Financial Machine Learning

Bryan Kelly

Yale University and AQR Capital Management

bryan.kelly@yale.edu

Dacheng Xiu

University of Chicago

dacheng.xiu@chicagobooth.edu

Electronic copy available at: https://ssrn.com/abstract=4501707

Contents

1 Introduction: The Case for Financial Machine Learning

1.1 Prices are Predictions . . . . . . . . . . . . . . . . . . . .

1.2 Information Sets are Large . . . . . . . . . . . . . . . . .

1.3 Functional Forms are Ambiguous . . . . . . . . . . . . . .

1.4 Machine Learning versus Econometrics . . . . . . . . . . .

1.5 Challenges of Applying Machine Learning in Finance (and

the Benefits of Economic Structure) . . . . . . . . . . . .

1.6 Economic Content (Two Cultures of Financial Economics)

9

10

2 The

2.1

2.2

2.3

15

16

20

26

Virtues of Complex Models

Tools For Analyzing Machine Learning Models . . . . . . .

Bigger Is Often Better . . . . . . . . . . . . . . . . . . . .

The Complexity Wedge . . . . . . . . . . . . . . . . . . .

3 Return Prediction

3.1 Data . . . . . . . . . . . . . . . . .

3.2 Experimental Design . . . . . . . . .

3.3 A Benchmark: Simple Linear Models

3.4 Penalized Linear Models . . . . . . .

3.5 Dimension Reduction . . . . . . . .

3.6 Decision Trees . . . . . . . . . . . .

3.7 Vanilla Neural Networks . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Electronic copy available at: https://ssrn.com/abstract=4501707

.

.

.

.

.

.

.

2

2

3

5

6

28

31

32

37

40

44

53

59

3.8 Comparative Analyses . . . . . . . . . . . . . . . . . . . .

3.9 More Sophisticated Neural Networks . . . . . . . . . . . .

3.10 Return Prediction Models For “Alternative” Data . . . . .

4 Risk-Return Tradeoffs

4.1 APT Foundations . . . . . .

4.2 Unconditional Factor Models

4.3 Conditional Factor Models .

4.4 Complex Factor Models . . .

4.5 High-frequency Models . . .

4.6 Alphas . . . . . . . . . . . .

64

68

70

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

79

79

80

88

94

96

98

5 Optimal Portfolios

5.1 “Plug-in” Portfolios . . . . . . . . . . . .

5.2 Integrated Estimation and Optimization .

5.3 Maximum Sharpe Ratio Regression . . . .

5.4 High Complexity MSRR . . . . . . . . . .

5.5 SDF Estimation and Portfolio Choice . . .

5.6 Trading Costs and Reinforcement Learning

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

105

107

111

112

116

118

126

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

6 Conclusions

132

References

134

Electronic copy available at: https://ssrn.com/abstract=4501707

Financial Machine Learning

Bryan Kelly1 and Dacheng Xiu2

1 Yale

School of Management, AQR Capital Management, and NBER;

bryan.kelly@yale.edu

2 University of Chicago Booth School of Business;

dacheng.xiu@chicagobooth.edu

ABSTRACT

We survey the nascent literature on machine learning in the

study of financial markets. We highlight the best examples

of what this line of research has to offer and recommend

promising directions for future research. This survey is designed for both financial economists interested in grasping

machine learning tools, as well as for statisticians and machine learners seeking interesting financial contexts where

advanced methods may be deployed.

Acknowledgements. We are grateful to Doron Avramov, Max Helman, Antti Ilmanen, Sydney Ludvigson, Yueran Ma, Semyon Malamud,

Tobias Moskowitz, Lasse Pedersen, Markus Pelger, Seth Pruitt, and

Guofu Zhou for helpful comments. AQR Capital Management is a global

investment management firm, which may or may not apply similar investment techniques or methods of analysis as described herein. The

views expressed here are those of the authors and not necessarily those

of AQR.

Electronic copy available at: https://ssrn.com/abstract=4501707

1

Introduction: The Case for Financial Machine

Learning

1.1

Prices are Predictions

Modern analysis of financial markets centers on the following definition

of a price, derived from the generic optimality condition of an investor:

Pi,t = E[Mt+1 Xi,t+1 |It ].

(1.1)

In words, the prevailing price of an asset, Pi,t , reflect investors’ valuation

of its future payoffs, Xi,t+1 . These valuations are discounted based on investors’ preferences, generically summarized as future realized marginal

rates of substitution, Mt+1 . The price is then determined by investor

expectations of these objects given their conditioning information It . In

other words, prices are predictions—they reflect investors’ best guesses

for the (discounted) future payoffs shed by an asset.

It is common to analyze prices in an equivalent expected return, or

“discount rate,” representation that normalizes (1.1) by the time t price:

E[Ri,t+1 |It ] = βi,t λt ,

(1.2)

where Ri,t+1 = Xi,t+1 /Pi,t − Rf,t is the asset’s excess return, Rf,t =

Cov[Mt+1 ,Ri,t+1 |It ]

E[Mt+1 |It ]−1 is the one-period risk-free rate, βi,t =

is

Var[Mt+1 |It ]

2

Electronic copy available at: https://ssrn.com/abstract=4501707

1.2. Information Sets are Large

3

t+1 |It ]

the asset’s covariance with Mt+1 , and λt = − Var[M

E[Mt+1 |It ] is the price

of risk. We can ask economic questions in terms of either prices or

discount rates, but the literature typically opts for the discount rate

representation for a few reasons. Prices are often non-stationary while

discount rates are often stationary, so when the statistical properties

of estimators rely on stationarity assumptions it is advantageous to

work with discount rates. Also, uninteresting differences in the scale of

assets’ payoffs will lead to uninteresting scale differences in prices. But

discount rates are typically unaffected by differences in payoff scale so

the researcher need not adjust for them.

More generally, studying market phenomena in terms of returns

alleviates some of the researcher’s modeling burden by partially homogenizing data to have tractable dynamics and scaling properties.

Besides, discount rates are also predictions, and their interpretation

is especially simple and practically important. E[Ri,t+1 |It ] describes

investors’ expectations for the appreciation in asset value over the next

period. As such, the expected return is a critical input to allocation

decisions. If we manage to isolate an empirical model for this expectation that closely fits the data, we have achieved a better understanding

of market functionality and simultaneously derived a tool to improve

resource allocations going forward. This is a fine example of duality in

applied social science research: A good model both elevates scientific

understanding and improves real-world decision-making.

1.2

Information Sets are Large

There are two conditions of finance research that make it fertile soil

for machine learning methods: large conditioning information sets and

ambiguous functional forms. Immediately evident from (1.1) is that

the study of asset prices is inextricably tied to information. Guiding

questions in the study of financial economics include “what information

do market participants have and how do they use it?” The predictions

embodied in prices are shaped by the available information that is

pertinent to future asset payoffs (Xi,t+1 ) and investors’ feelings about

those payoffs (Mt+1 ). If prices behaved the same in all states of the

world—e.g. if payoffs and preferences were close to i.i.d.—then infor-

Electronic copy available at: https://ssrn.com/abstract=4501707

4

Introduction: The Case for Financial Machine Learning

mation sets would drop out. But even the armchair investor dabbling

in their online account or reading the latest edition of The Wall Street

Journal quickly intuits the vast scope of conditioning information lurking behind market prices. Meanwhile, the production function of the

modern asset management industry is a testament to the vast amount of

information flowing into asset prices: Professional managers (in various

manual and automated fashions) routinely pore over troves of news

feeds, data releases, and expert predictions in order to inform their

investment decisions.

