t, thus implying a balanced

trade at all times. More generally, a first order approximation yields nxt = yt − ct − α st which

combined with (27) implies

ω

nxt = α

− 1 st .

(31)

σ

Again, in the special case of σ = η = γ = 1 we have nxt = 0 for all t, though the latter

property will also hold for any configuration of those parameters satisfying σ (γ − 1) + (1 −

α) (σ η − 1) = 0. More generally, the sign of the relationship between the terms of trade and net

exports is ambiguous, depending on the relative size of σ , γ , and η.17

3.2. The supply side: marginal cost and inflation dynamics

3.2.1. Marginal cost and inflation dynamics in the small open economy. In the small

open economy, the dynamics of domestic inflation in terms of real marginal cost are described

by an equation analogous to the one associated with a closed economy. Hence,

π H,t = β E t {π H,t+1 } + λ m

cct

(32)

where λ ≡ (1−βθ)(1−θ)

. Details of the derivation can be found in Appendix B.

θ

The determination of the real marginal cost as a function of domestic output in the small

open economy differs somewhat from that in the closed economy, due to the existence of a

wedge between output and consumption, and between domestic and consumer prices. Thus, in

our model we have

17. The fact that in our economy movements in the trade balance are allowed is a key difference with respect to

many models in the literature (see, e.g. Corsetti and Pesenti, 2001), which typically require log utility (σ = 1) and unitary

elasticity of substitution (η = 1) for balanced trade to hold continuously. Notice also that our framework requires stricter

conditions for balanced trade, in that it also requires γ = 1 (or any combination of η and γ such that ω

σ = 1).

718

REVIEW OF ECONOMIC STUDIES

mct = −ν + (wt − p H,t ) − at

= −ν + (wt − pt ) + ( pt − p H,t ) − at

= −ν + σ ct + ϕ n t + α st − at

= −ν + σ yt∗ + ϕ yt + st − (1 + ϕ) at

(33)

where the last equality makes use of (22) and (18). Thus, we see that marginal cost is increasing

in the terms of trade and world output. Both variables end up influencing the real wage, through

the wealth effect on labour supply resulting from their impact on domestic consumption. In

addition, changes in the terms of trade have a direct effect on the product wage, for any given

real wage. The influence of technology (through its direct effect on labour productivity) and of

domestic output (through its effect on employment and, hence, the real wage—for given output)

is analogous to that observed in the closed economy.

Finally, using (29) to substitute for st , we can rewrite the previous expression for the real

marginal cost in terms of domestic output and productivity, as well as world output:

mct = −ν + (σα + ϕ) yt + (σ − σα ) yt∗ − (1 + ϕ) at .

(34)

Notice that in the special cases α = 0 and/or σ = η = γ = 1, which imply σ = σα , the

domestic real marginal cost is completely insulated from movements in foreign output.

3.3. Equilibrium dynamics: a canonical representation

In this section we show that the linearized equilibrium dynamics for the small open economy

have a representation in terms of output gap and domestic inflation analogous to that of its

closed economy counterpart. That representation, which we refer to as the canonical one, has

provided the basis for the analysis and evaluation of alternative policy rules in much of the recent

literature. Let us define the domestic output gap xt as the deviation of (log) domestic output yt

from its natural level y t , where the latter is in turn defined as the equilibrium level of output in

the absence of nominal rigidities (and conditional on world output yt∗ ). Formally,

xt ≡ yt − y t .

The domestic natural level of output can be found after imposing mct = −µ for all t and

solving for domestic output in equation (34):

y t = + 0 at + α9 yt∗

v−µ

σα +ϕ ,

1+ϕ

σα +ϕ

(35)

σα

− σ2α +ϕ

.

where ≡

0≡

> 0, and 9 ≡

It also follows from (34) that the domestic real marginal cost and output gap will be related

according to

m

cct = (σα + ϕ) xt

which we can combine with (32) to derive a version of the new Keynesian Phillips curve (NKPC)

for the small open economy in terms of the output gap:

π H,t = β E t {π H,t+1 } + κα xt

(36)

where κα ≡ λ (σα + ϕ). Notice that for α = 0 (or σ = η = γ = 1) the slope coefficient is given

by λ (σ + ϕ) as in the standard, closed economy NKPC. More generally, we see that the form of

the Phillips equation for the open economy corresponds to that of the closed economy, at least

as far as domestic (i.e. producer) inflation is concerned. The degree of openness α affects the

dynamics of inflation only through its influence on the size of the slope of the Phillips curve, i.e.

the size of the inflation response to any given variation in the output gap. In the open economy,

GALÍ & MONACELLI

SMALL OPEN ECONOMY

719

a change in domestic output has an effect on marginal cost through its impact on employment

(captured by ϕ), and the terms of trade (captured by σα , which is a function of the degree of

openness and the substitutability between domestic and foreign goods). In particular, under the

assumption that σ η > 1, an increase in openness lowers the size of the adjustment in the terms of

trade necessary to absorb a change in domestic output (relative to world output), thus dampening

the impact of that adjustment on marginal cost and inflation.

