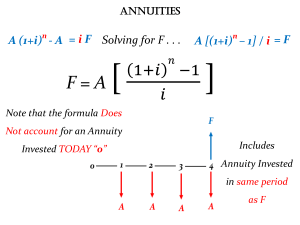

Financial Calculator – HP 10b II+ • The recommended financial calculator is the HP 10b II+. • Please familiarize yourself with this calculator and its functions!!! Basics of Investments • Definition of an investment: • A current commitment of money for a period of time in order to derive future payments that will compensate for: • The time the funds are committed • The expected rate of inflation • Uncertainty of future flow of funds • Why do we Invest: • By investing (saving money now instead of spending it), individuals can trade-off present consumption for a larger future consumption. Time Value of Money Time value of money Single cash flow (Lump sum) Multiple cash flows (Annuities) FV / PV / i / n Tables / Formulae / Calculator Uneven cash flows Ordinary annuities Annuities due FV / PV / PMT / i / n FV / PV / PMT / i / n Tables / Formulae / Calculator Tables / Formulae / Calculator Perpetuities PV Formula Time Value of Money • • Money loses its value over time, because of two general reasons: 1. Inflation (not TVM) 2. Money has an opportunity cost in the form of interest Interest compensates the owner for not having the money available for other productive use - This is the concept of TVM. • Which would you choose? 1. R100 today or R100 in two years time? 2. R1135,67 today or R1216,54 in two years time? • The choice is more challenging. Why? • Cash flows not at same point in time • Cash flows can only be compared in they are at same point in time • Change above amounts to make them comparable – either exclude or include interest portion Time Value of Money • • Basic Definitions • Present Value – earlier money on a time line • Future Value – later money on a time line • Interest rate – “exchange rate” between earlier money and later money • Discount rate • Cost of capital • Required return Calculator Keys: • Five TVM variables • N = number of periods • I/Y = interest rate • PV = present value • PMT = payment • FV = future value Time Value of Money – Simple Interest • Future Value FV = PV x (1 + r) x t • Example: You have R325 to invest for 2 years. If you earn simple interest at 14% p.a., how much will your investment be worth at the end of two years? 325 X 0.14 X 2 = 91 + 325= R416 Time Value of Money – Compound Interest • Future Value FV = PV x (1 + r)t • Example: Suppose you invest R1000 for one year at 5% per year. What is the future value in one year? Suppose you leave the money in for another year. How much will you have two years from now? • FV in one year: 1000 x 1.05 = R1 050.00 • FV in 2 years: 1000 x 1.052 = R1 102.50 Using a financial calculator: N: 2 i: 5 PV: 1 000 FV R1 102.50 Time Value of Money – Simple and Compound Interest Example (Simple interest and Compound interest) • Suppose you invest R1000 for two year at 5% per year. What is the future value in two year using simple interest? • What would the value be using compound interest • Explain the difference. Simple Interest: FV = 1000 x (1.05) x 2 = R1 100 Compound Interest: FV = 1000 x (1.05)2 = R1 102.50 The extra R2.50 comes from the interest of: 0.05 x (R50) = R2.50 earned on the first interest payment. Therefore, the difference is that with compound interest you get interest on (interest + capital) while with simple interest you only get interest on capital. Time Value of Money - FV - Effect of Compounding Example: • Suppose you had a relative deposit R10 at 5.5% interest 200 years ago. How much would the investment be worth today? • What is the effect of compounding? Using your financial calculator: N: 200 i: 5.5 PV: 10 FV R447 189.84 The effect of compounding: Simple interest = 10 + (200 x10 x 0.055) = 120 Compounding added (447189.84 – 120) = R447 069,84 to the value of the investment. Time Value of Money – Present Value • So far, we have seen how to calculate the future value of an investment • But we can turn this around to find the amount that needs to be invested to achieve some desired future value: PV FVN 1 i N Present Value – Important Relationship I For a given interest rate – the longer the time period, the lower the present value Present Value – Important Relationship II For a given time period – the higher the interest rate, the smaller the present value Time Value of Money – Effect of Discounting – Different Terms Example What is the present value of R500 to be received in (i) 5 years or (ii) 10 years, if the discount rate is 10%: 500 500 (i) PV = (1.10)5 = 𝑅310.46 (ii) PV = (1.10)10 = 𝑅192.77 (i) Using your financial calculator: FV: 500 (ii) FV: 500 n: 5 n: 10 i: 10 i: 10 PV: R310.46 PV: R192.77 Time Value of Money – Effect of Discounting – Different Interest Rates Example What is the present value of R500 to be received in 5 years if the discount rate is (ii) 10%p.a. or (ii) 15%p.a.: 500 500 (i) PV = (1.10)5 = 𝑅310.46 (ii) PV = (1.15)5 = 𝑅248.58 (i) Using your financial calculator: FV: 500 (ii) FV: 500 n: 5 n: 5 i: 10 i: 15 PV: R310.46 PV: R248.58 Time Value of Money – Present Value Example You want to begin saving for your daughter’s college education and you estimate that she will need R150 000 in 17 years. If you feel confident that you can earn 8% per year, how much do you need to invest today? Using your financial calculator: FV: 150 000 N 17 I: 8 PV R40 540.34 Time Value of Money – Present Value Example Your parents set up a trust fund for you 10 years ago that is now worth R19 671,51. If the fund earned 7% per year, how much did your parents invest? Using your financial calculator: FV: 19 671.51 I: 7 N: 10 PV R10 000 Time Value of Money – Implied Interest Rate Often we will want to know what the implied interest rate is in an investment Example: You need R80 000 for your university studies. If you have a lump sum of R35 000 now, what interest rate/ discount rate would you need to earn in order to accumulate R80 000 at the end of 8 years? Using your financial calculator: FV: 80 000 PV: (35 000) N: 8 I 10.89% Time Value of Money – Discount Rate Often we will want to know what the implied interest rate is in an investment Example: You are looking at an investment that will pay R1200 in 5 years if you invest R1000 today. What is the discount rate? Using your financial calculator: the sign convention matters!!! N=5 PV = -1000 (you pay 1000 today), PV is always entered as negative!!! FV = 1200 (you receive 1200 in 5 years) I/YR 3.714% Time Value of Money – Number of Periods Example: You are looking at an investment that will pay R10 000 000. If you earn interest at a rate of (i) 5%p.a. or (ii) 16% p.a. and you have R2 300 000 to invest today, how long will it take to accumulate R10 million? Using your financial calculator: (i) FV: 10000000 (ii) n: 30 years i: 5 PV: -2300000 FV: 10000000 n: 9.9 years i: 16 PV: -2300000 Time Value of Money – Number of Periods Example You want to purchase a new car and you are willing to pay R20 000. If you can invest at 10% per year and you currently have R15000, how long will it be before you have enough money to pay cash for the car? Using your financial calculator: FV: 20 000 PV: (15 000) I: 10 N: 3.02 years Time Value of Money - Annuities • An annuity is a series of nominally equal payments equally spaced in time • Annuities are very common: • Rent • Mortgage payments • Car payment • Pension income • The timeline shows an example of a 5-year, R100 annuity 0 100 100 100 100 100 1 2 3 4 5 Time Value of Money - The Principle of Value Additivity • How do we find the value (PV or FV) of an annuity? • First, you must understand the principle of value additivity: • The value of any stream of cash flows is equal to the sum of the values of the components • In other words, if we can move the cash flows to the same time period we can simply add them all together to get the total value Time Value of Money - Present Value of an Annuity • We can use the principle of value additivity to find the present value of an annuity, by simply summing the present values of each of the components: N PVA 1 i t 1 Pmt t t Pmt 1 1 i 1 Pmt 2 1 i 2 Pmt N 1 i N Time Value of Money - Present Value of an Annuity (cont.) • Using the example, and assuming a discount rate of 10% per year, we find that the present value is: PVA 100 . 110 1 100 . 110 2 100 . 110 3 100 . 110 4 100 . 