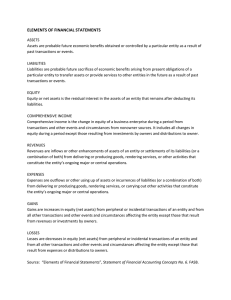

ACF 403: Introduction to Accounting Pre-course notes 1 The first set of notes introduces you to accounting terminology, the financial statements, accounting entities and the accounting equation. ACF 403 will assume that you are familiar with the contents of these course notes. Please treat these notes as revision if you have studied accounting recently. You should engage with the material to the extent that you need to, given your background in accounting. The Moodle page for ACF 403 contains some self-test questions and answers and a multiplechoice quiz (MCQ) for you to test your understanding of the content of these notes. Learning objectives: By reading these notes and doing the exercises you should be able to: - Explain the meaning of the key accounting terms and concepts Explain the relevance of the accounting entity concept in financial accounting. Distinguish between sole traders, partnerships and companies. Identify the key financial statements Describe the accounting equation, including how it is reflected in the statement of financial position Explain the nature of assets, liabilities and equity. Sources of definitions The main definitions in the notes below are derived from the Conceptual Framework for Financial Statements (2010) and from other pronouncements from by the International Accounting Standards Board (IASB). Information about the IASB will be covered in more detail in your course lectures for ACF 403. 1 Further reading These notes are designed to be a very brief outline of these basic areas. However, if you have not studied accounting recently and you find the content of these notes unfamiliar, you may also want to read further about the subjects covered in these notes. You are not expected to do any further pre-course work other than reading these notes and trying the exercises and questions. We do not recommend purchasing any textbook until you arrive at Lancaster as we have prepared a specific textbook for the accounting courses ACF 403 and ACF 503 which is only available at Lancaster. If you have access to any accounting textbooks, please read the relevant chapters which cover the contents of these notes. Examples of textbooks which provide basic financial accounting information include: Andrew Thomas and Anne Marie Ward, Introduction to Financial Accounting, 7th edition, McGraw Hill, 2012 Pauline Weetman, Financial accounting: an introduction, 6th edition, Pearson 2013 Michael Jones, Accounting, 3rd edition, Wiley 2013 (Section A only) You may have access to different textbooks, and you should feel free to use any suitable basic financial accounting textbook. If you use a US book, bear in mind there are differences between US standards and International Accounting Standards, although many good US textbooks outline these differences. At the basic level of these notes, these differences will not be important. Other sources: I have provided two dictionaries of accounting terminology for you to use throughout the course. They are included in the “Extra resources for self-study” section on the ACF 403 Moodle page. There are lots of Youtube videos dealing with various parts of the contents of these notes. A couple are suggested below but again, you should feel free to search for ones that you find easy to understand. http://www.youtube.com/watch?v=vLv6CqCK1Sc http://www.youtube.com/watch?v=yoN_feo9uHo 2 1. What is accounting? 1.1 Accounting information Accounting involves recording, classifying and interpreting business transactions to allow the communication of business information. Accounting reports aim to facilitate economic transactions by providing people with the information they need to make decisions about businesses. Accounting information should allow resources to be allocated efficiently. Accounting developed to allow wealthy individuals to identify what they owned and what they owed. The difference between what they owned (their assets) and what they owed (their liabilities) was their wealth (capital). As economies grew, the ownership and management of a business often become separate and accounting reports allowed owners, who were no longer able to access internal information as managers can, to gain information about the company. Accounting information allows business owners and/or managers to answer questions such as: - 1.2 How much profit has the company made? Can the company afford to pay dividends to owners/shareholders? Is there sufficient cash to pay staff wages? Can the company meet bank loan repayments? Can the company afford the investment required to introduce a new product? Financial and management accounting Financial accounting information is used by external users to the organisation for decisionmaking. Financial accounting is backward-looking information and meets an entity’s legal requirements. Financial statements are prepared using rules/standards and generally cover all the entity’s operations. In contrast, management accounting is information primarily prepared for internal users at an organisation to assist with managing costs and for decision-making. It is current and futurelooking, and is not covered by accounting standards and rules. It often focuses on specific departments or activities in the business rather than on the business as a whole. A summary table of the differences between financial and management accounting is given on the next page. The focus of ACF 403 is on financial accounting. 