The expanse of price-relevant information is compounded by the

panel nature of financial markets. The price of any given asset tends

to vary over time in potentially interesting ways—this corresponds to

the time series dimension of the panel. Meanwhile, at a given point in

time, prices differ across assets in interesting ways—the cross section

dimension of the panel. Time series variation in the market environment

will affect many assets in interconnected ways. For example, most asset

prices behave differently in high versus low risk conditions or in different

policy regimes. As macroeconomic conditions change, asset prices adjust

in unison through these common effects. Additionally, there are crosssectional behaviors that are distinct to individual assets or groups of

assets. So, conditioning information is not just time series in nature,

but also includes asset-level attributes. A successful model of asset

behavior must simultaneously account for shared dynamic effects as well

as asset-specific effects (which may themselves be static or dynamic).

As highlighted by Gu et al. (2020b),

The profession has accumulated a staggering list of predictors that various researchers have argued possess forecasting

power for returns. The number of stock-level predictive characteristics reported in the literature numbers in the hundreds

and macroeconomic predictors of the aggregate market number in the dozens.

Furthermore, given the tendency of financial economics research to

investigate one or a few variables at a time, we have presumably left

much ground uncovered. For example, only recently has the information

content of news text emerged as an input to empirical models of (1.1),

Electronic copy available at: https://ssrn.com/abstract=4501707

1.3. Functional Forms are Ambiguous

5

and there is much room for expansion on this frontier and others.

1.3

Functional Forms are Ambiguous

If asset prices are expectations of future outcomes, then the statistical

tools to study prices are forecasting models. A traditional econometric

approach to financial market research (e.g. Hansen and Singleton, 1982)

first specifies a functional form for the return forecasting model motivated by a theoretical economic model, then estimates parameters to

understand how candidate information sources associate with observed

market prices within the confines of the chosen model. But which of the

many economic models available in the literature should we impose?

The formulation of the first-order condition, or “Euler equation,”

in (1.1) is broad enough to encompass a wide variety of structural

economic assumptions. This generality is warranted because there is no

consensus about which specific structural formulations are viable. Early

consumption-based models fail to match market price data by most

measures (e.g. Mehra and Prescott, 1985). Modern structural models

match price data somewhat better if the measure of success is sufficiently

forgiving (e.g. Chen et al., 2022a), but the scope of phenomena they

describe tends to be limited to a few assets and is typically evaluated

only on an in-sample basis.

Given the limited empirical success of structural models, most empirical work in the last two decades has opted away from structural

assumptions to less rigid “reduced-form” or “no-arbitrage” frameworks.

While empirical research of markets often steers clear of imposing detailed economic structure, it typically imposes statistical structure (for

example, in the form of low-dimensional factor models or other parametric assumptions). But there are many potential choices for statistical

structure in reduced-form models, and it is worth exploring the benefits

of flexible models that can accommodate many different functional

forms and varying degrees of nonlinearity and variable interactions.

Enter machine learning tools such as kernel methods, penalized

likelihood estimators, decision trees, and neural networks. Comprised of

diverse nonparametric estimators and large parametric models, machine

learning methods are explicitly designed to approximate unknown data

Electronic copy available at: https://ssrn.com/abstract=4501707

6

Introduction: The Case for Financial Machine Learning

generating functions. In addition, machine learning can help integrate

many data sources into a single model. In light of the discussion in

Section 1.2, effective modeling of prices and expected returns requires

rich conditioning information in It . On this point, Cochrane (2009)1

notes that “We obviously don’t even observe all the conditioning information used by economic agents, and we can’t include even a fraction of

observed conditioning information in our models.” Hansen and Richard

(1987) (and more recently Martin and Nagel, 2021) highlight differences

in information accessible to investors inside an economic model versus

information available to an econometrician on the outside of a model

looking in. Machine learning is a toolkit that can help narrow the

gap between information sets of researchers and market participants

by providing methods that allow the researcher to assimilate larger

information sets.

The more expansive we can be in our consideration of large conditioning sets, the more realistic our models will be. This same logic

applies to the question of functional form. Not only do market participants impound rich information into their forecasts, they do it in

potentially complex ways that leverage the nuanced powers of human

reasoning and intuition. We must recognize that investors use information in ways that we as researchers cannot know explicitly and thus

cannot exhaustively (and certainly not concisely) specify in a parametric

statistical model. Just as Cochrane (2009) reminds us to be circumspect

in our consideration of conditioning information, we must be equally

circumspect in our consideration of functional forms.

1.4

Machine Learning versus Econometrics

What is machine learning, and how is it different from traditional econometrics? Gu et al. (2020b) emphasize that the definition of machine

learning is inchoate and the term is at times corrupted by the marketing purposes of the user. We follow Gu et al. (2020b) and use the

term to describe (i) a diverse collection of high-dimensional models for

1

Readers of this survey are encouraged to re-visit chapter 8 of Cochrane (2009)

and recognize the many ways machine learning concepts mesh with his outline of

the role of conditioning information in asset prices.

Electronic copy available at: https://ssrn.com/abstract=4501707

1.4. Machine Learning versus Econometrics

7

statistical prediction, combined with (ii) “regularization” methods for

model selection and mitigation of overfit, and (iii) efficient algorithms

for searching among a vast number of potential model specifications.

Given this definition, it should be clear that, in any of its incarnations, financial machine learning amounts to a set of procedures

for estimating a statistical model and using that model to make decisions. So, at its core, machine learning need not be differentiated from

econometrics or statistics more generally. Many of the ideas underlying

machine learning have lived comfortably under the umbrella of statistics

for decades (Israel et al., 2020).

In order to learn through the experience of data, the machine

needs a functional representation of what it is trying to learn. The

researcher must make a representation choice—this is a canvas upon

which the data will paint its story. Part (i) of our definition points

out that machine learning brings an open-mindedness to functional

representations that are highly parameterized and often nonlinear. Small

models are rigid and oversimplified, but their parsimony has benefits like

comparatively precise parameter estimates and ease of interpretation.

Large and sophisticated models are much more flexible, but can also be

more sensitive and suffer from poor out-of-sample performance when

they overfit noise in the system. Researchers turn to large models

when they believe the benefits from more accurately describing the

complexities of real world phenomena outweigh the costs of potential

overfit. At an intuitive level, machine learning is a way to pursue

statistical analysis when the analyst is unsure which specific structure

their statistical model should take. In this sense, much of machine

learning can be viewed as nonparametric (or semi-parametric) modeling.

Its modus operandi considers a variety of potential model specifications

and asks the data’s guidance in choosing which model is most effective

for the problem at hand. One may ask: when does the analyst ever

know what structure is appropriate for their statistical analysis? The

answer of course is “never,” which is why machine learning is generally

valuable in financial research. As emphasized by Breiman (2001), its

focus on maximizing prediction accuracy in the face of an unknown

data model is the central differentiating feature of machine learning

from the traditional statistical objective of estimating a known data

Electronic copy available at: https://ssrn.com/abstract=4501707

8

Introduction: The Case for Financial Machine Learning

generating model and conducting hypothesis tests.

Part (ii) of our definition highlights that machine learning chooses a

preferred model (or combination of models) from a “diverse collection”

of candidate models. Again, this idea has a rich history in econometrics

under the heading of model selection (and, relatedly, model averaging).

