Accounting Cycle & Account Classification Instructor's Manual

advertisement

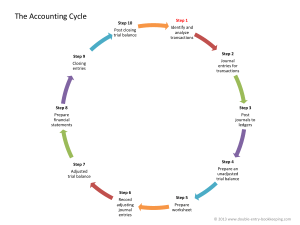

Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce CHAPTER 4: COMPLETING THE ACCOUNTING CYCLE AND CLASSIFYING ACCOUNTS Learning Objectives Closing Process (LO1) The Closing Process is an important step at end of accounting period to prepare for the next period. In the closing process we must: Identify accounts for closing. Record and post closing entries. Prepare a post-closing trial balance. After closing, effects on accounts are as follows: 1. Revenue, expense and withdrawals accounts will be reflected in equity and will begin the new period with a zero balance. 2. Owner’s equity account will reflect increases from profit and decreases from loss and withdrawals. Temporary and Permanent Accounts 3. Temporary (or nominal) accounts accumulate data related to one accounting period. (All income statement accounts, withdrawals accounts, and the Income Summary.) 4. Permanent (or real) accounts report on activities related to one or more future accounting periods. (All balance sheet accounts.) The closing process applies only to temporary accounts. Recording and Posting Closing Entries (LO2) Copyright © 2022 McGraw Hill 4-1 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce (Refer to Exhibit 4.2) Use a new temporary account called Income Summary. The four closing entries are: 1. Close credit balances in revenue accounts. (By debiting the accounts and crediting Income Summary) 2. Close debit balances in expense accounts. (By crediting the accounts and debiting Income Summary) 3. Close the Income Summary account to owner's capital account. 4. Note: Income Summary, prior to closing, will have a credit balance equal to profit or a debit balance equal to loss. Therefore, this entry will credit capital for the profit or debit capital for a loss. 5. Close withdrawals account to owner’s capital. (By crediting the account and debiting the owner’s capital account) After all closing entries are posted, all temporary accounts have a zero balance, and the capital account reflects the company’s period to date balance. Preparing a Post-Closing Trial Balance (LO3) Prepared after closing entries are journalized and posted. Verifies that total debits equal total credits for permanent accounts, and all temporary accounts have zero balances. Students should note that post-closing trial balance is usually very short. Copyright © 2022 McGraw Hill 4-2 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce Completing the Accounting Cycle (LO4) The sequence of accounting procedures followed each accounting period: 1. Analyze Transactions 2. Journalize 3. Post 4. Unadjusted trial balance 5. Adjust 6. Adjusted trial balance 7. Prepare statements 8. Close 9. Post closing trial balance Classified Balance Sheet (LO5) The Classified Balance Sheet is commonly used classifications and contains: A. Current assets—cash or other assets that are reasonably expected to be sold, collected, or consumed within one year or within the normal operating cycle of the business, whichever is longer. Examples are cash, short term investments, accounts receivable, notes receivable, merchandise inventory, prepaid expenses- reported in order of liquidity. Prepaid expenses are sometimes combined on a balance sheet. B. Non-current Investments—long term assets such as stocks, bonds, promissory notes, and land held for future expansion. C. Property, Plant and Equipment- tangible assets that are used for more than one accounting period to produce or sell goods and services. Examples include equipment, buildings, land. D. Intangible assets—long term resources used to produce or sell products and services; they do not have a physical form; their benefits are uncertain. Value comes from the privileges or rights that are granted to or held by the owner. Examples include patents, trademarks, franchises and copyrights. E. Current liabilities—obligations due to be paid or liquidated within one year or the operating cycle, whichever is longer. Examples include accounts payable, wages payable, taxes payable, interest payable, unearned revenues, current portions of long term liabilities. F. Non-current liabilities—obligations that are due to be paid beyond the longer of one year or the operating cycle of the business. Examples include notes payable, bonds payable, mortgages payable. G. Equity—presentation of the owner’s claim on the business. Equity section for sole proprietorship shows one owner’s capital account. Partnerships and corporations are discussed in detail in later chapters. Copyright © 2022 McGraw Hill 4-3 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce Financial Statement Analysis (LO6) Focus should be on the calculations and how these ratios are used within a company and for measurement against industry. Current Ratio: The current ratio is one important measure used to evaluate a company’s ability to pay its short-term obligations. The ability to pay day-to-day obligations (current liabilities) with existing liquid assets is commonly referred to as liquidity. Quick Ratio: The quick ratio is a simple modification from the current ratio, and is a more robust measure of liquidity. Debt to Equity Ratio: The debt-to-equity ratio (Exhibit 4.19) is another calculation that is important for understanding financial statements as it indicates the risk position of a company. Work Sheet as a Tool (LO7) Useful to organize accounting information. (Not a financial statement) A. Some benefits include reduces errors, captures linked accounting information, helps organize an audit, and plans interim financial statements and useful for “what if” analysis and planning purposes. B. Steps to prepare a work sheet: (Refer to Exhibit 4A.1 for the format and steps) 1. Enter the unadjusted trial balance in the first two columns. 2. Enter the adjustments in the third and fourth columns. Total columns to verify debit adjustments equal credit adjustments. 3. Prepare the adjusted trial balance. Total Adjusted Trial Balance columns to verify debits equal credits. 4. Extend the adjusted trial balance amounts to the financial statement columns. 