Taxation Exam: Business Management, University of Caloocan City

advertisement

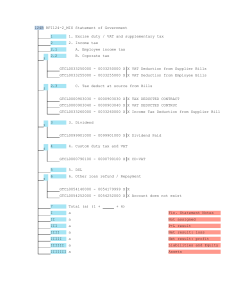

lOMoARcPSD|16874964 TAX_PRTC 1stPB with answers Business Management (University of Caloocan City) Studocu is not sponsored or endorsed by any college or university Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com) lOMoARcPSD|16874964 TAXATION First Preboard SIA/TABAG OCT 2020 Choose the letter of the correct answer. 1. The 30% corporate income tax is increased to 35% by the Congress for the purpose of raising revenue to be used for national road expansion project near Bonifacio Global City, a private corporation. Is the exercised of the taxing power unconstitutional? a. Yes, because taxing power must be exercised exclusively for public purpose without any incidental benefit to any private entity. b. No, because the it is exercised directly for public purpose and the benefit to a private entity is only incidental. c. Yes, because the increase in tax rate constitutes deprivation of right to property of corporation without due process of law for being excessive and unreasonable. d. No, because the constitution does not expressly state that the power of taxation must be used only for public purpose, thus, it may be used to benefit a private entity. 2. Which of the following statements is correct? a. The amount of sales to PWDs and SCs to be reported by a private establishment shall be the gross selling price and the applicable discount. b. The amount of discount granted to PWDs and SCs must not be reflected as a deduction from gross income of the seller but as a deduction from gross sales to arrive at the correct amount of net sales. c. The input vat attributable to sales made to PWDs and SCs shall be reflected in the income statement of the seller as a deduction from gross income d. All of the above 3. Which of the following are basic principles of a sound tax system? a. Fiscal Adequacy, economic Feasibility and Theoretical Justice. b. Fiscal Adequacy, Administrative Feasibility and Theoretical Justice. c. Progressive Taxation, Ability to Pay, Symbiotic Relationship. d. Fiscal, Deficit, administrative Feasibility and Ability to Pay. 6. Donor’s tax return for a donation on January 15, 2020 was filed on January 31, 2018. Last day to file donor’s tax return shall be? a. Jan. 15, 2020 c. Feb. 14, 2020 b. Jan. 31, 2020 d. Feb. 28, 2020 7. The Congress enacted RA7716 also known as Expanded Value Added Tax Law. An association of taxpayers questions the constitutionality of this law on the ground that RA7716 did not originate exclusively in the House of Representatives as required by the Constitution, because it is in fact the result of the consolidation of two distinct bills, one from the House of Representatives and the other from the Senate. Is the vat law unconstitutional? a. Yes, because all appropriation, revenue or tariff bills, bills authorizing increase of public debt, bills of local application, and private bills, shall originate exclusively in the House of Representatives. b. Yes, because the Senate has no authority to propose or concur any amendments with the revenue or tax bill proposed by House of Representatives. c. No, because all appropriation, revenue or tariff bills, bills authorizing increase of public debt, bills of local application, and private bills, shall be initiated by the Senate. d. No, because it is not the law but the revenue bill which is required by the constitution to originate exclusively in the House of Representatives and insisting otherwise would violate the coequality of legislative power of the two houses of Congress and in fact would make the House superior to the Senate. The next three (3) questions are based on the following data: Mr. and Mrs. Pinagpala donated the following during 2020: March 30 ▪ 4. The concept of “situs of taxation” is based on which limitation of taxation? a. Territoriality b. International comity c. Exemption of the government d. Public Purpose 5. Statement 1: The inherent powers of the State can never be taken away. Statement 2: No laws are necessary to confer the inherent powers of the State upon any government exercising sovereignty. a. Only statement 1 is correct b. Only statement 2 is correct c. Both statements are correct d. Both statements are incorrect ▪ ▪ Land valued at P620,000 to Ana, legitimate daughter, on account of marriage. Cash of P100,000 to Juan, legitimate son, for successfully passing the CPA Licensure exam Second hand car (capital property) valued at P400,000 to Mr. Pinagpala’s long-time friend, Pedro May 15 ▪ ▪ Cash of P200,000 to Melda, mother of Mrs. Pinagpala Jewelry (paraphernal property) worth P100,000 to Emma, Mrs. Pinagpala’s best friend December 25 ▪ Cash of P250,000 to Quezon City government for public use 8. The donor’s tax due on the March 30 donation should be: a. P0 for Mr. & Mrs. b. P18,600 each for Mr. & Mrs. Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com) lOMoARcPSD|16874964 c. d. P30,600 for Mr.; P6,600 for Mrs. P30,000 for Mr.; P6,000 for Mrs. 9. The donor’s tax due on the May 15 donation should be: a. P6,000 for Mr.; P6,600 for Mrs. b. P6,000 for Mr.; P12,000 for Mrs. c. P36,600 for Mr.; P18,600 for Mrs. d. P40,000 for Mr. and Mrs. 10. The donor’s tax due on the December 25 donation should be: a. P0 for Mr. and Mrs. b. P6,000 for Mr.; P12,000 for Mrs. c. P36,600 for Mr.; P18,600 for Mrs. d. P40,000 for Mr. and Mrs. 11. Statement 1: Resident alien would be subject to donor’s tax only on their donations of property located in the Philippines. Statement 2: A donation by a foreign corporation of its own shares of stock to resident employees is not subject to gift tax but may be subjected to income tax. a. Only the first statement is correct b. Only the second statement is correct. c. Both statements are correct. d. Both statements are incorrect. 12. There is reciprocity, when the donor and the donated property is: Donor Property Intangible Personal Property a. Non-resident alien Immovable b. Non-resident citizen Tangible Personal Property c. Non-resident alien Any kind of property d. Resident alien Use the following data for the next two (2) questions: On December 19, 2017, Pres. Rodrigo R. Duterte signed into law the Package 1 of the Comprehensive Tax Reform Program (CTRP), also known as the “Tax Reform for Acceleration and Inclusion (TRAIN) as RA 10963. The law took effect on January 1, 2018. Pedro died on November 1, 2017. His administrator and heirs filed the estate tax return on May 1, 2018. 13. For estate tax purposes, which law shall be applied in determining the estate tax liability on the estate of Pedro? a. The Tax Code prior to its amendment under RA 10963 b. The Tax Code as amended under RA 10963 (TRAIN Law) c. Either “a” or “b” at the option of the executor or administrator d. Either “a” or “b”, at the option of the heirs 14. Using the same data in the preceding number but assuming Pedro died on January 25, 2018. Which law shall be applied in determining the estate tax liability on his estate? a. The Tax Code prior to its amendment under RA 10963 b. The Tax Code as amended under RA 10963 (TRAIN Law) c. Either “a” or “b” at the option of the executor or administrator d. Either “a” or “b”, at the option of the heirs 15. One of the following is not included in the gross estate of a decedent. a. Cash dividend that accrued before death. b. Shares of stock transferred in contemplation of death. c. d. Land held in trust but in decedent’s possession before death. Rent income on property that accrued before death. 16. A donation which takes effect upon the death of the donor I. Donation mort is causa II. Partakes of the nature of an intestate disposition III. Shall be gove rned by the law on succession a. I only c. I and III only b. I and II only d. I, II and III 17. A transfer subject to tax other than estate tax: a. Revocable transfer b. Transfer for insufficient consideration c. Transfer in contemplation of death d. Bonafide sale or transfer 18. Which is correct? a. A compulsory heir can question a donation and ask for its reduction if it impairs his legitime. b. Expenses primarily incurred by an heir intended to establish his interest in the estate are deductible judicial expenses from the gross estate. c. The Commissioner shall have authority to grant, in meritorious cases, a reasonable extension not exceeding six (6 months for filing the return. d. All of the above 19. One of the properties left by a decedent was gutted by fire during the settlement of the estate. The executor decided to claim the losses in computing income tax of the estate. One of the heirs objected to the executor since even before deducting the said losses, the taxable income of the estate is already zero. However, the executor stood his ground and insisted on claiming the losses as deduction in computing income tax. Which of the following statements is correct? a. The losses can no longer be deducted in computing the estate tax. b. The losses can still be claimed as deduction in computing the estate tax since there is no prohibition against it under the tax laws, rules and regulations. c. The losses can still be claimed as deduction in computing the estate tax since there was no tax benefit resulted in the deduction in the computation of income tax. d. The losses cannot be claimed as deduction both in the computation of estate tax and income tax since it occurred during the settlement of the estate. 