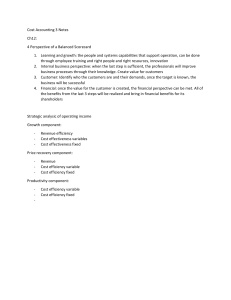

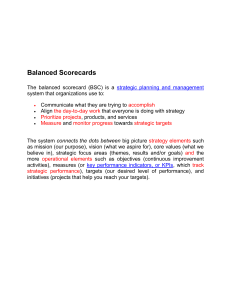

Principles of Management Topic 10 CONTROL: WHEN MANAGERS MONITOR PERFORMANCE MSc. Giang Nguyen Learning Programme Topic Session topic Indicative reading (core text) 1 Topic 1. An introduction to management concepts and theories Ch1 & 2 2 Topic 2. Organization and environment Ch3, Ch4 & Ch8 3 Topic 3. Planning Ch5 & Ch6 4 Topic 4. Decision making Ch7 5 Topic 5. Organizational Structure and design Ch8 6 Ch9 7 Topic 6. Human Resource Management Topic 7. Motivating employees 8 9 10 Topic 8. Power, Influence and Leadership Topic 9. Organizational communication Topic 10. Controlling Ch14 Ch15 Ch16 Ch12 2 Core text: Kinicki, Angelo & Williams, Brian K. (2013). Management, a practical introduction. (6th Ed.). McGraw-Hill 1 LEARNING OUTCOMES ▰To understand the foundation of control, the control process, levels and areas of control ▰To recognise different controlling tools and techniques i.e balance scorecard, TQM etc 3 CONTENTS 1 The nature of control 2 Levels and areas of control 3 The balanced scorecard 4 Strategy map 5 Measurement management 4 2 1. THE NATURE OF CONTROL What is Control? Controlling is monitoring performance, comparing it with goals, and taking corrective action as needed. 5 1. THE NATURE OF CONTROL What is Control? 6 3 1. THE NATURE OF CONTROL Why Control? ▰To adapt to change and uncertainty ▰To discover irregularities and errors ▰To reduce costs, increase productivity or add value ▰To detect opportunities ▰To deal with complexity ▰To de-centralize decision making and facilitate teamwork 7 1. THE NATURE OF CONTROL The Control Process “What is the desired outcome we want?” Establish standards “What is the actual outcome we got?” Measure performance “How do the desired and actual outcomes differ?” Compare performance to standards “What changes should we make to obtain desirable outcomes?” Take corrective action, if necessary 8 4 1. THE NATURE OF CONTROL The Control Process Step 1: Establish Standards ▰ Standards are best measured when can be made quantifiable ▰ Standards in: Nonprofit institution vs for-profit organizations ▰ Standards can be subjective ▰ Technique for setting standards: the balanced scorecard 9 1. THE NATURE OF CONTROL The Control Process Step 2: Measure Performance ▰ Sources: ▻ written reports ▻ oral reports ▻ personal observation ▻ statistical reports 10 5 Personal observation Advantages - Get firsthand knowledge - Information isn’t filtered - Intensive coverage of work activities - Easy to visualize Statistical reports - Effective for showing relationships Oral reports Written reports Drawbacks - Subject to personal biases - Time-consuming - Obstructive - Provide limited information - Ignore subjective factors - Fast way to get information - Allow for verbal and nonverval feedback - Information is filtered - Information can’t be documented - Comprehensive - Formal - Easy to file and retrieve - Take more time to prepare 11 1. THE NATURE OF CONTROL The Control Process Step 3: Compare performance to standards ▰ The greater the difference between desired and actual performance, the greater the need for action ▰ The acceptable deviation depends on the range of variation built in to the standards in step 1. 12 6 1. THE NATURE OF CONTROL The Control Process Step 4: Take Corrective action, if necessary 3 possibilities: ▰ Make no changes ▰ Recognize and reinforce positive performance ▰ Take action to correct negative performance 13 1. THE NATURE OF CONTROL The Control Process 14 7 Revision Question 1 Establishing standards, comparing actual results with standards and taking corrective actions are the steps included in the process of A. planning B. controlling C. directing D. organizing 15 Question 2 Control function of management cannot be performed without: A. planning B. organizing C. staffing D. motivation 16 8 Question 3 What is not true about controlling A. Standards can be objective or subjective B. Standards are best measured when can be made qualifiable C. Different sources of measuring have different level of reliability D. Setting tandards are very important in controlling 17 Question 4 Daniel manages a team that has missed their production goals for the past three months. After reviewing each employee's performance record, Daniel adjusted the sales goal to take additional quality control measures into consideration. Why is this an example of controlling? A. Because somebody will likely get fired as a result of this analysis B. Because Daniel acted as a leader and took responsibility for the project C. Because Daniel looked at team results and took appropriate corrective action. D. Because Daniel is micromanaging his employees. 