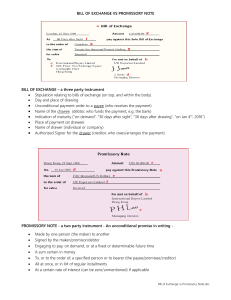

28 Student: ___________________________________________________________________________ 1. Which of the following are not negotiable instruments? A. Cheques. B. Certified cheques. C. A cheque made payable to "Mickey Mouse." D. A promissory note. E. A bill of sale. 2. The most superior position in which parties to a negotiable instrument can find themselves is a(n) A. endorser. B. holder. C. holder for value. D. holder in due course. E. holder in any event. 3. A consumer note arises when A. any consumer purchase is made on the basis of a promissory note. B. the lender of funds to the consumer is not at arm's length with the seller. C. the purchaser acts as an end-user and not as a purchaser for resale, and the goods are obtained by credit. D. a debt under a negotiable instrument representing a consumer purchase is assigned to a finance company. E. None of the responses are correct. 4. Which is a true statement? A. Real defences are effective against holders, holders in due course, and endorsers. B. Defect of title defences are effective against holders and endorsers. C. Personal defences are effective against holders, and against endorsers if they are an immediate party. D. All of the responses are true. E. None of the responses are true. 5. Once a bill is drawn it is sent to the ___________ for ___________. Before the date for payment it may be negotiated to others, called _______________ by way of ___________. A. maker; endorsement; holders; exchange B. drawee; endorsement; endorsers; acceptance C. drawee; payment; endorsers; endorsement D. drawee; acceptance; holders; endorsement E. maker; acceptance; endorsers; endorsement 6. A paper reads: To: Empire Bank. Five days after the next full moon, pay to Nathan Montrose or anyone named by him the sum of $500. Signed: "Monica Traymoor," August 15, 2007. Most correctly, this is A. a bill of exchange. B. a negotiable instrument. C. a promissory note. D. a banker's acceptance. E. a bill of exchange and a negotiable instrument. 7. A certified cheque is A. a promissory note. B. legal tender. C. a liability of the bank and not the drawer. D. provided for under the Bills of Exchange Act. E. All of these elements. 8. Where a bill of exchange is used in a purchase and sale transaction for goods sold on credit terms, the bill is "accepted" by the A. seller. B. buyer. C. seller's bank. D. buyer's bank. E. None of these are the acceptor. 9. Where a cheque is made payable to Lucien Colbert, and on its reverse are written the words "For deposit only to the credit of L. Colbert," A. the endorsement is a restrictive endorsement. B. the endorsement is a special endorsement. C. the endorsement is a failure. D. the bill can only be cashed. E. None of the responses are correct. 10. Law relating to certified cheques in Canada are found in A. the Bank Act. B. the Bills of Exchange Act. C. provincial statutes. D. Common Law. E. None of the responses are correct. 11. Bill writes Nick a cheque for $500 on his account at the Friendly Bank. Bill is the _______ and Nick is the __________ and the Friendly Bank is the ______________. A. Drawer; Payee; Drawee B. Drawer; Drawee; Payee C. Drawee; Drawer; Payee D. Drawee; Payee; Drawer E. Payee; Drawer; Drawee 12. Erin writes Lorie a promissory note for $500. Erin is the _________ and Lorie is the ________. A. Promisor; Promisee B. Promisee; Promisor C. Maker; Bearer D. Bearer; Maker E. Bearer; Drawee 13. The legislation creating promissory notes is found in which statute? A. Promissory Notes Act B. Bills of Exchange Act C. Securities Act D. Financial Instruments Act E. Personal Property Security Act 14. Does a bill of exchange have to be written? A. No, in accordance with the Statute of Frauds. B. No, in accordance with the Common Law. C. No, in accordance with the Personal Property Security Act. D. No, in accordance with the Bills of Exchange Act. E. Yes, in accordance with the Bills of Exchange Act. 15. Who can the holder of a bill of exchange sue if it is dishonoured? A. Drawer B. Acceptor C. Endorser D. Drawer and Acceptor E. Drawer, Acceptor and Endorser 16. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. The acceptance of the cheque by the sales clerk constitutes payment of the debt in full. True False 17. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. The cheque is only conditional payment, and remains so until the cheque is honoured by Magda's bank. True False 18. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. If Magda had presented a certified cheque as payment, the acceptance of the cheque would extinguish the debt. True False 19. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. If the clothing shop owner took Magda's cheque to the bank, and had it certified, Magda's debt to the seller would be extinguished. True False 20. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. Brendan may contact the bank upon which the cheque was drawn, and countermand payment of the cheque. The bank must thereafter refuse payment of the cheque if it should be presented for payment. True False 21. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. If Joey found Brendan's cheque by accident, and presented it for payment, Brendan might resist payment on the basis of lack of delivery. True False 22. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. If the cheque was not found for over six months, the bank should refuse payment, even if it was presented by the payee, Joey. True False 23. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. If the cheque had been made payable to "Humpty Dumpty" instead of Joey, any finder of the cheque would be entitled to demand payment. True False 24. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If Henry should default on the note, Iso Motors may take legal action against Henry either on the contract of sale, or on the promissory note. True False 25. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If the promissory note is properly drawn and signed by Henry, Iso Motors may negotiate it to Friendly Finance Company. True False 26. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If the promissory note is negotiated to Friendly Finance Company, the company (as a holder), may enforce payment. True False 27. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If the automobile is a consumer purchase, the note must be marked "consumer note." True False 28. A bill payable "three days after sight," presented on March 20th is payable on March 23rd. True False 29. The maker of a bill of exchange may raise a defect of title defence successfully against a holder in due course. True False 30. Where neither Smith nor Jones are mere holders, Smith may successfully raise a defect of title defence, Jones must be an endorser. True False 31. Where neither Smith nor Jones are mere holders, Smith may successfully raise a defect of title defence, Jones must be an endorser. Smith must be a holder in due course. True False 32. In the absence of defects, once certified, liability for payment of a cheque shifts from the drawer to the financial institution. True False 33. Situations exist where the holder of a bill may validly negotiate it to another without endorsement or incurring liability under it. True False 34. Kara in Toronto has received a cheque from Pam in Vancouver, which Kara endorses with her signature and the words "Pay to John Black only," and mails it to John Black in Halifax. Black takes it to his bank to cash. The bank will refuse to do so. True False 35. Where a financial transaction involves bills of exchange moving between New York, London, and Montreal, it must be very carefully structured to avoid being crippled by differing legislation in each jurisdiction. True False 36. Generally speaking, all cheques are bills of exchange, the reverse is untrue, and promissory notes differ in form and use from either one. True False 37. An instrument that conforms in all other respects to the Bills of Exchange Act except that it reads "Pay to the bearer on demand $500 in gold bullion based on the London noon gold spot price on date of demand," would still not be either a bill of exchange or promissory note. True False 38. The law governing negotiable instruments is the Bills of Exchange Act. True False 39. The Constitution assigns jurisdiction relating to the governance of negotiable instruments to the federal Parliament. True False 40. Under the Bills of Exchange Act, a negotiable instrument is void ab initio where it attempts to create a debtor-creditor relationship between the parties to it. True False 41. A single person cannot simultaneously be an endorsee, holder, and bearer of a negotiable instrument. True False 42. A holder in due course has much greater certainty of payment under a negotiable instrument than an ordinary holder. True False 43. List and describe the real defences to payment of a negotiable instrument. 44. Explain the different types of endorsement that may appear on a negotiable instrument, and give examples of their proper use. 45. Discuss the ways in which the principles of consumer protection have been incorporated into the Bills of Exchange Act, and obligations imposed by the Act on consumer transactions. 