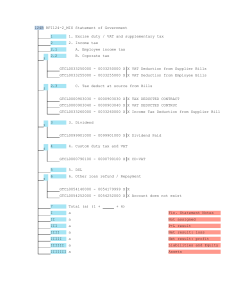

ACCA Paper Russian Taxation Pocket Notes 2020 Contents ► A Guide to the Exam ► Russian Tax System ► Corporate Profits Tax ► Value Added Tax ► Personal Income Tax ► Insurance Contributions ► Corporate Property Tax ► Tax Planning, Administration and Control. Все права защищены. «Эрнст энд Янг» A Guide to the Exam ALL questions are COMPULSORY: MAX 3 hours Section А 1 15 multiple choice questions 2 marks each Section В 2 Corporate Profit Tax (CPT) 3 Insurance contributions (IC) 4 Personal Income Tax (PIT) 10 marks each 5 VAT 6 Personal Income Tax (PIT) 7 Corporate Profits Tax (CPT) Все права защищены. «Эрнст энд Янг» 15 marks each Pass mark: MIN 50 marks of 100 Reading & planning time To be used for: ► Read the requirement ► Plan the layout of your answer ► Carefully read the scenario ► While reading annotate the question ► Highlight relevant information & key items ► Make preliminary calculations ► Plan your answer ► Pay attention to marks awarded ► Plan the order of your answers Все права защищены. «Эрнст энд Янг» Examination hints Practice CBE workspace at www.accaglobal.com Time management ► Allocate your time in proportion to the marks: 1 mark ~ 2 mark question ~ 10 mark question ~ 15 mark question ~ ► 1,8 min 3,6 min 18 min 27 min Attempt all the questions Layout ► Use standard format for tax computations ► Use the layout from the model answers Все права защищены. «Эрнст энд Янг» Examination hints Reading the question ► Start reading from the requirement ► Read carefully the scenario ► Do not write information not required by the question ► Do not write out the question Making assumptions ► Make only brief assumptions ► Use assumptions only if necessary for computation Все права защищены. «Эрнст энд Янг» Russian Tax System Taxes and Taxation TC art. 8 A tax is a compulsory and individually non-refundable payment which is collected from organization and physical persons for the purpose of financing the activities of the State and/or municipalities. Purpose of taxation: ► Revenue to the budget ► Redistribution of income ► Repricing Types of taxes: Direct ► Indirect ► Все права защищены. «Эрнст энд Янг» Progressive ► Regressive ► Proportional ► Tax Legislation Tax Code Part 2 (specific taxes) Part 1 (basic elements) Principles ► Rights And Obligations Of ►Taxpayers, Tax Authorities ► Rules For Tax Audit ► Все права защищены. «Эрнст энд Янг» Corporate Profits Tax ► Value Added Tax ► Personal Income Tax ► Corporate Property Tax ► Insurance Contributions ► Basic elements of tax Tax payers Tax base Tax period Who ? In what amount ? When ? Object What ? Tax rate Tax How much ? Payment Reporting Tax calculation When and how much ? How often ? Formula Все права защищены. «Эрнст энд Янг» Types of taxable income Companies CPT VAT IC Tax agent Individuals PIT Wages & salaries Individual Entrepreneurs PIT on business income PIT on individual income IC VAT Все права защищены. «Эрнст энд Янг» Taxpayers, Tax agents & Tax authorities Tax authorities Control on-site tax audit in-house tax audit transfer pricing tax audit Clarify tax legislation Tax monitoring Tax payment to budget Tax declaration Calculation of tax Tax agents Taxpayers ► Pay taxes on their own income ► Pay taxes on others behalf Obliged to withhold and remit to the budget ► Все права защищены. «Эрнст энд Янг» Special tax regimes Special tax regime Unified agricultural tax Simplified tax system Unified tax on imputed income Substituted taxes Object of taxation Income less expenses Corporate profits tax (20%), Personal income tax, VAT (except import VAT), property tax (except cadastral value) Все права защищены. «Эрнст энд Янг» Income Income less expenses Based on patent amount (statutory level of income for certain type of business) Statutory level of income for certain type of business Tax rate 6% 6% 15% 6% 15% Tax payments Current year: by 25th of July Following year: by 31st March Current year: by 25th April, 25th July, 25th October Following year: by 31st March Within 25 days from the beginning of the activities (not less that 1/3 of tax), the rest amount – within 25 days after the end of patent Current year: by 25th April, 25th July, 25th October Following year: 25th January Corporate Profits Tax Corporate Profits Tax Exam success factors: Use the layout of model answers ► Finish the computation ► Do not forget to exclude VAT if necessary ► Give clear reference to notes ► Все права защищены. «Эрнст энд Янг» Corporate Profits Tax - NEW ►Since 01.01.2018 till 31.12.2027 taxpayers are granted investment deduction in the amount of acquired and/or modernized fixed assets (article 286.1 TC) ►Tax regulations for multinational groups of companies (chapter 14/4-1 TC) and corresponding sanctions for non-compliance (articles 129.9, 129.10, 129.11 TC) are effective since 2017. ►Since 01.01.2019 increasing depreciation coefficient – up to 2 shall be used to fixed assets included in state list of innovative facilities (item 1 article 259.3 TC) ►Employer’s expenses on recreation of employees and their families in Russian Federation (including travel, living and meals if provided, resort treatment and excursions) shall be deductible limited to 50 000 RR per person annually and is included into medical insurance expenses limited to 6% of labour costs (item 24.2 article 255 TC) Все права защищены. «Эрнст энд Янг» Corporate Profit tax Taxpayers Tax base Tax period Legal entities Taxable profit Calendar year FLE – not tested Object of taxation Taxable income less Deductible expenses Tax rate CPT 20 % 13 % / 15 % Payment Reporting Tax calculation Monthly: + 28 days/ by 28th of March Quarterly/ Monthly: + 28 days/ by 28th of March Taxable profit *20% Все права защищены. «Эрнст энд Янг» Taxable profits What items to include in taxable profits? Income Type Date of recognition Все права защищены. «Эрнст энд Янг» - = Expenses Type Test on deductibility Direct/indirect (date/period of recognition) Taxable profit Accruals vs cash methods Cash method Accruals method Income & expenses are recognised in the reporting period which they relate to, regardless of money &/or property receipt/payments ► Matching principle (direct relation & allocation) ► Split of long-term income/expenses between the reporting periods according to the terms of agreement Все права защищены. «Эрнст энд Янг» Income & expenses are recognized when actually paid ► Limited use: average income (net of VAT) for previous 4 quarters should not exceed 1mln RR per quarter ► In case of breach recalculation starting the beginning of the tax period Taxable income & deductible expenses Operational income: 1. 2. 3. 4. Sales of goods produced Property/property rights sales Sales of purchased goods Sales of fixed assets Production & sales expenses: 1. 2. 3. 4. Non-operational expenses: Non-operational income: ► ► ► ► ► ► ► ► ► ► Rental income Copyright income Interest income Fines & penalties for breach of commercial contracts Free property receipts (incl free financing) unless from related party ownership 50 % Foreign currency exchange gains Income of past years Income from participation in other entities “Claw-back” of previous provisions Accounts payable write-offs Все права защищены. «Эрнст энд Янг» Cost of goods produced sold Cost of property/property rights sold Cost of purchased goods sold Cost of fixed assets sold ► ► ► ► ► ► ► ► ► Leased assets related expense Copyright income Interest expense Fines & penalties for breach of commercial contracts Foreign currency exchange losses Expenses of past years Bad debt provisions Accounts receivable write-offs Bank fees Exempt income & non-deductible expenses Exempt income: ► ► ► ► ► ► Advances received under accruals method Contributions received to charter capital Property received by commissioner (excl. commissioner fee) Loans received property received from related party (if not transferred to a 3rd party within a year) property received for the purposes of direct financing Non-deductible expenses: ► ► ► ► ► ► ► ► ► ► Все права защищены. «Эрнст энд Янг» Advances made under accruals method Dividends & profits distribution Penalties & fines paid to budget Contributions to charter capital Partially deductible expenses (exceeding statutory norms) Property transferred to commissioner (excl. commissioner fee) Loans given Cost of property given free of charge Property given for the purposes of direct financing Certain benefits to employees Expenses deductible partially deductible non-deductible General criteria for deductibility: - Justifiable & - Documentary proved costs & - Linked to income-generated activities if any of these criteria is not met, expenses are treated as non-deductible art. 252 Все права защищены. «Эрнст энд Янг» Deductible expenses Deductible expenses Indirect Direct decrease taxable base of the period partially Cost of sales in full WIP (allocated to closing stock of goods) ►Taxpayer may define the list of direct/indirect expenses himself in the principles for tax purposes art. 318, 320 Все права защищены. «Эрнст энд Янг» Direct & indirect costs Direct costs Services Trading company Production ► Purchased cost of trading stock ► & related transport costs ► Materials & components used in production ► Depreciation of production fixed assets ► Direct wages & salaries ► & Related IC company Все права защищены. «Эрнст энд Янг» Indirect costs ► All the expenses are allowed to be treated as indirect ► All the other expenses of the period ► Indirect materials (for packaging, fuel & energy, instruments, special cloth, low valued items) ► Depreciation of non-production fixed assets ► Indirect wages & salaries ► & Related IC Allocation of transport costs Cost of ending trading stock: - FIFO – Weighted average – Actual unit cost Goods Transport costs 100 15 plus purchases for the period 1 000 200 less closing balance (200) Opening balance Cost of Sales Average percentage of transport costs Все права защищены. «Эрнст энд Янг» ? = x% ( ?? ) ??? Transport costs (opening balance + purchases for the period ) Goods (opening balance + purchases for the period ) Allocation for production operations Method may be chosen by a taxpayer but should be justifiable Sample methods: Type of activities Processing of raw materials Works & services Other types of production activities Все права защищены. «Эрнст энд Янг» Method of allocation of direct expense % in natural units: raw materials in ending stock to total raw materials % of uncompleted works (services) in the total works (services) of the period based on standard costs Partially deductible expenses Business travel Interest Advertising Business entertainment Insurance Business training Compensation of interest paid by employees on mortgage loans Все права защищены. «Эрнст энд Янг» Advertising expenses (indirect) Fully deductible ► Mass media advertising (incl. video & cinema shows) ► Out-of-door advertising ► Participation in exhibitions/fairs ► ► Partially deductible Maintenance of demonstration halls, Printing of advertising catalogues & brochures Все права защищены. «Эрнст энд Янг» ► All the other advertising expenses Limit: Deductible up to 1 % of sales revenue (net of VAT) art. 264 Business training expenses (indirect) Fully deductible Non deductible if ALL is met: ►At licensed russian or foreign educational institution ►To permanent employees other ►The training program improves the professional skills of employee & result a better efficiency at working place ► ► ALSO Higher & middle-special education Education of future employees Все права защищены. «Эрнст энд Янг» art. 264 Business travel expenses (indirect) Deductible for CPT (when supported by documents): ► NO statutory norms but LE’s norms required ► Travel costs (incl. taxi to & from airport) ► Airport fees & commission charges ► Luggage fare ► Accommodation expenses (hotel, but not meals, laundry, sports, recreation) ► Business communication expenses (business calls) ► Cost on visas & passports preparation Travel outside Russia: ► No statutory norms but LE’s norms required ► Principle of arrival country ► Exchange rate as at the date when travel report is approved art. 264 Все права защищены. «Эрнст энд Янг» Business entertainment expenses (indirect) 1. Expenses connected with the reception & servicing the representatives of other organisations, who conduct business negotiations with the taxpayer 2. Expenses incurred with the relation of the board of directors 1. Cost of official reception (breakfast, lunch, dinner) 2. Transport costs (local) 3. Cost of buffet (meals) during negotiations 4. Cost of external translators Deductible up to 4 % of deductible labour costs (incl. bonuses, compensations, voluntary insurance, not IC) Must be documented !!! art. 264 Все права защищены. «Эрнст энд Янг» Insurance expense medical personal > 1 year against death, harm to heath pension Any breach of conditions Include previously deducted expenses into non-operational income > 5 years, license, personal Deductible if license, age Insurance premium covering more than one reporting period - deductible proportionally to calendar days Deductible within the list set by the law – enlarged Employees life Deductible within the tariffs set by the law Property & 3rd party liabilities > 5 years Mandatory Voluntary non-state pension Insurance deductible within the limit of (12 % of LC) (6 % of LC) (15 TRR) Все права защищены. «Эрнст энд Янг» Labour costs Deductible expenses ► ► ► ► ► All kinds of payments both in cash and in kind, production incentives, compensations for working conditions and environment, operating bonuses and onetime incentives, other payments under legislation of RF and labour agreements, e.g.: Wages and salaries for worked hours, paid vacations (including provisions made), payments for unused vacations, study leaves, other paid absence according to legislation of RF Mandatory and voluntary insurance of employees (subject to certain limitations) Payments to individuals (not individual entrepreneurs) under civil-law contracts for works /services performed Compensation of interest paid by employees on mortgage loans (within limit) Все права защищены. «Эрнст энд Янг» Non-deductible expenses ► ► ► ► ► ► Gifts in cash or in kind & related expenses payable to employees Financial aid Price Difference when selling goods to employees below market prices Free or low-priced meals to employees (unless provided in the labour contracts) Compensation of commuting expenses to the work place & back (unless provided in the labour contracts) Travel, recreation, medical treatment, sports, entertainment provided to employees art.255 /art. 270 Other benefits for employees 1. Compensation of interest paid by employees on mortgage loans Partially deductible Statutory limit for compensation of interest paid on mortgage loans: 3 % of labour cost ► Effective for unlimited period ► If deductible for CPT ➔ non-taxable for PIT 2. Payment for recreation of employees and their families including travel, living and meals if provided, resort treatment and excursions in Russian Federation deductible within 50 000 RR per person limited to 6 % of labour costs (along with medical expenses) Все права защищены. «Эрнст энд Янг» Labour costs as the limit for CPT Labour costs Business entertainment expense Voluntary life insurance Voluntary medical insurance Compensation of interest paid on mortgage loans Limit 4% 12 % 6% 3% Wages YES YES YES YES Bonus YES YES YES YES Benefits in kind (deductible for CPT) YES YES YES YES Voluntary insurance YES NO NO YES IC NO NO NO NO Все права защищены. «Эрнст энд Янг» Interest income & expense (non-operational) BASIC RULE: Interest income & expense – NO LIMITS LOAN / 365 days * DAYS of the period* ACTUAL RATE ►Taxable / deductible at ACTUAL RATE ► for the period of actual use of borrowed funds (based on number of days – do not take the first day but take the last) ► at the end of each month Exemption # 1: Controlled loans Interest income: Interest expense: at actual rate, at actual rate, if > lower limit if < upper limit Interest for threshold limit: at the end of the month or at agreement date if no change of interest rate in loan agreement Threshold interest rates Currency Lower limit Upper limit Rouble 75 % * key rate CB 125 % * key rate CB EUR EURIBOR + 4% EURIBOR + 7% USD USD LIBOR +4% USD LIBOR +7% Exemption # 2: Thin capitalisation rules Все права защищены. «Эрнст энд Янг» art. 269 Thin capitalisation rules Controlled loan: 1. Lender (FLE) owns > 25 % of RLE 2. Lender (RLE) is affiliated to FLE owning > 25 % of RLE 3. Such FLE (its affiliate) guarantees the loan to RLE gives FLE Loan + %% 3 times exceeds net assets & (excl. tax liabilities) of RLE (borrower) Loan + %% loan guarantees directly or indirectly owns more than 25 % >3 RLE Net assets (excl. tax liabilities) ? Yes Thin capitalisation rules: ► Capitalization ratio ► Deductible interest ► “Deemed” dividends and the CPT at 15 % Все права защищены. «Эрнст энд Янг» No interest is deductible under general rules Thin capitalisation rules interest on controlled loan deductible Capitalization ratio = Deductible interest = deemed dividends Controlled loan + unpaid interest (Net assets (excl. tax liabilities) * % ownership*3) Interest at limited rate Capitalization ratio “Deemed dividends” = Actual interest – Deductible interest CPT on “deemed dividends” = “deemed dividends” * 15 % Все права защищены. «Эрнст энд Янг» Depreciation Depreciable fixed assets: ► Used for > 12 months ► Initial cost > 100 000 RR But not: NBV end = NBV beginning *(1-k%)n Depreciable cost: Initial cost (net of VAT) less 10 % (30 %) write off But not: Land and natural resources ► Inventory ► Incomplete capital construction ► Securities ► Also excluded: Interest expense ► Forex differences ► registration fees ► state duties & taxes ► Revaluation ► Given for gratuitous use ► Conservated for > 3 months ► Reconstructed (modernized) for > 12 months ► Modernization additional cost Useful life: is determined according to 10 depreciation groups Depreciation STARTS: next month after fixed asset was put into use Methods of depreciation: straight - line non-linear 1/n * 100 % to original cost K % to NBV to group increase of useful life Special coefficients: change change depreciable value depreciation rate 10 % (30 %) write off Все права защищены. «Эрнст энд Янг» Leasing – up to 3 (not to 1-3rd groups) ► Fixed assets used in innovative facilities – up to 2 ► Investment deduction (2018 – 2027) ➢ ➢ ➢ ➢ ➢ Right of taxpayer → accounting policy for 3 years Fixed assets of 3rd – 7th depreciation groups If enacted in the Region Can be carried forward to the following years To be recovered if fixed asset is sold Instead of ▪ Write off ▪ Depreciation Investment deduction when put in use decrease Regional CPT Federal CPT 90% of initial cost 10 % of initial cost limited to 17%-5% = 12% of CPT tax base before deduction without any limit art.286.1 Все права защищены. «Эрнст энд Янг» Leased assets - depreciation Lease operational financial on the balance of lessor on the balance of lessee Lessor income expense Lessor leasing payments depreciation x3 ~ income leasing payments expense proportionally to income (leasing payments) Lessee Lessee ► expense leasing payments = Все права защищены. «Эрнст энд Янг» expense Depreciation x3 Rest amount of leasing payment ► Leased assets – capital improvements lessee makes capital improvements lessor approves & reimburses expenses approves & BUT doesn’t reimburse expenses lessee shall depreciate capital improvements lessor shall depreciate capital improvements Depreciation under statutory norms during the lease period (the rest amount is non-deductible) ► 10 % (30 %) write off is applicable to capital improvements ► Все права защищены. «Эрнст энд Янг» 10 % (30 %) write off is applicable to capital improvements ► Research & development costs Deductible expenses: upon completion of R&D works or their stages not for R&D for customers 1. Depreciation of fixed and intangible assets for the period (full calendar months) when such assets were used solely for R&D activities; 2. Labour costs for employees for the period (proportion allocation is possible) when they participated in R&D activities; 3. Material expenses directly related to R&D activities; 4. Other expenses directly related to R&D activities limited to 75 % of labour costs related to R&D activities; 5. Purchased R&D works as per agreement with supplier; 6. Payments to Science and Innovation Fund limited to 1,5 % of sales. ► ► ► ► If in State list, deductible expenses = actual * 1,5. To be supported with technical report submitted to tax authorities If intangible asset, deductible expenses = depreciation during useful life or 2 years. Sale at loss of intangible R&D asset shall be non-deductible. Все права защищены. «Эрнст энд Янг» Non-operational income & expenses Foreign exchange gains and losses Loan* (Exchange rate date of receipt of loan– Exchange rate end of quarter ) Assets received and given for free: ► Taxable income vs non-deductible expense Fines and penalties: Taxable income & deductible expense for customers & suppliers ► Non-taxable income & non-deductible expense for budget ► Profits and losses for the previous years: Understated tax liability (profit revealed) – must amend previous years tax calculations ► Overstated tax liability (loss revealed) – may include in tax calculations of the current period ► Все права защищены. «Эрнст энд Янг» Property disposals Type of property Result on disposal Sales (net of VAT) Stock Sales (net of VAT) Fixed & intangible assets -NBV (tax) (X) X / (X) X (X) - sales related expenses (X) Gain / Loss Все права защищены. «Эрнст энд Янг» X less balance value (tax) Gain / Loss Loss treatment X / (X) reduces taxable income in the period of disposal reduces taxable income for the rest period of useful life in equal amounts Factoring Delivery Supplier (creditor) Customer (debtor) Payment Debt assignment Cash Factoring company (factor) discount on factoring is treated Delivery (shipment) date as interest Deductible within the limit: - upper limit for interest - using transfer pricing rules deductible limit for rouble debts: Sum received from factor * CB RR * 1,25 * N of days to due term / 365 days Все права защищены. «Эрнст энд Янг» Time of settlement of receivable under agreement as bad debt Loss is fully deductible at factoring date Bad debt expense Bad debts written off expiration of statutory term of debt collection (3 years) ► Official liquidation of the company (bankruptcy) Bad debt provision right of the taxpayer ► After Deductible non-operational expense ► If bad debt is written off for which bad debt provision has been created, no expense is recognised in the period of writing it off. limits depending on the age of debt: ► Less than 45 days 0% ► 45 days – 90 days 50 % ► More than 90 days 100 % ► Deductible within the limit: 10 % of Sales revenue (net of VAT) of the current or pervious tax period ► Overestimated provision is added to non-operational income ► Debt shall be decreased by payables owed to the customer ► Все права защищены. «Эрнст энд Янг» Only customer’s debts Losses carried forward ➢Losses can reduce taxable profits only by 50 % of tax profit of the period (starting from 01.01.2017) ➢Losses of previous tax periods can be utilized without any period limitation ➢FIFO METHOD IS USED ➢TAXPAYER SHALL NOT REDUCE TAX BASE ON LOSSES RECEIVED WHEN TAXPAYER’S INCOME WAS SUBJECT TO 0 % Все права защищены. «Эрнст энд Янг» CPT & subdivisions Federal budget + Regional budget 20% = 3% + 17% Subdivision: ► Territory separated office ► Workplace established for more than 1 month ► Doesn’t matter if not in charter documents Regional part of CPT (17 %) shall be allocated to each subdivision and paid to regional budget Allocation of CPT to subdivision: % of FA NBV (tax) FA % of labour costs or % of average staff + 2 Все права защищены. «Эрнст энд Янг» = % of allocation of regional CPT to each subdivision Dividend income Tax = Share of dividends * Tax rate * (Distributable – Received ) dividends dividends 13 % Russian