110 5 62.1 68.3 75.1 82.6 90.9 379.08 0 100 100 100 100 100 1 2 3 4 5 379.08 Time Value of Money - Present Value of an Annuity (cont.) • Actually, there is no need to take the present value of each cash flow separately • We can use a closed-form of the PVA equation instead: N PVA 1 i t 1 Pmt t t 1 1 N 1 i Pmt i Time Value of Money - Present Value of an Annuity (cont.) • We can use this equation to find the present value of our example annuity as follows: 1 1 5 110 . PVA Pmt 379.08 010 . This equation works for all regular annuities, regardless of the number of payments Time Value of Money – Present Value of an Annuity Example Using the example of a 5 year, R100 annuity. Calculate the present value of the annuity if the discount rate is 10%p.a. Using your financial calculator: (Set your calculator to END mode) FV: 0 PMT: 100 I: 10 N: 5 PV: R379.08 (as for the formula) Time Value of Money – The Future Value of an Annuity We can also use the principle of value additivity to find the future value of an annuity, by simply summing the future values of each of the components: N FVA t 1 Pmt t 1 i Nt Pmt 1 1 i N 1 Pmt 2 1 i N 2 Pmt N Time Value of Money – The Future Value of an Annuity (cont.) Using the example of a 5 year, R100 annuity, and assuming a discount rate of 10% per year, we find that the future value is: FVA 100110 . 100110 . 100110 . 100110 . 100 610.51 4 3 2 1 } 146.41 133.10 121.00 110.00 0 100 100 100 100 100 1 2 3 4 5 = 610.51 at year 5 The Future Value of an Annuity (cont.) • Just as we did for the PVA equation, we could instead use a closedform of the FVA equation: N FVA Pmt 1 i t t 1 Nt 1 i N 1 Pmt i This equation works for all regular annuities, regardless of the number of payments The Future Value of an Annuity (cont.) • We can use this equation to find the future value of the example annuity: 5 110 . 1 610.51 FVA 100 . 010 Time Value of Money – Future Value of an Annuity Example Using the example of a 5 year, R100 annuity. Calculate the future value of the annuity if the discount rate is 10%p.a. Using your financial calculator: (set your calculator to END mode) PV: 0 PMT: 100 I: 10 N: 5 FV: R610.51 (as for the formula) Time Value of Money – Annuities Due • Thus far, the annuities that we have looked at begin their payments at the end of period 1; these are referred to as regular annuities • An annuity due is the same as a regular annuity, except that its cash flows occur at the beginning of the period rather than at the end 5-period Annuity Due 5-period Regular Annuity 100 0 100 100 100 100 100 100 100 100 100 1 2 3 4 5 Time Value of Money – Present Value of an Annuity Due • We can find the present value of an annuity due in the same way as we did for a regular annuity, with one exception • Note from the timeline that, if we ignore the first cash flow, the annuity due looks just like a four-period regular annuity • Therefore, we can value an annuity due with: PVAD 1 1 N 1 1 i Pmt Pmt i Present Value of an Annuity Due (cont.) • Therefore, the present value of our example annuity due is: PVAD 1 1 51 110 . 100 100 416.98 010 . Note that this is higher than the PV of the, otherwise equivalent, regular annuity Time Value of Money – Present Value of an Annuity Example Using the example of a 5 year, R100 annuity. Calculate the future value of the annuity if the discount rate is 10%p.a. Using your financial calculator: (Set your calculator to BEGIN mode) FV: 0 PMT: 100 I: 10 N: 5 PV: R416.98 (as for the formula) Time Value of Money – Future Value of an Annuity Due • To calculate the FV of an annuity due, we can treat it as regular annuity, and then take it one more period forward: FVAD 1 i N 1 1 i Pmt i Pmt Pmt Pmt Pmt Pmt 0 1 2 3 4 5 Time Value of Money – Future Value of an Annuity Due (cont.) • The future value of our example annuity is: FVAD 5 110 . 1 110 100 . 67156 . . 010 Note that this is higher than the future value of the, otherwise equivalent, regular annuity Time Value of Money – Future Value of an Annuity Example Using the example of a 5 year, R100 annuity. Calculate the future value of the annuity if the discount rate is 10%p.a. Using your financial calculator: (Set your calculator to BEGIN mode) PV: 0 PMT: 100 I: 10 N: 5 FV: R671.56 (as for the formula) Time Value of Money – Deferred Annuities • A deferred annuity is the same as any other annuity, except that its payments do not begin until some later period • The timeline shows a five-period deferred annuity 0 1 2 100 100 100 100 100 3 4 5 6 7 Time Value of Money – Present Value of a Deferred Annuity • We can find the