Using (30) it is straightforward to derive a version of the so-called dynamic IS equation for

the open economy in terms of the output gap:

xt = E t {xt+1 } −

1

(rt − E t {π H,t+1 } − rr t )

σα

(37)

where

∗

rr t ≡ ρ − σα 0(1 − ρa ) at + ασα (2 + 9) E t {1yt+1

}

is the small open economy’s natural rate of interest.

Thus we see that the small open economy’s equilibrium is characterized by a forwardlooking IS-type equation similar to that found in the closed economy. Two differences can be

pointed out, however. First, the degree of openness influences the sensitivity of the output gap

to interest rate changes. In particular, if ω > 1 (which obtains for “high” values of η and γ ), an

increase in openness raises that sensitivity (through the stronger effects of the induced terms of

trade changes on demand). Second, openness generally makes the natural interest rate depend on

expected world output growth, in addition to domestic productivity.

4. OPTIMAL MONETARY POLICY: A SPECIAL CASE

In this section we derive and characterize the optimal monetary policy for our small open

economy, as well as its implications for a number of macroeconomic variables. Our analysis

is restricted to a special case for which a second order approximation to the welfare of the

representative consumer can be easily derived analytically.

Let us take as a benchmark the well-known closed economy version of the Calvo economy

with staggered price-setting. As discussed in Rotemberg and Woodford (1999), under the

assumption of a constant employment subsidy τ that neutralizes the distortion associated with

firms’ market power, it can be shown that the optimal monetary policy is the one that replicates

the flexible price equilibrium allocation. That policy requires that real marginal costs (and thus

mark-ups) are stabilized at their steady state level, which in turn implies that domestic prices be

fully stabilized. The intuition for that result is straightforward: with the subsidy in place, there is

only one effective distortion left in the economy, namely, sticky prices. By stabilizing mark-ups

at their “frictionless” level, nominal rigidities cease to be binding, since firms do not feel any

desire to adjust prices. By construction, the resulting equilibrium allocation is efficient, and the

price level remains constant.18

In an open economy—and as noted, among others, by Corsetti and Pesenti (2001)—there is

an additional factor that distorts the incentives of the monetary authority (beyond the presence of

market power): the possibility of influencing the terms of trade in a way beneficial to domestic

consumers. This possibility is a consequence of the imperfect substitutability between domestic

and foreign goods, combined with sticky prices (which render monetary policy non-neutral).19

As shown below, and similarly to Benigno and Benigno (2003) in the context of a two-country

18. See Galı́ (2003) for a discussion.

19. This distinguishes our analysis from that of Goodfriend and King (2001) who assume that the price of domestic

goods is determined in the world market.

720

REVIEW OF ECONOMIC STUDIES

model, the introduction of an employment subsidy that exactly offsets the market power distortion is not sufficient to render the flexible price equilibrium allocation optimal, for, at the margin,

the monetary authority would have an incentive to deviate from it to improve the terms of trade.

For the special parameter configuration σ = η = γ = 1 we can derive analytically the

employment subsidy that exactly offsets the combined effects of market power and the terms of

trade distortions, thus rendering the flexible price equilibrium allocation optimal.20 That result,

in turn, rules out the possibility of the existence of an average inflation (or deflation) bias, and

allows us to focus on policies consistent with zero average inflation, in a way analogous to the

analysis for the closed economy found in the literature.

Let us first characterize the optimal allocation from the viewpoint of a social planner

facing the same resource constraints to which the small open economy is subject in equilibrium

(vis-à-vis the rest of the world), given our assumption of complete markets. In that case,

the optimal allocation must maximize U (Ct , Nt ) subject to (i) the technological constraint

Yt = At Nt , (ii) a consumption/output possibilities set implicit in the international risk sharing

conditions (17), and (iii) the market clearing condition (25).

The derivation of a tractable, analytical solution requires that we restrict ourselves to the

special case of σ = η = γ = 1. In that case, (18) and (26) imply the exact expression

Ct = Yt1−α (Yt∗ )α . The optimal allocation (from the viewpoint of the small open economy, which

takes world output and consumption as given), must satisfy

−

U N (Ct , Nt )

Ct

= (1 − α)

UC (Ct , Nt )

Nt

1

which, under the assumed preferences, implies a constant employment N = (1 − α) 1+ϕ .

