Instructor's Manual: Making Hard Decisions with DecisionTools

advertisement

INSTRUCTOR’S MANUAL

for

Making Hard Decisions

with DecisionTools, 3rd Ed.

Revised 2013

Samuel E. Bodily

University of Virginia

Robert T. Clemen

Duke University

Robin Dillon

Georgetown University

Terence Reilly

Babson College

Table of Contents

GENERAL INFORMATION

Introduction

Influence Diagrams

Decision Analysis Software

1

2

2

CHAPTER NOTES AND PROBLEM SOLUTIONS

Chapter 1

Chapter 2

Chapter 3

Chapter 4

Chapter 5

Chapter 6

Section 1 Cases

Athens Glass Works

Integrated Siting Systems, Inc.

International Guidance and Controls

George’s T-Shirts

Chapter 7

Chapter 8

Chapter 9

Chapter 10

Chapter 11

Chapter 12

Chapter 13

Section 2 Cases

Lac Leman Festival de la Musique

Sprigg Lane

Appshop, Inc.

Calambra Olive Oil

Scor-eStore.com

Chapter 14

Chapter 15

Chapter 16

Chapter 17

Section 3 Cases

John Carter

Sleepmore Mattress Manufacturing

Susan Jones

TOPICAL INDEX TO PROBLEMS

4

8

14

39

66

85

90

98

116

130

145

165

176

201

223

240

267

283

297

330

339

353

371

395

403

416

423

438

447

461

GENERAL INFORMATION

INTRODUCTION

Making Hard Decisions with DecisionTools, 3rd Edition presents the basic techniques of modern decision

analysis. The emphasis of the text is on the development of models to represent decision situations and the

use of probability and utility theory to represent uncertainties and preferences, respectively, in those

models. This is a new edition of the text. New examples and problems have been added throughout the text

and some chapters have either been completely rewritten (Chapters 5 & 11) or are entirely new (Chapters 6

& 13). In addition, we have added 15 cases from Darden Business Publishing. The Darden cases are

grouped together at the end of each of the three sections.

The first section of the book deals with structuring decision models. This part of the process is undoubtedly

the most critical. It is in the structuring phase that one comes to terms with the decision situation, clarifies

one’s objectives in the context of that situation, and confronts questions regarding the problem’s essential

elements. One must decide exactly what aspects of a problem are to be included in a model and make

fundamental modeling choices regarding how to represent each facet. Discussions with decision analysts

confirm that in most real-world applications, the majority of the time is spent in structuring the problem,

and this is where most of the important insights are found and creative new alternatives invented. The

discussion of model structuring integrates notions of tradeoffs and multiple objectives, something new to

the second edition of the book. Although complete discussion of modeling and analysis techniques are put

off until later, students should have enough information so that they can analyze simple multiattribute

models after finishing Chapter 4. This early introduction to this material has proven to be an excellent

motivator for students. Give them an interesting problem, ask them to discuss the objectives and tradeoffs,

and you will have trouble getting them to be quiet!

Making Hard Decisions with DecisionTools provides a one-semester introduction to the tools and concepts

of decision analysis. The text can be reasonably well adapted to different curricula; additional material

(readings, cases, problems from other sources) can be included easily at many different points. For

example, Chapters 8 and 15 discuss judgmental aspects of probability assessment and decision making, and

an instructor can introduce more behavioral material at these points. Likewise, Chapter 16 delves into the

additive utility function for decision making. Some instructors may wish to present goal programming or

the analytic hierarchy process here.

The Darden cases are grouped at the end of each of the 3 sections. Instead of tying each case to a particular

chapter, a group of cases are associated with a group of chapters. The goal is to show that the various

concepts and tools covered throughout the section can be applied to the cases for that section. For example,

to solve the cases at the end of Section One, Modeling Decisions, students will need to understand the

objectives of the decision maker (Chapter 2), structure and solve the decision model (Chapters 3 and 4),

perform a sensitivity analysis (Chapter 5), and, perhaps, incorporate organizational decision making

concepts (Chapter 6). Instructors can either assign a case analysis after covering a set of chapters asking the

students to incorporate all the relevant material or can assign a case after each chapter highlighting that

chapter’s material. Students need to understand that a complete and insightful analysis is based on

investigating the case using more than one or two concepts.

Incorporating Keeney’s (1992) value-focused thinking was challenging because some colleagues preferred

to have all of the multiple-objective material put in the same place (Chapters 15 and 16), whereas others

preferred to integrate the material throughout the text. Ultimately the latter was chosen especially stressing

the role of values in structuring decision models. In particular, students must read about structuring values

at the beginning of Chapter 3 before going on to structuring influence diagrams or decision trees. The

reason is simply that it makes sense to understand what one wants before trying to structure the decision.

In order for an instructor to locate problems on specific topics or concepts without having to read through

all the problems, a topical cross-reference for the problems is included in each chapter and a topical index

for all of the problems and case studies is provided at the end of the manual.

1

INFLUENCE DIAGRAMS

The most important innovation in the first edition of Making Hard Decisions was the integration of

influence diagrams throughout the book. Indeed, in Chapter 3 influence diagrams are presented before

decision trees as structuring tools. The presentation and use of influence diagrams reflects their current

position in the decision-analysis toolkit. They appear to be most useful for (1) structuring problems and (2)

presenting overviews to an audience with little technical background. In certain situations, influence

diagrams can be used to great advantage. For example, understanding value-of-information analysis is a

breeze with influence diagrams, but tortuous with decision trees. On the other hand, decision trees still

provide the best medium for understanding many basic decision-analysis concepts, such as risk-return

trade-offs or subjective probability assessment.

Some instructors may want to read more about influence diagrams prior to teaching a course using Making

Hard Decisions with DecisionTools. The basic reference is Howard and Matheson (1981, reprinted in ).

This first paper offers a very general overview, but relatively little in the way of nitty-gritty, hands-on help.

Aside from Chapters 3 and 4 of Making Hard Decisions with DecisionTools, introductory discussions of

influence diagrams can be found in Oliver and Smith (1990) and McGovern, Samson, and Wirth (1993). In

the field of artificial intelligence, belief nets (which can be thought of as influence diagrams that contain

only uncertainty nodes) are used to represent probabilistic knowledge structures. For introductions to belief

nets, consult Morawski (1989a, b) as well as articles in Oliver and Smith (1990). Matzkevich and

Abramson (1995) provides an excellent recent review of network models, including influence diagrams and

belief nets.

The conference on Uncertainty in Artificial Intelligence has been held annually since 1985, and the

conference always publishes a book of proceedings. For individuals who wish to survey the field broadly,

these volumes provide up-to-date information on the representation and use of network models.

Selected Bibliography for Influence Diagrams

Howard, R. A. (1989). Knowledge maps. Management Science, 35, 903-922.

Howard, R. A., and J. E. Matheson (1981). “Influence Diagrams.” R. Howard and J. Matheson (Eds.),The

Principles and Applications of Decision Analysis, Vol II, Palo Alto: Strategic Decisions Group,

(1984), 719-762. Reprinted in Decision Analysis, Vol 2 (2005), 127-147.

Matzkevich, I., and B. Abramson (1995). “Decision Analytic Networks in Artificial Intelligence.”

Management Science, 41, 1-22.

McGovern, J., D. Samson, and A. Wirth (1993). “Influence Diagrams for Decision Analysis.” In S. Nagel

(Ed.), Computer-Aided Decision Analysis. Westport, CT: Quorum, 107-122.

Morawski, P. (1989a). “Understanding Bayesian Belief Networks.” AI Expert (May), 44-48.

Morawski, P. (1989b). “Programming Bayesian Belief Networks.” AI Expert (August), 74-79.