46. Discuss why presentment of a cheque for certification by the payee discharges liability of the drawer, but presentment of a cheque for certification by its drawer may not. 47. David operated a small delivery business. He approached the Empire Bank for money to buy a truck to be used in the business. The bank was willing to loan David the money, and took a chattel mortgage over the truck. As further security in the event that David defaulted on the mortgage, the bank required his wife to sign a promissory note for the full amount of the mortgage. After experiencing some financial difficulty, David defaulted on the mortgage and the Empire Bank took possession of the truck and sold it pursuant to the chattel mortgage. The passage of sale was insufficient to cover the full amount of the loan and the bank sued David's wife for the remainder owing on the basis of the promissory note. Discuss the rights and duties of the bank and David's wife, and render a decision. 48. Joan made a promissory note payable in the amount of $1,000 to Thomas. Since Thomas owed approximately $1,000 to an acquaintance, William, Thomas gave the note to William having inscribed on the back of it "I transfer all my rights in this note." William was not aware of the provisions in the Bills of Exchange Act. When William attempted to collect upon the promissory note from Joan, it was dishonoured, and the bank told William it did not know of Joan's whereabouts. William sought recourse against Thomas on the basis of his endorsement. Thomas pleaded he had transferred his rights in the note to William without any warranty or recourse, and the endorsement constituted only an assignment of his interest in the note and not an endorsement under the terms of the Bills of Exchange Act. Discuss the issues raised in this case and render a decision. 49. Hector had planned a new business venture, and Thomson was interested in participating in it. Thomson felt that it would take her four weeks to determine whether she could fully devote her time to the business. As the success of the venture depended on an immediate start, Hector was reluctant to include Thomson. To convince Hector of her sincerity, Thomson offered to provide him with a cheque for $5,000, which he could cash if she decided to back out of the project within four weeks. Hector agreed, and Thomson gave him the cheque fully completed and with the current date marked: "to be cashed only if deal cancelled." As matters turned out, Thomson decided only a day later that she could not devote the time to participate in the venture. She told Hector that she was backing out, and attended at the bank and placed a stop payment on the cheque. The cheque was duly dishonoured when Hector tried to cash it, and he sued Thomson pursuant to the Bills of Exchange Act for the $5,000. His claim was also for a further $1,000 that he was forced to pay as a fee to a broker for finding him another investor on short notice. Discuss. 28 Key 1. Which of the following are not negotiable instruments? A. Cheques. B. Certified cheques. C. A cheque made payable to "Mickey Mouse." D. A promissory note. E. A bill of sale. Difficulty: Easy Willes - Chapter 28 #1 2. The most superior position in which parties to a negotiable instrument can find themselves is a(n) A. endorser. B. holder. C. holder for value. D. holder in due course. E. holder in any event. Difficulty: Easy Willes - Chapter 28 #2 3. A consumer note arises when A. any consumer purchase is made on the basis of a promissory note. B. the lender of funds to the consumer is not at arm's length with the seller. C. the purchaser acts as an end-user and not as a purchaser for resale, and the goods are obtained by credit. D. a debt under a negotiable instrument representing a consumer purchase is assigned to a finance company. E. None of the responses are correct. Difficulty: Easy Willes - Chapter 28 #3 4. Which is a true statement? A. Real defences are effective against holders, holders in due course, and endorsers. B. Defect of title defences are effective against holders and endorsers. C. Personal defences are effective against holders, and against endorsers if they are an immediate party. D. All of the responses are true. E. None of the responses are true. Difficulty: Moderate Willes - Chapter 28 #4 5. Once a bill is drawn it is sent to the ___________ for ___________. Before the date for payment it may be negotiated to others, called _______________ by way of ___________. A. maker; endorsement; holders; exchange B. drawee; endorsement; endorsers; acceptance C. drawee; payment; endorsers; endorsement D. drawee; acceptance; holders; endorsement E. maker; acceptance; endorsers; endorsement Difficulty: Moderate Willes - Chapter 28 #5 6. A paper reads: To: Empire Bank. Five days after the next full moon, pay to Nathan Montrose or anyone named by him the sum of $500. Signed: "Monica Traymoor," August 15, 2007. Most correctly, this is A. a bill of exchange. B. a negotiable instrument. C. a promissory