Notice, on the other hand, that the flexible price equilibrium in the small open economy

(with corresponding variables denoted with an upper bar) satisfies

1−

1

= MC t

ε

(1 − τ ) α U N (C t , N t )

=−

St

At

UC (C t , N t )

(1 − τ ) Y t ϕ

N t Ct

=

At

Ct

1+ϕ

= (1 − τ ) N t

.

Hence, by setting τ such that (1 − τ )(1 − α) = 1 − 1ε is satisfied (or, equivalently,

ν = µ + log(1 − α)) we guarantee the optimality of the flexible price equilibrium allocation.

As in the closed economy case, the optimal monetary policy requires stabilizing the output gap

(i.e. xt = 0, for all t). Equation (36) then implies that domestic prices are also stabilized under

that optimal policy (π H,t = 0 for all t). Thus, in the special case under consideration, (strict)

domestic inflation targeting (DIT) is indeed the optimal policy.

4.1. Implementation and macroeconomic implications

In this section we discuss the implementation and characterize the equilibrium processes for a

number of variables of the small open economy, under the assumption of a domestic inflation

20. Condition σ = η = 1 corresponds to the one required in the two-country framework of Benigno and Benigno

(2003). Our model of a small open economy in a multicountry world requires, in addition, that the substitutability (in the

home consumer’s preferences) between goods produced in any two foreign countries is also unity (i.e. γ = 1).

GALÍ & MONACELLI

SMALL OPEN ECONOMY

721

targeting policy (DIT). While we have shown that policy to be optimal only for the special case

considered above, in this subsection we look at the implications of that policy for the general

case.

4.1.1. Implementation. As discussed above full stabilization of domestic prices implies

xt = π H,t = 0

for all t. This in turn implies that yt = y t and rt = rr t will hold in equilibrium for all t, with all

the remaining variables matching their natural level all the time.

Interestingly, however, rt = rr t cannot be interpreted as a “rule” that the central bank could

follow mechanically in order to implement the optimal allocation. For, while xt = π H,t = 0

would certainly constitute an equilibrium in that case, the same equilibrium would not be

unique; instead, multiple equilibria and the possibility of stationary sunspot fluctuations may

arise. The previous result should not be surprising given the equivalence shown above between

the dynamical system describing the equilibrium of the small open economy and that of the

closed economy, and given the findings in the related closed economy literature. In particular,

and as shown in Appendix C, we can invoke that literature to point to a simple solution to that

problem. In particular, the indeterminacy problem can be avoided, and the uniqueness of the

optimal equilibrium allocation restored, by having the central bank follow a rule which would

imply that the interest rate should respond to domestic inflation and/or the output gap were those

variables to deviate from their (zero) target values. More precisely, suppose that the central bank

commits itself to the rule

rt = rr t + φπ π H,t + φx xt .

(38)

As shown by Bullard and Mitra (2002), if we restrict ourselves to non-negative values of φπ

and φx , a necessary and sufficient condition for uniqueness of the optimal allocation is given by

κα (φπ − 1) + (1 − β) φx > 0.

(39)

Notice that, once uniqueness is restored, the term φπ π H,t + φx xt appended to the interest

rate rule vanishes, implying that rt = rr t for all t. Thus, we see that stabilization of the output

gap and inflation requires a credible threat by the central bank to vary the interest rate sufficiently

in response to any deviations of inflation and/or the output gap from the target; yet, the very

existence of that threat makes its effective application unnecessary.

4.1.2. Macroeconomic implications. Under strict domestic inflation targeting (DIT), the

behaviour of real variables in the small open economy corresponds to the one we would observe

in the absence of nominal frictions. Hence, we see from inspection of equation (35) that domestic

output always increases in response to a positive technology shock at home.

The sign of the response to a rise in world output is ambiguous, however, and it depends on

the sign of 2, as shown in (35). To obtain some intuition for the forces at work notice first that

the natural level of the terms of trade is given by

s t = σα (y t − yt∗ )

= σα + σα 0 at − σα 8 yt∗

where 8 ≡ σσα+ϕ

+ϕ > 0. Thus, an increase in world output always generates an improvement in the

terms of trade (i.e. a real appreciation). The resulting expenditure-switching effect, together with

the effect of the real appreciation on domestic consumption through the risk sharing transfer of

resources (see (17)), tends to reduce aggregate demand and domestic economic activity. For any

given terms of trade, that effect is offset to a lesser or greater extent by a positive direct demand

722

REVIEW OF ECONOMIC STUDIES

effect (resulting from higher exports) as well as by a positive effect on domestic consumption

associated with international risk sharing (and given the implied higher world consumption). It

can be easily checked that the contractionary (expansionary) effect dominates whenever ω > 1

(ω < 1). In the special case considered above ω = 1, thus implying that a change in world output

leaves the terms of trade and domestic output unchanged under DIT policy.