Neapolitan, R. E. (1990). Probabilistic Reasoning in Expert Systems. New York: Wiley.

Oliver, R. M., and J. Q. Smith (1989). Influence Diagrams, Belief Nets and Decision Analysis (Proceedings

of an International Conference 1988, Berkeley). New York: John Wiley.

Pearl, J. (1988). Probabilistic Reasoning in Intelligent Systems. San Mateo, CA: Morgan Kaufman.

Shachter, R. D. (1986). “Evaluating Influence Diagrams,” Operations Research, 34, 871-882.

Shachter, R. D. (1988). Probabilistic inference and influence diagrams. Operations Research, 36, 389-604.

Shachter, R. D., and C. R. Kenley (1989). Gaussian Influence Diagrams. Management Science, 35, 527550.

DECISION ANALYSIS SOFTWARE

Making Hard Decisions with DecisionTools integrates Palisade Corporation’s DecisionTools, version 6.0

throughout the text. DecisionTools consists of six programs (PrecisionTree, TopRank, @RISK, StatTools,

NeuralTools, and Evolver), each designed to help with different aspects of modeling and solving decision

problems. Instructions are given on how to use PrecisionTree and @RISK, typically, at the end of the

chapter. PrecisionTree is a versatile program that allows the user to construct and solve both decision trees

and influence diagrams. @RISK allows the user to insert probability distributions into a spreadsheet and

run a Monte Carlo simulation. . Each of these programs are Excel add-ons, which means that they run

within Excel by adding their ribbon of commands to Excel’s toolbar.

2

In the textbook, instructions have been included at the ends of appropriate chapters for using the programs

that correspond to the chapter topic. The instructions provide step-by-step guides through the important

features of the programs. They have been written to be a self-contained tutorial. Some supplemental

information is contained in this manual especially related to the implementation of specific problem

solutions.

Some general guidelines:

•

To run an add-in within Excel, it is necessary to have the “Ignore other applications” option turned

off. Choose Tools on the menu bar, then Options, and click on the General tab in the resulting

Options dialog box. Be sure that the box by Ignore other applications is not checked.

•

Macros in the add-in program become disabled automatically if the security level is set to High.

To change the security level to Medium, in the Tools menu, point to Macros and then click

Security.

•

When the program crashes, restart the computer. It may appear as if the program has closed

properly and can be reopened, but it probably has not, and it is best to restart the computer.

•

The student version of PrecisionTree may limit the tree to 50 nodes. Some of the problems that

examine the value of information in Chapter 12 can easily exceed this limit.

•

When running @RISK simulations in the student version, make sure that only one worksheet is

open at a time. Otherwise, the program will display that error message “Model Extends Beyond

Allowed Region of Worksheet.”

More tips are provided throughout this manual as they relate to implementing specific problem solutions.

JOIN THE DECISION ANALYSIS SOCIETY OF INFORMS

Instructors and students both are encouraged to join the Decision Analysis

Society of INFORMS (Institute for Operations Research and Management

Science). This organization provides a wide array of services for decision

analysts, including a newsletter, Internet list server, a site on the World Wide

Web (https://www.informs.org/Community/DAS), annual meetings, and

information on job openings and candidates for decision-analysis positions. For

information on how to join, visit the web site.

3

CHAPTER 1

Introduction to Decision Analysis

Notes

This chapter serves as an introduction to the book and the course. It sets the tone and presents the basic

approach that will be used. The ideas of subjective judgment and modeling are stressed. Also, we mention

some basic aspects of decisions: uncertainty, preferences, decision structure, and sensitivity analysis.

In teaching decision analysis courses, it is critical to distinguish at the outset between good decisions and

good outcomes. Improving decisions mostly means improving the decision-making process. Students

should make decisions with their eyes open, having carefully considered the important issues at hand. This

is not to say that a good decision analysis foresees every possible outcome; indeed, many possible

outcomes are so unlikely that they may have no bearing whatsoever on the decision to be made. Often it is

helpful to imagine yourself in the future, looking back at your decision now. Will you be able to say,

regardless of the outcome: “Given everything I knew at the time — and I did a pretty good job of digging

out the important issues — I made the appropriate decision. If I were put back in the same situation, I

would go through the process pretty much in the same way and would probably make the same decision.”

If your decision making lets you say this, then you are making good decisions. The issue is not whether you

can foresee some unusual outcome that really is unforeseen, even by the experts. The issue is whether you

carefully consider the aspects of the decision that are important and meaningful to you.

Chapter 1 emphasizes a modeling approach and the idea of a requisite model. If the notion of a requisite

model seems a bit slippery, useful references are the articles by Phillips. (Specific references can be found

in Making Hard Decisions with DecisionTools.) The concept is simple: A decision model is requisite if it

incorporates all of the essential elements of the decision situation. The cyclical process of modeling,

solution, sensitivity analysis, and then modeling again, provides the mechanism for identifying areas that

require more elaboration in the model and portions where no more modeling is needed (or even where

certain aspects can be ignored altogether). After going through the decision analysis cycle a few times, the

model should provide a reasonable representation of the situation and should provide insight regarding the

situation and available options. Note that the process, being a human one, is not guaranteed to converge in

any technical sense. Convergence to a requisite model must arise from 1) technical modeling expertise on

the part of the analyst, and 2) desire on the part of the decision maker to avoid the cognitive dissonance

associated with an incomplete or inappropriate model.

Also important is that the modeling approach presented throughout the book emphasizes value-focused

thinking (Keeney, 1992), especially the notion that values should be considered at the earliest phases of the

decision-making process. This concept is initially introduced on pages 5-6.

To show that that decision analysis really is used very broadly, we have included the section “Where is

Decision Analysis Used?” Two references are given. The Harvard Business Review article by Ulvila and

Brown is particularly useful for students to read any time during the course to get a feel for real-world

applications of decision analysis.

Finally, we have included the section “Where Does the Software Fit In?” to introduce the DecisionTools

suite of programs.

Topical cross-reference for problems

Constructionist view

Creativity

Rice football

Requisite models

Subjective judgments

1.12,Du Pont and Chlorofluorocarbons

1.8

1.7

1.2

1.3, 1.5

4

Solutions

1.1. Answers will be based on personal experience. It is important here to be sure the distinction is made

between good decisions on one hand (or a good decision-making process) and lucky outcomes on the other.

1.2. We will have models to represent the decision structure as well as uncertainty and preferences. The

whole point of using models is to create simplifications of the real world in such a way that analysis of the

model yields insight regarding the real-world situation. A requisite model is one that includes all essential

elements of the problem. Alternatively, a requisite model is one which, when subjected to sensitivity

analysis, yields no new intuitions. Not only are all essential elements included, but also all extraneous

elements are excluded.

1.3. Subjective judgments will play large roles in the modeling of uncertainty and preferences. Essentially

we will build representations of personal beliefs (probabilities) and preferences (utilities). In a more subtle

— and perhaps more important — way, subjective judgments also direct the modeling process. Subjective

judgments are necessary for determining the appropriateness of a model’s structure, what should be

included in the model, and so on. Thus, subjective judgments play central roles in decision analysis. Good

decision analysis cannot be done without subjective judgments.

1.4. An appropriate answer would be that decision analysis can improve your decisions — the way you

make decisions — by providing a framework for dealing with difficult decisions in a systematic way.

Along with the analytical framework, decision analysis provides a set of tools for constructing and

analyzing decision models, the purpose of which is to obtain insight regarding difficult decision problems.

1.5. You require her subjective judgments on a number of matters. First is the problem of identifying

important aspects of the problem. Her input also will be required for the development of models of her

uncertainty and her preferences. Thus, her judgments will be critical to the analysis.