present value of a deferred annuity in the same way as any other annuity, with an extra step required • Before we can do this however, there is an important rule to understand: • When using the PVA equation, the resulting PV is always one period before the first payment occurs Time Value of Money – Present Value of a Deferred Annuity (cont.) • To find the PV of a deferred annuity, we first find use the PVA equation, and then discount that result back to period 0 • Here we are using a 10% discount rate PV2 = 379.08 PV0 = 313.29 0 0 0 100 100 100 100 100 1 2 3 4 5 6 7 PV of a Deferred Annuity (cont.) Step 1: 1 1 5 110 . PV2 100 379.08 010 . Step 2: PV0 379.08 . 110 2 313.29 Time Value of Money – FV of a Deferred Annuity • The future value of a deferred annuity is calculated in exactly the same way as any other annuity • There are no extra steps at all Time Value of Money - Uneven Cash Flows • Very often an investment offers a stream of cash flows which are not either a lump sum or an annuity • We can find the present or future value of such a stream by using the principle of value additivity Time Value of Money - Uneven Cash Flows: An Example (1) • Assume that an investment offers the following cash flows. If your required return is 7%, what is the maximum price that you would pay for this investment? 100 0 PV 200 1 300 2 100 . 107 1 3 200 . 107 2 4 300 . 107 3 5 513.04 Time Value of Money - Uneven Cash Flows: An Example (2) • Suppose that you were to deposit the following amounts in an account paying 5% per year. What would the balance of the account be at the end of the third year? 300 0 500 700 2 3 1 4 5 FV 300105 . 500105 . 700 1,555.75 2 1 Time Value of Money - Non-annual Compounding • So far we have assumed that the time period is equal to a year • However, there is no reason that a time period can’t be any other length of time • We could assume that interest is earned semi-annually, quarterly, monthly, daily, or any other length of time • The only change that must be made is to make sure that the rate of interest is adjusted to the period length Time Value of Money - Non-annual Compounding (cont.) • Suppose that you have $1,000 available for investment. After investigating the local banks, you have compiled the following table for comparison. In which bank should you deposit your funds? Bank First National Second National Third National Interest Rate 10% 10% 10% Compounding Annual Monthly Daily Time Value of Money - Non-annual Compounding (cont.) • To solve this problem, you need to determine which bank will pay you the most interest • In other words, at which bank will you have the highest future value? • To find out, let’s change our basic FV equation slightly: i FV PV 1 m Nm In this version of the equation ‘m’ is the number of compounding periods per year Time Value of Money - Non-annual Compounding (cont.) • We can find the FV for each bank as follows: First National Bank: Second National Bank: Third National Bank: FV 1,000110 . 1100 , 1 010 . FV 1,000 1 12 12 010 . FV 1,000 1 365 365 1104 , .71 Obviously, you should choose the Third National Bank 110516 , . Time Value of Money - Continuous Compounding • There is no reason why we need to stop increasing the compounding frequency at daily • We could compound every hour, minute, or second • We can also compound every instant (i.e., continuously): F Pe rt Here, F is the future value, P is the present value, r is the annual rate of interest, t is the total number of years, and e is a constant equal to about 2.718 Time Value of Money - Continuous Compounding • Suppose that the Fourth National Bank is offering to pay 10% per year compounded continuously. What is the future value of your $1,000 investment? F 1,000e 0 .10 1 110517 , . This is even better than daily compounding The basic rule of compounding is: The more frequently interest is compounded, the higher the future value Time Value of Money - Continuous Compounding • Suppose that the Fourth National Bank is offering to pay 10% per year compounded continuously. If you plan to leave the money in the account for 5 years, what is the future value of your $1,000 investment? F 1,000e 0.10 5 1,648.72 Time Value of Money – Non-annual Compounding • • • Jack Bond plans to move into a rented flat in Melville in 8 month’s time. The owner of the flat, Ms Moneypenny, requires a deposit of R20 000 to be paid upon occupation of the flat to protect her against breakages. Luckily, Jack inherited R100 000 a couple of years ago, and he still has R18 424,38 left. YOU ARE REQUIRED TO: calculate the effective annual interest rate at which Jack should invest his money to enable him to pay the required deposit eight months from today. 