note. D. a banker's acceptance. E. a bill of exchange and a negotiable instrument. Difficulty: Moderate Willes - Chapter 28 #6 7. A certified cheque is A. a promissory note. B. legal tender. C. a liability of the bank and not the drawer. D. provided for under the Bills of Exchange Act. E. All of these elements. Difficulty: Easy Willes - Chapter 28 #7 8. Where a bill of exchange is used in a purchase and sale transaction for goods sold on credit terms, the bill is "accepted" by the A. seller. B. buyer. C. seller's bank. D. buyer's bank. E. None of these are the acceptor. Difficulty: Easy Willes - Chapter 28 #8 9. Where a cheque is made payable to Lucien Colbert, and on its reverse are written the words "For deposit only to the credit of L. Colbert," A. the endorsement is a restrictive endorsement. B. the endorsement is a special endorsement. C. the endorsement is a failure. D. the bill can only be cashed. E. None of the responses are correct. Difficulty: Moderate Willes - Chapter 28 #9 10. Law relating to certified cheques in Canada are found in A. the Bank Act. B. the Bills of Exchange Act. C. provincial statutes. D. Common Law. E. None of the responses are correct. Difficulty: Moderate Willes - Chapter 28 #10 11. (p. 266) Bill writes Nick a cheque for $500 on his account at the Friendly Bank. Bill is the _______ and Nick is the __________ and the Friendly Bank is the ______________. A. Drawer; Payee; Drawee B. Drawer; Drawee; Payee C. Drawee; Drawer; Payee D. Drawee; Payee; Drawer E. Payee; Drawer; Drawee Difficulty: Challenging Willes - Chapter 28 #11 12. (p. 569) Erin writes Lorie a promissory note for $500. Erin is the _________ and Lorie is the ________. A. Promisor; Promisee B. Promisee; Promisor C. Maker; Bearer D. Bearer; Maker E. Bearer; Drawee Difficulty: Challenging Willes - Chapter 28 #12 13. (p. 562) The legislation creating promissory notes is found in which statute? A. Promissory Notes Act B. Bills of Exchange Act C. Securities Act D. Financial Instruments Act E. Personal Property Security Act Difficulty: Easy Willes - Chapter 28 #13 14. (p. 564) Does a bill of exchange have to be written? A. No, in accordance with the Statute of Frauds. B. No, in accordance with the Common Law. C. No, in accordance with the Personal Property Security Act. D. No, in accordance with the Bills of Exchange Act. E. Yes, in accordance with the Bills of Exchange Act. Difficulty: Easy Willes - Chapter 28 #14 15. (p. 565) Who can the holder of a bill of exchange sue if it is dishonoured? A. Drawer B. Acceptor C. Endorser D. Drawer and Acceptor E. Drawer, Acceptor and Endorser Difficulty: Moderate Willes - Chapter 28 #15 16. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. The acceptance of the cheque by the sales clerk constitutes payment of the debt in full. FALSE Difficulty: Easy Willes - Chapter 28 #16 17. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. The cheque is only conditional payment, and remains so until the cheque is honoured by Magda's bank. TRUE Difficulty: Easy Willes - Chapter 28 #17 18. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. If Magda had presented a certified cheque as payment, the acceptance of the cheque would extinguish the debt. FALSE Difficulty: Easy Willes - Chapter 28 #18 19. Magda purchased some new clothes at a clothing store, and gave the sales clerk a cheque for the price of the goods as payment. If the clothing shop owner took Magda's cheque to the bank, and had it certified, Magda's debt to the seller would be extinguished. TRUE Difficulty: Moderate Willes - Chapter 28 #19 20. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. Brendan may contact the bank upon which the cheque was drawn, and countermand payment of the cheque. The bank must thereafter refuse payment of the cheque if it should be presented for payment. TRUE Difficulty: Easy Willes - Chapter 28 #20 21. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. If Joey found Brendan's cheque by accident, and presented it for payment, Brendan might resist payment on the basis of lack of delivery. TRUE Difficulty: Moderate Willes - Chapter 28 #21 22. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. If the cheque was not found for over six months, the bank should refuse payment, even if it was presented by the payee, Joey. TRUE Difficulty: Easy Willes - Chapter 28 #22 23. Brendan prepared a cheque payable to Joey, and placed it in the pocket of his coat. Later in the day, while shopping, his coat was stolen. If the cheque had been made payable to "Humpty Dumpty" instead of Joey, any finder of the cheque would be entitled to demand payment. FALSE Difficulty: Moderate Willes - Chapter 28 #23 24. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If Henry should default on the note, Iso Motors may take legal action against Henry either on the contract of sale, or on the promissory note. TRUE Difficulty: Easy Willes - Chapter 28 #24 25. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If the promissory note is properly drawn and signed by Henry, Iso Motors may negotiate it to Friendly Finance Company. TRUE Difficulty: Easy Willes - Chapter 28 #25 26. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If the promissory note is negotiated to Friendly Finance Company, the company (as a holder), may enforce payment. TRUE Difficulty: Easy Willes - Chapter 28 #26 27. Henry purchased an automobile from Iso Motors, and as a part of the payment, gave Iso Motors a promissory note in the amount of $4,000. If the automobile is a consumer purchase, the note must be marked "consumer note." FALSE Difficulty: Easy Willes - Chapter 28 #27 28. A bill payable "three days after sight," presented on March 20th is payable on March 23rd. FALSE Difficulty: Easy Willes - Chapter 28 #28 29. The maker of a bill of exchange may raise a defect of title defence successfully against a holder in due course. FALSE Difficulty: Moderate Willes - Chapter 28 #29 30. Where neither Smith nor Jones are mere holders, Smith may successfully raise a defect of title defence, Jones must be an endorser. TRUE Difficulty: Moderate Willes - Chapter 28 #30 31. Where neither Smith nor Jones are mere holders, Smith may successfully raise a defect of title defence, Jones must be an endorser. Smith must be a holder in due course. FALSE Difficulty: Moderate Willes - Chapter 28 #31 32. In the absence of defects, once certified, liability for payment of a cheque shifts from the drawer to the financial institution. TRUE Difficulty: Easy Willes - Chapter 28 #32 33. Situations exist where the holder of a bill may validly negotiate it to another without endorsement or incurring liability under it. TRUE Difficulty: Moderate Willes - Chapter 28 #33 34. Kara in Toronto has received a cheque from Pam in Vancouver, which Kara endorses with her signature and the words "Pay to John Black only," and mails it to John Black in Halifax. Black takes it to his bank to cash. The bank will refuse to do so. TRUE Difficulty: Moderate Willes - Chapter 28 #34 35. Where a financial transaction involves bills of exchange moving between New York, London, and Montreal, it must be very carefully structured to avoid being crippled by differing legislation in each jurisdiction. FALSE Difficulty: Easy Willes - Chapter 28 #35 36. Generally speaking, all cheques are bills of exchange, the reverse is untrue, and promissory notes differ in form and use from either one. TRUE Difficulty: Moderate Willes - Chapter 28 #36 37. An instrument that conforms in all other respects to the Bills of Exchange Act except that it reads "Pay to the bearer on demand $500 in gold bullion based on the London noon gold spot price on date of demand," would still not be either a bill of exchange or promissory note. TRUE Difficulty: Moderate Willes - Chapter 28 #37 38. The law governing negotiable instruments is the Bills of Exchange Act. TRUE Difficulty: Easy Willes - Chapter 28 #38 39. The Constitution assigns jurisdiction relating to the governance of negotiable instruments to the federal Parliament. TRUE Difficulty: Easy Willes - Chapter 28 #39 40. Under the Bills of Exchange Act, a negotiable instrument is void ab initio where it attempts to create a debtor-creditor relationship between the parties to it. FALSE Difficulty: Easy Willes - Chapter 28 #40 41. A single person cannot simultaneously be an endorsee, holder, and bearer of a negotiable instrument. FALSE Difficulty: Moderate Willes - Chapter 28 #41 42. A holder in due course has much greater certainty of payment under a negotiable instrument than an ordinary holder. TRUE Difficulty: Moderate Willes - Chapter 28 #42 43. List and describe the real defences to payment of a negotiable instrument. Real Defences are those that go to the root of the instrument, and are effective against all holders, including holders in due course. They are: a. Forgery—if the signature of a maker, drawer, or endorser is forged, the holder may not enforce payment through the forged signature. b. Minority—a minor cannot incur liability under a negotiable instrument. c. Lack of Delivery of an Incomplete Instrument—both elements must be present; the maker or drawer must not have fully completed the instrument, and must not have delivered it. If a subsequent person obtains the instrument and completes it, the defence is effective against a claim for payment under it. d. Material alteration—a complete defence against the extent of the alteration, but not against the original terms. e. Fraud as to the Nature—the equivalent