This question may also lead students to consider the implications of delegating decisions to agents. How

can you ensure that the agent will see things the way you do? Will the same aspects of the problem be

important? Does the agent agree with you regarding the uncertainty inherent in the situation (which

outcomes are more or less likely)? Does the agent have the same feeling regarding trade-offs that must be

made? In many cases it may be appropriate to obtain and use an expert’s information. Can you identify

some specific decision situations where you would be willing to accept an agent’s recommendation? Does

it matter who the agent is? Can you identify other situations in which some of the agent’s input can be

taken at face value (a forecast, say), but must be incorporated into a model based primarily on your own

judgments?

1.6. Answers will be based on personal experience.

1.7. Some of the issues are 1) the monetary costs of staying in Division 1-A and of moving to Division III,

2) impact on both alumni and local businesses of moving to Division III, 3) political and social impact on

campus of changing divisions.

Alternatives include 1) stay in Division 1-A, 2) move to Division III, 3) move to Division II, 4) delay the

decision for a year or more to gather information, 5) investigate other sources of funding to cover the

deficit, 6) drop out from the NCAA altogether ...

There is considerable uncertainty around the impact on the school of switching divisions. What will the

fallout be from the faculty, students, alumni, and local businesses if Rice went to Division III? Will it

impact recruiting? If so, how? What are the financial consequences? Is the deficit due to mismanagement or

is it structural? What are the long-term consequences versus the immediate uproar? Sources of information

could be surveys given to each constituency and/or interviews with leaders of the constituencies. Perhaps

other schools have changed divisions, and information can be found from their experience.

The objectives that different groups want to work toward include 1) minimize short-term and long-term

deficit, 2) minimize social upheaval, 3) maximize enjoyment of collegiate sports, 4) maximize student

5

opportunity to participate in sports, 5) maximize quality of sports programs. Some students may identify

still other objectives. Trading off these objectives may mean trying to balance the issues that are important

to different constituent groups.

1.8. This is a creativity question. The Friends of Rice Athletics could fund raise, tuition and/or ticket prices

could be increased, the stadium’s name can be sold, the athletic staff could all take a pay cut, etc.

1.9. Answers will be based on personal experience.

1.10. Instead of thinking only about risk versus return, the socially responsible investor also must consider

how to trade off risk and return for ethical integrity. It would not be unreasonable to suspect that to obtain a

higher level of ethical integrity in the portfolio, the investor must accept a lower expected return, higher

level of risk, or both.

1.11. For the most part, decision analysis is most appropriate for strategic, or one-time, decisions. These are

situations that we have not thought about before and “don’t know what to do.” Hence, it is worthwhile to

engage in some “decision making,” or decision analysis, to figure out what would be an appropriate action.

This is not to say that decision analysis is inappropriate for repetitive decisions. In fact, if a decision is

repeated many times, the savings that can be achieved over time by improving the decision-making process

can be substantial. In fact, this is the basis of much of management science. However, the reliance on

subjective judgments for the construction of tailored decision models in each decision situation may render

decision analysis, as portrayed here, unsuitable for dealing with repetitive situations. The point, though, is

that if one anticipates a long string of repetitive decisions in the future, and an optimal decision strategy has

not been previously developed, then the situation is indeed one of “not knowing what to do.” A decisionmodeling approach would indeed be appropriate in that case.

1.12. Beliefs and values do appear to change and develop over time as we think about new issues. Decision

analysis implicitly provides a framework for such changes through the identification and modeling of

decision problems, beliefs regarding uncertainty, and preferences.

Case Study: Commercial Space Travel

A student’s answer to being an early adopter or waiting until the industry matures is a personal choice and

depends on many factors. Some of these are: track record of industry, affordability, health of student vis-àvis demands of space travel, interest level, etc.

It certainly is true that new firms can come along and change an industry with leaner production or

management systems. Often, these firms do not have to contend with the legacy of older systems in more

established firms. In addition, the savings of a younger workforce and less established pension program can

be quite significant. Thus, it is reasonable that the new furry animals can be competitive with a massive

governmental organization.

On the other hand, the lack of experience of extreme situations might turn into a disaster for a newly

established firm. The cost savings of the newer firms could come from more efficient operations or it could

come from not having the equipment and policies in place to handle unusual situations. A space-flight

disaster would make headlines across the world and probably doom the responsible for-profit company. To

continue the survival-of-the-fittest analogy, it is not that every for-profit company will survive by avoiding

life-threatening situations; it is that a subgroup will survive. Would you want to put your life or the life of a

loved one on the line given the uncertainties surrounding early adopters in space travel?

Case Study: Du Pont and Chlorofluorocarbons

The major issues include shareholder welfare, social and environmental responsibility, and ethics. Of

course, all of these might be thought of as means for ensuring the long-run profitability or survivability of

the firm. The major sources of uncertainty involve research and development. Will substitute products

work? Will they be accepted? The CEO might wonder whether the ozone problem really is a problem, or

6

whether the observed recent changes are part of a normal cycle. Finally, could Du Pont’s efforts really have

an effect, and how much?

It is undoubtedly the case that Du Pont’s views of the situation have changed over time. Early on, the

chlorofluorocarbon issue was essentially ignored; no one knew that a problem existed. In the 1970s and

1980s, it became apparent that a problem did exist, and as scientific evidence accumulated, the problem

appeared to become more serious. Finally, we have arrived at a position where the ozone issue clearly

matters. (In fact, it matters mostly because of consumers’ views and preferences rather than because of the

scientific evidence, which appears to be less than conclusive.) Du Pont appears to be asking “Can we do

anything to help?” Many companies have developed a kind of “social awareness” in the past two decades

as a way to maintain a high-integrity profile.

Case Study: Choosing a Vice-Presidential Candidate

A vice president tends not to have an important role in American politics except in gaining electoral votes

during the election. A running mate is often chosen to balance the ticket geographically and ideologically.

For example, choosing a conservative, women from Alaska helped McCain appeal to the conservative base

of the Republican Party and to women. Alaska, however, has the minimum number of possible electoral

votes at 3. While McCain could reasonably count on winning Alaska’s 3 electoral votes, he could have

chosen someone else from a more populous state for the electoral votes. McCain must have thought that

Ms. Palin would provide a ticket with a wide appeal and that she could help pick up votes across the whole

country.

It is hard to know how McCain’s health affected his choice of Ms. Palin. Clearly, he knew how he felt, and

given that he is still in office eight years later, it is reasonable to assume that his health was not a major

concern when choosing Ms. Palin. A portion of the population, however, did find his age coupled with her

inexperience troubling. If he personally was not concerned, he might at least have considered how the

voters would perceive Ms. Palin being one heartbeat away from the presidency of the U.S.A.

The president is constantly gathering information, from the daily threat-assessment reports to meetings with

his cabinet, congressional members, and world leaders. However, even with all of these intelligence

reports, much uncertainty still remains, often requiring the president to make a judgment call. One of the

more famous examples of this is President Obama’s decision to send U.S. forces into Pakistan after Osama

bin Laden. Although it was thought that bin Laden was hiding inside a residence, there was not definitive

proof. Moreover, Obama also had to make judgment calls concerning the size of the force to send in and

whether to alert Pakistani officials. Generally, the president’s decisions are based (hopefully) on both facts

and judgments. McCain’s choice of Sarah Palin led many voters to question his judgment.

Choosing Sarah Palin might have turned out to be a very good choice for the United States, but it certainly

had many political overtones. In all fairness, the choice of a vice-presidential running mate is a very

political decision, one specially aimed at winning the election – a political event. On the other hand,

appearances are of utmost importance in elections, and even an unsubstantiated rumor can completely

derail a candidate. Thus, in choosing his running mate, McCain probably should have weighed the pros and

cons of each candidate using his fundamental objectives, the fundamental objectives of his party, and, of

course, the fundamental objectives of the United States as a whole.