legal entity 15 % Foreign legal entity 0% RLE owning >50 % of the share capital ► for > 365 days ► if from FLE it must be incorporated outside offshore zones ► ► Should be withhold by tax agent (paying out entity) & remitted to budget within 1 day after dividends are paid out ► If dividends are received from foreign legal entity tax is paid at 13 % rate along with submission of CPT declaration Все права защищены. «Эрнст энд Янг» Dividends. Exam approach CPT on dividends to FLE CPT = Distributed dividends * Share of ownership * 15% CPT on dividends to RLE (1) Total distributed dividends (DO NOT INCLUDE dividends payable to FLE) (2) Less net dividends received (DO NOT INCLUDE dividends received taxable at 0%) (1)-(2) Dividends taxable at 13 % CPT= 13% * Share of dividends at 13% (*) Total dividends withheld at source RR ХХ ХХ (ХХ) ХХ ХХ ХХ Все права защищены. «Эрнст энд Янг» Transfer pricing ► Effective since 01.01.2012: Article 25 TC ► Controlled transactions Article 105 TC ► Not controlled transactions ► Transfer Pricing Documentation ► Transfer pricing methods ► Transfer pricing tax audit ► Advance pricing agreements ► Consolidated group of taxpayers Все права защищены. «Эрнст энд Янг» Related parties Related parties for CPT shall be: LE or Individuals directly or indirectly own > 25 % of other entities ► LE which executive and supervisory bodies are appointed by 1 person/entity or by group of related parties ► Companies are allowed to declare themselves as related parties for CPT ► Companies - parties of a transaction - may be treated as related partied for CPT upon court decision ► Parties shall not be treated as related for CPT only due to : leading market position or monopoly - ownership in companies which are also owned by Russian Federation, regions of Russian Federation, municipalities ► Все права защищены. «Эрнст энд Янг» Transfer pricing Controlled transactions 1. Deals between related parties 2. Cross-border operations for commodities (if annual deals > 60 mln RR) 3. Cross-border operations with offshore LE (if annual deals > 60 mln RR) Not controlled transactions 1. Deals between companies of consolidated group of taxpayers 2. Deals between RLE: ► Registered in one region (not in special economic zone) ► No sub-divisions in other regions or abroad (i.e. CPT is not paid to the budget of other regions) ► No tax losses ► No MET or % CPT or special tax regimes Все права защищены. «Эрнст энд Янг» Transfer pricing documentation LIST of controlled transactions: ► No later than May 20 of the following year ► Information on kind of transactions, parties, amounts DOCUMENTATION on controlled transactions: ► Submitted upon request of tax authorities: - which shall be issued no later than 1 June of the year following the calendar year - within 30 days after receiving the request ► Shall include: - structure and terms of the transaction, the parties involved and their functions, and the pricing methodology; description of the transfer pricing methods, sources of information used, and rationale for the choice of transfer pricing method; other factors that might influence the price (for example, marketing strategy); ► Shall include Adjustments to the tax base. Penalties on non-submission /late submission/ incorrect information = 5 000 RR Все права защищены. «Эрнст энд Янг» Transfer pricing methods 1 Comparable uncontrolled price (CUP) method Compare price used in controlled transaction with prices for similar peer goods sold under comparable terms between independent parties 2 Resale minus method Compare price of resale of goods adjusted for market gross margin with purchase price in controlled transaction: calculate actual gross margin in controlled transaction and compare it with range of gross margins for comparable transactions. 3 Cost plus method Compare price of controlled transaction with market price calculated as costs of controlled transaction increased by normal margin 4 Comparable profits method Compare operating margin (return on sales, return on assets, return on costs, return on general and administrative costs) of controlled transaction with range of operating margin for comparable transactions 5 Profit split method Profit from sales is split between parties of controlled transaction proportionally to each party’s contribution to sales profit Все права защищены. «Эрнст энд Янг» Transfer pricing – APA & CGT Advance pricing agreements (APA): ► Applicable for “Major taxpayers” ► Worth 1,5 mln RUB of state duty ► 6/9 months for review by tax authorities ► Approved advance pricing agreement is valid for 3 years and may be prolonged for an additional 2 years at the taxpayer’s request ► Will not be changed even if relevant provisions of tax legislation are amended Consolidated group of taxpayers (CGT): ► Applicable for RLE owing not less than 90 % of the others ► One authorized entity of consolidated group of taxpayers shall calculate and pay cumulative taxes based on cumulative financial result ► Application with an agreement on entering consolidated group of taxpayers must be submitted and to be confirmed by tax authorities ► Special procedures for reporting, tax audits and penalties and fines Все права защищены. «Эрнст энд Янг» Multinational Group of Companies MGC– is a group of entities (incorporated and not) which are related to each other by ownership or by control if all the criteria are met: 1.Consolidated financial reporting is filed according to legislation of RF or stock exchange 2. At least one of the companies is either - a tax resident of Russian Federation / not a tax resident of Russian Federation A member of the multinational group of companies shall submit the following documentation: - notice of a membership in a multinational group of companies - country information on a multinational group of companies - global documentation - national documentation - country report of a multinational group of companies on states which recognize members of a multinational group as its tax residents Chapter 14 TC Все права защищены. «Эрнст энд Янг» Multinational Group of Companies Notice of a membership in the MGC • • • reveals info on members of MGC: titles, incorporation states, registration numbers etc submitted to the Tax authorities as electronic documents within 8 months after the end of a reporting period for the parent company of MGC Country information • • • • income and expenses, profit and loss received in Russian Federation and/or abroad key indicators on operations of a member of a multinational group of companies taxes paid in Russian Federation and abroad for consolidated income over 50 billion RR Global documentation (for the periods starting since 2017) • • • is submitted upon request from tax authorities within 12-26 months after reporting to be replied within 3 months after the request of tax authorities shall constitute information on capital and control structure of a multinational group and markets of business operations, intangible assets of a members, business and financial information of a member of MGC National documentation (for the periods starting since 2018) • • • is submitted by request of tax authorities terms and requirements are similar to tax documentation on controlled deals describes operations (including pricing basis) of controlled transactions if one of the counterparts is a foreign member of MGC refers to submitted global documentation Country report (for the periods starting since 2017) • Все права защищены. «Эрнст энд Янг» • • is submitted upon the request of tax authorities in a formalized way as electronic document within 12 months after the end of reporting period consists information for the reporting period on income/expense on transactions, profit/loss before taxation, amounts of taxes paid, amount of capital and accumulated profits, number of staff, amounts of tangible assets and identification of each member of MGC based on consolidated financial reporting according IFRS Breach of tax rules for Multinational Group of Companies Tax offence Tax penalty Breach of reporting terms of notice of a member of MCG or submission of false information * 50 000 RR Breach of reporting terms of country report or submission of false information * 100 000 RR Non submission of national documentation 100 000 RR Non submission of global documentation * 100 000 RR * Violations of MGC reporting requirements shall not be penalized in 2017-2019 Все права защищены. «Эрнст энд Янг» Reporting & payment Quarterly Reporting Monthly Reporting Quarterly Reporting & Payment Monthly advance payments based on estimated profits Monthly advance payments based on actual profits Limited to small companies (> 15 mln RR per quarter) Reports 4 times a year Reports 12 times a year Reports 4 times a year Reporting periods: 1st Reporting periods: 1 month, quarter, half a year, 9 months 2 months, 3 months …. 11 months Reporting periods: 1st quarter, half a year, 9 months Pays 16 times a year Pays 12 times a year Pays 4 times a year Reporting dates: 28th of April, 28th of July, 28th of October Reporting and payment dates: advance payments: 28th of each month following the reporting period annual payment: 28th of March Reporting and payment dates: 28th of April, 28th of July, 28th of October annual payment: 28th of March Payment dates: 28th of each month annual payment: 28th of March Cumulative calculation of tax for the reporting period annual payment: 28th of March Tax formula Amount Calculation + Sales income (excl. VAT) - Sales expenses (excl. VAT) = Operational profit + Non-operational income (excl. VAT) - Non-operational expenses (excl. VAT) = Tax base (before loss carried forward) - Loss carried forward = Tax base (after loss carried forward) x Tax rate = Tax Все права защищены. «Эрнст энд Янг» Value Added Tax Value Added Tax Exam Success Factors: ► Attempt the question devoted to VAT (Q4 Section B) ► Use all the data provided in the questions ► Follow the model answers layout. Все права защищены. «Эрнст энд Янг» Value Added Tax NEW 1st of January 2019 standard VAT is increased to 20% (article 164 TC); ►Declarative procedure of VAT recovery can be applied by taxpayers with the amounts of taxes paid for the previous 3 years exceeding 2 billion RR (article 176.1 TC); ►Declarative procedure of VAT recovery requires bank guarantee for at least 10 months since tax declaration submission day (subitem 1 item 4 article 176.1 TC); ►Taxpayer is allowed not to use 0% tax rate on export of goods and related services to all of its operations (not to specific deals) by submission of application before tax period start for not less than 1 year (article 164 TC); ►In-house audit on VAT shall be limited to 2 months with the possible extension up to 3 months in case of signs of taxpayers violations (item 2 article 88 TC); ►Since 1st of January 2018 VAT tax rate for re-export shall be 0% (subitem 1 item 1 article 164 TC). ►Since Все права защищены. «Эрнст энд Янг» Value Added Tax Taxpayers Legal entities Individual entrepreneurs Tax base 1. Revenue 2. Customs cost 3. Cost of construction Object of taxation 1. Sales 2. Import 3. Self-supplied construction Tax period Quarter Tax rate VAT 20% / 10% / 0% Tax calculation Payment Monthly: +25 days (1/3) Все права защищены. «Эрнст энд Янг» Reporting Quarterly: +25 days Output VAT less Input VAT Company B Buys ore 120 (incl. VAT 20) Wages & IC 100 Sells steel 360 (incl. VAT 60) Buys steel 360 (incl. VAT 60) Wages & IC 100 Sells heater 840 (incl. VAT 140) 60 20 steel Company A 60-20 =40 140-60 =80 Federal Budget Все права защищены. «Эрнст энд Янг» 140 60 heater Principle of VAT taxation Individual VAT tax rates 0% Exports 10 % Lower 20% Basic ► ► Goods exported outside Russia Works (services) related to the production & sales of exported goods (e.g. transportation, loading) art. 164 Все права защищены. «Эрнст энд Янг» Limited list of products (mostly food & children items) - Special VAT rates 20/120 or 10/110 for: ► Advances (both received & paid) ► Sales related income ► VAT withheld by tax agents ► Goods with capitalised