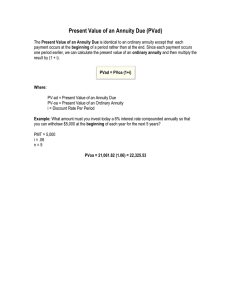

Section 2-3 FV of an Annuity; Sinking Funds Goal: To calculate future values of annuities and solve problems involving sinking funds Any sequence of payments at equal time intervals is called an annuity. To calculate the future value of an annuity: r nt 1 1 n , FV PMT r n where FV = future value ($) PMT = periodic payment ($) r = annual interest rate (as a decimal) t = time in years and n = number of payments per year (periods) If the payments into an account are in the form of an ordinary annuity and the account is established for accumulating funds to meet a future obligation, then the account is called a sinking fund. (Unless otherwise noted, round monetary answers to the nearest dollar, precents to two decimal places when written as a percentage, and time to the nearest year.) 1. Annual deposits of $2,500 are made for 15 years into an annuity that pays 6.25% compounded annually. Find 𝑖 (the rate per period) and 𝑛 (the number of periods) for each annuity. i = 0.065; n = 15 2. USG Annuity and Life offered an annuity that pays 6.95% compounded monthly. If $800 is deposited into this annuity every month, how much is in the account after 12 years? How much of this is interest? r = 0.0695 / 12 = 0.0058 PMT = 800 t = 12 n = 12 FV = 800 * ((1 + 0.0058/ 12)144 – 1) / (0.0058 / 12) = 119 273.77 Total payment = 800 * 12 * 12 = 115 200 Interest earned = 119 273.77 – 115 200 = 4 073.77 3. John wanted to save for his retirement but he procrastinates and does not make his first $1,000 deposit into an IRA until he is 36, but then he continues to deposit $1,000 each year until he is 65 (30 deposits in all). If John’s IRA also earns 6.4% compounded annually, how much is in his IRA when he makes his last deposit on his 65th birthday? PMT = 1000 t = 30 r = 0.064 FV = 1000 * ((1 + 0.064)30 – 1) / (0.064) = 84852.51