7

CHAPTER 2

Elements of Decision Problems

Notes

This chapter is intended to start the reader thinking about decision problems in decision-analysis terms.

Thus, we talk about decisions to make, uncertain events, and valuing consequences. To make sure that the

richness of the terrain is understood, we introduce the concepts of dynamic decision making, a planning

horizon, and trade-offs.

In our definition of terms, we refer to a decision maker’s objectives where the term values is used to refer to

the decision maker’s set of objectives and their structure. The terms decision and alternative are adopted,

and are used throughout the book rather than similar terms such as “choice” and “option.” Likewise, we

have adopted the term uncertain event (and sometimes chance event), which then has outcomes. Finally,

and perhaps most significant, we have adopted Savage’s term consequence to refer to what the decision

maker experiences as a result of a combination of alternative(s) chosen and chance outcome(s). Another

term that we use that comes from Keeney’s value-focused thinking is the notion of decision context. This

term is discussed in the text and still more thoroughly in Keeney’s book. Briefly, it refers to the specific

identification of the problem (from which we might suspect that when one solves the wrong problem, one

has used the wrong decision context). It also can be used as a way to identify the class of alternatives that

one is willing to consider; a broader context (safety in auto travel as compared to specific traffic laws, for

example) leads a decision maker to consider a broader class of alternatives.

The time value of money appears in Chapter 2 and may seem out of place in some ways. It is here because

it is a fundamental way that streams of cash flows are valued, and because it provides a nice example of a

basic trade-off. Also, we have found that since most students have already been exposed to discounting, we

have been able to incorporate NPV calculations into problems and case studies throughout the book. For

the few students who have not encountered the topic, the early introduction to discounting in Chapter 2

provides enough information for them to proceed. Of course, the section on NPV may be skipped and used

as a reference later for problems that require discounting or for the discussion of trade-offs in Chapter 15.

Topical cross-reference for problems

Requisite models

“Secretary” problem

Sequential decisions

Time value of money

2.13

2.6

2.2, 2.6, Early Bird, Inc.

2.9-2.12, The Value of Patience

Solutions

2.1. a. Some objectives might be to minimize cost, maximize safety, maximize comfort, maximize

reliability, maximize cargo capacity (for shopping or vacationing), maximize maneuverability (in city

traffic). Students will undoubtedly come up with others as well.

b. In this new context, appropriate objectives might be minimize travel time, maximize exercise, minimize

total transportation cost, minimize use of fossil fuels, maximize ease (suitably defined) of visiting friends

and shopping. New alternatives to consider include using a bicycle or public transportation, walking,

rollerblading, skateboarding, motorcycle or scooter, renting a car, such as Zipcar. One might even consider

moving in order to live in a more convenient location.

2.2. Future alternatives can affect the eventual value of the consequence. For example, a university faculty

member, when accepting a position at a different institution, may not immediately resign his or her position

at the first university. Instead, a leave of absence may be taken. The leave of absence provides the

opportunity to decide in the future whether to stay at the new institution or return to the old one. A faculty

member would most likely think about the two different situations — resigning the current position

immediately versus taking a leave and postponing a permanent decision — in very different ways.

8

Another good example is purchasing a house. For many people in our mobile society, it is important to

think about the potential for selling the house in the future. Many purchasers might buy an unusual house

that suits them fine. However, if the house is too unusual, would-be purchasers might be afraid that, if they

decide to sell the house in the near future, it may be difficult to find a buyer and the sales price might be

lower than it would be for a more conventional house.

Finally, the current choice might eliminate a future valuable option. For example, our policy of powering

cars with fossil fuels reduces our options for using oil for potentially more valuable and less destructive

future activities.

2.3. In the first case, the planning horizon may be tied directly to the solution of the specific problem at

hand. If the problem is an isolated one not expected to repeat, this is a reasonable horizon. If more similar

problems are anticipated, the planning horizon might change to look forward in time far enough to

anticipate future such situations. If the firm is considering hiring a permanent employee or training existing

employees, then a planning horizon should be long enough to accommodate employee-related issues

(training, reviews, career advancement, and so on). In this broader context, the firm must consider

objectives related to hiring a new person (or training), which might include maximizing the welfare of

current employees, minimizing long-term costs of dealing with the class of problems, satisfying

affirmative-action requirements, or equity in treatment of employees.

2.4. In making any decision, it is important to 1) use all currently available information and 2) think

carefully about future uncertainty. Thus it is necessary to keep track of exactly what information is

available at each point in time. If information is lost or forgotten, then it will either be treated as an

uncertainty or simply not used when deciding. Clearly, the farmer would want to keep up to date on the

weather and incorporate any change to the forecast.

2.5. Some possibilities: insurance, hire another firm to manage the protection operation, press for

regulatory decisions and evaluations (i.e., get public policy makers to do the necessary analysis), do

nothing, develop a “cleanup cooperative” with other firms, or design and develop equipment that can serve

a day-to-day purpose but be converted easily to cleanup equipment. Students may come up with a wide

variety of ideas.

2.6. The employer should think about qualifications of the applicants. The qualifications that he seeks

should be intimately related to what the employer wants to accomplish (objectives — e.g., increase market

share) and hence to the way the successful applicant will be evaluated (attributes — e.g., sales). The

planning horizon may be critical. Is the employer interested in long-term or short-term performance? The

uncertainty that the employer faces, of course, is the uncertainty regarding the applicant’s future

performance on the specified attributes.

If the decision maker must decide whether to make a job offer at the end of each interview, then the

problem becomes a dynamic one. That is, after each interview the decision maker must decide whether to

make the offer (and end the search) or to continue the search for at least one more interview, at which time

the same decision arises. In this version of the problem, the decision maker faces an added uncertainty: the

qualifications of the applicants still to come. (This dynamic problem is sometimes known as the “Secretary

Problem,” and has been analyzed extensively and in many different forms in the operations-research

literature. For example, see DeGroot (2004) Optimal Statistical Decisions, Hoboken, NJ: Wiley & Sons. P.

325.)

2.7. Decisions to make: How to invest current funds. Possible alternatives include do nothing, purchase

specific properties, purchase options, etc. Other decisions might include how to finance the purchase, when

to resell, how much rent to charge, and so on. Note that the situation is a dynamic one if we consider future

investment opportunities that may be limited by current investments.

Uncertain events: Future market conditions (for resale or renting), occupancy rates, costs (management,

maintenance, insurance), and rental income.

9

Possible outcomes: Most likely such an investor will be interested in future cash flows. Important trade-offs

include time value of money and current versus future investment opportunities.

2.8. Answers depend on personal experience and will vary widely. Be sure to consider current and future

decisions and uncertain events, the planning horizon, and important trade-offs.

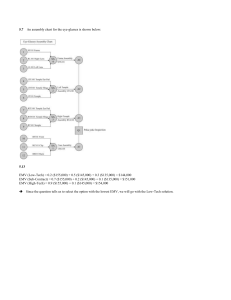

2.9. NPV

=

-2500 1500

1700

+

+

0

1

1.13

1.13

1.132

= -2500 + 1327.43 + 1331.35

= $158.78.

Or use Excel’s function NPV:

=-2500+NPV(0.13,1500,1700) = $158.78

The Excel file, “Problem 2.9.xls” has the equation set-up as a reference to cells that contain the cash flows.

