Economics Principles: Micro, Macro, Market, Demand, Supply

advertisement

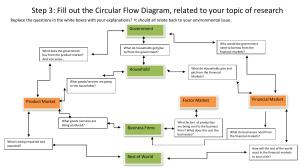

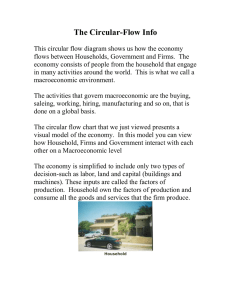

CHAPTER 1: REVISITING ECONOMICS APPROACHES AND PRINCIPLES ECONOMICS ● Is a social science which deals with the proper allocation and efficient use of scarce resources for the maximum satisfaction of human wants (Fajardo, 1990) ● Economy is derived from greek word “Oikonomus” or “Oikonomia” which means “One who manages a household. SCARCITY - Limited nature of society’s resources DIVISIONS OF ECONOMICS 1. Microeconomics Deals w/ the problems and analysis of behavior of individual economic unit such as the consumer (household), seller (firm), and owners of factors of production 2. Macroeconomics Deals w/ the problem of the whole economy and how aggregated economic units or sectors such as consumer, business, government and foreign sectors are interrelated 2. Communism/Command economy: This is the opposite of capitalism wherein the government controls the economy. 3. Socialism: It s a mixture of capitalism and communism. FACTORS IN DECISION MAKING 1. People face tradeoffs. 2. Opportunity cost. 3. Making decisions at the margin. 4. People respond to incentives. HOW INDIVIDUAL DECISIONS AFFECT OTHERS 5. Trade (exchange) can benefit everyone. 6. Markets are often a good way to organize exchange. 7. Government can sometimes improve on markets. THE CIRCULAR FLOW OF/ECONOMIC MODEL HUMAN WANTS Goods and services needed by human beings. GOODS AND SERVICES Those that yield satisfaction (tangible and intangible) Classification of Goods: 1. Consumer Goods - Those that yield direct satisfaction 2. Capital Goods - Those that are used in the production of other goods (and services) 3. Essential Goods - These are the “basic” needs of man 4. Luxury Goods - These are those that contribute to mans comfort and wellbeing RESOURCES Refer to the factors or inputs of production. They are those which are needed to produce goods and services. Classification of Resources 1. Land - natural resources, not man-made 2. Labor - physical and mental 3. Capital - anything that is used to produced other goods and services. 4. Entrepreneurship - ability to organize and coordinate land, labor, and capital MICROECONOMICS AGENTS Firms - Produces and sell goods and services - Buy inputs (labor,capital & raw materials) Consumers/ Households - Buy goods and services - Sell inputs (labor services, loanable funds) CHAPTER 2: DEMAND, SUPPLY, AND MARKET EQUILIBRIUM THE BASIC DECISION-MAKING UNITS ● A firm is an organization that transforms resources (inputs) into products (outputs). Firms are the primary producing units in a market economy. ● An entrepreneur is a person who organizes, manages, and assumes the risks of a firm, taking a new idea or a new product and turning it into a successful business. ● Households are the consuming units in an economy. THE CIRCULAR FLOW OF ECONOMIC ACTIVITY BASIC ECONOMIC PROBLEMS 1. What goods and services to produce? 2. How to produce the goods and services and how much? 3. From whom are these goods and services? MODELS OF ECONOMIC SYSTEM 1. Capitalism/Market economy: Refers to the free enterprise or laissez faire economy. ● The circular flow of economic activity shows the connections between firms and households in input and output markets Output, or product, markets are the markets in which goods and services are exchanged. Input markets are the markets in which resources—labor, capital, and land—used to produce products, are exchanged. Payments flow in the opposite direction as the physical flow of resources, goods, and services (counterclockwise). ● ● ● THE DEMAND CURVE INPUT MARKETS INCLUDES ● The labor market, in which households supply work for wages to firms that demand labor. The capital market, in which households supply their savings, for interest or for claims to future profits, to firms that demand funds to buy capital goods. The land market, in which households supply land or other real property in exchange for rent. ● ● DEMAND ● Demand is the schedule of various quantities of goods and services w/c buyers are willing and able to purchase at a given price, time and place and all other factors are held constant (ceteris paribus). - “The only thing that affects the demand is the price of the product.” DETERMINANTS OF HOUSEHOLD DEMAND A household’s decision about the quantity of a particular output to demand depends on: ● ● ● ● ● ● ● ● ● ● ● ● price of the product quality of the product season population tastes and preferences number of buyers income of the buyers (inferior-/normal goods+) prices of related products/goods (substitute +/complementary-) expected prices religion customs and tradition promotion and advertisement Quantity Demanded: is the amount (number of units) of a product that a household would buy in a given time period if it could buy all it wanted at the current market price. DEMAND IN OUTPUT MARKETS THE LAW OF DEMAND OTHER PROPERTIES OF QUANTITY DEMANDED: ● Demand curves intersect the quantity (X)-axis, as a result of time limitations and diminishing marginal utility. ● Demand curves intersect the (Y)-axis, as a result of limited incomes and wealth. INCOME AND WEALTH ● Income is the sum of all households wages, salaries, profits, interest payments, rents, and other forms of earnings in a given period of time. It is a flow measure. ● Wealth, or net worth, is the total value of what a household owns minus what it owes. It is a stock measure. RELATED GOODS AND SERVICES ● Normal Goods: are goods for which demand goes up when income is higher and for which demand goes down when income is lower. ● Inferior Goods: are goods for which demand falls when income rises. ● Substitutes: are goods that can serve as replacements for one another; when the price of one increases, demand for the other goes up. Perfect substitutes are identical products. ● Complements: are goods that “go together”; a decrease in the price of one results in an increase in demand for the other, and vice versa. (e.g. 3in1) Shift of Demand Versus Movement Along a Demand Curve A Change in Demand Versus a Change in Quantity Demanded TO SUMMARIZE: THE IMPACT OF A CHANGE IN THE PRICE OF RELATED GOODS PLOT THE DEMAND CURVE PRICE Qd 20 12 30 40 SUPPLY IN OUTPUT MARKETS FROM HOUSEHOLD TO MARKET DEMAND ● Demand for a good or service can be defined for an individual household, or for a group of households that make up a market. ● Market demand is the sum of all the quantities of a good or service demanded per period by all the households buying in the market for that good or service. CHANGES IN DEMAND A change in demand is a shift of the demand curve to the right (an increase in demand), or to the left (a decrease in demand). ● Shifts are cause by a change in one or more of the determinants of demand. THE SUPPLY CURVE AND THE SUPPLY SCHEDULE THE LAW OF SUPPLY DETERMINANT OF SUPPLY ● The price of the good or service. ● The cost of producing the good, which in turn depends on: ● The price of related products. (substitute -/complementary+) ● Technology ● Price expectation ● Taxes and Subsidies ● Number of sellers A CHANGE IN SUPPLY VERSUS CHANGE IN QUANTITY SUPPLIED PLOT THE SUPPLY CURVE PRICE Qs 20 2 30 40 MARKET EQUILIBRIUM ● The operation of the market depends on the interaction between buyers and sellers. ● An equilibrium is the condition that exists when quantity supplied and quantity demanded are equal. ● At equilibrium, there is no tendency for the market price to change. ● When supply shifts to the right, supply increases. This causes quantity supplied to be greater than it was prior to the shift, for each and every price level. TO SUMMARIZE: MARKET DISEQUILIBRIA INCREASE IN DEMAND AND SUPPLY DECREASES IN DEMAND AND SUPPLY RELATIVE MAGNITUDES OF CHANGE