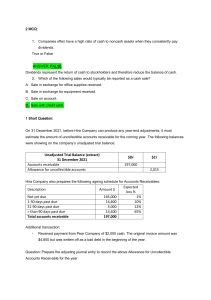

BHMH2101 Financial Accounting Reinforcement exercise – Chapter 7(2) Part A 1. The Allowance for Impairment will appear on the __________. A. Income statement B. Statement of Financial Position C. Cash flow statement D. Statement of Changes in Equity 2. Uncollectible accounts expense: A. Should not occur if the credit department properly investigates prospective customers who wish to purchase merchandise on credit. B. Is the amount of cash a business must pay each time a credit customer fails to pay his or her account. C. Is the amount a business must pay to a collection agency to recover amounts on overdue accounts receivable. D. Represents the loss in value of accounts receivable that are estimated to be uncollectible. 3. The Allowance for Impairment represents: A. Cash set aside to make up for bad debt losses. B. The amount of uncollectible accounts written off to date. C. The difference between total credit sales and collections on credit sales. D. The difference between the face value of accounts receivable and the estimated collectible amount of accounts receivable. 4. At December 31, before adjusting and closing the accounts had occurred, the Allowance for Impairment of Seaboard Corporation showed a debit balance of $3,200. An aging of the accounts receivable indicated the amount probably uncollectible to be $2,100. Under these circumstances, a year-end adjusting entry for Impairment Loss of Receivables would include a: A. Debit to the Allowance for Impairment for $1,100. B. Credit to the Allowance for Impairment for $1,100. C. Debit to Uncollectible Accounts Expense of $2,100. D. Debit to Uncollectible Accounts Expense of $5,300. Semester 1 2019-20 Page 1 5. Oceanside Company uses the Statement of Financial Position approach in estimating uncollectible accounts expense. It has just completed an aging analysis of accounts receivable at December 31, 201Y. This analysis disclosed the following information: What is the appropriate balance for Oceanside's Allowance for Impairment at December 31, 201Y A. $95,000. B. 2% of credit sales in 201Y. C. $1,560. D. $2,160. Part B Question 1 At the end of the year, 31 December 201X, the unadjusted trial balance of Angel Company included the following accounts: Debit Sales (80% represent credit sales) Accounts Receivable Allowance for Impairment Credit $780,575 $101,475 $1,218 (a) (i) If Angel Company uses the Statement of Financial Position Approach to estimate uncollectible accounts, and aging the accounts receivable indicates the estimated uncollectible portion to be $6,075, what will the Impairment Loss of Receivable for the year be? _________________________________ (ii)Show the adjusting entry at year-end to record the Impairment Loss of Receivable for the year. Debit $ Semester 1 2019-20 Credit $ Page 2 (iii) Compute the estimated collectible amount of accounts receivable. _________________________________________ (iv)The Accounts Receivable presented in the Angel Company’s Statement of Financial Position at 12/31/201X would be: (b) (i) If Angel Company uses income statement approach to estimating the uncollectible accounts, and the estimated uncollectible is to be 1% of net credit sales, what is the amount of the Impairment Loss of Receivable for the year? ___________________________________________________________ (ii) Show the adjusting entry at year-end to record the Impairment Loss of Receivable for the year. Debit $ Credit $ Question 2 (past paper) On 1 November, 2016, Eastern Company wrote off an account receivable of HK$10,300 as worthless because of the bankruptcy of the client, Western Company. However, this amount was subsequently collected in full on 3 December, 2016. Required: Prepare the journal entries that Eastern Company would make upon the collection on 3 December, 2016. Semester 1 2019-20 Page 3