2.10. NPV

-12000 5000

5000 -2000

6000

6000

+

+

+

+

= 1.12 +

2

3

4

5

1.12

1.12

1.12

1.12

1.126

= -10,714.29 + 3985.97 + 3558.90 - 1271.04 + 3404.56 + 3039.79

= $2003.90

Using Excel’s NPV function:

=NPV(0.12,-12000,5000, 5000,-2000,6000,6000)

= $2,003.90

The internal rate of return (IRR) for this cash flow is approximately 19.2%.

The Excel file, “Problem 2.10.xls” has the equation set-up as a reference to cells that contain the cash

flows.

2.11.

If the annual rate = 10%, then the monthly (periodic) rate r = 10% / 12 = 0.83%.

NPV(0.83%)

90

= -1000 + 1.0083 +

90

90

+ ... +

2

12

1.0083

1.0083

= $23.71.

Or use Excel’s NPV function, assume the 12 payments of $90 appear in cells B13:B24:

=-1000+NPV(0.1/12,B13:B24)= $23.71

(As shown in the Excel file “Problem 2.11.xls”)

If the annual rate = 20%, then the monthly (periodic) rate r = 20% / 12 = 1.67%.

NPV(1.67%)

90

= -1000 + 1.0167 +

90

90

+ ... +

= $-28.44.

2

1.0167

1.016712

10

Or use Excel’s NPV function, assume the 12 payments of $90 appear in cells B13:B24:

=-1000+NPV(0.2/12,B13:B24)= $-28.44

(As shown in the Excel file “Problem 2.11.xls”)

The annual interest rate (IRR) that gives NPV=0 is approximately 14.45%. You can verify this result by

substituting 14.45% / 12 = 1.20% for r in the calculations above.

Or with Excel’s IRR function, IRR(Values, Guess), assume the series of payments (the initial $1000

payment and the series of 12 payments of $90) are in cells B12:B24:

=IRR(B12:B24,0) = 1.20%

(As shown in the Excel file “Problem 2.11.xls”)

2.12. a. If the annual rate = 10%, then the monthly rate r = 10%/12 = 0.83%. Always match the periodicity

of the rate to that of the payments or cash flows.

-55

NPV(Terry) = 600 + 1.0083 +

-55

-55

+ ... +

2

1.0083

1.008312

= $-25.60.

Be sure to get the orientation correct. For Terry, the loan is a positive cash flow, and the payments are

negative cash flows (outflows). Thus, the NPV is negative. Because of the negative NPV, Terry should

know that this deal is not in his favor and that the actual interest rate being charged is not 10% annually. If

it were, then NPV should equal zero. The actual annual interest being charged must be greater than 10% as

NPV is less than zero.

Or with Excel’s NPV function, assume the series of 12 payments of $55 are in cells B12:B23.

=NPV(0.1/12,B12:B23)+600

= -$25.60

These calculations and those associated with the remaining parts of the question are shown in the Excel file

“Problem 2.12.xls”.

b. For the manager, the $600 loan is a negative cash flow, and the payments are positive cash flows. Hence,

NPV(Mgr)

55

= -600 + 1.0083 +

55

55

+ ... +

1.00832

1.008312

= $25.60.

Or with Excel’s NPV function, assume the series of 12 receipts of $55 are in cells B12:B23.

=NPV(0.1/12,B12:B23)-600

= $25.60

c. If the annual rate is 18%, then NPV is about $-0.08. In other words, the actual rate on this loan (the

internal rate of return or IRR) is just under 18%.

Using Excel’s IRR function, and assuming the cash flows are in cells B11:B23:

11

=IRR(B11:B23,0)*12

= 17.97% annually

2.13. Should future decisions ever be treated as uncertain events? Under some circumstances, this may not

be unreasonable.

If the node for selling the car is included at all, then possible consequences must be considered. For

example, the consequence would be the price obtained if he decides to sell, whereas if he keeps the car, the

consequence would be the length of the car’s life and cost to maintain and repair it.

If the node is a decision node, the requisite model would have to identify the essential events and

information prior to the decision. If the node is a chance event, this amounts to collapsing the model, and

hence may be useful in a first-cut analysis of a complicated problem. It would be necessary to think about

scenarios that would lead to selling the car or not, and to evaluate the uncertainty surrounding each

scenario.

2.14. Vijay’s objectives include maximizing profit, minimizing unsavory behavior, minimizing legal costs,

and maximizing Rising Moon’s appeal. Students will think of other objectives. Vijay’s decision is to apply

for a liquor license, and if granted, then he could decide on how to manage drinking at Rising Moon. For

example, he might be able to create a separate area of his place, such as a beer garden, where drinking

alcohol is allowed. Vijay could also decide to broaden his menu in other ways than serving alcohol. The

uncertainties include future sales and profit for Rising Moon, market reaction to offering alcohol, amount

of disruption occurring from serving alcohol, and legal liabilities. Consequence measures for sales, profit,

and legal costs are clear. He could simply count the number of disruptions to the business due to alcohol or

he could try to associate a cost figure to the unsavory behavior. Rising Moon’s appeal could be measured

by the change in sales volume due to introducing alcohol.

Vijay will certainly, as law requires, hedge by carrying insurance, and he will want to think carefully about

the level of insurance. As mentioned, he might be able to have a designated area for drinking alcohol. He

could gather information now via surveys or speaking to other local merchants. And he can always change

his mind later and stop serving alcohol.

Case Study: The Value of Patience

The Excel solution for this case is provided in the file “Value of Patience case.xlsx”.

1.

NPV

= -385,000 +

100,000 100,000

100,000

+

+ ... +

= $-3847.

2

1.18

1.18

1.18 7

Thus, Union should not accept the project because the NPV is negative.

Using Excel’s NPV function and assuming the series of 7 payments of $100,000 are in cells B12:B18:

=-385000+NPV(0.18,B12:B18)

= -$3847

2.

NPV

= -231,000 +

50,000 50,000

50,000

+

+ ... +

= $12,421.

2

1.10

1.10

1.10 7

This portion of the project is acceptable to Briggs because it has a positive NPV.

Using Excel’s NPV function and assuming the series of 7 payments of $50,000 are in cells E12:E18:

= -231,000+NPV(0.1,E12:E18)

= $12,421

12

3.

NPV

= -154,000 +

50,000 50,000

50,000

+

+ ... +

= $36,576.

2

1.18

1.18

1.18 7

Thus, this portion of the project is profitable to Union.

Using Excel’s NPV function and assuming the series of 7 payments of $50,000 are in cells H12:H18:

= -154,000+NPV(0.18,H12:H18)

= $36,576

Some students will want to consider the other $231,000 that Union was considering investing as part of the

entire project. Note, however, that if Union invests this money at their 18% rate, the NPV for that particular

investment would be zero. Thus the NPV for the entire $385,000 would be the sum of the two NPVs, or

$36,576.

4. Patience usually refers to a willingness to wait. Briggs, with the lower interest rate, is willing to wait

longer than Union to be paid back. The higher interest rate for Union can be thought of as an indication of

impatience; Union needs to be paid back sooner than Briggs.

The uneven split they have engineered exploits this difference between the two parties. For Briggs, a

payment of $50,000 per year is adequate for the initial investment of $231,000. On the other hand, the less

patient Union invests less ($154,000) and so the $50,000 per year is satisfactory.

As an alternative arrangement, suppose that the two parties arrange to split the annual payments in such a

way that Union gets more money early, and Briggs gets more later. For example, suppose each invests half,

or $192,500. Union gets $100,000 per year for years 1-3, and Briggs gets $100,000 per year for years 4-7.

This arrangement provides a positive NPV for each side: NPV(Union) = $24,927, NPV(Briggs) = $45,657.

Briggs really is more patient than Union!

Case Study: Early Bird, Inc.

1. The stated objective is to gain market share by the end of this time. Other objectives might be to

maximize profit (perhaps appropriate in a broader strategic context) or to enhance its public image.