Given that under DIT domestic prices are fully stabilized, it follows that et = s t − pt∗ , i.e.

under the DIT regime the nominal exchange rate moves one-for-one with the (natural) terms of

trade and (inversely) with the world price level. In the limiting case of constant world prices,

the nominal exchange rate will inherit all the statistical properties of the (natural) terms of trade,

including its stationarity (and thus its reversion to a constant mean).21 Of course, stationarity

does not necessarily imply low volatility. In particular, in the case of constant world prices, the

volatility of the nominal exchange rate under DIT will be proportional to the volatility of the gap

between the natural level of domestic output (in turn related to productivity) and world output.

A high positive (negative) correlation between domestic productivity and world output will tend

to decrease (increase) the volatility of the nominal and real exchange rates.

In addition, we can also derive the implied equilibrium process for the level of the CPI.

Given the constancy of domestic prices it is given by

p t = α(et + pt∗ )

= α st .

Thus, we see that under domestic inflation targeting the CPI level will vary with the (natural)

terms of trade and will inherit its statistical properties. If the economy is very open, and if

domestic productivity (and hence the natural level of domestic output) is not much synchronized

with world output, CPI prices could potentially be highly volatile, even if the domestic price level

is constant.

4.2. The welfare costs of deviations from the optimal policy

Under the particular assumptions for which strict domestic inflation targeting has been shown

to be optimal (i.e. log utility and unit elasticity of substitution between goods of different

origin), it is possible to derive a second order approximation to the utility losses of the domestic

representative consumer resulting from deviations from the optimal policy. As we show in

Appendix D, those losses, expressed as a fraction of steady state consumption, can be written

as

i

(1 − α) X∞ t h ε 2

W=−

β

π H,t + (1 + ϕ) xt2 .

(40)

t=0

2

λ

Taking unconditional expectations on (40) and letting β → 1, the expected welfare losses

of any policy that deviated from strict inflation targeting can be written in terms of the variances

of inflation and the output gap:

i

(1 − α) h ε

V=−

var(π H,t ) + (1 + ϕ) var(xt ) .

(41)

2

λ

Below we make use of the previous approximation to assess the welfare implications of

alternative suboptimal monetary policy rules, and to rank those rules on welfare grounds.

21. The stationarity of the terms of trade is, in turn, an implication of the stationarity of the productivity differential

coupled with our assumption of complete asset markets.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

723

5. SIMPLE MONETARY POLICY RULES FOR THE SMALL OPEN ECONOMY

In the present section we analyse the macroeconomic implications of three alternative monetary

policy regimes for the small open economy. Two of the simple rules considered are stylized

Taylor-type rules. The first has the domestic interest rate respond systematically to domestic

inflation, whereas the second assumes that CPI inflation is the variable the domestic central

bank reacts to. The third rule we consider is one that pegs the effective nominal exchange rate.

Formally, the domestic inflation-based Taylor rule (DITR, for short) is specified as follows:

rt = ρ + φπ π H,t .

The CPI inflation-based Taylor rule (CITR, for short) is assumed to take the form

rt = ρ + φπ πt .

Finally, the exchange rate peg (PEG, for short) implies

et = 0

for all t.

Below we provide a comparison of the equilibrium properties of several macroeconomic

variables under the above simple rules for a calibrated version of our model economy. We

compare such properties to those associated with a strict domestic inflation targeting (DIT),

the policy that is optimal under the conditions discussed above, and which we assume to be

satisfied in our baseline calibration. We next briefly describe the calibration strategy underlying

that exercise.

5.1. A numerical analysis of alternative rules

5.1.1. Calibration. In this section we present some quantitative results based on a

calibrated version of our model economy. Let us first state the main assumptions underlying

our baseline calibration, which we take as a benchmark. We set σ = η = γ = 1, in a way

consistent with the special case considered above. We assume ϕ = 3, which implies a labour

supply elasticity of 31 , and a value for the steady state mark-up µ = 1·2, which implies that ε, the

elasticity of substitution between differentiated goods (of the same origin), is 6. Parameter θ is set

equal to 0·75, a value consistent with an average period of one year between price adjustments.