3 Financial Accounting Management Accounting Users Mainly external Internal Regulations Regulated Unregulated Detail of Information Focus on financial information, and report highly aggregated information Often very detailed, encompassing financial, non-financial and qualitative information Reporting Interval Annually. In some cases quarter or semi-annual reports are produced Any frequency – on an hourly, daily, weekly, yearly etc. basis Time Period Mostly historical Historical and current information as well as expected future performance and activities 2. Accounting terminology – the language of accounting 2.1 The financial statements The objective of general purpose financial statements is to provide information about the financial position, financial performance, and cash flows of an entity that is useful to a wide range of users in making economic decisions. To meet that objective, financial statements provide information about an entity’s assets, liabilities, equity, income and expenses, including gains and losses, contributions by and distributions to owners and cash flows. (IAS 1, Presentation of Financial Statements, 2007) All entities have to produce documents periodically (usually at least annually) with details of the performance (profit or loss) during the period and the financial position of the firm at the end of the period. The performance statement can be presented as one statement, called the Statement of Comprehensive Income. This includes profits for the period plus any gains and losses (often unrealised) on other assets. Companies more commonly split the performance statement into two parts, the first showing performance in the period, called the Statement of Profit and/or Loss (SOPL) or the Income Statement and the second, which shows the gains and losses, called the Statement of Other Comprehensive Income. 4 The statement showing the financial position of the firm is called either the Statement of Financial Position (SOFP) or the Balance Sheet. Larger firms also have to provide a third statement, called the Statement of Cash Flows (SOCF) which shows how cash has been generated and used in the period. These statements are called collectively the Financial Statements or the Accounts. In addition, Notes to the Accounts are provided which give more detail on the figures in the financial statements. The accounts also usually contain business reviews and other reports which are required under accounting standards or law, such as information on corporate governance. Combining the financial statements with, all these different reports may cause large firms’ accounts to be very large documents, for example, Tesco plc’s 2013 accounts are 142 pages long. As well as being called the Accounts, this document may also be called the Annual Report. 2.2 The elements of financial statements The financial statements portray the financial effects of transactions and other events by grouping them into broad classes (elements) according to their economic characteristics. The main elements relating to the statement of financial position are assets, liabilities and equity. The main elements relating to performance (the statement of profit or loss/the statement of comprehensive income/the income statement) are income (revenues) and expenses. (IASB, 2010) Each of the main elements are briefly outlined below. (a) Assets An asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity (IASB, 2010). Assets are items held by entities to generate income. Assets may be grouped into the categories, such as: - Tangible assets (property, plant and equipment/inventory) are assets which can be seen and touched, such as a factory or car. Intangible assets – assets which cannot be seen or touched but which have value, for example, a brand or patent. Available for sale assets – these are investments which the entity expects to sell in the future Investments – in associate companies, for example. Assets must be grouped by how long a company intends to keep them: 5 - (b) Current assets – assets which are expected to turn into cash by sale or use within a year Non-current assets – assets which will be used for more than one year from the date of the financial statements. Liabilities A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits. (IASB, 2010). Liabilities are amounts owed by the company. These could be payments to suppliers (trade payables), accruals, which are expenses owed at the date of the SOFP, repayments of bank loans (often classified as financial liabilities) or provisions, which are amounts provided for liabilities likely to occur in the future. As for assets, liabilities are grouped into current liabilities or non-current liabilities by whether the entity is required to pay the liability within a year or beyond. (c) Equity Equity is