12 P/Yr PV = 18 424,38 FV = 20 000 n=8 I/YR = 12,37% (nominal) EFF = 13,0982% Time Value of Money – Multiple Uneven Cash Flows • Multiple Uneven Cash Flows • 2 Ways: • compound accumulated balance forward one year at a time • calculate future value of each cash flow and add them up EXAMPLE 1 (Multiple Cash Flows – Future Values) • Find the value at year 3 of each cash flow and add them together, using at rate of 8%. Investment at follows: Today: 7000, Years 1 – 3: 4000 • Today (year 0): PV = 7 000; I = 8%; n = 3; FV = 8 817,98 • Year 1: PV = 4 000; I = 8%; n = 2; FV = 4 665,60 • Year 2: PV = 4 000; I = 8%; n = 1; FV = 4 320 • Year 3: Value = 4 000 • Total value in 3 years = 8 817,98 + 4 665,60 + 4 320 + 4 000 = 21 803,58 • Value at year 4 = PV =21 803,58; I = 8%; n = 1; FV = 23 547,87 Time Value of Money – Multiple Uneven Cash Flows EXAMPLE 2 (Multiple Cash Flows – Future Values) • Suppose you invest R500 in a mutual fund today and R600 in one year. If the fund pays 9% annually, how much will you have in two years? N: 2 N: 1 PV: 500 PV: 600 I: 9 I: 9 P/Y: 1 P/Y: 1 FV: 594.05 FV: 654 • Total: 594.05 + 654 = R1 248.05 Time Value of Money – Multiple Uneven Cash Flows EXAMPLE 3 (Multiple Cash Flows – Future Values) • How much will you have in 5 years if you make no further deposits? • First way: • FV = • PV = 500; I = 9%; n = 5 + PV = 600; I = 9%; n = 4 • = 1 616,26 • Second way – use value at year 2: • PV= 1 248,05; N = 3; I = 9; FV = 1 616,26 Time Value of Money – Multiple Uneven Cash Flows EXAMPLE 4 (Multiple Cash Flows – Future Values) • Suppose you plan to deposit R100 into an account in one year and R300 into the account in three years. How much will be in the account in five years if the interest rate is 8%? PV = 100; N = 4; I = 8 FV = 136.05 (FV1) PV = 300; N = 2 (5 – 3); I = 8 FV = 349,92 (FV2) FV1 + FV2 = 485,97 Time Value of Money – Multiple Uneven Cash Flows EXAMPLE 5 (Multiple Cash Flows – Present Values) • Present value with multiple cash flows – 2 methods: • Discount back 1 period at a time • Calculate PV individually and add them together • • • • • You are considering an investment that will pay you R1 000 in one year, R2 000 in two years and R3 000 in three years. If you want to earn 10% on your money, how much would you be willing to pay? PV = ?; FV = 1 000; I = 10%; n = 1; PV = 909,09 PV = ?; FV = 2 000; I = 10%; n = 2; PV = 1 652,89 PV = ?; FV = 3 000; I = 10%; n = 3; PV = 2 253,94 PV = 909,09 + 1 652,89 + 2 253,94 = 4 815,93 Time Value of Money – Annuities & Perpetuities • Annuities and Perpetuities • Annuity – finite series of equal payments that occur at regular intervals • If the first payment occurs at the end of the period, it is called an ordinary annuity • If the first payment occurs at the beginning of the period, it is called an annuity due • Perpetuity – infinite series of equal payments Time Value of Money – Annuities & Perpetuities • • Annuities (finite number of payments) • You can use the PMT key on the calculator for the equal payment • The sign convention still holds Ordinary annuity versus annuity due • You can switch your calculator between the two types by using the BGN function on your Texas instrument • If you see “BGN” or “Begin” in the display of your calculator, you have it set for an annuity due • Most problems are ordinary annuities Time Value of Money – Annuities & Perpetuities • Ordinary annuity vs. Annuity due • Ordinary annuity – payment (cash flows) is made at the end of the period. Calculator in END mode • Annuity due – payment (cash flows) is made at the beginning of the period. Calculator in BGN mode Example: 6 year annuity; payment R400 per year; I = 10% Ordinary annuity Annuity due BGN mode PMT: 400 400 I: 10 10 N: 4 4 PV: R1 267.95 R1 394.74 • Remember Annuity due: BGN mode Time Value of Money – Annuities & Perpetuities EXAMPLE 7 (Planning for Retirement) • You are offered the opportunity to put some money away for retirement. You will receive five annual payments of R25 000 each beginning in 40 years. How much would you be willing to invest today if you desire an interest rate of 12%? PMT: 25 000 N: 5 I: 12 PV: 90 119.41 THEN FV: 90 119.41 N: 39 I: 12 PV: R1 084.71 Time Value of Money – Annuities & Perpetuities EXAMPLE 8 (Ordinary Annuity – Present Value) • Suppose you win the Publishers Clearinghouse R10 million sweepstakes. The money is paid in equal annual instalments of R333 333,33 over 30 years. If the appropriate discount rate is 5%, how much is the sweepstakes actually worth today? PMT = 333 333.33 N = 30 I = 5 PV = 5 124 150.29 Time Value of Money – Annuities & Perpetuities EXAMPLE 9 (Finding Payment of Annuity) • Suppose you want to borrow R20 000 for a new car. You can borrow at 8% per year, compounded monthly. If you take a 4 year loan, what is your monthly payment? PV = 20 000 I = 8 N = 4 X 12 = 48 P/Y = 12 PMT = R488.26 Time Value of Money – Annuities & Perpetuities EXAMPLE 10 (Finding Rate of Payment) • Suppose you borrow R10 000 from your parents to buy a car. You agree to pay R207,58 per month for 60 months. What is the compounded monthly interest rate? Sign convention matters!!! N = 60 PV = 10 000 PMT = -207.58 I/YR = 9% Time Value of Money – Annuities & Perpetuities EXAMPLE 11 (Ordinary Annuity – Future Value) • Suppose you begin saving for your retirement by depositing R2 000 per year in a fund. If the interest rate is 7,5%, how much will you have in 40 years? PMT = 2 000 I/Y = 7.5% P/Y = 1 N = 40 FV = R454 513.04 Time Value of Money – Annuities & Perpetuities EXAMPLE 12 (Annuity Due – Future Value) • You are saving for a new house and you put R10 000 per year in an account paying 8%. The first payment is made today. How much will you have at the end of 3 years? BGN mode (2nd BGN 2nd Enter) PMT = 10 000 I/Y = 8% P/Y = 1 N = 3 FV = R35 061.12 Time Value of Money – Annuities & Perpetuities EXAMPLE 13: Finding the Payment • Suppose you want to buy a new computer system and the store is willing to sell it to allow you to make monthly payments. The entire computer system costs R3 500. The loan period is for 2 years and the interest rate is 16,9% with monthly compounding. What is your monthly payment? P/Y = 12 PV = 3 500 I = 16.9 N = 24 (2 X 12) PMT = R172.88 Time Value of Money – Annuities & Perpetuities EXAMPLE 14: Finding the Number of Payments • You ran a little short of cash during your December holiday break, so you put R5 000 of your expenses on your credit card. You can only afford to make a premium of R200 per month. The interest rate on your credit card is 24.5% compounded monthly. How long will it take you to pay off the R5 000 P/Y = 12 PV = 5 000 I = 24.5 PMT = -200 N = 35.33/12 = 2.94 years Time Value of Money - Perpetuity • • • • Perpetuity ( Infinite number of payments) Golden Delicious Limited The cumulative preference shares are non-redeemable and have a face value of R20 each. An annual dividend of 15% is paid at the end of each year. In addition to the dividend due in year 1, an amount of R9,00 relating to dividends in arrears will also be paid at that date. The required return is 17%. The shares are currently trading at R24,00 each. Timeline with contents • PV perpetuity = Annuity ÷ i • = 3.00 (R20 X 15% = R3) ÷ 0.17 = R17.65 • You now have to decide at what period (T) you will calculate the PV of the perpetuity: You can calculate it at either T1 or T2. Either way you will get the same answer. • IMPORTANT: remember that the PV of a perpetuity is always in the period before e.g. if we calculate the PV of the perpetuity in T1 it is the value at T0, and if we calculate the value at T2 it is the value at T1. Time Value of Money - Perpetuity OPTION 1: If we calculate it at T1: • PV perpetuity = R17.65 and this value is at T0 • So we need to discount the dividend in arrears of R9 to T0 and add the two values (the value of the div in arrears and that of the perp) to get the total value per share. • Discounting of div in arrears to T0: • FV = 9 ; I/Yr = 17 • N = 1 ; PV = 7.69 • Value per share = 17.65 + 7.69 = R25.34 • She should not pay more than R25.34 per share. At R24.00 the shares are underpriced and I