of non est factum, open to a person honestly believing upon signing the instrument that it was of a nature other than a negotiable instrument. f. Cancellation—must be apparent on the face of the instrument, and is only a sure defence where no early accidental payment has been made. Difficulty: Moderate Willes - Chapter 28 #43 44. Explain the different types of endorsement that may appear on a negotiable instrument, and give examples of their proper use. The following are the types of endorsement to a negotiable instrument: a. In Blank—endorser merely signs their name on the reverse, and the instrument becomes a bearer instrument. Most commonly used in the endorsement of cheques in the course of bank deposit. b. Restrictive Endorsement—prevents any further endorsement of the instrument. Commonly takes the form of "Deposit to the Credit of Payee Only." Most commonly used in the bank deposits of businesses, as security from theft by employees. c. Special Endorsement—halts further endorsement of an instrument until the endorsement of a particular individual appears on the instrument. Takes the form of "Pay to the order of J. Brown," on the reverse. Commonly used for security by holders at a distance, when one must send the instrument endorsed over to the other, but does not want to create a bearer instrument in the process. d. Endorsement without Recourse—an endorsement preventing subsequent endorsers from looking to that endorser for payment of the instrument on dishonour by the drawer. Very rarely would a cheque endorsed in this manner be accepted as a bank deposit. Takes the form of "J. Brown without recourse." e. Endorsement for identification—rarely used, this endorsement creates no liability, but is used to allay the fears of a subsequent recipient as to the identity of the holder, by an endorsement of a person known to the subsequent recipient who knows the holder. Takes the form of "J. Brown is hereby identified, J. Smith." Smith is known to the subsequent recipient, but incurs no liability, as he is only identifying Brown. Difficulty: Challenging Willes - Chapter 28 #44 45. Discuss the ways in which the principles of consumer protection have been incorporated into the Bills of Exchange Act, and obligations imposed by the Act on consumer transactions. In the 1970s, amendments to the Act resulted in explicit consumer protection provisions. These took the form of two new negotiable instruments, consumer bills and consumer notes, which were like their ordinary counterparts, but arose out of consumer purchases. The consumer purchase was defined as a non-cash sale from a person selling consumer goods and services to a person for personal use. The intent of the amendments was to circumvent the use of the privity rules of contract, where a person could not raise the defence of defective goods against a finance company that had purchased a note from a now "disappeared" seller. Often the assignment of notes had taken place at less than arm's length, but the purchaser was estopped from raising a defence. Now if the seller and the lender are not at arm's length, the consumer note or bill is caught by the Act, and the holder of such an instrument is subject to any defences that the purchaser could have raised against the seller if the goods are defective or unsatisfactory. Under the Act, any such note or bill must be marked as arising under a consumer purchase, to warn any other holders of this potential liability, and any note or bill not so marked is void as against the purchaser. Difficulty: Moderate Willes - Chapter 28 #45 46. Discuss why presentment of a cheque for certification by the payee discharges liability of the drawer, but presentment of a cheque for certification by its drawer may not. The answer is found in the passage quoted in the text. On presentment by the payee, who can take legal tender at that time, certification represents the payee's election to take the bank's undertaking to pay in place of that of the drawer. The drawer is therefore discharged. In the case of a cheque being presented for certification by the drawer, there is no delivery of payment to the payee, and the certification only represents the addition of a guarantor which the payee may choose to accept or reject on delivery, in favour of demanding legal tender. Difficulty: Challenging Willes - Chapter 28 #46 47. David operated a small delivery business. He approached the Empire Bank for money to buy a truck to be used in the business. The bank was willing to loan David the money, and took a chattel mortgage over the truck. As further security in the event that David defaulted on the mortgage, the bank required his wife to sign a promissory note for the full amount of the mortgage. After experiencing