18 9 Question 5 What is a benefit of controlling? A. To deal with change B. To deal with complexity C. To deal with uncertainty D. To deal with threats 19 2. LEVELS AND AREAS OF CONTROL Levels of Control Strategic control Operational control Tactical control 20 10 2. LEVELS AND AREAS OF CONTROL Levels of Control ▰Strategic Control: - monitoring performance to ensure that strategic plans are being implemented and taking corrective action as needed - mainly performed by top managers (CEO and VP levels) - every 3, 6, 12, or more months 21 2. LEVELS AND AREAS OF CONTROL Levels of Control ▰Tactical Control: - monitoring performance to ensure that tactical plans (divisional or departmental level) are being implemented and taking corrective action as needed - done mainly by middle managers (division head, plant manager,…) - done on a weekly or monthly basis 22 11 2. LEVELS AND AREAS OF CONTROL Levels of Control ▰Operational Control: - monitoring performance to ensure that operational plans (day-to-day goals) are being implemented and taking corrective action as needed - done mainly by first-level managers (department head, team leader, supervisor…) - done on a daily basis 23 2. LEVELS AND AREAS OF CONTROL Areas of Control Physical Area Human Resources Area Cultural Area Informati onal Area Structural Area Financial Area 24 12 2. LEVELS AND AREAS OF CONTROL Areas of Control ▰Physical Area Equipment controls Quality controls Inventorymanagement control 25 2. LEVELS AND AREAS OF CONTROL Areas of Control ▰ Human Resources Area Personality Tests & drug testing v For hiring Performance evaluations v Work productivity Performance tests v For training Employee surveys v Access job satisfaction and leadership 26 13 2. LEVELS AND AREAS OF CONTROL Areas of Control ▰Informational Area Production Schedules Sales forecasts Environmental impact statement Analyses of competition PR briefings 27 2. LEVELS AND AREAS OF CONTROL Areas of Control ▰Financial Area budgets Bills, money owed, cash on hand…? ratio analysis financial statements audits 28 14 2. LEVELS AND AREAS OF CONTROL Areas of Control ▰Structural Area Bureaucratic control Decentralized control ▰ Cultural Area: informal method of control 29 3. THE BALANCED SCORECARD • adopted by over 50% of large US firms • top ten most widely used management tools around the world • the most influential business ideas of the past 75 years Robert S. Kaplan Havard Business School David P. Norton Renaissance Strategy Group 30 15 3. THE BALANCED SCORECARD 4 indicators in Balanced Scorecard: - Financial measures - Innovation and improvement activities - Customer satisfaction - Internal processes 31 3. THE BALANCED SCORECARD 32 16 3. THE BALANCED SCORECARD The balanced scorecard establishes goals and performance measures according to four “perspectives” or areas: ▰ Financial Perspective: “How do we look to shareholders?” ▰ Innovation and Learning Perspective: “Can we continue to improve and create value?” ▰ Customer perspective: “How do customers see us” ▰ Internal Business perspective: “What must we excel at?” 33 4. STRATEGY MAP ▰ Strategy map is a visual representation of the four perspectives of the balanced scorecard that enables managers to communicate their goals so that everyone in the company can understand how their jobs are linked to the overall objective of the organizations 34 17 4. STRATEGY MAP ▰ “Strategy maps show the cause-and-effect links by which specific improvements create desired outcomes” 35 4. STRATEGY MAP (Kaplan & Norton 1996) 36 18 37 5. SOME FINANCIAL TOOLS FOR CONTROL ▰2 tools: ▻ Budget: a formal financial projection ▻Financial statement: A summary of some aspect of an organization’s financial status 38 19 5. SOME FINANCIAL