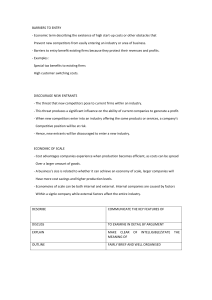

Market Structures ECON110-Principles of Economics REVIEW: REVENUES, PROFIT § In general, total revenue is price x output (Q) 𝑇𝑅 = 𝑃𝑄 § Total profit (Π ) is equal to total revenue minus total cost. Π=TR−TC § Like costs, profit and revenue can be expressed in average (per output) units. Average profit (AP) is average revenue minus average costs, or equivalently: Π 𝑇𝑅 𝑇𝐶 𝐴𝑃 = = − 𝑄 𝑄 𝑄 § Since 𝑇𝑅 = 𝑃𝑄,it follows that 𝑨𝑷 = 𝑷 − 𝑨𝑪 Therefore, AP, and total profits stays positive, as long as P > AC. PROFIT MAXIMIZATION: WHY MR = MC? Perfect Competition case: • Discussion: https://www.youtube.com/watch?v=w0H bGX0KFFM&t=325s&ab_channel=JacobCli fford • Lecture: https://www.youtube.com/watch?v=BQvt njWZ0ig&ab_channel=JacobClifford General case (optional but with calculus) • See Canvas or classroom board notes Market Structure: Porter’s Five Forces 1. Competition Rivalry 2. Threat of New Entrants 3. Threat of Substitutes 4. Power of Suppliers 5. Power of Buyers 4 I. Competition • Let’s contrast two extreme forms of market competition: 1. Perfect Competition 2. Monopoly 5 Perfect Competition In general, such competitive firms sell homogeneous products and are price takers. • If you have prices t h at differ too much from competitors, you lose if yours is too high (obviously). • In addition, since firms are price-takers, P =MR. (any further increase in output has the same price) Therefore, P =AR =MR. • Since MR = MC under profit maximization, competitive firms will attempt to charge P=MC. • If there is initially a different P, other firms will act depending on available incentives and restore P=MC accordingly (think about shifts in the market supply curve) 6 Perfect Competition: Shutdown and Exit Condition • What if prices are too low? • Recall: In the long run, there are no fixed costs. • Firms earn profits if TR > TC or P > AC • On the other hand, if P cannot even cover AC, firms exit the market. • In the short run, firms need to worry about variable costs (fixed costs are a given an d cannot be recovered). • Firms may shutdown temporarily if TR < VC or P < AVC. But they still pay fixed costs (i.e. stay in the market, but produce Q = 0) 7 Perfect Competition: Profits • Zero economic profit in the long-run. Recall: Profits are positive if P > AC • Positive economic profits attract other firms to enter, which will reduce prices until this condition holds. In the long run, P=MC=AC Zero economic profit applies if • 𝑻𝒐𝒕𝒂𝒍 𝑹𝒆𝒗𝒆𝒏𝒖𝒆(𝑻𝑹) = 𝑻𝒐𝒕𝒂𝒍 𝑪𝒐𝒔𝒕 • 𝑻𝑹 = 𝑬𝒙𝒑𝒍𝒊𝒄𝒊𝒕𝑪𝒐𝒔𝒕 + 𝑰𝒎𝒑𝒍𝒊𝒄𝒊𝒕𝑪𝒐𝒔𝒕 But accounting profit may remain positive if • 𝑻𝒐𝒕𝒂𝒍 𝑹𝒆𝒗𝒆𝒏𝒖𝒆 > 𝑻𝒐𝒕𝒂𝒍 𝑬𝒙𝒑𝒍𝒊𝒄𝒊𝒕 𝑪𝒐𝒔𝒕 Therefore, under competitive markets, firms earn enough accounting profits to compensate for the time and money invested to keep the business going. No more, no less. 6 Monopoly: Excess Market Power § One seller, multiple buyers. § Price Maker: I t can m a ke ou tp u t decisions on its own, a n d it follows t h a t it can influence t h e price on its own. § (Probably t he most famous § cartoon example: Krusty Krab) § As a n alternative, government may opt to regulate price a n d ou tp u t decisions of monopolies. § A monopolist has no supply curve since it is powerful enough to choose a specific point 9 II. Threat of New Entrants • Perfect Competition • No barriers to entry, incentive to e a r n until long r u n zero economic profit condition achieved • Free entry or exit depending on how P compares with AC • Monopoly Strong Barriers to Entry Natural barriers (e.g. economies of scale) Small firms will find it very costly to compete Legal barriers • Oligopoly • ”In between case” – involves a few players selling homogeneous products 10 III. Threat of Substitutes • More substitutes decreases profitability of an industry. The more substitutes, the more ”competitors” and the more pressure not to increase prices. Recall: If the price of substitutes go down, quantity demanded goes down. Also consider: cross-price elasticity of demand. • Branding and product differentiation may also play a role in the industry. • Monopolistic Competition: Multiple sellers, but some monopoly power present due to product differentiation 11 IV. Suppliers • If suppliers have market power, they can bring down the profitability of an industry. Shift costs downwards (from the supplier industry to the incumbent industry). • Example: The profitability of airlines gets affected by the nature of aircraft manufacturing (BoeingAirbus duopoly) 12 V. Buyers • We can say more about buyers in consumer theory a n d marketing , b u t in general, buyers m ay also affect t h e n a t u r e of a n industry. • Some consumers a re more price sensitive (consider: elasticity of demand) • Some capture more value t h a n others • Example 1: by social class? • Example 2: Sports a p p a re l i n d u str y = depends on sports fans • A n o t h e r ca s e : I n l a b o r m a r ke t s , f i r m s a re b u ye rs ( t h i n k a b o u t t h e i r m a r ke t p o w e r i n s o m e c a s e s / i n d u s t r i e s ) 13 Porter’s Five Forces: Example (Airlines) 1. Competition Rivalry Oligopoly 2. Threat of New Entrants Easier to enter when LCC’s became popular 3. Power of Suppliers Aircraft manufacturers = duopoly, government / airport rules 4. Power of Buyers Business vs. Leisure Travelers Branding, Marketing 5. Threat of Substitutes Road trips? Boats? Video conference instead of travels. 14