20. Who among the following transferors is not liable for estate tax on the property transferred during his lifetime? a. The testator who bequeaths property to his heirs in a last will and testament executed and probated during his lifetime. b. The donor who reserves his right to amend or revoke the donation of property in favor of the donee. c. The donee of an appointed property who is required under a power of appointment to transfer such property upon death to his eldest child. d. The transferor of personal property who sold it for insufficient consideration. 21. The following properties will be classified uniformly under Conjugal Partnership of Gains and Absolute Community of Property, except: a. Property inherited or received as donation during the marriage Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com) lOMoARcPSD|16874964 b. c. d. Property acquired from labor, industry, work or profession of spouses Fruits or income due or derived during the marriage coming from common properties Fruits or income due or derived during the marriage coming from exclusive properties 22. The following deductions are also part of the gross estate, except: a. Claims against the estate b. Claims against insolvent persons c. Transfer for public use d. Death benefits under Republic Act. 4917 23. Which of the following allowable deductions of a nonresident alien decedent should be prorated? a. Net share of the surviving spouse b. Transfers for public use c. Unpaid mortgage d. Property previously taxed 24. Decedent died on May 1, 2018. If the estate is settled judicially, the maximum allowable extension for filing is up to: a. November 1, 2018 b. December 1, 2018 c. April 30, 2019 d. May 30, 2019 Use the following data for the next four (4) questions: Mr. Bu Ang, single and a non-resident alien, died of a heart attack in 2020, leaving the following properties in favor of his heirs: Gross estate within the Philippines P30,000,000 Gross estate outside the Philippines 20,000,000 Funeral Expense 500,000 Judicial and administrative expenses 2,000,000 Claims against the estate 5,000,000 His gross estate includes family home valued at P8,000.000. 25. How much is the gross taxable estate of Mr. Ang? a. P45,000,000 c. P30,000,000 b. P35,000,000 d. P50,000,000 26. How much is the deductible ordinary deductions of Mr. Ang’s estate? a. P4,320,000 c. P5,000,000 b. P3,000,000 d. P4,200,000 27. How much is the deductible special deductions of Mr. Ang’s estate? a. P500,000 c. P5,500,000 b. P5,000,000 d. P1,518,000 28. How much is the estate tax due of Mr. Ang’s estate? a. P1,470,000 c. P1,590,000 b. P1,500,000 d. P1,620,000 Use the following data for the next four (4) questions: Mr. Pim Musay, Filipino and married, died in 2019, leaving his estate in favor of his surviving spouse. The following information were made available: Real property in Quezon City, acquired during marriage. Said property is supported by a barangay certification that the spouses resided in this property at the time of Mr. Musay’s death. The fair market value of this property as per latest tax declaration is P15,000,000 while the zonal valuation as of the time death is P 20,000,000. Said real property was held as a mortgage in a loan applied by the spouses. As of the time of death, the outstanding balance of the mortgage payable amounted to P5,000,000. Real property in Batangas, inherited by Mr. Musay during marriage, two and half years ago, from his late father. The fair market value per tax declaration as of his death is P8,000,000 while the zonal valuation is P12,000,000. Said property was previously taxed at a value of P10,000,00 when Mr. Musay inherited the property from his father. Real property in Cavite, donated to Mrs. Musay, 10 years ago (before marriage) by his parents-in-law . The fair market value as per latest tax declaration as of the time of Mr. Musay’s death is P3,000,00 while the zonal valuation is P4,000,000. Other exclusive properties of Mr. Musay P1,000,000; Other properties of Mr. and Mrs. Musay- P3,000,000. Funeral expenses incurred by the estate during the wake and burial of Mr. Musay amounted to P1,900,000. 