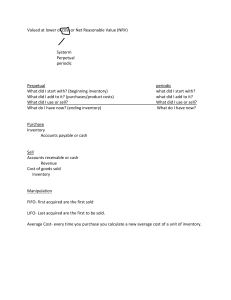

Section 10 - Inventory Control What is Stock Valuation? This is the assignment of a value to stock, usually stock on hand at the end [ closing inventory] of a financial period. Why is Stock Valuation necessary? In order to prepare financial statements a value is required for the closing stock. *Income Statement requires a figure for closing stock to calculate Cost of Goods Sold and Balance sheet requires a figure for closing stock to calculate total current assets How is stock valued? Three methods available to value stock are : 1. First In, First out (FIFO) 2. Last In, First Out (LIFO) 3. Average Cost (AVCO) Concept of perpetual and periodic stock valuation Perpetual inventory system and periodic inventory systems are the two systems of keeping records of inventory. In perpetual inventory system, merchandise inventory and cost of goods sold are updated continuously on each sale and purchase transaction. In periodic inventory system, merchandise inventory and cost of goods sold are not updated continuously. Instead this is done at the end of a financial period. A worked example The following table show the stock received and issued by Company ABC along with the relevant dates. 650 units were sold on November 30, 2011. What is the value of the 100 units on hand at December 31, 2011 using FIFO, LIFO and AVCO? DATE 2011 DATAILS UNITS COST $ TOTAL COST $ Jan 01 Opening Stock 100 20 2000 Apr 15 150 21 3150 Aug 24 200 22 4400 Nov 27 300 23 6900