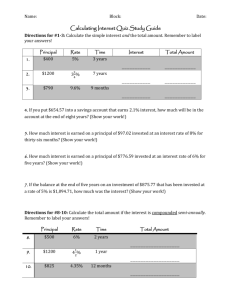

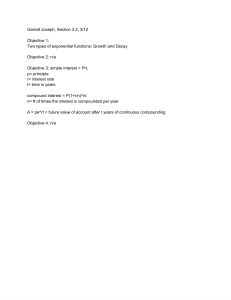

BASIC LONG-TERM FINANCIAL CONCEPTS “A peso today is worth more than a peso tomorrow”. Identifying the a) principal, b) interest rate, and time period in the examples below. 1. Your mother invested P 18 000 in government securities that yields 6% annually for two years. 2. Your sister placed her graduation gifts amounting to P 25 000 in a special savings account that provides an interest of 2% for 8 months. 3. Your brother borrowed from your neighbor P 7 000 to buy a new mobile phone. The neighbor charged 11% for the borrowed amount payable after three years. 4. You deposited P 5 000 from the savings of your daily allowance in a time deposit account with your savings bank at a rate of 15% per annum. This will mature in 6 months. Interest • In general business terms, interest is defined as the cost of using money over time. This definition is in close agreement with the definition used by economists, who prefer to say that interest represents the time value of money. • is the excess of resources (usually cash) received or paid over the amount of resources loaned or borrowed which is called the principal SIMPLE INTEREST • is the product of the principal amount multiplied by the period’s interest rate (a one-year rate in standard). 𝐈=𝐏×𝐑×𝐓 where: I = interest P = Principal R = Interest rate T = Time period Example 1: You invested P 10 000 for 3 years at 9% and the proceeds from the investment will be collected at the end of 3 years. Using a simple interest assumption, the calculation will be as follows: COMPOUND INTEREST • is the interest paid on both the principal and the amount of interest accumulated in prior periods. FV= 𝑷(𝟏 + 𝒊)𝒏 • where: FV = Future Value P = Principal i = Interest rate per compound interest period or periodic rate n = Time period or number of compound interest periods Subtract the principal from the future value to get the compound interest. Hence, Ic= FV – P. • Example 2: Using example 1 where you invested P 10 000 for 3 years at 9% and the proceeds from the investment will be collected at the end of 3 years, compound interest will be computed as follows: FUTURE VALUE OF MONEY • is the value of the present value after n time periods. • To account for time value for single lump-sum payment, we use the same formula provided for under compound interest rates FV= 𝑷𝑽(𝟏 + 𝒊)𝒏 where, PV = Present Value (𝟏 + 𝒊)𝒏 = Future value interest factor (FVIF)* • Example 3: Using the formula, find the future values of P 1 000 compounded at a 10% annual interest at the end of one year, two years and five years. • Example 4: Determine the compound amount on an investment at the end of 2 years if P 20 000 is deposited at 4% compounded a) semiannually and b) quarterly. PRESENT VALUE OF MONEY • To get the present value of a lump-sum amount, PV= 𝑭𝑽(𝟏 + 𝒊)𝒏 • where, (𝟏 + 𝒊)𝒏 = Present value interest factor (PVIF)* or discount factor EVALUATION 1. Lisa receives an amount of P 20 000 deposited in her account on her 18th birthday. If the bank pays 6% interest monthly and no withdrawals are made, how much should be credited in her account on his 21 st birthday? 2. James borrows P 5 000 with interest at 15% quarterly. How much should he pay at the end of 2 years and 6 months to settle her debt? 3. Mr. Santos invested P 15 000 in an account for each of his children. The accounts paid 8% compounded semi-annually. Determine the balance of each account for the following: a. The youngest child withdrew the balance after 5 years for college b. The second child withdrew the balance after 8 years to buy a car c. The third child withdrew the balance after 10 years to travel 4. A man wishes to accumulate P 10 000 in 2 years, how much should he invest now at 15% compounded semi-annually? What is the present worth of P 5 000 for 2 years at 12% compounded quarterly? 5. ANNUITIES • An installment that requires a buyer to pay equal payments at a certain period illustrates an annuity – a series of equal cash flow – payments in this case for a specific number of periods. • If payment is made and interest is computed at the end of each payment interval, then it is called ordinary annuity. • To get the present value interest factor for an ordinary annuity (FVIFA) use the formula below: • • Where, R = regular payment • To get the future value of an ordinary annuity, use this formula: • Example 6: • What lump sum would have to be invested at 6% compounded annually to provide an ordinary annuity of P 10 000 per year for 4 years? • If the cash flow happens at the beginning of each period, then it is called a annuity due. The formulas to use are shown below: • Example 7: If a supplier would allow you to pay P 50 000 annually at 10% for 3 years with the first payment due immediately, how much would be the present value and the future value? • If the cash flow stream lasts forever or is indefinite, then it is called a perpetuity. The formula for present value of a perpetuity is simply LOAN AMORTIZATION • refers to the amount of principal and interest paid each month over the course of your loan term. • For some corporate long-term loans, principal payment is fixed, and the interest expense is adjusted based on the declining principal balance. • Example 8: On July 1, 2015, DD Company borrowed P 3 million from ASC Bank at the rate of 10% a year. The loan is paid at the rate of P 500 000 every December 31 and June 30 until the full amount is paid. Below is an amortization table for the loan. • To compute for the interest expense from June 30 to December 31, 2015: Interest = 3 000 000 x 10% x (6 /12) = 150 000 • To compute for the equal regular payment, use the formula in annuity • Example 9: You borrowed P 50 000 from a bank to buy a mobile phone. Assuming you need to repay the loan by equal payments at the end of every 6 months for 3 years at 10% interest compounded semi-annually. What is your periodic payment? NET PRESENT VALUE METHOD • to determine whether a project should be accepted or rejected by a company. • The basic decision rule is to accept the project if the net present value is positive and reject if it is negative. • The basic formula is: NPV = PV of Inflows – PV of Outflows or NPV = PV of Future Cash Flows – Initial Investment • Example 10: A company wants to purchase an equipment that will cost P 100 000 and estimated to be used for 5 years. Operating cash inflows from the use of equipment would be P 50 000 while annual operating cash outflows (due to repairs and maintenance) are estimated at P 10 000. Compute for the NPV. RISK-RETURN TRADE-OFF • In finance, we assume that individuals are risk averse but have different levels of risk aversion. • Risk aversion means that individuals maximize returns for a given level of risk or minimize risk if the returns are the same. Riskaverse individuals would require a higher return if the risk level increases. • In general, the riskier the investment, the higher the potential return should be, indicating a direct relationship between risk and potential return. As a business owner you should know to balance the risk and the potential return of your investments. • Risk is defined here as the uncertainty of returns. One way to reduce risk to an acceptable level is through diversification wherein you invest in different types of investments with different risks and returns. This is an application of the saying: • “ Don’t put all your eggs in one basket.”