VAT VAT invoice and VAT registers VAT invoice ► ► ► ► ► ► Issued by seller within 5 days after shipment of goods (works, services) or prepayment receipt Essential for VAT recovery Required for: - VATable operations Not required for: - retail sales - VAT exempt operations Signed by director and chief accountant Can be nominated in foreign currency Customer: Seller: Input VAT Output VAT Purchase Book Sales Book - + VAT return Sales agents, forwarding agents, developers: Register VAT invoices in Journals of VAT invoices received and issued (except own operations) Все права защищены. «Эрнст энд Янг» Content of VAT invoice 1 2 3 number and date of issue name, address and identification numbers of the taxpayer and the purchaser name and address of the consignor and of the consignee 4 5 6 7 Number of the payment and settlement document Description of the goods supplied Quantity of goods supplied Price (tariff) per unit of measurement 8 9 10 11 Value of goods for the entire quantity of goods supplied excluding tax Amount of excise duty for excisable goods Tax rate Amount of tax charged to the purchaser of the goods 12 13 14 Value of the entire quantity of goods supplied including the amount of tax Country of origin of the goods Number of the customs declaration Content of VAT invoice Все права защищены. «Эрнст энд Янг» Input VAT recovery is possible Amended VAT invoice ► Issued by seller to purchaser in case of changes of purchase price of goods (works, services) sold due to changes in price or quantity 5 days ► After seller has informed purchaser on price change and received confirmation from the purchaser that the price change is accepted (addition l agreement or other written acceptance shall be signed). ► Shall include information on: ► Number and date of initial VAT invoice; ► Initial amount of goods, initial price for goods and initial purchase price; ► Amended amount of goods, amended price for goods and amended purchase price; ► Difference between initial VAT invoice and Amended VAT invoice. ► If negative difference – minus. Все права защищены. «Эрнст энд Янг» Amended VAT invoice Increase of purchase price Seller Customer Add to Output VAT Add to Input VAT At the date of written document confirming price change Add to Input VAT Decrease of purchase price Все права защищены. «Эрнст энд Янг» At the date of amended VAT invoice Add to Output VAT (claw back of previously recovered Input VAT) At the date of amended VAT invoice Output VAT Recognized at the earliest of dates: Dispatch date Payment date (prepayment date) Sales related amounts: ► Interest (discounts) on bonds & promissory notes, received for sales of goods (services, works), exceeding current CB RR ► Interest on commercial credits, exceeding current CB RR – Related amounts are VAT exempt if the main sale is VAT exempt Sum differences ► Not adjusting VAT tax base (Output VAT) and Input VAT ► Shall be recognized as taxable income and deductible expenses. Volume discounts to customers ► shall not influence VAT liability unless stated in the agreement Все права защищены. «Эрнст энд Янг» VAT exempt operations ► ► ► ► ► ► ► Currency circulation (Russian & foreign) Insurance Interest Assets transfer during reorganization Sale of assets of bankrupt entities Charter capital contributions Some other Special rules for VAT exempt operations ► Separate accounting for VATable and VAT exempt operations ► Input VAT allocation rules ► Licensed activities are exempt only if license obtained ► Agents do not enjoy exemption for their commission on VAT exempt goods. Все права защищены. «Эрнст энд Янг» Recovery of Input VAT Condition of recovery goods (works, services) should be used for activities subject to VAT General criteria for recovery 1. goods (works, services) received & booked 2. supporting documents (VAT invoice & trade documents) NB! Все права защищены. «Эрнст энд Янг» Input VAT shall be recovered in full amount for partially deductible expenses except for business travel expenses & business entertainment expenses VAT on advance payments Tax Period Output VAT Prepay -ment Input VAT CUSTOMER makes prepayment Payment Shipment Period Period Prepayment / 120 * 20 (Prepayment / 120 * 20) (Prepayment / 120 * 20) Output VAT Shipment Input VAT SELLER receives prepayment Payment Shipment Period Period Prepayment / 120 * 20 Sale /120 * 20 (Purchase / 120 * 20) On receiving prepayment supplier shall be obliged to issue VAT invoice and customer shall have right to recognise VAT amount as input VAT ► No Output VAT on advance payments received from foreign customers on export sales since 2006. ► Все права защищены. «Эрнст энд Янг» Allocation of Input VAT Separate accounting Output VAT Input VAT VATable operations VAT exempt operations - * 20 % if relate only to VATable if relate only to VAT operations exempt operations recovered included to costs or capitalized if relate to both VATable & VAT exempt operations Can be ignored if cost of VAT exempt sales is < 5 % of total costs Then such input VAT is fully recovered Все права защищены. «Эрнст энд Янг» Input VAT allocation proportionally to sales (net of VAT) Export operations Output VAT 0% Separate accounting at the last day of tax period when confirmation package is submitted to tax authorities exchange rate as at the last date of quarter otherwise recovered if confirmed within 180 days starting Input VAT from export date • Only for resource exports Export confirmation package: 1. Contract with FLE 2. Shipment documents with customs stamp 3. Customs declaration with customs stamp 4. Commission agreement • No output VAT on advances for export sales Export is treated as unconfirmed • Taxpayer is allowed not to use 0% tax rate on export of goods and related services to all of its operations (not to specific deals) by submission of application before tax period start for not less than 1 year • Since 1st of January 2018 VAT tax rate for re-export shall be 0% Все права защищены. «Эрнст энд Янг» Unconfirmed export Export is treated as unconfirmed if confirmation packaged is not provided to tax authorities within 180 days starting from export date Output VAT 20 % Input VAT recovered at export date amended VAT return for export date tax period late payment interest: 1/300 & 1/150 CB RR (current) Later confirmation of export operation: 1. Submit confirmation package 2. Calculate Output VAT at 0 % (exchange rate at the last date of the quarter when confirmation package is submitted to tax authorities) 3. Deduct Input VAT 4. Deduct VAT paid on unconfirmed export ► No right to recover late payment interest Все права защищены. «Эрнст энд Янг» “Claw-back” of recovered VAT Shift to VAT exempt operations ► Contribution to the charter capital ► “Claw-back” of recovered VAT include in Output VAT estate property materials & fixed assets stock NBV * 20 % tax value * 20 % recovered VAT / 10 years * VAT exempt year sales Total year sales in the current tax period Deductible expense for CPT Все права защищены. «Эрнст энд Янг» last tax period in the year Property disposals Fixed asset has been used for VATable operations Fixed asset has been used for VAT exempt operations Input VAT has been recovered from the budget Input VAT has been capitalized Output VAT on sale: Selling price *20/120 Все права защищены. «Эрнст энд Янг» Output VAT on sale: ( Selling price – Accounting net book value ) *20/120 VAT on goods returned to supplier Goods returned due to 1. Poor quality or inconsistency with agreement Supplier Customer Input VAT Output VAT based on the original VAT invoice of the supplier if adjustment is made to sales within one year since customer’s refusal to accept goods 2. Other reasons Ex-supplier Input VAT ►Supplier: Все права защищены. «Эрнст энд Янг» = New sale VAT invoice General rules Ex-customer Output VAT recovery of output VAT on prepayment (input VAT is recognised) if agreement is cancelled Factoring Delivery Customer (debtor) Payment Output VAT Supplier (creditor) Debt assignment Cash No output VAT No input VAT, unless for financial services Все права защищены. «Эрнст энд Янг» Factoring company (factor) Profit on further debt sale is VATable at the rate 20/120 Commission agreement VAT on agent’s commission only No VAT: - in relation with goods transfer between agent & principle - in relation to expenses reimbursed to agent by principle VAT invoicing procedure (sale) Principle Agent Customer in the Journal, but not in Purchases Book VAT invoice on sale VAT invoice on purchase VAT invoice on sale in Sales Book Все права защищены. «Эрнст энд Янг» in the Journal, but not in Sales Book in the Journal, but not in Purchases Book in Purchases Book VAT invoicing procedure (purchase) Principle Agent Supplier in Purchases Book VAT invoice on purchase VAT invoice on sale in the Journal, but not in Purchases Book in Sales Book VAT invoice on purchase VAT invoicing procedure (commission) Principle VAT invoice on commission in Purchases Book Все права защищены. «Эрнст энд Янг» Agent VAT invoice on commission in Sales Book Self-supplied construction Current tax period Output VAT If used in VATable operations on the last day: 20 % * cost incurred for capital construction in the financial accounting Input VAT general rules recovery of output VAT assessed on self-supplied construction in the same tax period Recovery of Output VAT assessed on self-supplied construction can be done in the same period if the general recovery criteria for Input VAT is met. Все права защищены. «Эрнст энд Янг» Construction costs for self-supplied construction for CPT, VAT & PT Type of expense Depreciable value of FA for CPT Tax base for VAT Initial value for PT Materials used YES YES YES Wages of construction workers YES YES YES IC on wages YES YES YES Cost of subconstructors YES NO YES Interest on loan NO YES YES Все права защищены. «Эрнст энд Янг» Reporting and Payment ► One VAT tax return ► Quarterly reporting & payment ► Only electronic form of VAT tax return since 2014 ► Deadline for reporting & payment – 25th of the month following the end of the quarter ► VAT liability is payable 1/3 of VAT liability per quarter – 3 months after the end of the quarter Все права защищены. «Эрнст энд Янг» How to get the refund? Input VAT > Output VAT In-house tax audit: ► In case of VAT refund upon the submission of VAT tax return ► In relation to VAT recovery on export operations Amount not confirmed for refund End of Quarter Amount confirmed for refund Late payment interest from the budget Submission of End of in-house Decision on VAT VAT tax return tax audit in-house tax audit refund In-house tax audit 1/365 CB RR per day of 25 days 2(3) months 7 days 5 days delay Все права защищены. «Эрнст энд Янг» Declarative procedure of VAT refund Valid for taxpayers: ► With taxes paid during previous 3 years > 2 billion roubles ► In case bank guarantee for 10 months is provided Written request to refund within 5 days after VAT return submitted Decision on refund is to be issued by tax authorities within 5 days after the request received In-house tax audit under general rules In case of any refunded amount is not confirmed during in-house tax audit, taxpayer shall return it to the budget and pay interest for cash usage at CB RR * 2 Все права защищены. «Эрнст энд Янг» VAT Exam Question Answer Format Output VAT Calculation VAT on goods (works, services) sold VAT on prepayment received VAT on sales related income VAT on capital construction VAT on property used for non-VATable transactions VAT on prepayment made recovered Total output VAT Input VAT VAT on materials bought VAT on services bought in VAT on business entertainment expenses VAT on capital construction VAT on prepayment received recovered VAT on prepayment made Total input VAT VAT payable (recoverable) Все права защищены. «Эрнст энд Янг» Amount XXX (XXX) XXX Personal Income Tax Personal Income Tax Exam Success Factors: Start each part of PIT question (Q5 Section B) on a new page ► Do not mix the information between the parts ► Calculate tax base for each tax rate separately ► Use all the data