the residual interest in the assets of the entity after deducting all its liabilities (IASB, 2010). Equity (capital) refers to the ownership interest in the company. It is a type of liability because it is what the business owes to the owner. Equity includes the capital invested by the owners plus their share of profits and reserves of the firm. (d) Income Income is increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity other than those relating to contributions from equity participants. (IASB, 2010). Income is defined to include both revenues (sales) and gains. Revenues arise from the firm’s activities, usually selling goods or services. Gains are increases in the value of other economic benefits of the firm. We will focus mainly on revenues in ACF 403. (e) Expenses Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity other than those relating to distributions to equity participants. (IASB, 2010). 6 Expenses are generally the yearly costs of running the business, such as utility bills and staff wages. The wider definition given by the IASB includes reductions in value of other economic benefits. As with income, we will focus mainly on the yearly running expenses of the company for ACF 403. The terminology here will be frequently used in ACF 403 and a more detailed discussion of these elements will be part of the lecture course. 3. Accounting entities 3.1 The entity concept An accounting entity is the organisational unit for which the accounting records are prepared. It can be a legal entity, such as a club, or part of a legal entity. The term “entity” is used to show that the business is separate from its owners. This means that, for example, when a shop owner pays his business rates, that is an expense of the business but when he buys a washing-machine for his house, that is a personal expense. The accounting entity concept determines which transactions will be recorded in the financial statements as revenue and expenses of the business. An accounting entity can also be part of another accounting entity. Examples include where one company is a subsidiary of another, and where a branch of a larger store produces its own accounts as well as being included in the accounts of the whole store. The accounting entity concept is also called the business entity or the entity concept. 3.2 Types of entity The accounting information an entity needs to provide will depend on the type of entity providing the information. In ACF 403 we will focus on companies’ accounting requirements, which are covered by accounting standards. However, there are different types of entity which have more simple requirements than companies. (a) Sole traders Sole traders are individuals who start their own business, of which they are the owner and manager. Sole traders are responsible for the debts of the business (unlimited liability), and businesses are not separate legal entities (unincorporated). Profits are regarded as their own and income tax (not corporation tax) is charged on them. Sole trader’s accounts tend to be less complicated than those of companies and partnerships. Typical examples of sole traders would be a small shop or a sole practitioner accountant. (b) Partnerships Partnerships result from two or more people deciding to go into business together. Partnerships are usually unincorporated businesses and similar rules to sole traders apply to 7 them. Partners face unlimited liability and are jointly liable for the business debts. Profits are shared between partners according to a partnership agreement. Partnerships usually have financial statements for the tax authorities and pay income tax on their share of partnership profits. In recent years, some partnerships have chosen to become limited liability partnerships which allow them to limit their liability. Limited liability partnerships face similar rules to companies, as discussed below. Typical examples of partnerships are architects, lawyers and accountants. Many of the large accounting firms have become limited liability partnerships in recent years. (c) Companies Companies are incorporated as separate legal entities. The company exists independently of owners and managers, and owners’ liability is limited to the amount of capital they have invested. This means that creditors cannot pursue them for the company’s debts beyond the amount of the owners’ original investment. Companies can own assets and act in their own right. Two main types of companies exist: public limited companies (which have PLC at the end of their title) and private limited companies (which have Limited at the end of their title). In both cases, the equity of the business is divided into shares, which investors purchase. PLC’s offer shares to investors on public stock exchanges, such as the London Stock Exchange. Limited companies are privately owned, often by families or small groups of investors. Shareholders benefit from their investments in two possible ways; first by receiving dividends, which are a share of profits for the year, and second, by the value of their shares increasing over time, which means they can sell them for more than the shares cost. Companies are usually owned and managed by separate people, with the directors running the company, and the owners having the ability to vote on who the directors are. This is known as the separation or divorce of ownership and control. We focus on companies in ACF 403 and will come back to issues relating to companies during the course. Typical examples of PLC’s are Google Inc (the US equivalent of PLC) or Marks and Spencer plc. Large limited companies include Virgin Atlantic Airways Limited. 