The difference is that machine learning puts model selection at the

heart of the empirical design. The process of searching through many

models to find top performers (often referred to as model “tuning”)

is characteristic of all machine learning methods. Of course, selecting

from multiple models mechanically leads to in-sample overfitting and

can produce poor out-of-sample performance. Thus machine learning

research processes are accompanied by “regularization,” which is a

blanket term for constraining model size to encourage stable performance

out-of-sample. As Gu et al. (2020b) put it, “An optimal model is a

‘Goldilocks’ model. It is large enough that it can reliably detect potentially

complex predictive relationships in the data, but not so flexible that it is

dominated by overfit and suffers out-of-sample.” Regularization methods

encourage smaller models; richer models are only selected if they are

likely to give a genuine boost to out-of-sample prediction accuracy.

Element (iii) in the machine learning definition is perhaps its clearest differentiator from traditional statistics, but also perhaps the least

economically interesting. When data sets are large and/or models are

very heavily parameterized, computation can become a bottleneck. Machine learning has developed a variety of approximate optimization

routines to reduce computing loads. For example, traditional econometric estimators typically use all data points in every step of an iterative

optimization routine and only cease the parameter search when the

routine converges. Shortcuts such as using subsets of data and halting

a search before convergence often reduce computation and do so with

little loss of accuracy (see, e.g., stochastic gradient descent and early

stopping which are two staples in neural network training).

Electronic copy available at: https://ssrn.com/abstract=4501707

1.5. Challenges of Applying Machine Learning in Finance (and the

Benefits of Economic Structure)

1.5

9

Challenges of Applying Machine Learning in Finance (and the

Benefits of Economic Structure)

While financial research is in many ways ideally suited to machine learning methods, some aspects of finance also present challenges for machine

learning. Understanding these obstacles is important for developing

realistic expectations about the benefits of financial machine learning.

First, while machine learning is often viewed as a “big data” tool,

many foundational questions in finance are frustrated by the decidedly

“small data” reality of economic time series. Standard data sets in macro

finance, for example, are confined to a few hundred monthly observations.

This kind of data scarcity is unusual in other machine learning domains

where researchers often have, for all intents and purposes, unlimited

data (or the ability to generate new data as needed). In time series

research, new data accrues only through the passage of time.

Second, financial research often faces weak signal-to-noise ratios.

Nowhere is this more evident than in return prediction, where the forces

of market efficiency (profit maximization and competition) are ever

striving to eliminate the predictability of price movements (Samuelson, 1965; Fama, 1970). As a result, price variation is expected to

emanate predominantly from the arrival of unanticipated news (which

is unforecastable noise from the perspective of the model). Markets

may also exhibit inefficiencies and investor preferences may give rise to

time-varying risk premia, which result in some predictability of returns.

Nonetheless, we should expect return predictability to be small and

fiercely competed over.

Third, investors learn and markets evolve. This creates a moving

target for machine learning prediction models. Previously reliable predictive patterns may be arbitraged away. Regulatory and technological

changes alter the structure of the economy. Structural instability makes

finance an especially complex learning domain and compounds the

challenges of small data and low signal-to-noise ratios.

These challenges present an opportunity to benefit from knowledge

gained by economic theory. As noted by Israel et al. (2020),

“A basic principle of statistical analysis is that theory and

model parameters are substitutes. The more structure you

Electronic copy available at: https://ssrn.com/abstract=4501707

10

Introduction: The Case for Financial Machine Learning

can impose in your model, the fewer parameters you need

to estimate and the more efficiently your model can use

available data points to cut through noise. That is, models are

helpful because they filter out noise. But an over-simplified

model can filter out some signal too, so in a data-rich and

high signal-to-noise environment, you would not want to use

an unnecessarily small model. One can begin to tackle small

data and low signal-to-noise problems by bringing economic

theory to describe some aspects of the data, complemented

by machine learning tools to capture aspects of the data for

which theory is silent.”

1.6

Economic Content (Two Cultures of Financial Economics)

We recall Breiman (2001)’s essay on the “two cultures” of statistics,

which has an analogue in financial economics (with appropriate modifications). One is the “structural model/hypothesis test” culture, which

favors imposing fully or partially specified structural assumptions and

investigating economic mechanisms through hypothesis tests. The traditional program of empirical asset pricing analysis (pre-dating the

emergence of reduced form factor models and machine learning prediction models) studies prices through the lens of heavily constrained

prediction models. The constraints come in the form of i) specific functional forms/distributions, and ii) limited variables admitted into the

conditioning information set. These models often “generalize” poorly

in the sense that they have weak explanatory power for asset price

behaviors outside the narrow purview of the model design or beyond

the training data set. This is such an obvious statement that one rarely

considers out-of-sample performance of fully specified structural asset

pricing models.

The other is the “prediction model” culture, which values statistical explanatory power above all else, and is born largely from the

limitations of the earlier established structural culture. The prediction

model culture willingly espouses model specifications that might lack

an explicit association with economic theory, so long as they produce

meaningful, robust improvements in data fit versus the status quo. In

Electronic copy available at: https://ssrn.com/abstract=4501707

1.6. Economic Content (Two Cultures of Financial Economics)

11

addition to reduced-form modeling that has mostly dominated empirical

finance since the 1990’s, financial machine learning research to date

falls squarely in this second culture.

“There is no economics” is a charge sometimes lobbed at the statistical prediction research by economic seminar audiences, discussants, and

referees. This criticism is often misguided and we should guard against

it unduly devaluing advancements in financial machine learning. Let

us not miss the important economic role of even the purest statistical

modeling applications in finance. Relatively unstructured prediction

models makes them no less economically important than the traditional

econometrics of structural hypothesis testing, they just play a different

scientific role. Hypothesis testing learns economics by probing specific

economic mechanisms. But economics is not just about testing theoretical mechanisms. Atheoretical (for lack of a better term) prediction

models survey the empirical landscape in broader terms, charting out

new empirical facts upon which theories can be developed, and for which

future hypothesis tests can investigate mechanisms. These two forms of

empirical investigation—precision testing and general cartography—play

complementary roles in the Kuhnian process of scientific advancement.

Consider the fundamental question of asset pricing research: What

determines asset risk premia? Even if we could observe expected returns

perfectly, we would still need theories to explain their behavior and

empirical analysis to test those theories. But we can’t observe risk

premia, and they are stubbornly hard to estimate. Machine learning

makes progress on measuring risk premia, which facilitates development

of better theories of economic mechanisms that determine their behavior.

A critical benefit of expanding the set of known contours in the

empirical landscape is that, even if details of the economic mechanisms

remain shrouded, economic actors—financial market participants in

particular—can always benefit from improved empirical maps. The

prediction model culture has a long tradition of producing research

to help investors, consumers, and policymakers make better decisions.

Improved predictions provide more accurate descriptions of the statedependent distributions faced by these economic actors.

Economics is by and large an applied field. The economics of the prediction model culture lies precisely in its ability to improve predictions.

Electronic copy available at: https://ssrn.com/abstract=4501707

12

Introduction: The Case for Financial Machine Learning

Armed with better predictions—i.e., more accurate assessments of the

economic opportunity set—agents can better trade off costs and benefits

when allocating scarce resources. This enhances welfare. Nowhere is

this more immediately clear than in the portfolio choice problem. We

may not always understand the economic mechanisms by which a model

delivers better return or risk forecasts; but if it does, it boosts the utility

of investors and is thus economically important.