provided in the question ► Follow the model answers layout. ► Все права защищены. «Эрнст энд Янг» Personal Income Tax NEW PIT rules for income from sale of property (purchased after 1st January 2017) have been changed: ►Sale of property shall be exempt if property has been owned for 5 years and more ►Sale of property shall be exempt if property has been owned for 3 years and more and has been inherited, received as a present from relative or privatized ►If selling price is less than 70% of cadastral value as at 1st January of the year of sale tax base shall be calculated as 70% of cadastral value of immovable property ►Regions are allowed to decrease minimal period of ownership and per cent of cadastral value threshold for PIT Since 01.01.2018 interest income on Russian quoted corporate bonds in RR exceeding key CB rate increased by 5% (item 1 article 214.2 TC) Все права защищены. «Эрнст энд Янг» Personal Income Tax Taxpayers Tax base Tax period Individuals Individual entrepreneurs Taxable income per each rate (in cash & in kind) Calendar year Object of taxation Taxable income Tax rate PIT 13% / 35 % 13% / 30% Payment Reporting Tax calculation up to 15th July Tax agent: payment date up to 30th April Tax agent: + 1 month (quarterly) by 1st of April Taxable income less deductions* 13% Taxable income *35% Taxable dividend income *13% Все права защищены. «Эрнст энд Янг» Income recognition date Basic: Payment date deposit interest civil-law agreement copyright income Benefits in-kind: receipt date BUT 1. Wages & Salaries: last date of the month Bonus: when accrued 2. Imputed interest income for low rate loans: last date of the month art.223 Все права защищены. «Эрнст энд Янг» Tax rate 35 % Increased 13 % Basic ► ► ► ► Salary, wages Bonus Gift from the LE (>4000 RR) Business income ► Taxable portion of prizes & awards from advertising games (incl. VAT; > 4 000 RR) ► Interest on bank deposits /quoted corporate bonds exceeding CB RR +5 % (roubles) or 9 % (foreign currency) ► Imputed interest (income) on low rate loans !!! Casino winning ► 12 % Dividend income (separate tax base) 30 % ► All types of income received by tax non-residents Tax base is determined separately for income taxed at different rates Все права защищены. «Эрнст энд Янг» Taxable & exempt income Taxable Exempt ►Dividends ►Payments and interest received ►Insurance payments received in case of insured incident ►Income on copy-rights and related rights ►Rent income, including transport lease ►Income from the sale of property, including immovable property, shares, securities, claims ►Employment remuneration and remuneration for work performed or services rendered ►Pensions, benefits, scholarships and similar payments received under foreign legislation !!! sick-leave payment established by Law ►Reimbursement of costs related to employment and duties performance ►Interest income < CB RR + 5 % (9 %) ►Financial aid to employees in case of the birth of a child < 50 000 RR per child ►Inherited property, gifts from close relatives, gift from individuals if no state registration is required for such gifts ►Increase of shares due to revaluation of assets, rights issue and reorganization ►Mother’s capital received under the rules of the government national program Partially exempt (> 4 000 RR per group): 1. 2. 3. 4. 5. Gifts from LE (13 %) Support payments (13 %) Reimbursement of medical expenses prescribed (13 %) Gifts & prizes in competitions & tournaments held under decisions of authorities (13 %) Gifts & awards in competitions, games & other events held for advertising purposes (35 %) Все права защищены. «Эрнст энд Янг» Benefits in-kind Taxable 13 % Payments to enable employees to perform their duties or to provide ► better working conditions ► If required by law travel expenses up to statutory norms membership of a fitness club medical insurance for employees and relatives trip to Singapour business expenses – reimbursements provision of personal driver free meals provision of mobile phone set company’s payment for private calls business expenses - cash advances discounts provision of car for business purposes training in time management provision of accommodation employer’s payment for medical treatment of a relative car allowance within the government limits grace credit card period (1 month) ► At fair market value (incl. VAT) The arms length principle should be taken into account Non-taxable Все права защищены. «Эрнст энд Янг» ► Allowances & deductions Standard dependant charity Social Property child education agent only cash up to 25 % tax return 50 000 RR per child for both parents tax return agent medical, pension, life insurance, educational expenses education: own, brother, sister medical , life insurance (>5years), pension expenses: own & close relatives up to 120 000 RR sale of property movable – 1 000 000 RR, immovable – 250 000 RR owned > minimum period of ownership (5/3) – exempt tax return purchase of residential property 2 000 000 RR for several objects + interest on 1 mortgage loan up to 3 000 000 RR tax return agent actual expenses IE civil-law contracts, author agreements fixed IE, author agreements, 20 %- 40% tax return agent period of ownership listed securities, open PIFs owned > 3 years 3 000 000 RR * Ks tax return agent investment to ind inv account up to 400 000 RR per year, > 3 years tax return income on ind inv account Financial result , > 3 years agent Professional Investment 1 400/ 3 000 RR up to 350 000 RR Все права защищены. «Эрнст энд Янг» Standard child deduction 1 400 RR per 1st & 2nd child 3 000 RR per 3rd & next child up to 350 000 RR My tax plan: Submit written request on deduction to employer to both parents for each child under 18 y.o. (under 24 y.o. for qualifying students) ► Granted at written request to employer at only one place of employment ► To individual entrepreneurs based on the average monthly income ► No standard allowance under civil agreement at source (possible on submission the annual tax declaration) ► Increased amounts of standard & children allowances Все права защищены. «Эрнст энд Янг» art. 218 Social deductions Charity in cash 25 % ► ► ► Own education, brother’s / sister’s education medical, life insurance (>5years), pension – own & close relatives 120 000 RR Educational 50 000 RR per child Unused social deductions are not carried forward Applicable only to income taxed at 13 % Granted upon submission of the annual tax declaration ► Taxpayer is allowed to claim social deduction related to pension (additional payments for accumulative part of pension, contributions to non-state pension fund, pension insurance) & life insurance at employer before the end of the tax period provided that expenses are documentary proved and if employer withheld such payments from the salary and remitted to State Pension Fund art.219 Все права защищены. «Эрнст энд Янг» Educational deduction On own education & on brother’s/sister’s education (up to 120 000 RR) incl. evening courses ► ► My tax plan: ??? Pay for sister’s design classes Pay for own English courses Pay for son’s computer classes Все права защищены. «Эрнст энд Янг» ► ► On children’s education (up to 50 000 RR per one child) & ► ► ► ALSO for evening courses One deduction for both parents Children under 24 years old Only in licensed educational institutions Granted in the amount of expenses Must be supported by confirming documents (incl. license) Granted upon submission of the annual tax declaration YES ??? NO CLAIM DEDUCTION Check license !!! Keep documents !!! Budget: 120 000 RR + 50 000 RR Pay for niece’s MBA Pay for wife’s cooking classes Pay for mother’s knitting classes Better to give cash for their own payment, so that they can claim deduction Medical deduction ► ► ► ► ► On own medical treatment & insurance On medical treatment of spouse, parents, children under 18 y.o. Only medical treatment approved by the government Total amount is limited up to 120 000 RR (except for certain types of expensive medical treatment) Only in licensed medical institutions of Russian Federation ► ► ► My tax plan: ??? Pay for mother’s medical treatment Buy medical insurance for wife Take son to the doctor Все права защищены. «Эрнст энд Янг» ► Granted in the amount of expenses No deduction if paid by employer Must be supported by confirming documents (incl. license) Granted upon submission of the annual tax declaration YES CLAIM DEDUCTION Check license ! Keep documents!!! Budget:120 000 RR ??? Pay for sister’s medicine or buy insurance for her Medical centre in Germany or in Russia Pay for plastic surgery NO To claim deduction : sister should pay herself, medical centre should be in Russia, medical treatment should be due to medical reasons PIT on property sale EXEMPT for PIT If owned for MORE than MINIMUM PERIOD OF OWNERSHIP: 3 years – immovable property: inherited, received as present from family member, privatised; other property 5 years – other immovable property (except mentioned above) Tax base = selling price but not less than70% of cadastral value If selling price is less than 70 % of cadastral value as at 1st of January of the year of sale, use 70 % of cadastral value as taxable income for PIT Regional authorities are allowed to decrease: ► Minimum period of ownership ► Per cent of cadastral value Все права защищены. «Эрнст энд Янг» Property deduction on property sale owned for less than minimum period of ownership: property deduction Movable (car) Immovable (old house) 250 000 RR 1 000 000 RR for all sales per tax period (year) ► ► ► ► May be substituted with actual expenses Allocation of property deduction between the owners Not applicable for individual entrepreneurs Tax agents: no obligation to withhold, BUT obligation to submit data to tax authorities My tax plan: +++ Plan sale after 3 years of purchase Все права защищены. «Эрнст энд Янг» ++ Keep documents on purchase (agreement, payment orders) ++ Compare which is beneficial: actual expenses or fixed deduction ++ Plan sale of property for different years Housing incentive deduction ► ► ► ► ► ► ► ► ► ► ► ► 13 % taxable income can be reduced by the amount invested in qualifying property (houses, apartments, rooms, cottages, parts in property, plots of land) To receive housing incentive: own actual expenses + ownership + own income Maximum - 2 000 000 RR per several objects of property Maximum of interest on mortgage loan - 3 000 000 RR (only for 1 object of qualifying property) Is granted once in a lifetime Granted at written request supported by appropriate documents confirming property acquisition (title of ownership) & related expenses Additional expenses on decorations is applicable if need for it separately stated in the main agreement (incl. design documents) Can be used for refinanced mortgage loans Parents can use housing incentive on property bought for children under 18 years old Taxpayer can claim housing incentive from several tax agents No incentive if between related parties or paid by employer Unused incentive amount is carried forward until fully utilised Все права защищены. «Эрнст энд Янг» Options for utilising the housing incentive: 1. General: at written request along with annual tax declaration 2. Special: before the end of tax period when appropriate documents are obtained: ► Written application to the tax authority for confirming right to the housing incentive at source ► Within 1 month receive confirmation from the tax authorities in the special format ► Transfer this confirmation to the employer ► Employer provides housing incentive for PIT Все права защищены. «Эрнст энд Янг» Professional deductions Civil-law agreements ► ► Copy-right agreements Expenses Expenses incurred for generating income (documentary proven on CPT pattern) or SIC accrued on business income of Individual entrepreneur Individual entrepreneurs Fixed professional deduction ► 20 % of the gross business revenue (only for registered entrepreneurs) ► Fixed professional deduction is not valid for civil-law agreement ► Fixed professional deduction for copy-right agreement is 20 – 40 %% Granted on written request to tax agent or along with the annual tax declaration ► ► Only for 13 % income Все права защищены. «Эрнст энд Янг» Investment deduction Ownership term deduction Positive result on sale/redemption of listed securities owned > 3 years: 3 000 000 RR * Ks Individual Investment Account (400 000 RR per year, > 3 years): Deduction amount Period for deduction Other taxable income How to receive deduction If individual investment account is closed before 3 years If individual investment account is closed after 3 years Все права защищены. «Эрнст энд Янг» Investment deduction on investment Investment deduction on income Investments made to individual investment account (not more than 400 000 RR) annual Positive result on operations through individual investment account Is required for deductions Through annual PIT tax return Claw back of investment deductions received + fines + PIT = 13 % of positive result on operations through individual investment account PIT = 13% of positive result on operations through individual investment account When individual investment account is closed (after 3 years) Is not required for deductions Through tax agent upon submission confirmation from tax authorities PIT = 13% of positive result on operations through individual investment account Deduction in the amount of positive result on operations through individual investment account Insurance income Insurance PREMIUMS – taxable by PIT, if employer pays for employee Insurance PAYMENTS – taxable by PIT Exempt – not taxable for PIT ► Obligatory insurance (according to legislation) ► Obligatory insurance (according to legislation) ► Insurance against harm to life & health ► ► Medical insurance (except for payments for recreation & resort facilities) Insurance payments as a result of death or compensation of harm to health or reimbursement of medical expenses ► Insurance payments under voluntary pension insurance (insurance premium paid by employee), if conditions for insurance payments are similar to state pension conditions ► Contributions made by employer on behalf of employee to non-state pension funds or under voluntary pension insurance agreements and additional payments to cumulative part of state pension (limited to 12 000 RR) Все права защищены. «Эрнст энд Янг» Insurance income Life insurance: 13 % * ( Total insurance payment received - Total contributions made increased by CB RR (at average rate) ) Insurance income on property destruction: 13 % Insurance compensation ( * received - Market value of destroyed property - Insurance contributions ) Insurance income on property damage: 13 % Insurance compensation ( * received - Actual repair expenses - Insurance ) contributions art.213 Все права защищены. «Эрнст энд Янг» Insurance income Type of insurance Classification of expense for CPT Voluntary accumulative labour pension Non-state pension insurance Deductible within 12 % of labour costs Life insurance Deductible within 6 % of labour costs (if >1 year) Personal Deductible within insurance the limit of against harm to 15 000 RR per health and death insured person Medical insurance Все права защищены. «Эрнст энд Янг» Classification of income for PIT Classification of income for IC on contributions on payments 30 % / 27,1 % >12 000 RR per year per person 13 % >12 000 RR per year per person Non-taxable Non-taxable 13 % 30 % / 27,1 % Taxable 13 % > CB RR Non-taxable (if >1 year) Non-taxable (excl. health resorts) Non-taxable Non-taxable Interest on bank deposits and Russian quoted corporate bonds in roubles Deposit (actual sum) / 365 days * Days * of the period Rate 35 % CB RR + 5% Actual Taxable ►Interest exceeding: 9% rate rate CB RR +5 % for rouble deposits 9% for currency deposits ►Bank – tax agent: withhold tax when paying interest out & remit it to the budget not later than the next day ►No rounding-up for days ►Decrease of CB RR – special rules: no taxable income if under limit at agreement date ► within 3 years after decrease ► no option of decrease in deposit rate in agreement ► Interest income on Russian quoted corporate bonds is taxable in the amount exceeding CB RR + 5% ► Все права защищены. «Эрнст энд Янг» Imputed interest income on low rate loans Loan (actual sum) / 365 * days Days * of the period 2/3 CB RR 9% 1. 2. 2. 3. 4. 5. 6. Rate Actual rate 35 % Imputed rate At the last date of each month during the loan period Calculate interest on loan using 2/3 CB RR for rouble loans 9 % for currency loans Imputed interest – Actual interest =Imputed interest income (if > 0) Include in the annual tax declaration Obligation for tax agents to calculate & withhold tax on imputed interest No rounding-up the days No imputed interest income for mortgage loans qualified for housing incentive art.212 Все права защищены. «Эрнст энд Янг» Securities & PIFs Unquoted Quoted Income (loss) = per each group: Sales proceeds Losses on quoted securities shall be carried forward for next 10 years against taxable income on quoted securities only ► Allocation of expenses PIFs For quoted securities: if loss test against weighted average market price - Expenses Purchase price ► Depositary fee ► Broker’s commission ► Exchange fee ► Registrar’s fee ► Interest at CB RR*1,1 paid on loan taken to finance purchase of listed securities ► Loss on each group shall not reduce taxable income from the other group Exempt for PIT sale of securities ► Tax base is calculated at: owned for more than 5 years: ► End of tax period - unquoted shares of RLE ► Payment to the taxpayer - quoted shares of innovative RLE ► Все права защищены. «Эрнст энд Янг» Prizes, gifts & awards NO PIT: ► Between close relatives (spouses, parents, children, grandparents, grandchildren, brothers, sisters) ► ► Individual Individual (unless statutory registration needed) Sport awards: if Olympic, official championship EXEMPT in the amount < 4 000 RR per each group in a tax period: 1. Gifts from LE (13 %) 2. Support payments (13 %) 3. Reimbursement of medical expenses prescribed (13 %) 4. Gifts & prizes in competitions & tournaments held under decisions of authorities (13 %) 5. Gifts & awards in competitions, games & other events held for advertising purposes (35 %). Все права защищены. «Эрнст энд Янг» Business travel expenses NOT subject to PIT (when supported by documents): ► Per diem allowance within statutory norms ► (for each day of business trip including travel days): Russia 700 RR ► Abroad 2 500 RR Travel costs (incl. Taxi to & from airport) Airport fees & commission charges Luggage fare Accommodation expenses (hotel) Business communication expenses ► ► ► ► ► ► Income shall be recognised at the last day of the month in which expense report is approved Все права защищены. «Эрнст энд Янг» Dividend income Tax = Share of dividends * Tax rate * (Distributable – Received ) dividends dividends 13 % Separate tax base (1) (2) (1)(2) PIT on dividends payable to Individual (tax resident): Total distributable dividends ХХ RR DO NOT INCLUDE dividends payable to FLE Less net dividends received from FLE (tax agent) (ХХ RR) DO NOT INCLUDE dividends received taxable at 0% Dividends taxable at 13 % ХХ RR PIT= 13% * Share of dividends taxable at 13% (*) ► ХХ RR Should be withhold by tax agent (paying out entity) & remitted to budget within 1 day Все права защищены. «Эрнст энд Янг» Taxpayer’s obligations Obligation on ► ► ► ► ► ► Income from non tax agents (ex. Rent of the apartment to individuals) Income from sales of personal property Income from sources outside Russia Income in-kind (if tax was not withheld) Income from gambling & lottery prizes Declaration by 30th of April the following year Payment by 15th of July the following year Tax payments before submission of tax declaration 1. Upon payment order issued by tax inspectorate to the taxpayer 2. In 2 equal installments: ► Within 30 days after receipt of payment order ► Within 30 days after the 1st installment art. 228 Все права защищены. «Эрнст энд Янг» Tax agents’ obligations art. 226 ► On a monthly basis cumulatively for 13 % rate income ► Separately for each amount taxed at different rates 2. To withhold at the moment of payment from the amount payable (not out of tax agent’s own funds) Obligation 1. To calculate tax: Payment in-kind 1. Withhold from other cash payments (up to 50 %) 2. Do not withhold BUT 3. Report within 1 month Payment to the budget At the location of taxpayer: 1. The day of the actual receipt of cash in bank 2. The day of a wire cash transfer 3. Not later than the following day in other cases of cash receipt 4. The day following the date of actual tax withholding Reporting within 1 month after the end of 1st quarter, 1st half of year, nine months annual report - until 1st of April the following year Все права защищены. «Эрнст энд Янг» Tax agent’s liability Tax offence Liability Based on Delay in tax agent’s Fine – 1 000 RR for each month (part item 1.2 article reporting on calculated or full) overdue 126 TC and withheld PIT Blockage of operations at bank item 3.2 article accounts in case of report delay for 76 TC 10 days Mistakes in tax agent’s Fine - 500 RR for false information article 126.1 reporting on calculated submitted for each document TC and withheld PIT Все права защищены. «Эрнст энд Янг» Business income ► ► ► ► Business income of registered individual entrepreneurs Business income of private notaries & other private practice in accordance with the law May be decreased by allowable professional tax deduction Loss cannot be carried forward. Все права защищены. «Эрнст энд Янг» PIT reporting for individual entrepreneurs Tax declaration must be submitted (by 30 th of April of the following year) by: 1. Individual Entrepreneurs, conducting business activities 2. Individuals, engaged in private practice (private notaries) 3. Individuals receiving income from non tax agents or income free of tax withholding 4. Individuals receiving income from abroad ► Preliminary declaration on estimates business income: Issued by individual entrepreneurs & private practitioners Within 1 month & 5 days after first income Payment orders issued by tax inspectorate ► Amended preliminary declaration if considerable (>50 %) change in estimated income ► On termination business individual entrepreneur is to submit final tax declaration (within 5 days) ► ► Все права защищены. «Эрнст энд Янг» Payment obligations for individual entrepreneurs art. 227 ► ► ► ► Must make advance payments Based on estimated income Per a preliminary tax declaration According to payment orders issued by tax inspectorate Amounts 50 % 25 % 25 % final Все права защищены. «Эрнст энд Янг» & by Deadlines 15th July of the current year 15th October of the current year 15th January of the next year 15th July of the following year PIT proforma Income taxed at 13 % Employment income Income from business activities Income from sale of property Other income taxed at 13 % Total income taxed at 13 % Deductions & allowances Standard personal deduction Standard dependant deduction Business expenses Social deduction Professional deductions Property deduction Housing incentive Other deductions/allowances Total deductions & allowances Taxable income subject to 13 % Tax at 13 % Dividend income Tax on dividends at 13% Income taxed at 35 % Tax at 35 % Total tax liability Less: tax withheld (including tax on dividends) Additional tax payment (refund) required Все права защищены. «Эрнст энд Янг» Amount Amount Insurance Contributions Insurance Contributions NEW ►Threshold limit for tax rates for Insurance Contributions shall be: - 1 150 000 RR for Contributions to Pension Fund - 865 000 RR for Contributions to Social Security Fund - none for Contributions to Medical Insurance Fund (article 426 TC, Act of Government RF # 1426 dd 28.11.2018) ►Payers of IC making payments to individuals shall use: - 22 % IC rate for contributions to Pension Fund under 1 150 000 RR - 10 % IC rate for contributions to Pension Fund over 1 150 000 RR - 2.9 % IC rate for contributions to Social Security Fund under 865 000 RR - 5.1 % IC rate