TOOLS FOR CONTROL There are two different ways to budget: ❖ Incremental budgeting allocates increased or decreased funds to a department by using the last budget as a reference point—only incremental changes in the budget request are reviewed ❖ Zero-based budgeting forces each department to start from zero in projecting its funding needs for the budget period There two different types of budgets: ❖ Fixed budgets allocate resources on the basis of a single estimate of costs ❖ Variable budgets allow the allocation of resources to vary in proportion with various levels of activity 39 5. SOME FINANCIAL TOOLS FOR CONTROL ❖ There are two basic types of financial statements: ❖ A balance sheet summarizes an organization’s overall financial worth (assets and liabilities) at a specific point in time where: ❖ -assets are the resources the organization controls, current assets are cash and other assets that are readily convertible to cash fixed assets are property, buildings, and equipment that are harder to convert to cash, and liabilities are claims by suppliers, lenders, and others 40 20 5. SOME FINANCIAL TOOLS FOR CONTROL ❖ The income statement summarizes an organization’s financial results - revenues (the assets from the sale of goods) and expenses (the costs required to produce goods and services) - over a specified period of time ❖ Liquidity ratios indicate how easily a company’s assets can be converted to cash ❖ Debt-management ratios indicate the degree to which an organization can meet its long-term financial obligations ❖ Asset management ratios indicate how effectively an organization is managing resources ❖ Return ratios indicate how effective management is at generating a return on assets 41 5. SOME FINANCIAL TOOLS FOR CONTROL ❖ Formal verifications of an organization’s financial and operational systems are called audits ❖ There are two types of audits: ❖ An external audit is a formal verification of an organization’s financial accounts and statements by outside experts ❖ An internal audit is a verification of an organization’s financial accounts and statements by the organization’s own professional staff 42 21 6. MANAGING CONTROL EFFECTIVELY Successful control systems are: 1. Strategic & results oriented – they support strategic plans and focus on activities that will make a real difference to the firm 2. Timely, accurate, & objective 3. Realistic, positive, & understandable & encourage self-control 4. Flexible - so that they can be modified as needed 43 6. MANAGING CONTROL EFFECTIVELY There are several barriers that can limit successful control: 1. Too much control - when companies exert too much control, employees may rebel 2. Too little employee participation - employee participation can enhance productivity 3. Overemphasis on means instead of ends 4. Overemphasis on paperwork - unnecessary emphasis on paperwork can reduce effort in other areas 5. Overemphasis on one instead of multiple approaches - using multiple control activities can increase accuracy and objectivity 44 22 Question The balanced score card sets goals and performance measures from all of the following perspectives except A) innovation and learning B) financial C) customer D) productivity 45 Question Which type of control issues reports on a weekly or monthly basis? A) strategic B) operational C) supervisory D) tactical 46 23 Question Ratios that indicate how effectively an organization is managing resources are A) return ratios B) liquidity ratios C) asset management ratios D) debt management ratios 47 Question Which of the following is not a barrier to successful control? A) flexibility B) too much control C) overemphasis on paperwork D) too little employee participation 48 24 Question A UPS driver fails to perform according to the standards set for the route and traffic conditions. A supervisor rides along and gives suggestions for improvement. This is the ____________ stage of the control process. A. Compare performance to standards B. Establish standards C. Take corrective action D. Measure performance Question A drug test employed by an organization in its hiring process is an example of a(n) _______ resource control. A. Physical B. Human C. Financial D. Informational 25