5. Enter profit (or loss) and balance the financial statement columns. Prepare financial statements from worksheet information. Copyright © 2022 McGraw Hill 4-4 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce It is helpful to know what to are look for in completing the final 4 columns. You should only be “filling in” the 2 inside columns for a loss and the 2 outside columns for a profit. Reversing Entries (LO8) Reversing entries are optional entries used to simplify recordkeeping. They are prepared on the first day of the new accounting period. Reversing entries are prepared for those adjusting entries that created accrued assets and liabilities (such as interest receivable and salaries payable). Copyright © 2022 McGraw Hill 4-5 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce Summary of THE ACCOUNTING CYCLE STEPS 1. Journalizing 2. Posting 3. Work sheet 4. Preparing the statements 5. Journalizing and posting of adjusting entries 6. Journalizing and posting of closing entries 7. Post-closing trial balance Assuming a worksheet is used PURPOSE To record the daily transactions TIMING During the period To transfer the amounts from journal entries to the individual accounts affected by the recorded transaction To summarize the balances of ledger accounts and test the accuracy of journalizing and posting and the computation of account balances (unadjusted trial balance columns) To plan the adjusting entries and the income statement and balance sheet numbers To prove the mathematical accuracy of profit To provide information for closing entries To report financial information During the period To bring the ledger accounts to adjusted balances End of period To bring all temporary accounts to zero and the capital account up-to-date To prove the accuracy of the adjusting and closing procedures End of period Copyright © 2022 McGraw Hill 4-6 End of period End of period End of period Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce Additional Example of Classified Balance Sheet (Very comprehensive, uses all classifications) MUSIC WORLD BALANCE SHEET DECEMBER 31, 2022 Assets Current Assets Cash Short-Term Investments Accounts Receivable Merchandise Inventory Prepaid Insurance Supplies Total Current Assets Non-current Investments Land Held for Future Use $30,360 2,000 43,000 60,700 6,600 1,696 $144,356 13,950 Property, Plant and Equipment: Land Building Less Accumulated Depreciation Office Equipment Less Accumulated Depreciation Total Plant and Equipment Intangible Assets Trademark Total Assets $ 4,500 $20,650 8,640 $ 8,600 5,000 12,010 3,600 20,110 500 $178,916 Liabilities Current Liabilities Accounts Payable Salaries Payable Current portion of long-term liabilities Total Current Liabilities Non-current Liabilities Mortgage Payable (less current portion) Total Liabilities 25,683 17,000 10,200 $52,883 27,600 $ 80,483 Equity Joy Melody, Capital Total Liabilities and Equity 98,433 $178,916 Copyright © 2022 McGraw Hill 4-7 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce Chapter 4 Alternate Demo Problem The trial balance of Large Company, Inc. at the end of its annual accounting period is as follows: LARGE COMPANY, INC. Trial Balance December 31, 2021 Cash .............................................................................. Prepaid Insurance ......................................................... Supplies ....................................................................... Equipment ................................................................... Accumulated Depreciation—Equipment ........................ C. Large, Capital ............................................................ C. Large, Withdrawals ................................................... Revenue ........................................................................ Salaries Expense ............................................................ Rent Expense ................................................................ Totals ............................................................................ Additional information: 1. Expired insurance, $600. 2. Unused supplies, per inventory, $800. 3. Estimated depreciation, $1,000. 4. Earned but unpaid salaries, $700 Required 1. Prepare adjusting entries. 2. Prepare closing entries. 3. Prepare a post-closing trial balance. Copyright © 2022 McGraw Hill 4-8 $ 4,000 1,600 2,100 20,000 $ 2,000 19,000 2,000 33,000 18,300 6,000 $54,000 ______ $54,000 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce Chapter 4 Solution: Alternate Demo Problem 1. Insurance Expense ................................................. 600 Prepaid Insurance ........................................... Supplies Expense ................................................... 600 1,300 Supplies .......................................................... Depreciation Expense Equip. .................................. 1,300 1,000 Accumulated Depreciation Equip. .................... Salaries Expense .................................................... 1,000 700 Salaries Payable .............................................. 2. Revenue ................................................................ 700 33,000 Income Summary ............................................ Income Summary ................................................... 33,000 27,900 Salaries Expense .............................................. 19,000 Rent Expense .................................................. 6,000 Insurance Expense ........................................... 600 Supplies Expense ............................................. 1,300 Depreciation Expense ...................................... 1,000 Income Summary ................................................... 5,100 C. Large, Capital............................................... C. Large, Capital ..................................................... C. Large, Withdrawal ....................................... Solution continued next page Copyright © 2022 McGraw Hill 4-9 5,100 2,000 2,000 Instructor’s Manual for Larson/Dieckmann/Harris Fundamental Accounting Principles 17ce 3. LARGE COMPANY, INC. Post-Closing Trial Balance December 31, 2021 Dr. Cash....................................................................... $4,000 Prepaid Insurance .................................................. 1,000 Supplies ................................................................. 800 Equipment ............................................................. 20,000 Cr. Accumulated Depreciation, Equipment .................. $ 3,000 Salaries Payable ..................................................... 700 C. Large, Capital ..................................................... ______ 22,100 Totals..................................................................... $25,800 $25,800 Copyright © 2022 McGraw Hill 4-10