2. Early Bird’s planning horizon must be at least through the end of the current promotion. In a first-cut

analysis, the planning horizon might be set at the end of the promotion plus two months (to evaluate how

sales, profits, and market share stabilize after the promotion is over). If another promotion is being planned,

it may be appropriate to consider how the outcome of the current situation could affect the next promotion

decision.

3, 4.

Customer

response

New Morning’s

reaction

Move up promotion start date?

Reaction to

New Morning

Now

13

Market

Share or

Profits

CHAPTER 3

Structuring Decisions

Notes

Chapters 3 and 4 might be considered the heart of Making Hard Decisions with DecisionTools. Here is

where most of the action happens. Chapter 3 describes the process of structuring objectives and building

influence diagrams and decision trees. Chapter 4 discusses analysis. The chapter begins with a

comprehensive discussion of value structuring and incorporates value-focused thinking throughout.

Constructing influence diagrams and decision trees to reflect multiple objectives is demonstrated, and the

chapter contains a discussion of scales for measuring achievement of fundamental objectives, including

how to construct scales for objectives with no natural measures.

Understanding one’s objectives in a decision context is a crucial step in modeling the decision. This section

of the chapter shows how to identify and structure values, with an important emphasis on distinguishing

between fundamental and means objectives and creating hierarchies and networks, respectively, to

represent these. The fundamental objectives are the main reasons for caring about a decision in the first

place, and so they play a large role in subsequent modeling with influence diagrams or decision trees.

Students can generally grasp the concepts of influence diagrams and how to interpret them. Creating

influence diagrams, on the other hand, seems to be much more difficult. Thus, in teaching students how to

create an influence diagram for a specific situation, we stress basic influence diagrams, in particular the

basic risky decision and imperfect information. Students should be able to identify these basic forms and

modify them to match specific problems. The problems at the end of the chapter range from simple

identification of basic forms to construction of diagrams that are fairly complex.

The discussion of decision trees is straightforward, and many students have already been exposed to

decision trees somewhere in their academic careers. Again, a useful strategy seems to be to stress some of

the basic forms.

Also discussed in Chapter 3 is the matter of including in the decision model appropriate details. One issue

is the inclusion of probabilities and payoffs. More crucial is the clarity test and the development of scales

for measuring fundamental objectives. The matter of clarifying definitions of alternatives, outcomes, and

consequences is absolutely crucial in real-world problems. The clarity test forces us to define all aspects of

a problem with great care. The advantage in the classroom of religiously applying the clarity test is that the

problems one addresses obtain much more realism and relevance for the students. It is very easy to be lazy

and gloss over definitional issues in working through a problem (e.g., “Let’s assume that the market could

go either up or down”). If care is taken to define events to pass the clarity test (“The market goes up means

that the Standard & Poor’s 500 Index rises”), problems become more realistic and engaging.

The last section in Chapter 3 describes in detail how to use PrecisionTree for structuring decisions. The

instructions are intended to be a self-contained tutorial on constructing decision trees and influence

diagrams. PrecisionTree does have an interactive video tutorial along with video tutorials on the basics and

videos from experts. These videos along with example spreadsheets and the manual all can be found in the

PrecisionTree menu ribbon under Help, then choosing Welcome to PrecisionTree.

Please note that if you enter probability values that do not sum to 100% for a chance node, then the

program uses normalized probability values. For example, if a chance node has two branches and the

corresponding probabilities entered are (10%, 80%), then the model will use (11.11%, 88.89%) – i.e.,

0.1/(0.1+0.8) and 0.8/(0.1+0.8).

Because this chapter focuses on structuring the decision, many of the problems do not have all of the

numbers required to complete the model. In some cases, the spreadsheet solution provides the structure of

the problem only, and the formulas were deleted (for example, problem 3.10). In other cases, the model is

14

completed with representative numbers (for example, problem 3.5). In the completed model, you will see

expected values and standard deviations in the decision trees and influence diagrams. These topics are

discussed in Chapter 4.

Topical cross-reference for problems

Branch pay-off formula

Calculation nodes

Clarity test

Constructed scales

Convert to tree

Decision trees

3.25 – 3.28

3.14, Prescribed Fire

3.4, 3.5, 3.12, 3.21, Prescribed Fire

3.3, 3.14, 3.20, 3.21

3.11, 3.26, 3.28, Prescribed Fire

3.5 - 3.7, 3.6 - 3.11, 3.13, 3.20 - 3.28,

Prescribed Fire, S.S. Kuniang, Hillblom

Estate

3.9, 3.11

3.4, 3.6 - 3.9, 3.11, 3.14, 3.16, 3.20, 3.21,

3.26, 3.28, Prescribed Fire, S.S. Kuniang

3.24, 3.25

3.1 - 3.3, 3.7, 3.10, 3.14 - 3.19, 3.21, 3.23,

Prescribed Fire

3.5, 3.9, 3.24 - 3.28, Prescribed Fire, S.S.

Kuniang

3.20

3.9

Imperfect information

Influence diagrams

Net present value

Objectives

PrecisionTree

Sensitivity analysis

Umbrella problem

Solutions

3.1. Fundamental objectives are the essential reasons we care about a decision, whereas means objectives

are things we care about because they help us achieve the fundamental objectives. In the automotive safety

example, maximizing seat-belt use is a means objective because it helps to achieve the fundamental

objectives of minimizing lives lost and injuries. We try to measure achievement of fundamental objectives

because we want to know how a consequence “stacks up” in terms of the things we care about.

Separating means objectives from fundamental objectives is important in Chapter 3 if only to be sure that

we are clear on the fundamental objectives, so that we know what to measure. In Chapter 6 we will see that

the means-objectives network is fertile ground for creating new alternatives.

3.2. Answers will vary because different individuals have different objectives. Here is one possibility.

(Means objectives are indicated by italics.)

Best Apartment

Minimize

Travel time

To School To Shopping

Maximize

Ambiance

To Leisure-time

Activities

Maximize

Use of leisure

time

Alone Friends Neighbors

Maximize

Discretionary $$

Centrally

located

Maximize

features (e.g.,

pool, sauna,

laundry)

Parking

at apartment

Maximize

windows, light

15

Minimize

Rent

3.3. A constructed scale for “ambiance” might be the following:

Best

--

--

-Worst

Many large windows. Unit is like new. Entrance and landscape are clean and inviting

with many plants and open areas.

Unit has excellent light into living areas, but bedrooms are poorly lit. Unit is clean and

maintained, but there is some evidence of wear. Entrance and landscaping includes some

plants and usable open areas but is not luxurious.

Unit has one large window that admits sufficient light to living room. Unit is reasonably

clean; a few defects in walls, woodwork, floors. Entrance is not inviting but does appear

safe. Landscaping is adequate with a few plants. Minimal open areas.

Unit has at least one window per room, but the windows are small. Considerable wear.

Entrance is dark. Landscaping is poor; few plants, and small open areas are not inviting.

Unit has few windows, is not especially clean. Carpet has stains, woodwork and walls are

marred. Entrance is dark and dreary, appears unsafe. Landscaping is poor or nonexistent;

no plants, no usable open areas.

3.4. It is reasonable in this situation to assume that the bank’s objective is to maximize its profit on the

loan, although there could be other objectives such as serving a particular clientele or gaining market share.

The main risk is whether the borrower will default on the loan, and the credit report serves as imperfect

information. Assuming that profit is the only objective, a simple influence diagram would be:

Credit

report

Default?

Make

Loan?

Profit

Note the node labeled “Default” Some students may be tempted to call this node something like “Credit

worthy?” In fact, though, what matters to the bank is whether the money is paid back or not. A more

precise analysis would require the banker to consider the probability distribution for the amount paid back

(perhaps calculated as NPV for various possible cash flows).