We assume β = 0·99, which implies a riskless annual return of about 4% in the steady state.

We set a baseline value for α (or degree of openness) of 0·4. The latter corresponds roughly

to the import/GDP ratio in Canada, which we take as a prototype small open economy. In the

calibration of the interest rate rules we follow the original Taylor estimate and set φπ equal to

1·5, while ρ = (0·99)−1 − 1.

In order to calibrate the stochastic properties of the exogenous driving forces, we fit AR(1)

processes to (log) labour productivity in Canada (our proxy for domestic productivity), and (log)

U.S. GDP (our proxy for world output), using quarterly, HP-filtered data over the sample period

1963:1–2002:4. We obtain the following estimates (with standard errors in parantheses):

at = 0·66 at−1 + εta ,

σa = 0·0071

∗

+ εt∗ ,

yt∗ = 0·86 yt−1

σ y ∗ = 0·0078

(0·06)

(0·04)

with corr(εta , εt∗ ) = 0·3.

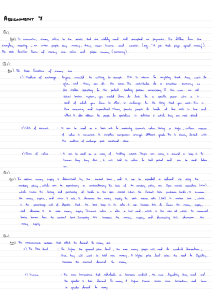

5.1.2. Impulse responses. We start by describing the dynamic effects of a domestic

productivity shock on a number of macroeconomic variables. Figure 1 displays the impulse

724

REVIEW OF ECONOMIC STUDIES

Optimal

DITR

Domestic inflation

0.4

CITR

PEG

Output gap

0·5

0.2

0

0

– 0·5

–0·2

–0·4

0

5

10

15

20

CPI inflation

0·4

–1

0

5

10

15

20

15

20

15

20

15

20

Terms of trade

1

0.2

0

0·5

–0·2

–0·4

0

5

10

15

20

Nominal exchange rate

1

0

0

5

10

Nominal interest rate

0·1

0

0

–0·1

–1

–0·2

–2

0

5

10

15

20

Domestic price level

0·5

–0·3

0

0

–0·5

–0·5

–1

–1

0

5

10

15

20

–1·5

0

10

CPI level

0·5

0

–1·5

5

5

10

F IGURE 1

Impulse responses to a domestic productivity shock under alternative policy rules

responses to a unit innovation in at under the four regimes considered. By construction, domestic

inflation and the output gap remain unchanged under the optimal policy (DIT). We also see that

the shock leads to a persistent reduction in the domestic interest rate as it is needed in order

to support the transitory expansion in consumption and output consistent with the flexible price

equilibrium allocation. Given the constancy of the world nominal interest rate, uncovered interest

parity implies an initial nominal depreciation followed by expectations of a future appreciation,

as reflected in the response of the nominal exchange rate. Relative to all other regimes, the

constancy of domestic prices accounts for a larger real depreciation and therefore for a further

expansion in demand and output through a rise in net exports (not shown here). Given constant

world prices and the stationarity of the terms of trade, the constancy of domestic prices implies

a mean-reverting response of the nominal exchange rate.

It is interesting to contrast the implied dynamic behaviour of the same variables under the

optimal policy to the one under the two stylized Taylor rules (DITR and CITR). Notice, at first,

that both rules generate, unlike the optimal policy, a permanent fall in both domestic and CPI

GALÍ & MONACELLI

SMALL OPEN ECONOMY

725

prices. The unit root in domestic prices is then mirrored, under both rules, by the unit root in the

nominal exchange rate.

A key difference between the two Taylor rules concerns the behaviour of the terms of trade.

While under DITR the terms of trade depreciate on impact and then start immediately to revert

to steady state (mirroring closely the response under the optimal policy), under CITR the initial

response of the terms of trade is more muted, and is followed by a hump-shaped pattern. The

intuition is simple. Under both rules, the rise in domestic productivity and the required real

depreciation lead, for given domestic prices, to an increase in CPI inflation. However, under

CITR the desired stabilization of CPI inflation is partly achieved, relative to DITR, by means of

a more muted response of the terms of trade (since the latter affect the CPI), and a fall in domestic

prices. The fall in prices, in turn, requires a negative output gap and hence a more contractionary

monetary policy (i.e. a higher interest rate). Under our calibration the latter takes the form of

an initial rise in both nominal and real interest rates, with the subsequent path of the real rate

remaining systematically above that implied by the optimal policy or a DITR policy.22

Finally, the same figure displays the corresponding impulse responses under a PEG. Notice

that the responses of output gap and inflation are qualitatively similar to the CITR case. However,

the impossibility of lowering the nominal rate and letting the currency depreciate, as would be

needed in order to support the expansion in consumption and output required in order to replicate

the flexible price allocation, leads to a very limited response in the terms of trade, and in turn to an

amplification of the responses of domestic inflation and output gap. Interestingly, under a PEG,

the complete stabilization of the nominal exchange rate generates stationarity of the domestic

price level and, in turn, also of the CPI level (given the stationarity in the terms of trade). This is

a property that the PEG regime shares with the optimal policy as specified above. The stationarity

in the price level also explains why, in response to the shock, domestic inflation initially falls and

then rises persistently above the steady state.