for contributions to Medical Insurance Fund (article 426 TC) Все права защищены. «Эрнст энд Янг» Insurance Contributions Taxpayers Tax base Tax period Legal entities Individual entrepreneurs Taxable payments to individuals Calendar years Object of taxation Payments to individuals Tax rate IC Pension fund: 22% / 10% Social security fund: 2.9% (not for civil-law & copyright) Medical Insurance: 5.1% Payment Reporting Tax calculation Monthly: +15 days Quarterly: +30 days Pension fund: 1 150 000 * 22% + (>1 150 000)*10% Social security fund: (<865 000)*2.9% Medical insurance: without limit *5.1% Все права защищены. «Эрнст энд Янг» Taxable & exempt income Tax exempt: Taxable: payments and remunerations to employees in cash and in kind. ALSO: Non-deductible for CPT ►Assistance payments required by law ► Compensation paid under legislation ► Mandatory insurance contributions Voluntary personal medical insurance of employees (> 1 year or against the death or health damage) ► ► Value of uniforms and outfits ► Financial aid (less 4 000 RR) ► Business trip expenses (within limits) ► Education compensation ► Compensation of mortgage loans ► Tax base - cumulatively for the tax period for each employee separately. ► Tax base – separately for each employer (LE) Все права защищены. «Эрнст энд Янг» Reporting & payment procedures Declaration 30th of month following the quarter Additional calculations/files to: Pension Fund: by 15th of the following month (annual – up to 1st March) Federal Social Fund: by 25th of month following the quarter Payments Monthly advance & final annual payment: by 15th of the following month Separate subdivisions (balance and a separate bank account) : ► Payment & reporting at the location of subdivision Все права защищены. «Эрнст энд Янг» Civil-law & Copy-right agreement Civil-law agreement Taxpayers - legal entities and individual entrepreneurs in relation to payments under civil-law agreements: RR Remuneration under copy-right agreement XX less Actual expenses (XX) Tax base (threshold limit 1 150 000 RR) XX Tax at (22%+5.1%) % / (10%+5.1%) XX Copy-right agreement Taxpayers - legal entities and individual entrepreneurs in relation to copy-rights payments: RR Remuneration under copy-right agreement XX less Actual expenses or fixed professional deduction (XX) Tax base (threshold limit 1 150 000 RR) XX Tax at (22%+5.1%) % / (10%+5.1%) XX Все права защищены. «Эрнст энд Янг» Examination answer format Taxpayers – legal entities and individual entrepreneurs in relation to payments to employees: Gross remuneration payable to physical persons in cash Gross remuneration payable to physical persons in kind Tax base Tax to: Pension Fund (threshold limit 1 150 000 RR) 22% / 10% Social Securiy Fund (limit 865 000 RR) 2.9% Medical insurance (no limit) 5.1% Taxpayers - legal entities and individual entrepreneurs in relation to copy-rights payments & civil-law agreements: Remuneration under copy-right/civil-law agreement less Actual expenses or fixed professional deduction Tax base Tax to: Pension Fund (threshold limit 1 150 000 RR) 22% / 10% Medical insurance (no limit) 5.1% Все права защищены. «Эрнст энд Янг» RR XX XX RR XX XX RR XX (XX) RR XX XX Corporate Property Tax Corporate Property Tax NEW ► ► ► Movable property shall not be taxable with Property tax (item 2 article 374 TC) Taxable base in the amount of cadastral value of immovable property can be changed during the tax period in case property’s attributes or cadastral value are changed (item 15 article 378.2 TC) Taxable base in the amount of cadastral value can be changed for the previous years in case of mistakes recovered or according to court decision (item 15 article 378.2 TC) Corporate Property Tax Taxpayers Tax base Tax period Legal entities Net balance value Cadastral value Calendar year Object of taxation Immovable property Tax rate PT Maximum 2.2 % (NBV) 1.6 % (Cadastral) Payment Reporting Tax calculation Quarterly: + 30 days till 30th March the following year Average value * 2.2% Cadastral value * 1.6% Все права защищены. «Эрнст энд Янг» Reporting & payment procedures Object of taxation: BUT NOT: Immovable property ► Land & natural resources ► Objects of cultural heritage Corporate property tax is paid at the location of: ► Legal Entity (Russian or Foreign via permanent establishment) ► Separate subdivision (balance and a separate bank account) ► Immovable property Declaration Annual tax return: by 30th of March the following year Payments Quarterly advance payment: by 30th of the following month Final annual payment: by 30th of March the following year Все права защищены. «Эрнст энд Янг» Average property value (old rules) 1. Add NBV of FA (accounting) as at the 1sts of months: Q1 – January, February, March, April Q2 – January, February, March, April, May, June, July Q3 – January, February, March, April, May, June, July, August, September, October Q4 – January, February, March, April, May, June, July, August, September, October, November, December + 31st of December 2. Divide by the number of months Quarterly advance payment: Average property value * ¼ * 2.2 % Annual tax = Average property value * 2.2 % Annual tax liability= Annual tax – Quarterly advance payments Все права защищены. «Эрнст энд Янг» Cadastral value (new rules) ► Tax base of the certain immovable property shall be recognized as cadastral value: ►Business centers; ►Shopping centers; ►Business premises intended for offices, shops, dining and services ►Premises belonging to foreign companies without permanent office in Russia. ► Tax base defined as cadastral value shall be excluded from calculation of average property value ► Cadastral value shall be fixed as at 1 January: ►At Federal State Registration official site: https://rosreestr.ru/wps/portal/ Exam rate: ►At official site of Region of Russian Federation; 1.6 % ►In the Tax Authorities office at the location of immovable property. ► Cadastral value shall be defined for each Region Tax period object of property separately 2014 2015 2016 and ► Cadastral value of premises shall be equal after it’s share in the building ► If cadastral value is not defined as at 1 Moscow 1,5 % 1,7 % 2% January, old rules shall be applied Other regions 1% 1,5 % 2% Quarterly advance payment: Cadastral value as at 1 January * ¼ * tax rate % * number of months of ownership Annual tax = Cadastral value as at 1 January * tax rate % * number of months of ownership Annual tax liability= Annual tax – Quarterly advance payments Все права защищены. «Эрнст энд Янг» Tax Planning, Administration & Control Tax Administration and Control NEW Late payment interest shall be increased in case payment is delayed for more than 30 days and is calculated using 1/150 of Central Bank Refinancing Rate per each day of delay (item 4 article 75 TC); ► The total amount of late payment interest shall not exceed the amount of delayed payment (item 3 article 75 TC); ►Taxpayer can decrease tax base or tax amount provided that: ► Legal entity has not misstated tax and accounting reports and presented correctly all deals and objects of taxation ► Counterpart has fulfilled its part of the deal (article 54.1 TC). ► Все права защищены. «Эрнст энд Янг» MINIMISATION OF TAXES vs DELIBERATE TAX EVASION Taxpayer has right to pay minimum of tax established by law Tax optimisation Tax evasion minimization of tax liabilities by considerable legal actions of taxpayer which means utilization of all preferences and allowances, tax deductions and other legal options and in general eliminate or minimize unreasonable overpayment of taxes and tax penalties deliberate actions of taxpayer to violate law in order to minimize taxes payable or to completely avoid tax payments, which is actually tax offence or even tax crime Example: - contract planning: choice of type of agreement, of legal entity, terms of agreement - choice of region of company’s location / registration - legal structure of business Example: - sham transactions - deals with suspicious parties - lack of economic benefit (business purpose) Business purpose in taxpayer’s operations Minimisation of tax payments substitutes business purpose in taxpayer’s operations Все права защищены. «Эрнст энд Янг» Tax Planning – Focus on exam TARGET Maximize tax deductions CPT - 10 % (30 %) write off Minimize tax paid Choice of option between - maximum deductible expenses activities of IE or incorporated business PIT - standard deductions - social deductions Choice between options - housing incentive with different level of - professional deductions deductible expenses Все права защищены. «Эрнст энд Янг» Tax Penalties TAX VIOLATIONS Chapter 16 TC 1. Breach of tax registration rules – deadline for submission of registration application & business activities without registration 2. Non-submission of tax return – breach of deadline and method of submission of tax return (calculation) 3. Serious violation of tax accounting rules for income, expenses and tax objects 4. Non-payment or underpayment of taxes, also in controlled transactions by using non-market prices 5. Neglect of tax agent’s duties on withholding & remitting taxes. Все права защищены. «Эрнст энд Янг» Breach of tax registration rules art. 116 TC Tax offence Breach of terms for submission of registration application to tax authorities conducting business activities without tax registration Все права защищены. «Эрнст энд Янг» Tax penalty 10 000 RR 10 % of income earned during the period (not less 40 000 RR) Breach of tax audit rules art. 126 TC Tax offence Non-submission of documents and/or other information within the established period Tax penalty 200 RR for each nonsubmitted document Tax agent’s provision of documents 500 RR containing false information for each document with false information Non-provision of information about a taxpayer or provision of documents containing false 10 000 RR information Все права защищены. «Эрнст энд Янг» Breach of deadlines for tax payment art. 122, 123 TC Tax offence Understating the tax base and incorrect calculation resulted in understatement of tax paid, if discovered by the tax authorities during on-site audit. the same committed intentionally failure of tax agent to fulfill the duty of withholding and/or remitting taxes Late payment interest: Tax penalty 20 % of unpaid liability 40 % of unpaid liability 20 % of the amount that was subject to withholding and remittance art. 75 TC First 30 days: unpaid tax liability * 1/300 of CB RR * days of delay From 31st day on: unpaid tax liability * 1/150 of CB RR * days of delay Все права защищены. «Эрнст энд Янг» Breach of deadlines for tax reporting art. 119 TC Tax offence Failure to submit tax return to tax authorities within the deadline Tax penalty 5 % of tax payable as per tax return per each month (not more 30 % of tax amount, not less than 1 000 RR) failure to submit tax agent’s report 1 000 RR for each month on PIT calculated and withheld (part or full) Breach of the procedure for electronic submission of tax return (calculation) Все права защищены. «Эрнст энд Янг» 200 RR Breach of tax accounting rules Tax offence Serious violation of tax accounting rules which didn’t result into any decrease of a tax base, took place in one tax period Serious violation of tax accounting rules which didn’t result into any decrease of a tax base, took place in several tax periods Serious violation of tax accounting rules which resulted into the decrease of a tax base Tax penalty 10 000 RR 30 000 RR 20 % of tax underpaid (not less than 40 000 RR) Serious violation of tax accounting rules: - lack of supporting document - systematic undue and incorrect booking of operations Все права защищены. «Эрнст энд Янг» Breach of transfer pricing rules Tax offence Tax penalty Understatement of tax due to use of prices outside the market range 40 % of tax underpaid (but not less than 30 TRR) Non-submission or late submission of notification on controlled transactions or incorrect information 5 000 RR Все права защищены. «Эрнст энд Янг» Procedures for Tax Enforcement art. 45, 46, 47,48 TC If taxpayer