Breiman’s central criticism of the structural hypothesis test culture

is that

“when a model is fit to data to draw quantitative conclusions:

the conclusions are about the model’s mechanism, and not

about nature’s mechanism. If the model is a poor emulation

of nature, the conclusions may be wrong.”

We view this less as a criticism of structural modeling, which must

remain a foundation of empirical finance, but rather as a motivation

and defense of prediction models. The two-culture dichotomy is, of

course, a caricature. Research spans a spectrum and draws on multiple

tools, and researchers do not separate into homogenous ideological

camps. Both cultures are economically important. Breiman encourages

us to consider flexible, even nonparametric, models to learn about

economic mechanisms:

“The point of a model is to get useful information about

the relation between the response and predictor variables.

Interpretability is a way of getting information. But a model

does not have to be simple to provide reliable information

about the relation between predictor and response variables;

neither does it have to be a [structural] data model.”

Prediction models are a first step to understanding mechanisms. Moreover, structural modeling can benefit directly from machine learning

without sacrificing pointed hypothesis tests or its specificity of economic

mechanisms.2 Thus far machine learning has predominantly served the

prediction model culture of financial economics. It is important to recognize it as a similarly potent tool for the structural hypothesis testing

2

See, for example, our discussion of Chen and Ludvigson (2009), in Section 5.5.

Electronic copy available at: https://ssrn.com/abstract=4501707

1.6. Economic Content (Two Cultures of Financial Economics)

13

culture (this is a critical direction for future machine learning research

in finance). Surely, a research program founded solely on “measurement

without theory” (Koopmans, 1947) is better served by also considering

data through the lens of economic theory and with a deep understanding

of the Lucas Jr, 1976 critique. Likewise, a program that only interprets

data through extant economic models can overlook unexpected yet

economically important statistical patterns.

Hayek (1945) confronts the economic implications of dispersed information for resource allocation. Regarding his central question of how

to achieve an effective economic order, he notes

If we possess all the relevant information, if we can start

out from a given system of preferences, and if we command

complete knowledge of available means, the problem which

remains is purely one of logic... This, however, is emphatically not the economic problem which society faces. And

the economic calculus which we have developed to solve this

logical problem, though an important step toward the solution of the economic problem of society, does not yet provide

an answer to it. The reason for this is that the ‘data’ from

which the economic calculus starts are never for the whole

society ‘given’ to a single mind which could work out the

implications and can never be so given.

While Hayek’s main interest is in the merits of decentralized planning,

his statements also have implications for information technologies in

general, and prediction technologies in particular. Let us be so presumptuous as to reinterpret Hayek’s statement as a statistical problem: There

is a wedge between the efficiency of allocations achievable by economic

agents when the data generating process (DGP) is known, versus when

it must be estimated. First, there is the problem of model specification—

economic agents simply cannot be expected to correctly specify their

statistical models. They must use some form of mis-specified parametric model or a nonparametric approximating model. In either case,

mis-specification introduces a wedge between the optimal allocations

achievable when the DGP is known (call this “first-best”) and the allocations derived from their mis-specified models (call this “second-best”).

Electronic copy available at: https://ssrn.com/abstract=4501707

14

Introduction: The Case for Financial Machine Learning

But even second best is implausible, because we must estimate these

models with finite data. This gives rise to yet another wedge, that due

to sampling variation. Even if we knew the functional form of the DGP,

we still must estimate it and noise in our estimates produces deviations

from first-best. Compound that with the realism of mis-specification,

and we recognize that in reality we must always live with “third-best”

allocations; i.e., mis-specified models that are noisily estimated.

Improved predictions derived from methods that can digest vast

information and data sets provide an opportunity to mitigate the wedges

between the pure “logic” problem of first-best resource allocation noted

by Hayek, and third-best realistic allocations achievable by economic

agents. The wedges never shrink to zero due to statistical limits to

learnability (Da et al., 2022; Didisheim et al., 2023). But powerful

approximating models and clever regularization devices mean that machine learning is economically important exactly because they can lead

to better decisions. The problem of portfolio choice is an illustrative

example. A mean-variance investor who knows the true expected return and covariance matrix of assets simply executes the “logic” of a

Markowitz portfolio and achieves a first-best allocation. But, in analogy

to Hayek, this is emphatically not the problem that real world investors

grapple with. Instead, their problem is primarily one of measurement—

one of prediction. The investor seeks a sensible expected return and

covariance estimate that, when combined with the Markowitz objective,

performs reasonably well out-of-sample. Lacking high-quality measurements, the Markowitz solution can behave disastrously, as much research

has demonstrated.

Electronic copy available at: https://ssrn.com/abstract=4501707

2

The Virtues of Complex Models

Many of us acquired our econometrics training in a tradition anchored

to the “principle of parsimony.” This is exemplified by the Box and

Jenkins (1970) model building methodology, whose influence on financial

econometrics cannot be overstated. In the introduction to the most

recent edition of the Box and Jenkins forecasting textbook,1 “parsimony”

is presented as the first of the “Basic Ideas in Model Building”: “It is

important, in practice, that we employ the smallest possible number of

parameters for adequate representations” [their emphasis].

The principle of parsimony appears to clash with the massive parameterizations adopted by modern machine learning algorithms. The

leading edge GPT-3 language model (Brown et al., 2020) uses 175 billion

parameters. Even the comparatively skimpy return prediction neural

networks in Gu et al. (2020b) have roughly 30,000 parameters. For an

econometrician of the Box-Jenkins lineage, such rich parameterizations

seem profligate, prone to overfit, and likely disastrous for out-of-sample

performance.

Recent results in various non-financial domains contradict this view.

In applications such as computer vision and natural language processing,

1

Box et al. (2015), fifth edition of the original Box and Jenkins (1970).

15

Electronic copy available at: https://ssrn.com/abstract=4501707

16

The Virtues of Complex Models

models that carry astronomical parameterizations—and that exactly

fit training data—are often the best performing models out-of-sample.

In sizing up the state of the neural network literature, Belkin (2021)

concludes “it appears that the largest technologically feasible networks

are consistently preferable for best performance.” Evidently, modern

machine learning has turned the principle of parsimony on its head.

The search is underway for a theoretical rationale to explain the success of behemoth parameterizations and answer the question succinctly

posed by Breiman (1995): “Why don’t heavily parameterized neural

networks overfit the data?” In this section we offer a glimpse into the

answer. We draw on recent advances in the statistics literature which

characterize the behavior of “overparameterized” models (those whose

parameters vastly outnumber the available training observations).2

Recent literature has taken the first step of understanding the statistical theoretical implications of machine learning models and focus

on out-of-sample prediction accuracy of overparameterized models. In

this section, we are interested in the economic implications of overparameterization and overfit in financial machine learning. A number of

finance papers have documented significant empirical gains in machine

learning return prediction. The primary economic use case of these

predictions is constructing utility-optimizing portfolios. We orient our

development toward understanding the out-of-sample risk-return tradeoff of “machine learning portfolios” derived from highly parameterized

return prediction models. Our development closely follows Kelly et al.

(2022a) and Didisheim et al. (2023).

2.1

Tools For Analyzing Machine Learning Models

Kelly et al. (2022a) propose a thought experiment. Imagine an analyst

seeking a successful return prediction model. The asset return R is

generated by a true model of the form

Rt+1 = f (Xt ) + t+1

2

(2.1)

This line of work falls under headings like “overparameterization,” “benign

overfit,” and “double descent," and includes (among others) Spigler et al. (2019),

Belkin et al. (2018), Belkin et al. (2019), Belkin et al. (2020), Bartlett et al. (2020),

Jacot et al. (2018), Hastie et al. (2019), and Allen-Zhu et al. (2019).