therefore recommend that she invest. Time Value of Money - Perpetuity OPTION 2: If we calculate the perpetuity at T2 • PV perpetuity = R17.65, but this value is at T1 • We now have three values at T1: • The value of the perpetuity at R17.65 • The R9 div in arrears • As well as the R3 div for year 1 that has not been included in the calc of the value of the perpetuity as we calculated the value in year 2. • We now add the three values at T1 and discount them back to T0 to get the total value per share. • FV = (9+3+17.65); I /Yr = 17 • N = 1; PV = 25.34 • She should not pay more than R25.34 per share. At R24.00 the shares are under priced and I therefore recommend that she invest. • Both options give us the same correct answer. Time Value of Money – More Examples • We will now take a look at more challenging problems and also more TVM functions on the calculator. These include: • Solving mixed stream cash flows using the CF function on my calculator • Annuities where the frequency of payments and the frequency of interest compounding differs • Loans and amortisation, using the amortisation function on the calculator • • We have seen in the previous section that we can solve Multiple Uneven Cash Flows in 2 Ways: • compound accumulated balance forward one year at a time • calculate future value of each cash flow and add them up However, we can also solve these problems using the CF function on the calculator. Time Value of Money • • Use the highlighted key for starting the process of solving a mixed cash flow problem Press the CF key and down arrow key through a few of the keys as you look at the definitions on the next slide Time Value of Money Defining the calculator variables: For CF0:This is ALWAYS the cash flow occurring at time t=0 (usually 0 for these problems) For Cnn:* This is the cash flow SIZE of the nth group of cash flows. Note that a “group” may only contain a single cash flow (e.g., R351.76). For Fnn:* This is the cash flow FREQUENCY of the nth group of cash flows. Note that this is always a positive whole number (e.g., 1, 2, 20, etc.). * nn represents the nth cash flow or frequency. Thus, the first cash flow is C01, while the tenth cash flow is C10. Time Value of Money • • Example: Julie Miller will receive the set of cash flows below. What is the Present Value at a discount rate of 10%. (Answer: R1 677.15) 0 1 2 3 4 5 10% R600 R600 R400 R400 R100 PV0 Time Value of Money • • • • • • Up till now we have been dealing with scenarios with yearly payments (or receipts for that matter) and interest rates with yearly compounding. This meant that the frequency of the cash flow was equal to the frequency of the compounding of the interest rate. This will however not always be the case. We could for example be faced with a scenario where a person saves a monthly amount, and we are given a effective interest rate. Now the frequencies differ: cash flows are monthly, compounding is yearly (effective). This creates a problem when using the calculator. Lets explore this. Time Value of Money – Loan Amortisation • • Julie Miller is borrowing R10 000 at a compound annual interest rate of 12%. Amortise the loan if annual payments are made for 5 years. Step 1: Payment Inputs 5 N Compute • 12 I/Y 10,000 PV 0 PMT FV -2774.10 The result indicates that a R10 000 loan that costs 12% annually for 5 years and will be completely paid off at that time, will require R2 774.10 annual payments. Time Value of Money – Loan Amortisation End of Year 0 Payment Interest Principal --- --- --- 1 R2 774 R1 200 R1 574 8 426 2 2 774 1 011 1 763 6 663 3 2 774 800 1 974 4 689 4 2 774 563 2 211 2 478 5 2 775 297 2 478 0 R13 871 R3 871 R10 000 [Last Payment Slightly Higher Due to Rounding] Ending Balance R10 000 Time Value of Money – Loan Amortisation Press: 1 INPUT 1 AMORT (selects the period that you are interested in, which in this case is year 1) = = = Results: = -1,574.10 = PRIN (capital repaid) = -1,200.00 = INT (interest paid) = 8,425.90 = BAL (outstanding capital) Year 1 information only Time Value of Money – Loan Amortisation Press: 1 INPUT 5 AMORT (selects the period that you are interested in, which in this case is years 1 to 5) = = = Results: = -10 000 = PRIN (capital repaid) = -3 870.48 = INT (interest paid) = 0 = BAL (outstanding capital) Year 1-5 information Time Value of Money – Usefulness of Amortization • • Determine Interest Expense -- Interest expenses may reduce taxable income of the company. Calculate Debt Outstanding -- The quantity of outstanding debt may be used in financing the day-to-day activities of the company Time Value of Money - Example • • Mr Kruger is 45 years old today and wants to retire in 10 years time at age 55. He does not want to use any of his current investments for retirement. When he retires, he wants to buy a motor vehicle valued at R200 000. Exactly a year after that he wants to buy a house in Camps Bay valued at R4 500 000. He also wants to receive R500 000 per year at the end of each year for the rest of his life. YOU ARE REQUIRED TO: calculate the yearly payment which Mr Kruger has to invest today and the next seven years if he can earn 15%, compounded semi-annually on his annuity. Year 0 Year 10 R200 000 Year 11 R4,5million R500 000 Year 12 R500 000 Nominal interest rate = 15% per annum, compounded semi-annually Effective interest rate = 15,56% per annum 2 P/YR, NOM % = 15, EFF % = 15,56 Present value of R200 000 lump sum: P/YR = 1, FV = 200 000, n = 10, I/YR = 15,56, PV = 47 092,82 Time Value of Money • Present value of R4 500 000 lump sum: P/YR = 1, FV = 4 500 000, n = 11, I/YR = 15,56, PV = 916 916,21 • Present value (in year 10) of R500 000 perpetuity: 500 000 / 0,1556 = 3 213 367,61 • Present value (in year 0) of above lump sum: P/YR = 1, FV = 3 213 367,61, n = 10, I/YR = 15,56, PV = 756 632,54 • Present value of total amount required for retirement: PV of R200 000 lump sum 47 092,82 PV of R4 500 000 lump sum 916 916,21 PV of R500 000 perpetuity 756 632,54 1 720 641,57 Annual investment required to fund above lump sum: BEGIN Mode P/YR =1 n =8 I/YR = 15,56 PV = 1 720 641,57 PMT = 337 946,45 Time Value of Money • • • • • • • • • Shaun Klusener would like to attend the 2004 cricket World Cup in Australia. His cost estimates are as follows: Plane tickets (payable 31 March 2004) R10 000 Tickets for the games (payable 31 July 2004) R15 000 Australian Dollars for spending money (payable31 August 2004) R25 000 Shaun also plans to spend a whole year playing cricket in Australia after the World Cup. He estimates that he will need about R15 000 per month (payable at the end of every month) from October 2004 to cover his living expenses. After 12 months of non-stop cricket he will return to South Africa to resume his professional life as auditor. At the moment Shaun has R20 000 available in cash. He wants to deposit at the end of every month an amount to enable him to fulfil his dreams. He will deposit his R20 000 on 31 March 2000, and will make the first monthly payment on 30 April 2000. The last deposit in his investment account will be made on 31 July 2004. The return on the investment is 18% p.a., compounded quarterly. Round all calculations to two decimals. Calculate the monthly amount that Shaun should invest to enable him to carry out all his plans Time Value of Money 31/3/00 30/4/00 31/3/04 31/7/04 31/8/04 (10 000) (15 000) (25 000) 30/9/04 31/10 – 30/9 20 000 (15 000 p.m.) PV(10 000) PV(15 000) PV(25 000) PV (annuity) PV(annuity) Funds required Montly deposits Time Value of Money • • • • • • Rate of return = 18% p.a. compounded quarterly = 19,25% p.a. effective = 17,74% p.a. compounded monthly Calculate the PV (at 30/9/2004) of the R15 000 p.m. for 12 months: 12 P/YR, n = 12, I/YR = 17,74, PMT = 15 000, PV = 163 833,62 Calculate the PV (on 31/3/2000) of above amount: 12 P/YR, n = 54, I/YR = 17,74, FV = 163 833,62, PV = 74 172,59 Calculate the PV (at 31/3/2000) of the plane tickets: 12 P/YR, n = 48, I/YR = 17,74, FV = 10 000, PV = 4 944,02 Calculate the PV(at 31/3/2000) of the cricket tickets: 12 P/YR, n = 52, I/YR = 17,74, FV = 15 000, PV = 6 993,24 Calculate the PV (at 31/3/2000) of the spending money: 12 P/YR, n = 53, I/YR = 17,74, FV = 25 000, PV = 11 485,60 Time Value of Money • • At 31/3/2000 the situation is as follows: Deposit 20 000,00 Plane tickets (4 944,02) Cricket tickets (6 993,24) Spending money (11 485,60) 12 mnths money (74 172,59) Shortfall (77 595,45) Calculate the monthly payments where the PV is the above: 12 P/YR n = 52 I/YR = 17,74 PV = 77 595,45 PMT = 2 149,03