Another question is whether the arrow from “Default” to “Credit Report” might not be better going the

other way. On one hand, it might be easier to think about the probability of default given a particular credit

report. But it might be more difficult to make judgments about the likelihood of a particular report without

conditioning first on whether the borrower defaults.

Also, note that the “Credit Report” node will probably have as its outcome some kind of summary measure

based on many credit characteristics reported by the credit bureau. It might have something like ratings that

bonds receive (AAA, AA, A, and so on). Arriving at a summary measure that passes the clarity test could

be difficult and certainly would be an important aspect of the problem.

If the diagram above seems incomplete, a “Credit worthiness” node could be included and connected to

both “Credit report” and “Default”:

16

Credit

worthiness

Credit

report

Default?

Make

Loan?

Profit

Both of these alternative influence diagrams are shown in the Excel file “Problem 3.4.xlsx.” Two different

types of arcs are used in the diagrams: 1) value only and 2) value and timing, and these are explained in the

text. A value influence type influences the payoff calculation and a timing type exists if the outcome

precedes that calculation chronologically (or is known prior to the event).

3.5. This is a range-of-risk dilemma. Important components of profit include all of the different costs and

revenue, especially box-office receipts, royalties, licensing fees, foreign rights, and so on. Furthermore, the

definition of profits to pass the clarity test would require specification of a planning horizon. At the

specified time in the future, all costs and revenues would be combined to calculate the movie’s profits. In

its simplest form, the decision tree would be as drawn below. Of course, other pertinent chance nodes could

be included.

Revenue

Make

movie

Don't make movie

Profit = Revenue-Cost

Value of best

alternative

The revenue for the movie is drawn as a continuous uncertainty node in the above decision tree.

Continuous distributions can be handled two ways in PrecisionTree either with a discrete approximation

(see Chapter 8 in the text) or with simulation (see Chapter 11 in the text). This decision tree with a discrete

approximation of some sample revenue values is shown in the Excel file “Problem 3.5.xlsx.” A potentially

useful exercise is to have the students alter the sample values to see the effect on the model and specifically

the preferred alternative.

3.6.

Strengths

Weaknesses

Influence Diagrams

Compact

Good for communication

Good for overview of large problems

Decision Trees

Display details

Flexible representation

Details suppressed

Become very messy

for large problems

17

Which should he use? I would certainly use influence diagrams first to present an overview. If details must

be discussed, a decision tree may work well for that.

3.7. This problem can be handled well with a simple decision tree and consequence matrix. See Chapter 4

for a discussion of symmetry in decision problems.

Best

Representation

Max

Communication

Overview

Details

Influence

Diagram

Excellent for

large problems

Decision

Tree

Poor, due to

complexity

Details

hidden

Details

displayed

Max flexibility

Best for symmetric

decision problems

Very flexible

for assymetric

decisions

3.8.

Win Senate

election?

Run for

Senate?

Run for Senate

Run for House

Yes

No

Outcome

Run for

Senate

House

Win Senate?

Yes

No

Yes

No

Outcome

US Senator

Lawyer

US Representative

US Representative

Note that the outcome of the “Win Senate” event is vacuous if the decision is made to run for the house.

Some students will want to include an arc from the decision to the chance node on the grounds that the

chance of winning the election depends on the choice made:

18

Win

election?

Run for

Senate?

Win

Lose

Outcome

Run for

Senate

Run for Senate

Run for House

Win Election?

Outcome

Yes

US Senator

No

Lawyer

Yes

US Representative

House

Note that it is not possible to lose the House election.

The arc is only to capture the asymmetry of the problem. To model asymmetries in an influence diagram,

PrecisionTree uses structure arcs. When a structural influence is desired, it is necessary to specify how the

predecessor node will affect the structure of the outcomes from the successor node. By using a structure

arc, if the decision is made to run for the house, the “Win election?” node is skipped. This influence

diagram is shown in the Excel file “Problem 3.8.xlsx.”

3.9. (Thanks to David Braden for this solution.) The following answers are based on the interpretation that

the suit will be ruined if it rains. They are a good first pass at the problem structure (but see below).

suit not ruined, plus a sense of relief

rain

no rain

take umbrella

suit not ruined, but inconvenience incurred

suit ruined

do not take umbrella

rain

no rain

suit not ruined

(A) Decision tree

19

Weather

Forecast

Rain

Take

Umbrella?

Take

Umbrella?

Satisfaction

(B) Basic Risky Decision

Rain

Satisfaction

(C) Imperfect Information

The Excel solution “Problem 3.9.xlsx” shows a realization of this problem assuming the cost of the suit is

$200, the cost of the inconvenience of carrying an umbrella when it is not raining is $20, the probability of

rain is 0.25, and the weather forecaster is 90% accurate.

Note that the wording of the problem indicates that the suit may be ruined if it rains. For example, the

degree of damage probably depends on the amount of rain that hits the suit, which is itself uncertain! The

following diagrams capture this uncertainty.

suit not ruined,

plus a sense of relief

rain

no rain

suit not ruined, but

inconvenience incurred

take umbrella

suit ruined

suit ruined

do not take umbrella

suit not

ruined

rain

no rain

suit not ruined, but some

effort spent to avoid ruining

the suit

suit not ruined

(A) Decision tree

20

Weather

Forecast

Rain

Take

Umbrella?

Take

Umbrella?

Ruin

Suit

Satisfaction

Rain

Satisfaction

Ruin

Suit

(C) Imperfect Information

(B) Basic Risky Decision

3.10. (Thanks to David Braden for this solution.)

The decision alternatives are (1) use the low-sodium saline solution, and (2) don’t use the low-sodium

saline solution. The uncertain variables are: (1) The effect of the saline solution, consequences for which

are patient survival or death; (2) Possibility of court-martial if the saline solution is used and the patent

dies. The possible consequences are court-martial or no court-martial. The decision tree:

patient dead

do not use

saline solution

patient

saved

patient survives and the

use of saline solution justified

for other patients

use saline

solution

patient dead and

doctors suffer

patient dead

court-martial

no court-martial

patient dead

This decision tree is drawn in the Excel file “Problem 3.10.xlsx.”

3.11. a.

Sunny

Best

Weather

Rainy

Outdoors

Indoors

Party

decision

Terrible

Good

Satisfaction

No party

21

Bad

This influence diagram is drawn in the Excel file “Problem 3.11.xlsx” with some sample values assumed

(on a utility scale, a sunny party outside is worth 100, an indoors party is worth 80, no party is worth 20, a

party outside in the rain is worth 0, and the probability of rain is 0.3). A structure only arc is added in the

file between party decision and weather to include the asymmetries to skip the weather uncertainty if the

decision is made to have no party or have one indoors.

The second worksheet in the file shows the default decision tree created by the “Convert to Tree” button on

the influence diagram settings dialog box. (Click on the name of the influence diagram “Problem 3.11a” to

access the influence diagram settings. The Convert to Decision Tree button creates a decision tree from the

current influence diagram. This can be used to check the model specified by an influence diagram to insure

that the specified relationships and chronological ordering of nodes are correct. Conversion to a decision

tree also shows the impacts of any Bayesian revisions made between nodes in the influence diagram.

Once a model described with an influence diagram is converted to decision tree, it may be further edited

and enhanced in decision tree format. However, any edits made to the model in decision tree format will

not be reflected in the original influence diagram.

b. The arrow points from “Weather” to “Forecast” because we can easily think about the chances

associated with the weather and then the chances associated with the forecast, given the weather. That is, if

the weather really will be sunny, what are the chances that the forecaster will predict sunny weather? (Of

course, it is also possible to draw the arrow in the other direction. However, doing so suggests that it is easy

to assess the chances associated with the different forecasts, regardless of the weather. Such an assessment

can be hard to make, though; most people find the former approach easier to deal with.)