As discussed below, the different dynamics of the terms of trade are unambiguously

associated with a welfare loss, relative to the optimal policy.23

5.1.3. Second moments and welfare losses. In order to complement our quantitative

analysis, Table 1 reports business cycle properties of several key variables under alternative

monetary policy regimes. The numbers confirm some of the findings that were already evident

from visual inspection of the impulse responses. Thus we see that the critical element that

distinguishes each simple rule relative to the optimal policy is the excess smoothness of both

the terms of trade and the (first differenced) nominal exchange rate.24 This in turn is reflected in

too high a volatility of the output gap and domestic inflation under the simple rules. In particular,

the PEG regime is the one that amplifies both output gap and inflation volatility to the largest

extent, with the CITR regime lying somewhere in between. Furthermore, notice that the terms

of trade are more stable under an exchange rate peg than under any other policy regime. That

finding, which is consistent with the evidence of Mussa (1986), points to the existence of “excess

smoothness” in real exchange rates under fixed exchange rates. That feature is a consequence of

22. The implied pattern for the nominal rate is still consistent with the observed depreciation of the nominal

exchange rate on impact. It is, in fact, the behaviour of current and expected future interest rate differentials that

matters for the current nominal exchange rate, as can be easily seen by solving the uncovered interest parity condition

forward.

23. We display our results on welfare later. Notice, however, that the cost of dampening exchange rate volatility

(and therefore the relative ranking between DITR and CITR) may be a function of the lags with which exchange rate

movements affect prices, i.e. of the degree of pass-through. Intuitively, the lower the degree of pass-through, the smaller

(ceteris paribus) the cost of short-run relative price inertia, and therefore the more desirable to pursue a policy of CITR

relative to DITR.

24. We report statistics for the nominal depreciation rate, as opposed to the level, given that both DITR and CITR

imply a unit root in the nominal exchange rate.

726

REVIEW OF ECONOMIC STUDIES

TABLE 1

Cyclical properties of alternative policy regimes

Output

Domestic inflation

CPI inflation

Nominal infl. rate

Terms of trade

Nominal depr. rate

Optimal

sd%

DI Taylor

sd%

CPI Taylor

sd%

Peg

sd%

0·95

0·00

0·38

0·32

1·60

0·95

0·68

0·27

0·41

0·41

1·53

0·86

0·72

0·27

0·27

0·41

1·43

0·53

0·86

0·36

0·21

0·21

1·17

0·00

Note: Sd denotes standard deviation in %.

TABLE 2

Contribution to welfare losses

DI Taylor

CPI Taylor

Benchmark µ = 1·2, ϕ = 3

Var(Domestic infl.)

0·0157

0·0151

Var(Output gap)

0·0009

0·0019

Total

0·0166

0·0170

Peg

0·0268

0·0053

0·0321

Low steady state mark-up µ = 1·1, ϕ = 3

Var(Domestic infl.)

0·0287

0·0277

0·0491

Var(Output gap)

0·0009

0·0019

0·0053

Total

0·0297

0·0296

0·0544

Low elasticity of labour supply µ = 1·2, ϕ = 10

Var(Domestic infl.)

0·0235

0·0240

0·0565

Var(Output gap)

0·0005

0·0020

0·0064

Total

0·0240

0·0261

0·0630

Low mark-up and elasticity of labour supply µ = 1·1, ϕ = 10

Var(Domestic infl.)

0·0431

0·0441

0·1036

Var(Output gap)

0·0005

0·0020

0·0064

Total

0·0436

0·0461

0·1101

Note: Entries are percentage units of steady state consumption.

the inability of prices (which are sticky) to compensate for the constancy of the nominal exchange

rate.25

Table 2 reports the welfare losses associated with the three simple rules analysed in the

previous section: DITR, CITR, and PEG. There are four panels in this table. The top panel

reports welfare losses in the case of our benchmark parameterization, while the remaining three

panels display the effects of lowering, respectively, the steady state mark-up, the elasticity of

labour supply and both. All entries are to be read as percentage units of steady state consumption,

and in deviation from the first best represented by DIT. Under our baseline calibration all rules

are suboptimal since they involve non-trivial deviations from full domestic price stability. Also

one result stands out clearly: under all the calibrations considered an exchange rate peg implies

a substantially larger deviation from the first best than DITR and CITR, as one may have

anticipated from the quantitative evaluation of the second moments conducted above. However,

and as is usually the case in welfare exercises of this sort found in the literature, the implied

welfare losses are quantitatively small for all policy regimes.