Electronic copy available at: https://ssrn.com/abstract=4501707

2.1. Tools For Analyzing Machine Learning Models

17

where the set of predictor variables X may be known to the analyst, but

the true prediction function f is unknown. Absent knowledge of f and

motivated by universal approximation theory (e.g., Hornik et al., 1990),

the analyst decides to approximate f with a basic neural network:

f (Xt ) ≈

P

X

Si,t βi .

i=1

Each feature in this regression is a pre-determined nonlinear transformation of raw predictors,3

Si,t = f˜(wi0 Xt ).

(2.2)

Ultimately, the analyst estimates the approximating regression

Rt+1 =

P

X

Si,t βi + ˜t+1 .

(2.3)

i=1

The analyst has T training observations to learn from and must choose

how rich of an approximating model to use—she must choose P . Simple

models with small P enjoy low variance, but complex models with large

P (perhaps even P > T ) can better approximate the truth. What level

of model complexity (which P ) should the analyst opt for?

Perhaps surprisingly, Kelly et al. (2022a) show that the analyst

should use the largest approximating model that she can compute!

Expected out-of-sample forecasting and portfolio performance are increasing in model complexity.4 To arrive at this answer, Kelly et al.

(2022a) work with two key mathematical tools for analyzing complex

nonlinear (i.e., machine learning) models. These are ridge regression

with generated nonlinear features (just like Si,t above) and random

matrix theory for dealing with estimator behavior when P is large

relative to the number of training data observations.

3

Our assumption that weights wi and nonlinear function f˜ are known follows

Rahimi and Recht (2007), who prove that universal approximation results apply

even when the weights are randomly generated.

4

This is true without qualification in the high complexity regime (P > T ) and is

true in the low complexity regime as long as appropriate shrinkage is employed. Kelly

et al. (2022a) derive the choice of shrinkage that maximizes expected out-of-sample

model performance.

Electronic copy available at: https://ssrn.com/abstract=4501707

18

The Virtues of Complex Models

2.1.1

Ridge Regression with Generated Features

Their first modeling assumption5 focuses on high-dimensional linear

prediction models according to (2.3), which we refer to as the “empirical

model.” The interpretation of (2.3) is not that asset returns are subject

to a large number of linear fundamental driving forces. It is instead

that the DGP is unknown, but may be approximated by a nonlinear

expansion S of some (potentially small) underlying driving variables,

X.6 In the language of machine learning, S are “generated features”

derived from the raw features X, for example via nonlinear neural

network propagation.

A definitive aspect of this problem is that the empirical model is

mis-specified. Correct specification of (2.3) requires an infinite series

expansion, but in reality we are stuck with a finite number of terms, P .

Small P models are stable because there are few parameters to estimate

(low variance), but provide a poor approximation to the truth (large

bias). A foundational premise of machine learning is that flexible (large

P ) model specifications can be leveraged to improve prediction. Their

estimates may be noisy (high variance) but provide a more accurate

approximation (small bias). It is not obvious, ex ante, which choices

of P are best in terms of the bias-variance tradeoff. As economists, we

ultimately seek a bias-variance tradeoff that translates into optimal

economic outcomes—like higher utility for investors. The search for

models that achieve economic optimality guides Kelly et al. (2022a)’s

theoretical pursuit of high complexity models.

The second modeling assumption chooses the estimator of (2.3) to

be ridge-regularized least squares:

!−1

b

β(z)

=

zI + T

−1

X

t

St St0

1X

St Rt+1 ,

T t

5

(2.4)

We introduce assumptions here at a high level. We refer interested readers to

Kelly et al. (2022a) for detailed technical assumptions.

6

As suggested by the derivation of (2.3) from equation (2.1), this sacrifices little

generality as a number of recent papers have established an equivalence between

high-dimensional linear models and more sophisticated models such as deep neural

networks (Jacot et al., 2018; Hastie et al., 2019; Allen-Zhu et al., 2019). For simplicity,

Kelly et al. (2022a) focus on time-series forecasts for a single risky asset (extended

to multi-asset panels by Didisheim et al. (2023)).

Electronic copy available at: https://ssrn.com/abstract=4501707

2.1. Tools For Analyzing Machine Learning Models

19

where z is the ridge shrinkage parameter. Not all details of this estimator

are central to our arguments—but regularization is critical. Without

regularization the denominator of (2.4) is singular in the high complexity

regime (P > T ), though we will see it also has important implications

b

for the behavior of β(z)

in low complexity models (P < T ).

Finally, to characterize the economic consequences of high complexity

models for investors, Kelly et al. (2022a) assume that investors use

predictions to construct a trading strategy defined as

π

Rt+1

= πt Rt+1 ,

where πt is a timing weight that scales the risky asset position up and

down in proportion to the model’s return forecast. For their analysis,

πt is set equal to the expected out-of-sample return from their complex

prediction model. And they assume investor well-being is measured in

terms of the unconditional Sharpe ratio,

SR = q

π ]

E[Rt+1

π )2 ]

E[(Rt+1

.

(2.5)

While there are other reasonable trading strategies and performance

evaluation criteria, these are common choices among academics and

practitioners and have the benefit of transparency and tractability.

2.1.2

Random Matrix Theory

The ridge regression formulation above couches machine learning models

like neural networks in terms of linear regression. The hope is that,

with this representation, it may be possible to say something concrete

about expected out-of-sample behaviors of complicated models in the

P → ∞ limit with P/T → c > 0. The necessary asymptotics for

machine learning are different than those for standard econometric

characterizations (which use asymptotic approximations for T → ∞

with P fixed). Random matrix theory is ideally suited for describing the

behavior of ridge regression in the large P setting. To simplify notation,

we eliminate T from the discussion by always referring to the degree of

model parameterization relative to the amount of training data. That

is, we will simply track the ratio c = P/T , which we refer to as “model

complexity.”

Electronic copy available at: https://ssrn.com/abstract=4501707

20

The Virtues of Complex Models

b

The crux of characterizing β(z)

behavior when P → ∞ is the P × P

b := T −1 P St S 0 . Random matrix

sample covariance matrix of signals, Ψ

t

t

b eigenvalues. Knowledge

theory describes the limiting distribution of Ψ’s

of this distribution is sufficient to pin down the expected out-of-sample

prediction performance (R2 ) of ridge regression, as well as the expected

out-of-sample Sharpe ratio of the associated timing strategy. More

specifically, these quantities are determined by

1

b − zI)−1

m(z; c) := lim

(2.6)

tr (Ψ

P →∞ P

which is the limiting Stieltjes transform of the eigenvalue distribution of

b From (2.6), we recognize a close link to ridge regression because the

Ψ.

b − zI)−1 . The functional

Stieltjes transform involves the ridge matrix (Ψ

form of m(z; c) is known from a generalized version of the MarcenkoPastur law. From m(z; c) we can explicitly calculate the expected out-ofsample R2 and Sharpe ratio and its sensitivity to the prediction model’s

complexity (see Sections 3 and 4 of Kelly et al. (2022a) for a detailed

elaboration of this point).