Forecast

Weather

Party

decision

Satisfaction

22

Sunny

Rainy

Outdoors

Indoors

Forecast

= “Sunny”

No party

Rainy

Outdoors

Terrible

Good

Sunny

Forecast

= “Rainy”

Best

Indoors

No party

Bad

Best

Terrible

Good

Bad

The influence diagram including the weather forecast is shown in the third worksheet and the associated

default decision tree created by the “Convert to Tree” function is shown in the fourth worksheet.

Additionally, we assumed that the weather forecaster is 90% accurate.

3.12. The outcome “Cloudy,” defined as fully overcast and no blue sky, might be a useful distinction,

because such an evening outdoors would not be as nice for most parties as a partly-cloudy sky. Actually,

defining “Cloudy” to pass the clarity test is a difficult task. A possible definition is “At least 90% of the sky

is cloud-covered for at least 90% of the time.”

The NWS definition of rain is probably not as useful as one which would focus on whether the guests are

forced indoors. Rain could come as a dreary drizzle, thunderstorm, or a light shower, for instance. The

drizzle and the thunderstorm would no doubt force the guests inside, but the shower might not.

One possibility would be to create a constructed scale that measures the quality of the weather in terms that

are appropriate for the party context. Here are some possible levels:

(Best)

---(Worst)

Clear or partly cloudy. Light breeze. No precipitation.

Cloudy and humid. No precipitation.

Thunderclouds. Heavy downpour just before the party.

Cloudy and light winds (gusts to 15mph). Showers off and on.

Overcast. Heavy continual rain.

3.13.

23

Change product

Engineer

says “Fix #3.”

Replace

#3

Behind schedule

#3 Defective

On schedule, costly

#3 not

defective

Behind scedule,costly

Change product

Behind schedule

Engineer says

“#3 OK.”

Replace

#3

#3 Defective

On schedule, costly

#3 not

defective

Behind scedule,costly

This decision tree is drawn in the Excel file “Problem 3.13.xlsx.”

3.14.

Forecast

Hurricane

Path

Safety

Decision

Evacuation

Cost

Consequence

Note that Evacuation Cost is high or low depending only on the evacuation decision. Thus, there is no arc

from Hurricane Path to Evacuation Cost.

This influence diagram is drawn in the Excel file “Problem 3.14.xlsx.” Because PrecisionTree allows only

one payoff node per influence diagram, the “Safety” and “Evaluation Cost” nodes are represented by

calculation nodes. A calculation node (represented by a rounded blue rectangle) takes the results from

predecessor nodes and combines them using calculations to generate new values. These nodes can be used

to score how each decision either maximizes safety or minimizes cost.

The constructed scale for safety is meant to describe conditions during a hurricane. Issues that should be

considered are winds, rain, waves due to the hurricane’s storm surge, and especially the damage to

buildings that these conditions can create. Here is a possible constructed scale:

(Best)

--

Windy, heavy rain, and high waves, but little or no damage to property or infrastructure.

After the storm passes there is little to do beyond cleaning up a little debris.

Rain causes minor flooding. Isolated instances of property damage, primarily due to

window breakage. For people who stay inside a strong building during the storm, risk is

minimal. Brief interruption of power service.

24

--

Flooding due to rain and storm surge. Buildings within 100 feet of shore sustain heavy

damage. Wind strong enough to break many windows, but structural collapse rarely

occurs. Power service interrupted for at least a day following the storm.

-Flooding of roads and neighborhoods in the storm’s path causes areas with high property

damage. Many roofs are severely damaged, and several poorly constructed buildings

collapse altogether. Both electrical power and water service are interrupted for at least a

day following the storm.

(Worst) Winds destroy many roofs and buildings, putting occupants at high risk of injury or

death. Extensive flooding in the storm’s path. Water and electrical service are interrupted

for several days after the storm. Structural collapse of older wood-frame buildings occurs

throughout the region, putting occupants at high risk.

3.15. Answers to this question will depend largely on individual preferences, although there are some

typical responses. Some fundamental objectives: improve one’s quality of life by making better decisions,

help others make better decisions, improve career, graduate from college, improve one’s GPA (for one who

is motivated by grades). Some means objectives: satisfy a requirement for a major, improve a GPA (to have

better job opportunities), satisfy a prerequisite for another course or for graduate school. Note that “making

better decisions” is itself best viewed as a means objective because it can provide ways to improve one’s

life. Only a very few people (academics and textbook writers, for example), would find the study of

decision analysis to be its own reward!

The second set of questions relates to the design of the course and whether it is possible to modify the

course so that it can better suit the student’s objectives. Although I do not want to promote classroom

chaos, this is a valuable exercise for both students and instructor to go through together. (And the earlier in

the term, the better!) Look at the means objectives, and try to elaborate the means objectives as much as

possible. For example, if a class is primarily taking the course to satisfy a major requirement, it might make

sense to find ways to make the course relate as much as possible to the students’ major fields of study.

3.16. While individual students will have their own fundamental objectives, we based our hierarchy on a

study titled "Why do people use Facebook?" (Personality and Individual Differences, Volume 52, Issue 3,

February 2012, Pages 243–249). The authors, Ashwini Nadkarni and Stefan G. Hofmann from Boston

University, propose that Facebook meets two primary human needs: (1) the need to belong and (2) the need

for self-presentation. Thus, a particular student’s objectives may be a variation on these themes. Students

may find it interesting to see how their fundamental objectives for their own Facebook page compare and

contrast to the study.

The fact that one’s private area can sometimes be seen by outsiders, particularly employers or future

employers, interferes with presenting your private self. If the private area were truly private, then a user

could be more truthful discussing their revelries and celebrations or even their private thoughts. If you

believe someone is eavesdropping on your conversation, then you are naturally more guarded with your

speech. Thus, Facebook does not provide a good means to expressing your private self.

Maximize Socialization

Maximize Need for

Belonging

Maximize

Self Esteem

Maximize

Self Worth

Maximize Need for

Self Presentation

Minimize

Loneliness

25

Maximize

Public Persona

Maximize

Private Persona

Clearly, each individual will have their own FOH, but there are some facts that students may want to take

into consideration. First, it is naïve to think that future employers will not “Google” or “Facebook” you.

Such concerns are not usually on the mind of a college freshman or particularly a high-school student, but

there are a host of problems that can arise from indiscriminately sharing private information. Even if there

is no illegal activity being shown (underage drinking, drug use, etc.), different audiences will have different

norms, and pictures of drinking, dancing, and partying could be considered compromising or

unprofessional.

Second, a future employer or even your current employer may be interested in your postings. They may

want to know what religion you practice, what your interests are, what organizations you belong to, such as

the NRA. All of these could bias them, good or bad, towards you. Also, discretion might be an important

aspect of your position, and employers might view your postings to determine if you can be trusted with

proprietary information.

Posted Information can also be used by competing firms either to gain a direct benefit or more nefariously

to befriend you, and thereby learn more about their competitor. Your personal profile may include job

details and thus provide an opening by unscrupulous ‘cyber sharks’, or by competing businesses hoping to

learn from the eyes and ears of the opposition. You may even have posted confidential information without

realizing its sensitive nature.

Facebook, Inc. itself has rights to your private information and has wide latitude on how it can use your

info. Facebook’s privacy agreement states "We may use information about you that we collect from other

sources, including but not limited to newspapers and Internet sources such as blogs, instant messaging

services, Facebook Platform developers and other users of Facebook, to supplement your profile.”