failed to pay tax within deadline tax collection shall be enforced: - for legal entities and individual entrepreneurs – out of court - for individuals – in court Out of court tax collection – By cash at taxpayer’s bank accounts: 1. Tax authorities: issue tax payment demand 2. After expiration of payment term stated in tax payment demand (not later than 2 months): enforced collection (collection order to bank) 3. Otherwise: appeal to court within 6 months after expiration of payment term stated in tax payment demand 4. Besides, securing collection – blocking the accounts in the taxpayer’s banks Out of court tax collection – By other taxpayer’s assets: In case there is no cash in taxpayer’s bank accounts or information on it in tax authorities: 1. Tax authorities shall decide on tax collection by taxpayer’s assets (not later than 1 year after expiration of payment term in tax payment demand) – decision on tax collection by other assets is submitted to court bailiff for seizure of assets 2. Otherwise, appeal to court within 2 years after expiration of payment term in tax payment demand. Все права защищены. «Эрнст энд Янг» Refund & offset procedure art. 78, 79 TC Refund & offset procedures are done: 1. Upon written application of a taxpayer 2. Within 3 years form the day tax overpayment or tax collection Offset procedure: 1. Decision of tax authorities shall be issued within 10 days after application from taxpayer 2. Is performed for taxes paid to the same budget Refund procedure: 1. Decision of tax authorities - within 10 days after application from taxpayer 2. Refund is done after offset of all outstanding tax liabilities 3. Refund must be done within 1 month after application from taxpayer If this deadline is not met by tax authorities - interest for each day of delay in the refund at CBRR payable from the budget to the taxpayer. Все права защищены. «Эрнст энд Янг» INTEREST payable TO TAXPAYER for undue release of BLOCKED ACCOUNTS of taxpayer it.9.2. art 76 TC Blockage of taxpayer’s bank accounts shall be performed in case of: 1. Taxpayer doesn’t settle tax payment demand on overdue taxes, penalties, fines 2. Taxpayer doesn’t submit tax return within deadlines 3. As security during in-house/on site tax audit 4. Breach of deadlines for submission of receipt on documents from tax authorities The decision of tax authorities is base for: - Blockage of taxpayer’s bank accounts - Release of blocked bank accounts of taxpayer – shall be issued and send to bank on the day following the date of remedy of tax violation If decision on release of blocked accounts is not issued within the due term or in case of illegal blockage of taxpayer's bank accounts: ► taxpayer shall receive interest on the amount which is illegally blocked ► for each day of overdue blockage ► at current CB RR. Все права защищены. «Эрнст энд Янг» Tax Audits Tax audits of branches & subdivisions ► ► All types of tax audits are possible, BUT ONLY: ► for branches & representative offices ► in relation to regional & local taxes In-house tax audit of subdivisions: only in relation of taxes reported by subdivision ► ► On-site tax audit of subdivisions: ► separate tax audit of subdivision ► as part of tax audit of legal entity Decisions & acts related to audits of subdivisions: addressed/handed in at location of legal entity (head office) Terms of on-site tax audit can be prolonged if LE has subdivisions: Number Term of audit < 4 subdivisions > 4 subdivisions > 10 Subdivisions Все права защищены. «Эрнст энд Янг» Conditions If subdivisions have >50% taxes & >50% assets up to 4 months up to 6 months In all cases In-house tax audits art. 88 TC ► At the location of tax authorities ► On the basis of tax declarations ► On the basis of other documents concerning the taxpayer’s activities ► Within 3 months (2 months – for VAT) starting from the day submission of tax declaration (amended tax declaration) ► In case of errors revealed the tax payer shall be notified and requested to make appropriate corrections within the established time limit ► Additional tax paid under demands of tax authorities ► No penalty for tax underpayment ► Late payment interest at 1/300 (1/150) of CB RR for each day of delay ► Act on the in-house audit is issued within 10 days after it is finished ► Taxpayer is allowed to present explanations on the results of in-house tax audit within 1 month after the act on in-house tax audit and these explanations are to be studied Все права защищены. «Эрнст энд Янг» On site tax audits art. 89 TC ► May not exceed 2 months ► Increased up to 4 months ► In exceptional cases - up to 6 months ► + 1 month per each branch and representative office ► The tax audit report must indicate document-supported tax offences which were revealed or the absence of such violations and the conclusions and the recommendations of the inspectors and references to the articles of the TC ► Consequent on-site tax audit can be performed upon submission of amended tax return if the tax liability has been decreased ► Report on the tax audit can be send to the taxpayer by mail only in the case the taxpayer avoids it. Все права защищены. «Эрнст энд Янг» Transfer pricing – tax audit ► Performed by special tax authorities departments ► Based on notifications from taxpayers within a new form of tax audits & on information received during in-house and on site tax audits ► Tax control of amounts of CPT, MET and PIT and VAT as a result of controlled deals ► Period of audit is limited to 6 months to be performed within 2 years after the information on controlled deals received ► “Corresponding adjustments” are allowed for additional tax assessments as a result of a transfer pricing tax audit. Все права защищены. «Эрнст энд Янг» During on site tax audits Actions that may be carried by tax authorities during the tax audits: ► Perform an inventory of the taxpayers assets and examine the production, storage, trading and other premises used by a taxpayer ► Witnessed may be summoned (except for taxpayer’s auditor and legal adviser) ► Provision of additional documents may be requested ► Documents and other objects may be seized ► Experts, interpreters and external specialists may be recruited to perform audit. Все права защищены. «Эрнст энд Янг» Documents on site tax audits art. 100, 101 TC Actions and procedures to be carried after the tax audits: ► Immediately after the end of the tax audit tax authorities shall issue a certificate on audit having been performed ► Tax authorities shall issue audit act not later than 2 months after the certificate is issued or within 10 days if tax violations are revealed ► Audit act shall be handled to the taxpayer within 5 days after it is issued ► A taxpayer has right to prepare and submit to tax authorities written objections to tax audit act within 1 month after the act is received by the taxpayer. ► Tax authority shall consider taxpayer’s objections within10 days after receipt of taxpayer’s objections and taxpayer has right to attend the hearing ► Report on the audit is issued by tax authorities after the consideration of taxpayer\s objections. This report may provide for penalties imposed on the taxpayer, no penalties and additional measures of tax control to be taken ► Demand for payment is issued along with the report on the audit in relation to unpaid tax, penalties and late interest payment ► Decision of tax authorities on on-site audit come into effect within 1 month after being handled to the taxpayer. Все права защищены. «Эрнст энд Янг» Cancellation of results of on-site tax audit it. 12, art. 101.4 TC Decision on cancellation tax authority’s acts is made by higher tax authority or by court. Reason for cancellation of tax authority’s acts can be: ► ► ► Neglect of tax authorities of TC requirements Neglect of essential terms of consideration of acts and other materials of tax control: ► taxpayer was not invited to hearing ► taxpayer was not allowed to present its objections Other violations of consideration of materials of tax audit if such violations resulted or could result in wrong decisions. Все права защищены. «Эрнст энд Янг» Repeated tax audits art. 89 TC Limitation on tax audits: Can be performed only for the three calendar years immediately preceding the year of the audit ► No repeated on-site tax audits are allowed for the same taxes for the same tax period with the exception to: ► ► Audit during re-organisation or liquidation of a taxpayer ► Audit by a higher tax authority in the processes of control check More than 2 on-site tax audits are not allowed for one taxpayer (except for tax audit on special decision of head of tax authority). ► Все права защищены. «Эрнст энд Янг» Appealing against the acts and decisions of art. 137-139 TC tax authorities Every taxpayer or tax agent shall have right to appeal against ► Acts of tax authorities of a non-normative nature and ► Actions or inaction of their officials if taxpayer thinks that his rights were violated Appealing procedure: 1. Before act of tax authorities comes into effect – appeal petition to higher tax authority 2. After act of tax authorities came into effect – appeal to higher tax authority: - within 1 year after taxpayer has revealed that his rights were violated after appeal petition and decision of higher tax authority came into effect, tax payer shall not have right to repeat appeal for the same reasons, but appeal can be made to the Federal Tax Authority - 3. After pre-court decision – appeal to Arbitration Court (for legal entities) and to General jurisdiction court (for individuals) -within 3 months after taxpayer was informed on higher tax authority’s decision. Все права защищены. «Эрнст энд Янг» Appeal petition on acts and decisions of tax art. 138 TC authorities 1. A taxpayer shall appeal in writing to the higher tax authority within 1 month after he discovered that his rights were violated or he received act he wants to appeal 2. Appeal petition is submitted to higher tax authority trough tax authority which issued appealed act 3. Effective date of appealed act can be postponed for the period of appeal procedures 4. The appeal of a taxpayer shall be considered by the higher tax authority not later than 1 month after the day when it was received. 5. After considering the appeal tax authorities shall have right to: ► Reject the appeal ► Annul the tax authority’s act and order a further audit ► Annul the tax authority’s act an terminate the tax offence case ► Amend a decision or adopt a new decision. 6. The decision shall be made know with the taxpayer within 3 days after it has been adopted. Все права защищены. «Эрнст энд Янг» Tax Monitoring for big LE Form of tax control: (based on LE appeal): method of comprehensive information exchange (based on special regulations): ≥300 mln RR of taxes - on-line access to accounting & tax data ≥ 3 bln RR of income - similar to in-house tax audit ≥ 3 bln RR of assets Reasoned tax opinion: Advantages: document, stating opinion of tax authorities whether taxes are correctly calculated, in full amount, and timely paid (also issued on request of taxpayer) - solve tax disputes - avoid additional tax assessment, fines, late payment interest - no tax audits Pre-court resolution procedure at Federal Tax Authority level Все права защищены. «Эрнст энд Янг» Revision Exam Success Factors: Practice ALL past papers ► Follow the layout of the model answers ► Attempt all parts of the questions ► AND MOST IMPORTANT OF ALL: Work through exam standard questions under exam conditions Все права защищены. «Эрнст энд Янг» Feedback from the examiner ► Review of past papers performance ► Lessons learned Do not rely on typical questions Q5 & Q6 Section B ► Focus on VAT (Q4 Section B) ► ► How to improve Gain easy marks ► Focus on all parts of the question ► Structure the answer through workings ► Show the logic of answer if no time for calculations ► Все права защищены. «Эрнст энд Янг» 10 things to review 5 minutes before exam 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. Все права защищены. «Эрнст энд Янг»