We consider next the effect of lowering, respectively, the steady state mark-up to 1·1, by

setting ε = 11 (which implies a larger penalization of inflation variability in the loss function)

25. See Monacelli (2004) for a detailed analysis of the implications of fixed exchange rates.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

727

and the elasticity of labour supply to 0·1 (which implies a larger penalization of output gap

variability). This has a general effect of generating a substantial magnification of the welfare

losses relative to the benchmark case, especially in the third exercise where the two parameters

are lowered simultaneously. In the case of low mark-up and low elasticity of labour supply,

the PEG regime leads to non-trivial welfare losses relative to the optimum. Notice also that

under all scenarios considered here the two stylized Taylor rules, DITR and CITR, imply

very similar welfare losses. While this points to a substantial irrelevance in the specification

of the inflation index in the monetary authority’s interest rate rule, the same result may once

again be sensitive to the assumption of complete exchange rate pass-through specified in our

context.26

6. SUMMARY AND CONCLUDING REMARKS

The present paper has developed and analysed a tractable optimizing model of a small open

economy with staggered price setting à la Calvo. We have shown that the equilibrium dynamics

for that model economy have a canonical representation (in terms of domestic inflation and

the output gap) analogous to that of its closed economy counterpart. More precisely, their

representations differ only in two respects: (a) some coefficients of the equilibrium dynamical

system for the small open economy depend on parameters that are specific to the latter (the

degree of openness, and the substitutability across goods produced in different countries), and

(b) the natural levels of output and interest rates in the small open economy are generally a

function of both domestic and foreign disturbances. In particular, the closed economy is nested

in the small open economy model, as a limiting case.

Under some special—but not implausible—assumptions (log utility and unit elasticity of

substitution between bundles of goods produced in different countries) we have shown how a

second order approximation to the utility of the small open economy’s consumer can be derived,

and the welfare level implied by alternative monetary policy rules can be evaluated. In that case,

the implied loss function is analogous to the one applying to the corresponding closed economy,

i.e. it penalizes fluctuations in domestic inflation and the output gap. In particular, under our

assumptions, domestic inflation targeting emerges as the optimal policy regime.

We have then used our framework to analyse the properties of three alternative monetary

regimes for the small open economy: (a) a domestic inflation-based Taylor rule, (b) a CPI-based

Taylor rule, and (c) an exchange rate peg. Our analysis points to the presence of a trade-off

between the stabilization of both the nominal exchange rate and the terms of trade, on the one

hand, and the stabilization of domestic inflation and the output gap on the other. Hence a policy of

domestic inflation targeting, which achieves a simultaneous stabilization of both domestic prices

and the output gap, entails a substantially larger volatility of the nominal exchange rate and the

terms of trade relative to the simple Taylor rules and/or an exchange rate peg. The converse is true

for the latter regime. In general, a CPI-based Taylor rule delivers equilibrium dynamics that lie

somewhere between a domestic inflation-based Taylor rule and a peg. Perhaps not surprisingly,

an exchange rate peg generates substantially higher welfare losses than a Taylor rule, due to the

excess smoothness of the terms of trade that it entails. In all our simulations, a Taylor rule in

which the monetary authority reacts to domestic inflation is shown to deliver higher welfare than

a similar rule based on the CPI index of inflation.

Our framework lends itself to several extensions. First, it is important to emphasize that,

in our analysis, domestic price stability (along with fully flexible exchange rates) stands out

26. In the context of a different model, with both tradable and non-tradable goods and capital accumulation,

Schmitt-Grohé and Uribe (2001) point out that the welfare ranking between domestic and CPI targeting may be sensitive

to the specification of other distortions in the economy, for instance, the adoption of a transaction role for money.