some financial difficulty, David defaulted on the mortgage and the Empire Bank took possession of the truck and sold it pursuant to the chattel mortgage. The passage of sale was insufficient to cover the full amount of the loan and the bank sued David's wife for the remainder owing on the basis of the promissory note. Discuss the rights and duties of the bank and David's wife, and render a decision. The promissory note is void and unenforceable against David's wife. Her liability on the note is only conditional upon the default in the chattel mortgage. As the bill of exchange requires promissory note to be unconditional promise to pay, among other things, it does not fall within the meaning of the Act requiring a promissory note to be unconditional. Based on: Bank of Montreal v. Faulkner (1983), 43 Nfld. & P.E.I.R. 256 (Nfld. Dist. Ct.). Difficulty: Moderate Willes - Chapter 28 #47 48. Joan made a promissory note payable in the amount of $1,000 to Thomas. Since Thomas owed approximately $1,000 to an acquaintance, William, Thomas gave the note to William having inscribed on the back of it "I transfer all my rights in this note." William was not aware of the provisions in the Bills of Exchange Act. When William attempted to collect upon the promissory note from Joan, it was dishonoured, and the bank told William it did not know of Joan's whereabouts. William sought recourse against Thomas on the basis of his endorsement. Thomas pleaded he had transferred his rights in the note to William without any warranty or recourse, and the endorsement constituted only an assignment of his interest in the note and not an endorsement under the terms of the Bills of Exchange Act. Discuss the issues raised in this case and render a decision. If a person attempts to endorse or negotiate a note, and it intends to avoid future liability under that note, there must be a clear indication of restrictive endorsement. When Thomas endorsed this note, the fact that he wrote that he transferred all his rights is implicitly understood in the Act, the question remaining whether he restricts, in so doing, any of his liability under the note. As there is no restrictive element in this endorsement, the words do not expressly or impliedly negate some right that would accrue to the endorsee by the signature itself. In this case, the endorsement is simply an ordinary endorsement that happens to be in a much more elaborate form. Based on: Petsanis v. Durocher (1929), 35 R.L.N.S. 321 (Que.). Difficulty: Challenging Willes - Chapter 28 #48 49. Hector had planned a new business venture, and Thomson was interested in participating in it. Thomson felt that it would take her four weeks to determine whether she could fully devote her time to the business. As the success of the venture depended on an immediate start, Hector was reluctant to include Thomson. To convince Hector of her sincerity, Thomson offered to provide him with a cheque for $5,000, which he could cash if she decided to back out of the project within four weeks. Hector agreed, and Thomson gave him the cheque fully completed and with the current date marked: "to be cashed only if deal cancelled." As matters turned out, Thomson decided only a day later that she could not devote the time to participate in the venture. She told Hector that she was backing out, and attended at the bank and placed a stop payment on the cheque. The cheque was duly dishonoured when Hector tried to cash it, and he sued Thomson pursuant to the Bills of Exchange Act for the $5,000. His claim was also for a further $1,000 that he was forced to pay as a fee to a broker for finding him another investor on short notice. Discuss. The cheque does not come within the meaning of the Bills of Exchange Act, for while it was a cheque, it was not an unconditional promise to pay. The cheque was only an order to pay on the basis of the occurrence of a specific contingency. As such, Hector cannot sue on the face of the cheque with the support of the Act. It is however strong evidence of a particular contractual term that has been breached by Thomson through dishonour of the cheque. In this case however, Hector will be limited in his recovery to the actual damages suffered, as he would be in any breach of contract situation. In this case, Hector's actual damages would appear to be $1,000. The argument might be made that the amount of the cheque constitutes the parties' settlement for liquidated damages, but students who believe that Hector is entitled to $5,000 must not rely on the Bills of Exchange Act to support the argument. Difficulty: Challenging Willes - Chapter 28 #49 28 Summary Category Difficulty: Challenging Difficulty: Easy Difficulty: Moderate Willes - Chapter 28 # of Questions 6 22 21 49