In other words, model complexity plays a critical role in understanding model behavior. If T grows at a faster rate than the number of

predictors (i.e., c → 0), traditional large T and fixed P asymptotics kick

in. In this case the expected out-of-sample behavior of a model coincides

with the behavior estimated in-sample. Naturally, this is an unlikely and

fairly uninteresting scenario. The interesting case corresponds to highly

parameterized machine learning models with scarce data, P/T → c > 0,

and it is here that surprising out-of-sample model behaviors emerge.

2.2

Bigger Is Often Better

Kelly et al. (2022a) provide rigorous theoretical statements about the

properties of high complexity machine learning models and associated

trading strategies. Our current exposition focuses on the main qualitative

aspects of those results based on their calibration to the market return

prediction problem. In particular, they assume total return volatility

equal to 20% per year and an infeasible “true” predictive R2 of 20% per

month (if the true functional form and all signals were fully available

to the forecaster). Complexity hinders the model’s ability to hone in

Electronic copy available at: https://ssrn.com/abstract=4501707

2.2. Bigger Is Often Better

21

R2

b

kβk

0.3

6.00

0.2

5.00

0.1

4.00

0.0

3.00

-0.1

2.00

-0.2

1.00

-0.3

0.00

0

2

4

6

8

10

0

2

4

6

8

10

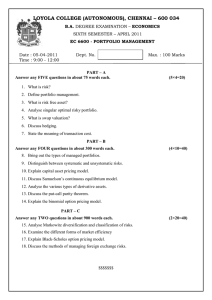

Figure 2.1: Expected Out-of-sample Prediction Accuracy From Mis-specified Models

Note: Limiting out-of-sample R2 and βb norm of ridge regression as a function of

c and z from Proposition 5 of Kelly et al. (2022a). Calibration assumes Ψ is the

identity matrix, b∗ = 0.2, and the complexity of the true model is 10.

on the true DGP because there is not enough data to support the

model’s heavy parameterization, thus the best feasible R2 implied by

this calibration is closer to 1% per month. We focus on the mis-specified

setting by considering empirical models that use various subsets of the

true predictors.7

In this calibration, the true unknown DGP is assumed to have a

complexity of c = 10. The parameter q ∈ [0, 1] governs the complexity

of the empirical model relative to the truth. We analyze the behavior

of approximating empirical models that range in complexity from very

simple (q ≈ 0, cq ≈ 0 and thus severely mis-specified) to highly complex

(q = 1, cq = 10 corresponds to the richest approximating model and in

fact recovers the correct specification). Models with very low complexity

are poor approximating models but their parameters can be estimated

with precision. As cq rises, the empirical model better approximates the

truth, but forecast variance rises (if not regularized). The calibration

also considers a range of ridge penalties, z.

b

First consider the ordinary least squares (OLS) estimator, β(0),

which is a special case of (2.4) with z = 0. When c ≈ 0 the model is

7

For simplicity the predictors are assumed to be exchangeable, so only the size

of a subset matters and not the identity of the specific predictors within the subset.

Electronic copy available at: https://ssrn.com/abstract=4501707

22

The Virtues of Complex Models

very simple, so it has no power to approximate the truth and delivers

an R2 of essentially zero. As P rises and approaches T from below,

the model’s approximation improves, but the denominator of the least

squares estimator blows up, creating explosive forecast error variance.

This phenomenon is illustrated in Figure 2.1. When P = T , the model

exactly fits, or “interpolates,” the training data (for this reason, c = 1

is called the “interpolation boundary”), so a common interpretation of

b

the explosive behavior of β(0)

is severe overfit that does not generalize

out-of-sample.

As P moves beyond T we enter the overparameterized, or high

complexity, regime. In this regime, there are more parameters than

observations, the least squares problem has multiple solutions, and

the inverse covariance matrix of regressors is not defined. However, its

pseudo-inverse is defined, and this corresponds to a particular unique

+ P

P

solution to the least squares problem: T −1 t St St0 T1 t St Rt+1 .8

Among the many solutions that exactly fit the training data, this one

has the smallest `2 norm. In fact, it is equivalent to the ridge estimator

as the shrinkage parameter approaches zero:

!−1

+

b

β(0

) = lim

z→0+

zI + T

−1

X

t

St St0

1X

St Rt+1 .

T t

b + ) is called the “ridgeless” regression estimator (the

The solution β(0

blue line in the Figure 2.1). When c ≤ 1, OLS is the ridgeless estimator,

while for c > 1 the ridgeless case is defined by the limit z → 0.

Surprisingly, the ridgeless R2 rises as model complexity increases

above 1. The reason is that, as c becomes larger, there is a larger space of

solutions for ridgeless regression to search over and thus it can find betas

with smaller `2 norm that still interpolate the training data. This acts as

a form of shrinkage, biasing the beta estimate toward zero. Due to this

bias, the forecast variance drops and the R2 improves. In other words,

despite z → 0, the ridgeless solution still regularizes the least squares

estimator, and more so the larger is c. By the time c is very large, the

expected out-of-sample R2 moves into positive territory. This property

8

Recall that the Moore-Penrose pseudo-inverse A+ of a matrix A is defined via

A = (A0 A)−1 A0 if A0 A is invertible, and A+ = A0 (AA0 )−1 if AA0 is invertible.

+

Electronic copy available at: https://ssrn.com/abstract=4501707

2.2. Bigger Is Often Better

23

of ridgeless least squares is a newly documented phenomenon in the

statistics literature and is still an emerging topic of research.9 The result

challenges the standard financial economics doctrine that places heavy

emphasis on model parsimony, demonstrating that one can improve

the accuracy of return forecasts by pushing model dimensionality well

beyond sample size.10

Figure 2.1 describes the statistical behavior of high complexity

models. Figure 2.2 turns attention to their economic consequences. The

right panel shows volatility of the machine learning trading strategy as

a function of model complexity. The strategy’s volatility moves one for

one with the norm of βb and with the R2 (all three quantities are different

representations of forecast error variance). The important point is that,

as model complexity increases past c = 1, trading strategy volatility

continually decreases. Complexity raises the implicit shrinkage of the

ridgeless estimator, which reduces return volatility (and z > 0 reduces

volatility even further).

The left panel of Figure 2.2 shows the key economic behavior of high

complexity models—the out-of-sample expected return of the timing

strategy. Expected returns are low for simple strategies. Again, this is

because simple models give a poor approximation of the DGP. Increasing model complexity gets you closer to the truth and monotonically

increases trading strategy expected returns.11

What does this mean for investor well-being? The bottom panel

in Figure 2.2 shows utility in terms of expected out-of-sample Sharpe

ratio.12 Out-of-sample Sharpe ratios boil down to a classic bias-variance

tradeoff. Expected returns purely capture bias effects. For low complexity

9

See Spigler et al. (2019), Belkin et al. (2018), Belkin et al. (2019), Belkin et al.

(2020), and Hastie et al. (2019).

10

The remaining curves in Figure 2.1 show how the out-of-sample R2 is affected

by non-trivial ridge shrinkage. The basic R2 patterns are the same as the ridgeless

case, but allowing z > 0 can improve R2 further.

11

In the ridgeless case, the benefit of added complexity reaches its maximum

when c = 1. The ridgeless expected return is flat for c ≥ 1 because the incremental

improvements in DGP approximation are exactly offset by the gradually rising bias

of ridgeless shrinkage.

12

In the calibration, the buy-and-hold trading strategy is normalized to have a

Sharpe ratio of zero. Thus, the Sharpe ratio in Figure 2.2 is in fact the Sharpe ratio

gain from timing based on model forecasts, relative to a buy-and hold investor.