4. The accounting equation. To start a business, owners will need resources to buy assets to generate cash. The total assets acquired will be equal to the total funds introduced by the owners. The basic accounting equation represents this: Assets = Sources of funds 8 Funds to purchase assets can come from an owner or from an external source such as a bank loan. Funds from an owner are called equity (or capital), and funds from other sources are liabilities. The basic accounting equation thus becomes: Assets = Equity + Liabilities A = E + L The statement of financial position/balance sheet is formed from this equation. It shows the list of assets owned by an entity and the sources of funds for those assets. The statement of financial position always balances because the assets of an entity always equal the equity and liabilities (this is where the name “balance sheet” comes from). The accounting equation can also be reformulated as follows: Assets - Liabilities A - L = Equity = E This is the conventional format of the statement of financial position (SOFP) in the UK. An example of Tesco plc’s Balance Sheet (SOFP) is provided at the end of these notes. You should note the format, which shows assets less liabilities is equal to equity. The accounting equation is premised on the concept of duality, which is that every transaction has two aspects which will affect the accounting equation. These two aspects may be one effect on an asset and one on a liability, or two changes to assets or liabilities. For example, if a business buys a motor vehicle for cash, it will increase the vehicle asset and reduce the cash asset. If it buys a motor vehicle using a loan, it will increase the vehicle asset and increase the loan liability. This duality and two aspects of each accounting transaction is discussed further in Pre-course notes 2 as part of a discussion of double-entry book-keeping. Equity/capital shows the ownership interest in the business. This changes from year to year as the company makes a profit. Profit is part of equity because it is owed to the owners of the firm. Profit is the difference between the revenues earned by the entity less the expenses incurred to generate the revenues. When an entity earns a profit, both its assets and equity increase. In a simple example, at the end of the first year of operation (time = t), equity is composed of two elements, the capital contributed by the owners plus the increase in the business value from the generation of profit since the company began at the start of the year (time = t-1). Equityt = Equityt-1 + profit for the year t 9 which can be expanded to Equityt = Equityt-1 + (Revenues – Expenses) And the accounting equation can be expressed as: Assets = Equityt-1 + (Revenues – Expenses) + Liabilities 1 Example A company starts with a motor vehicle worth £15,000 which was acquired through £10,000 paid by the owner and a £5,000 bank loan. In the first year of the business, the company makes £6,000 in profit, comprised of revenues of £9,000 and expenses of £3,000. Illustrate how the accounting equation works for this company. 1. At the start: A = E + L £15,000 = £10,000 + £5,000 2. At the end of the year A = E + L £21,000 = £16,000 + £5,000 Using the expanded definition of the accounting equation: Assets = Owners’ capital + (revenues – expenses) + Liabilities £21,000 = £10,000 + (£9,000 - £3,000) + £5,000 Assets have increased to £21,000. If these haven’t been used to buy other assets, these will be in the form of cash or receivables (amounts owing from customers). (Revenues – Expenses) equals profit and profit increases owner’s capital/equity. The accounting equation underlies double-entry book-keeping and the structure of financial statements. This is a very brief introduction and it will be covered further later in the precourse notes and over the course of ACF 403. This is the end of the first set of notes. Please look at the balance sheet/SOFP for Tesco to start familiarising yourself with the formats used in the UK and under international accounting standards. Try the self-test questions and the multiple choice quiz to test your understanding of these notes. 1 This simple formulation assumes that there are no introductions of capital and that profit is before any dividends are paid out. 10 Tesco plc – 2013 Balance Sheet/SOFP 11

0

0

advertisement

Download

advertisement

Add this document to collection(s)

You can add this document to your study collection(s)

Sign in Available only to authorized usersAdd this document to saved

You can add this document to your saved list

Sign in Available only to authorized users