728

REVIEW OF ECONOMIC STUDIES

as the welfare maximizing policy in the particular case of log utility and unitary elasticity of

substitution (both between domestic and foreign goods in general and between different foreign

countries’ goods), coupled with an appropriate subsidy scheme that guarantees the optimality

(from the viewpoint of the small open economy) of the flexible price equilibrium allocation. The

derivation of the relevant welfare function for the small open economy in the case of more general

preferences as well as that of uncorrected steady state distortions would allow a more thorough

analysis and quantitative evaluation of the optimal monetary policy and should certainly be the

object of future research.27

Second, a two-country version of the framework developed here would allow us to analyse

a number of issues that cannot be addressed with the present model, including the importance of

spillover effects in the design of optimal monetary policy, the potential benefits from monetary

policy coordination, and the implications of exchange rate stabilization agreements. Recent work

by Clarida et al. (2002), Benigno and Benigno (2003) and Pappa (2004) has already made some

inroads on that front.

A further interesting extension would involve the introduction, along with sticky prices,

of sticky nominal wages in the small open economy. As pointed out by Erceg, Henderson and

Levine (2000), the simultaneous presence of the two forms of nominal rigidity introduces an

additional trade-off that renders strict price inflation targeting policies suboptimal. It may be

interesting to analyse how that trade-off would affect the ranking across monetary policy regimes

obtained in the present paper.

Finally, it is worth noticing that our analysis features complete exchange rate pass-through

of nominal exchange rate changes to prices of imported (or exported) goods. Some of the

implications of less than complete pass-through associated with local currency pricing by

exporters and importers have already been analysed by several authors in the context of twocountry models with one-period advanced price-setting (see, e.g. Devereux and Engel (2002),

Bacchetta and van Wincoop (2003), and Corsetti and Pesenti (2005)). It would be interesting to

explore some of those implications (e.g. for the nature of the optimal monetary policy problem

and the relative performance of alternative policy regimes) in the context of the simple small

open economy with staggered price-setting proposed here.

APPENDIX A. THE PERFECT FORESIGHT STEADY STATE

In order to show how the home economy’s terms of trade are uniquely pinned down in the perfect foresight steady state,

we invoke symmetry among all countries (other than the home country), and then show how the terms of trade and output

in the home economy are determined. Without loss of generality, we assume a unit value for productivity in all foreign

countries, and a productivity level A in the home economy. We show that in the symmetric case (when A = 1) the

terms of trade for the home economy must necessarily be equal to unity in the steady state, whereas output in the home

economy coincides with that in the rest of the world.

First, notice that the goods market clearing condition, when evaluated at the steady state, implies

!−γ

!−η

Z 1

PFi

PH −η

PH

Y = (1 − α)

C +α

C i di

P

Pi

Ei PFi

0

!γ −η

Z 1

Ei PFi

PH −η

η i

=

(1 − α) C + α

Qi C di

P

PH

0

#

"

Z 1

γ −η η− 1

η

i

σ

di

= h(S) C (1 − α) + α

S Si

Qi

0

1

= h(S)η C (1 − α) + αS γ −η q(S)η− σ

27. See Benigno and Woodford (2004) for recent developments in this direction.

GALÍ & MONACELLI

SMALL OPEN ECONOMY

729

where we have made use of (17) and of the relationship

"

# 1

Z 1

1−η

P

1−η

= (1 − α) + α

di

(Si )

PH

0

h

i 1

= (1 − α) + α (S)1−η 1−η ≡ h(S)

and we have made the substitution Q = h(SS ) ≡ q(S). Notice that q(S) is strictly increasing in S.

Under the assumptions above, the international risk sharing condition implies that the relationship

1

C = C∗ Q σ

1

= C ∗ q(S) σ

must also hold in the steady state.

Hence, combining the two relations above, and imposing the world market clearing condition C ∗ = Y ∗ we obtain

1

Y = (1 − α) h(S)η q(S) σ + α S γ −η h(S)η q(S)η Y ∗

1

= (1 − α) h(S)η q(S) σ + α h(S)γ q(S)γ Y ∗

(A.1)

≡ v(S) Y ∗

(A.2)

where v(S) > 0, v 0 (S) > 0, and v(1) = 1.

Furthermore, the clearing of the labour market in the steady state implies

ϕ

Y

W

Cσ

=

A

P

= A

1 − 1ε PH

(1 − τ ) P

= A

1 − 1ε

1

(1 − τ ) h(S)

which, when combined with the sharing condition above, yields

Y =A

1+ϕ

ϕ

1 − 1ε

(1 − τ ) (Y ∗ )σ S

!1

ϕ

.

(A.3)

Notice that, conditional on A and Y ∗ , (A.2) and (A.3) constitute a system of two equations in Y and S, with a

unique solution, given by

! 1

1+ϕ

1 − 1ε σ +ϕ

∗

σ

+ϕ

Y =Y = A

1−τ

and

S=1

which in turn must imply Si = 1 for all i.

APPENDIX B. OPTIMAL PRICE-SETTING IN THE CALVO MODEL