Electronic copy available at: https://ssrn.com/abstract=4501707

24

The Virtues of Complex Models

Expected Return

Volatility

6.00

0.02

5.00

4.00

3.00

0.01

2.00

1.00

0.00

0.00

0

2

4

6

8

10

0

2

4

6

8

10

Sharpe Ratio

0.06

0.05

0.04

0.03

0.02

0.01

0.00

0

2

4

6

8

10

Figure 2.2: Expected Out-of-sample Risk-Return Tradeoff of Timing Strategy

Note: Limiting out-of-sample expected return, volatility, and Sharpe ratio of the

timing strategy as a function of cq and z from Proposition 5 of Kelly et al. (2022a).

Calibration assumes Ψ is the identity matrix, b∗ = 0.2, and the complexity of the

true model is c = 10.

models, bias comes through model misspecification but not through

shrinkage. For high complexity models, the mis-specification bias is

small, but the shrinkage bias becomes large. The theory, which shows

that expected returns rise with complexity, reveals that misspecification

bias is more costly than shrinkage bias when it comes to expected

returns. Meanwhile, the strategy’s volatility is purely about forecast

variance effects. Both simple models (c ≈ 0) or highly complex models

Electronic copy available at: https://ssrn.com/abstract=4501707

2.2. Bigger Is Often Better

25

(c 1) produce low variance. Given these patterns in the bias-variance

tradeoff, it follows that the out-of-sample Sharpe ratio is also increasing

in complexity, as shown in Figure 2.2.

It is interesting to compare these findings with the phenomenon

of “double descent,” or the fact that out-of-sample M SE has a nonmonotonic pattern in model complexity when z is close to zero (Belkin

et al., 2018; Hastie et al., 2019). The mirror image of double descent

in M SE is “double ascent” of the ridgeless Sharpe ratio. Kelly et al.

(2022a) prove that the ridgeless Sharpe ratio dip at c = 1 is an artifact

of insufficient shrinkage. With the right amount of shrinkage (explicitly

characterized by Kelly et al. (2022a)), complexity becomes a virtue even

in the low complexity regime: the hump disappears, and “double ascent”

turns into “permanent ascent.”

In summary, these results challenge the dogma of parsimony discussed at the start of this section. They demonstrate that, in the realistic

case of mis-specified empirical models, complexity is a virtue. This is

true not just in terms of out-of-sample statistical performance (as shown

by Belkin et al., 2019; Hastie et al., 2019, and others) but also in the

economic terms of out-of-sample investor utility. Contrary to conventional wisdom, the performance of machine learning portfolios can be

theoretically improved by pushing model parameterization far beyond

the number of training observations.

Kelly et al. (2022a) conclude with a recommendation for best practices in the use of complex models:

“Our results are not a license to add arbitrary predictors

to a model. Instead, we encourage i) including all plausibly

relevant predictors and ii) using rich nonlinear models rather

than simple linear specifications. Doing so confers prediction

and portfolio benefits, even when training data is scarce, and

particularly when accompanied by prudent shrinkage.”

To derive the results above, Kelly et al. (2022a) impose an assumption that predictability is uniformly distributed across the signals. At

first glance, this may seem overly restrictive, as many standard predictors would not satisfy this assumption. However, the assumption is

consistent with (and is indeed motivated by) standard neural network

Electronic copy available at: https://ssrn.com/abstract=4501707

26

The Virtues of Complex Models

models in which raw features are mixed and nonlinearly propagated

into final generated features, as in equation (2.2). The ordering of the

generated features S is essentially randomized by the initialization step

of network training. Furthermore, in their empirical work, Kelly et al.

(2022a), Kelly et al., 2022b, and Didisheim et al. (2023) use a neural

network formulation known as random feature regression that ensures

this assumption is satisfied.

2.3

The Complexity Wedge

Didisheim et al. (2023) extend the analysis of Kelly et al. (2022a) in a

number of ways and introduce the “complexity wedge,” defined as the

expected difference between in-sample and out-of-sample performance.

For simplicity, consider a correctly specified empirical model. In a

low complexity environment with c ≈ 0, the law of large numbers

applies, and as a result in-sample estimates converge to the true model.

Because of this convergence, the model’s in-sample performance is

exactly indicative of its expected out-of-sample performance. That is,

with no complexity, there is no wedge between in-sample and out-ofsample behavior.

But when c > 0, a complexity wedge emerges, consisting of two components. Complexity inflates the trained model’s in-sample predictability

relative to the true model’s predictability—this is the traditional definition of overfit and it is the first wedge component. But high complexity

also means that the empirical model does not have enough data (relative

to its parameterization) to recover the true model—this is a failure of

the law of large numbers due to complexity. This gives rise to the second

wedge component, which is a shortfall in out-of-sample performance

relative to the true model. This shortfall can be thought of as the “limits

to learning” due to model complexity. The complexity wedge—the expected difference between in-sample and out-of-sample performance—is

the sum of overfit and limits to learning.

The complexity wedge has a number of intriguing implications for

asset pricing. Given a realized (feasible) prediction R2 , one can use

random matrix theory to back out the extent of predictability in the

“true” (but infeasible) model. A number of studies have documented

Electronic copy available at: https://ssrn.com/abstract=4501707

2.3. The Complexity Wedge

27

significantly positive out-of-sample return prediction using machine

learning models, on the order of roughly 1% per month for individual

stocks. This fact, combined with a theoretical derivation for the limits

to learning, suggest that the true infeasible predictive R2 must be

much higher. Relatedly, even if there are arbitrage (or simply very high

Sharpe ratio) opportunities implied by the true model, limits to learning

make these inaccessible to real-world investors. In a realistic empirical

setting, Didisheim et al. (2023) suggest that attainable Sharpe ratios

are attenuated by roughly an order of magnitude relative to the true

data-generating process due to the infeasibility of accurately estimating

complex statistical relationships.

Da et al. (2022) consider a distinct economic environment in which

agents, namely arbitrageurs, adopt statistical arbitrage strategies in

efforts to maximize their out-of-sample Sharpe ratio. These arbitrageurs

also confront statistical obstacles (like “complexity” here) in learning

the DGP of alphas. Da et al. (2022) show that regardless of the machine

learning methods arbitrageurs use, they cannot realize the optimal

infeasible Sharpe ratio in certain low signal-to-noise ratio environments.

Moreover, even if arbitrageurs adopt an optimal feasible trading strategy,

there remains a substantial wedge between their Sharpe ratio and the

optimal infeasible one. We discuss more details of each of these papers

in Chapter 4.6.

Electronic copy available at: https://ssrn.com/abstract=4501707

3

Return Prediction

Empirical asset pricing is about measuring asset risk premia. This

measurement comes in two forms: one seeking to describe and understand differences in risk premia across assets, the other focusing on

time series dynamics of risk premia. As the first moment of returns,

it is a natural starting point for surveying the empirical literature of

financial machine learning. The first moment at once summarizes i) the

extent of discounting that investors settle on as fair compensation for

holding risky assets (potentially distorted by frictions that introduce an

element of mispricing), and ii) the first-order aspect of the investment

opportunities available to a prospective investor.

