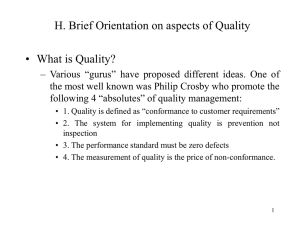

MSc Project Management GBEPM 620 Quality Management Quality Measurement and Costs 1 The Economics of Quality • There is a cost for building in quality • There is value received for building in quality • There is a cost (sometimes hidden) for poor quality • The cost of building quality into your processes is less than the cost of building poor-quality products • If the cost of quality is greater than the resulting benefit, then you are not building in quality into your processes Customer Quality Measures • Customers typically relate quality to: ✓ Feature based measures; “have” or “have not” - determined by design ✓ Performance measures - “range of values” - conformance to design or ideal value 2 True Vs Substitute Performance Measures • Customers - use “true” performance measures ✓ example: a true measure of a car door may be “easy to close”. ✓ true performance measures typically vary by each individual customer. ✓ Unfortunately, producers cannot measure performance as each individual customer does. • Producers - use “substitute” performance measures ✓ these measures are quantifiable (measurable units). ✓ Substitute measure for a car door: door closing force. • Other example: light bulb ✓ true performance measure -- brightens the room ✓ substitute performance measure – wattage or lumens Substitute Performance Measure • Another term for a substitute performance measure is a metric. ✓ Metric is a standard of measurement. ✓ In quality management, we use metrics to translate customer needs into producer performance measures. • Internal quality metrics ✓ scrap and rework ✓ process capability (Cp or Cpk) ✓ first time through quality (FTTQ) 3 The Economics of Quality and Producer Perspective ❑ If quality is viewed as the “conformance to specifications” then the economics of quality relates to the balance between: ▪ the Cost of Conformance ▪ the cost of Non-Conformance Performance measurement is a fundamental building block of TQM and a total quality organisation Performance Measurement ✓ Improving quality requires the establishment of effective metrics ✓ In a successful total quality organisation, performance is measured by the improvements seen by the customer as well as by the results delivered to other stakeholders A supply of consistent, accurate, and timely data across all functional areas of business provides realtime information for the evaluation, control, and improvement of processes, products, and services to meet both business objectives and rapidly changing customer needs. 4 Quality Metrics • A metric is a verifiable measure, stated in either quantitative or qualitative terms, that: ✓ captures performance in terms of how something is being done relative to a standard, ✓ allows and encourages comparison, ✓ supports business strategy. Effective Metrics • Effective metrics satisfy the following conditions: ✓ performance is clearly defined in a measurable entity (quantifiable). ✓ a capable system exists to measure the entity (e.g., a gauge). • Effective metrics allow for actionable responses if the performance is unacceptable. ✓ There is little value in a metric which identifies nonperformance if nothing can or will be done to remedy it. 5 Performance Measurement Terms ✓ Data: representations of facts that come from some type of measurement process ✓ Measurement: act of quantifying the performance dimensions of products, services, processes and other business activities ✓ Measures and Indicators: the numerical information that results from measurement ✓ Information: derived from the analysis of data and measurements and expressed in the context of a business or organisation Performance Measurement Process Flow Measurement Data Analysis Information 6 Understanding Quality Costs Iceberg illustration of Quality related Costs Commonly measured Cost of Quality Hidden Cost of Quality ❑ Understanding quality costs enables you to: ▪ Understand hidden costs ▪ Reduce and eliminate unnecessary cost ❑ Prevent problems from happening Quality Gurus Point of View ❑Philip B. Crosby: Quality is Free ▪ The system for causing quality is Prevention, not Appraisal ▪ The performance standard must be Zero Defects, not “that is close enough” ▪ The measurement of quality is the price of nonconformance ▪ Cost of quality is only the measure of operational performance ▪ “Quality is Free. It is not a gift, but it is free. What costs money are the unquality things – all the actions that involve not doing jobs right the first time.” 7 Quality Gurus Point of View ❑Edwards W. Deming: Quality can be and should be improved continuously ▪ Improving quality reduces cost and improves profitability What is Cost of Quality? A quality cost is considered to be any cost that the company or organization would not have incurred if the quality of the product or service were perfect! 8 Cost of Quality (COQ) • Quality costs can mean two things: • Cost of attaining quality • Cost of poor quality • COQ translates defects, errors, etc. into the “language of management” – We need to communicate to management the impact of quality in language they understand which is often in monetary terms. • Quality cost measurement and publication does not solve quality problems, but provides a basis for identifying improvement opportunities and success of improvement programs. Cost of Quality Measurement ❑The cost of doing a quality job, conducting quality improvements and achieving goals must be carefully managed, so that the long-term effect of quality on the organisation is a desirable one ❑These costs must be a true measure of the quality effort, and are best determined from an analysis of the costs of quality ❑Such an analysis provides: ▪ method of assessing the effectiveness of the management of quality ▪ means of determining problem areas, opportunities, savings and action priorities 9 Models of Quality Cost Reporting ❑ Quality costs can be categorised to enable better understanding ❑ Two basic approaches to the collection and presentation of the cost of quality have emerged: • Prevention, Appraisal and Failure (PAF) Model • Process Cost Model PAF Model Total Cost of Quality Prevention Costs Appraisal Costs Internal Failure Costs External 10 Prevention Costs ❑ Costs of all activities specifically designed to prevent poor quality in products or services ✓ Quality planning costs, e.g. development of new procedures, new equipment design, reliability studies ✓ Process control costs, e.g. analysing production processes and implementing process control plans ✓ Information systems costs, e.g. developing data requirements and measurements ✓ Training and management costs, e.g. internal and external training, clerical staff expenses, and miscellaneous supplies Appraisal Costs ❑ Costs associated with efforts to ensure conformance to requirements, generally through measurement and analysis of data to detect non-conformances ✓ Test and inspection costs, incoming materials, work-inprocess, finished goods, and equipment costs and salaries ✓ Instrument maintenance costs, calibration and repair of measuring instruments ✓ Process measurement and control costs, time spent to gather and analyze quality measurements 11 Internal Failure Costs ❑ Costs associated with the non-conformance of products or services prior to the transfer of ownership to the customer ✓ Scrap and rework costs, material, labour and overhead ✓ Costs of corrective action, time spent determining the causes of failure and correcting production problems ✓ Downgrading costs, revenue lost by selling a product at a lower price because it does not meet specifications ✓ Process failures, unplanned machine downtime or unplanned equipment repair External Failure Costs ❑ Costs associated with the non-conformance of products and which are detected after the transfer of ownership to the customer ✓ Costs due to customer complaints and returns, rework on returned items, cancelled orders, and freight premiums ✓ Product recall costs and warranty claims, cost of repair or replacement as well as associated administrative costs ✓ Product liability costs, legal actions and settlements 12 Traditional View of the Cost of Quality Total quality costs Cost per good unit of product Failure costs Cost of appraisal plus prevention 0% Quality of conformance 100% Total Quality View of the Cost of Quality Cost per good unit of product Total quality costs 0% Failure costs Cost of appraisal plus prevention Quality of conformance 100% 13 The 1-10-100 Rule of COQ ▪ One dollar spent on Prevention will save $10 on Appraisal and $100 on Failure costs ▪ This rule helps one to prioritise expenditure on prevention, which is sure to bring in greater returns The 1-10-100 Rule of COQ ▪ The lowest cost is generally obtained when non-conformances are prevented in the first place. ▪ If non-conformances occur, it is generally least expensive to detect them as soon as possible after their occurrence. ▪ The most expensive quality costs are from non-conformances detected by customers. 14 COQ and Quality Management Effectiveness Take Home Message ▪ Prevention cost is an investment of an organisation to do things right the first time ▪ Appraisal and failure costs are avoidable 15 Process Cost Model Cost of Quality (COQ) Cost of Conformance (COC) Cost of NonConformance (CONC) ❑ COC is the process cost of providing products/services to the required standards, by a given specified process in the most effective manner. ❑ CONC is the failure cost associated with a process not being operated to the requirements, or the cost due to the variability of the process. 16 The Process Cost of Quality Model Cost Quality Management Tools • Cost indexes • Pareto analysis 17 Quality Costs Bases: Performance Measures • Internal failure costs as a percent of total production costs • External failure costs as an average percent of net sales • Procurement appraisal costs as a percent of total purchased material costs • Operations appraisal costs as a percent of total production costs • Total quality costs as a percent of production costs Quality Costs Bases: Other Measures • A labour base (such as total labour, direct labour, or applied labour) • A cost base (such as shop cost, operating cost, or total material and labour) • A sales base (such as net sales billed, or sales value of finished goods) • A unit base (such as the number of units produced, or the volume of output) 18 Pareto Analysis ✓ Identifying the “Vital few”, leading to corrective action that has a high return for a low dollar input ✓ 70 to 80 percent of the quality problems are due to these “Vital few” ✓ Quality costs over time can be analysed to identify trends that require significant attention Cost Indexes Exercise: Compute a sales dollar base index for Midwest Sales, Inc., to analyse the following quality cost information, and prepare a memo to management.(Use a graph) (Figs in $’000) Q1 Q2 Total Sales 4,120 4,206 4,454 4,106 External Fail. 280.8 208.2 142.8 128.6 Internal Fail. 468.2 372.4 284.4 166.4 Appraisal 194.2 227.7 274.4 266.2 Prevention 28.4 29.2 971.6 837.5 Total Quality Costs Q3 50.2 Q4 80.2 751.8 641.4 19 Cost of Quality Categories Exercise: Show the different quality cost categories on a pie chart Cost Element Customer complaint remakes Printing plate revisions Quality improvement projects Gauging Other waste Correction of typographical errors Proofreading Quality planning Press downtime Bindery waste Checking and inspection Amount ($) 28,000 28,000 14,000 100,000 39,000 210,000 450,000 57,000 285,000 53,000 42,000 Pareto Analysis Exercise: Beecom Software Corporation has gathered the data on quality problems as shown in the table below and in the text. Management wishes to know which quality loss categories are the most significant. Use Pareto analysis to investigate the quality losses. What conclusions do you reach? 20 The Data Their losses are summarized as follows: Category Annual Loss Rework costs $ 30,000 Rejected disks (loaded) 360,000 Rejected disks (blank) 89,000 Inspection costs (extra)—incoming 18,000 Inspection costs (extra)—outgoing 28,000 Customer returns 185,000 Training and system improvement costs 67,000 System downtime 138,000 21