A return prediction is, by definition, a measurement of an asset’s

conditional expected excess return:1

Ri,t+1 = Et [Ri,t+1 ] + i,t+1 ,

(3.1)

Related to equation (1.2), Et [Ri,t+1 ] = E[Ri,t+1 |It ] represents a forecast

conditional on the information set It , and i,t+1 , collects all the remaining unpredictable variation in returns. When building statistical models

of market data, it is worthwhile to step back and recognize that the

1

Ri,t+1 is an asset’s return in excess of the risk-free rate with assets indexed by

i = 1, ..., Nt and dates by t = 1, ..., T .

28

Electronic copy available at: https://ssrn.com/abstract=4501707

29

data is generated from an extraordinarily complicated process. A large

number of investors who vary widely in their preferences and individual

information sets interact and exchange securities to maximize their wellbeing. The traders intermittently settle on prices, and the sequence of

price changes (and occasional cash flows such as stock dividends or bond

coupons) produce a sequence of returns. The information set implied

by the conditional expectation in (3.1) reflects all information—public,

private, obvious, subtle, unambiguous, or dubious—that in some way

influences prices decided at time t. We emphasize the complicated genesis of this conditional expectation because we next make the quantum

leap of defining a concrete function to describe its behavior:

Et [Ri,t+1 ] = g ? (zi,t ).

(3.2)

Our objective is to represent Et [Ri,t+1 ] as an immutable but otherwise

general function g ? of the P -dimensional predictor variables zi,t available

to we the researchers. That is, we hope to isolate a function that, once

we condition on zi,t , fully explains the heterogeneity in expected returns

across all assets and over all time, as g ? depends neither on i nor t.2

By maintaining the same form over time and across assets, estimation

can leverage information from the entire panel, which lends stability

to estimates of expected returns for any individual asset. This is in

contrast to some standard asset pricing approaches that re-estimate a

cross-sectional model each time period, or that independently estimate

time series models for each asset (see Giglio et al., 2022a). In light

of the complicated trading process that generates return data, this

“universality” assumption is ambitious. First, it is difficult to imagine

that researchers can condition on the same information set as market

participants (the classic Hansen-Richard critique). Second, given the

constantly evolving technological and cultural landscape surrounding

markets, not to mention the human whims that can influence prices, the

concept of a universal g ? (·) seems far-fetched. So, while some economists

might view this framework as excessively flexible (given that it allows

for an arbitrary function and predictor set), it seems that (3.2) places

2

Also, g ? (·) depends on z only through zi,t . In most of our analysis, predictions

will not use information from the history prior to t, or from individual stocks other

than the ith , though this is generalized in some analyses that we reference later.

Electronic copy available at: https://ssrn.com/abstract=4501707

30

Return Prediction

onerous restrictions on the model of expected returns. For those that

view it as implausibly restrictive, then any ability of this framework

to robustly describe various behaviors of asset returns—across assets,

time, and particular on an out-of-sample basis—can be viewed as an

improbable success.

Equations (3.1) and (3.2) offer an organizing template for the machine learning literature on return prediction. This section is organized

by the functional form g(zi,t ) used in each paper to approximate the true

prediction function g ? (zi,t ) in our template. We emphasize the main

empirical findings of each paper, and highlight new methodological

contributions and distinguishing empirical results of individual papers.

We avoid discussing detailed differences in conditioning variables in

different papers, but the reader should be aware that these variations

are also responsible for variation in empirical results (above and beyond

differences in functional form).

There are two distinct strands of literature associated with the

time series and cross section research agendas discussed above. The

literature on time series machine learning models for aggregate assets

(e.g., equity or bond index portfolios) developed earlier but is the smaller

literature. Efforts in time series return prediction took off in the 1980’s

following Shiller (1981)’s documentation of the excess volatility puzzle.

As researchers set out to quantify the extent of excess volatility in

markets, there emerged an econometric pursuit of time-varying discount

rates through predictive regression. Development of the time series

prediction literature occurred earlier than the cross section literature

due to the earlier availability of data on aggregate portfolio returns and

due to the comparative simplicity of forecasting a single time series. The

small size of the market return data set is also a reason for the limited

machine learning analysis of this data. With so few observations (several

hundred monthly returns), after a few research attempts one exhausts

the plausibility that “out-of-sample” inferences are truly out-of-sample.

The literature on machine learning methods for predicting returns in

panels of many individual assets is newer, much larger, and continues to

grow. It falls under the rubric of “the cross section of returns” because

early studies of single name stocks sought to explain differences in

unconditional average returns across stocks—i.e., the data boiled down

Electronic copy available at: https://ssrn.com/abstract=4501707

3.1. Data

31

a single cross section of average returns. In its modern incarnation,

however, the so-called “cross section” research program takes the form

of a true panel prediction problem. The objective is to explain both timevariation and cross-sectional differences in conditional expected returns.

A key reason for the rapid and continual expansion of this literature is

the richness of the data. The panel’s cross-section dimension can multiply

the number of time series observations by a factor of a few thousand or

more (in the case of single name stocks, bonds, or options, for example).

While there is notable cross-correlation in these observations, most of

the variation in single name asset returns is idiosyncratic. Furthermore,

patterns in returns appear to be highly heterogeneous. In other words,

the panel aspect of the problem introduces a wealth of phenomena for

empirical researchers to explore, document, and attempt to understand

in an economic frame.

We have chosen an organizational scheme for this section that

categorizes the literature by machine learning methods employed, and

in each section we discuss both time series and panel applications. Given

the prevalence of cross section studies, this topic receives the bulk of

our attention.

3.1

Data

Much of the financial machine learning literature studies a canonical

data set consisting of monthly returns of US stocks and accompanying

stock-level signals constructed primarily from CRSP-Compustat data.

Until recently, there were few standardized choices for building this

stock-month panel. Different researchers use different sets of stock-level

predictors (e.g., Lewellen (2015) uses 15 signals, Freyberger et al. (2020)

use 36, Gu et al. (2020b) use 94) and impose different observation filters

(e.g., excluding observations stocks with nominal share prices below

$5, excluding certain industries like financials or utilities, and so forth).

And it is common for different papers to use different constructions

for signals with the same name and economic rationale (e.g., various

formulations of “value,” “quality,” and so forth).

Fortunately, recent research has made progress streamlining these

data decisions by publicly releasing data and code for a standardized

Electronic copy available at: https://ssrn.com/abstract=4501707

32

Return Prediction

stock-level panel, available directly from the Wharton Research Data Services server. Jensen et al. (2021) construct 153 stock signals, and provide

source code and documentation so that users can easily inspect, analyze,

and modify empirical choices. Furthermore, their data is available not

just for US stocks, but for stocks in 93 countries around the world, and

is updated regularly to reflect annual CRSP-Compustat data releases.

These resources may be accessed at jkpfactors.com. Jensen et al. (2021)

emphasize a homogenous approach to signal construction by attempting

to make consistent decisions in how different CRSP-Compustat data

items are used in various signals. Chen and Zimmermann (2021) also

post code and data for US stocks at openassetpricing.com.

In terms of standardized data for aggregate market return prediction,

Welch and Goyal (2008) post updated monthly and quarterly returns

and predictor variables for the aggregate US stock market.3 Rapach and

Zhou (2022) provide the latest review of additional market predictors.

3.2

Experimental Design

The process of estimating and selecting among many models is central

to the machine learning definition given above. Naturally, selecting a

best performing model according to in-sample (or training sample) fit

exaggerates model performance since increasing model parameterization

mechanically improves in-sample fit. Sufficiently large models will fit

the training data exactly. Once model selection becomes part of the