29. Compute item 34 (Gross Estate) of BIR form no. 1801 a. P28,500,000 c. P30,000,000 b. P32,500,000 d. P40,000,000 30. Compute Schedule V (Ordinary deductions) of BIR Form no. 0801 a. P5,000,000 c. P12,000,000 b. P10,250,000 d. P8,500,000 31. Compute item 40 (Net Taxable Estate) of BIR from no. 1801 a. P3,750,000 c. P29,750,000 b. P13,750,000 d. P0 32. Compute item 20 (Estate Tax Payable) of BIR from no. 1801. a. P225,000 c. P1,785,000 b. P825,000 d. P0 The next four (4) questions are based on the following: Pedro, head of the family, died intestate on August 20, 2019 leaving the following properties: Land and house (family home) P8,000,000 Agricultural land inherited from his father 800,000 who died 2 ½ years before his death Other real properties 11,000,000 Other tangible personal properties 200,000 Bank deposit, PNB-Manila representing 500,000 amount received by heirs under R.A. No. 4917 Obligations of and charges against certain properties follow: Medical expenses of last illness P 600,000 (supported by bills and statements from hospital) Actual funeral expenses (30% paid for 500,000 from the estate, 70% paid for by relatives) Judicial expenses incurred within six (6) 100,000 months after death Claims against the estate other than 270,000 unpaid mortgage Unpaid mortgage on inherited agricultural 30,000 land Claims against insolvent persons 100,000 The value of the agricultural land at the time of inheritance was P500,000. It had an unpaid mortgage of P80,000. 33. How much was the vanishing deduction? a. P264,757 c. P159,107 b. P253,443 d. P318,214 34. The total ordinary deduction shall be: Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com) lOMoARcPSD|16874964 a. P264,757 b. P664,757 c. P5,000,000 d. P13,500,000 35. The total special deduction shall be: a. P264,757 c. P5,000,000 b. P664,757 d. P13,500,000 36. How much was the taxable net estate? a. P6,684,822 c. P6,435,243 b. P6,696,557 d. P6,631,786 37. The amounts withdrawn from the deposit accounts of decedent subjected to the 6% final withholding tax imposed under Section 97 of NIRC, shall be: a. Excluded from the gross estate for purposes of computing the estate tax. b. Included from the gross estate for purposes of computing the estate tax. c. Claimed as tax credit against estate tax due. d. Claimed as deduction from the gross estate. 38. The administrator of the Estate of Juan Santos claims as deduction from the gross estate a receivable from a person who absconded. His assertion is that the claim against that person can no longer be collected. He also explains that for income tax purposes bad debts are deductible from the gross income so the receivable from a person who absconded shall also be treated in the same manner as in estate tax. Despite the administrator’s contention the BIR disallowed as deduction the claim against a person who absconded. Is the BIR correct? a. Yes, to be allowed as deduction from the gross estate the claim must be against an insolvent debtor and that the incapacity of the person must be a fact and not merely alleged. b. No, not to allow it to be deducted from the gross estate will be a great injustice because of the fact that collection is almost impossible. c. No, all items that are deductible from gross income for income tax purposes are also allowed to be deducted from the gross estate. d. Yes, the regulations are not clear and it requires BIR ruling for such claim to be allowed as deduction. Use the following data for the next four (4) questions: Juan Dela Cruz , non-VAT registered lessor of residential and commercial units, had the following date for the 1 st and 2nd quarters of 2020. Gross Receipts 1st Quarter 2nd Quarter Lease of Residential Units ▪ Monthly rental of P2,500,000 P2,300,000 P13,000/unit ▪ Monthly rental of 1,000,000 1,200,000 P18,000/unit Lease of commercial units 2,300,000 2,400,000 Input vat from vat suppliers 150,000 120,000 39. How much is the business tax due for the 1 st quarter 2020 of Mr. Dela Cruz? a. P99,000 c. P396,000 b. P174,000 d. P246,000 40. How much is the business tax due for the 2 nd quarter 2020 of Mr. Dela Cruz? a. P432,000 c. P708,000 b. P312,000 d. P108,000 41. How much is the business tax due for the 2 nd quarter 2020 of Mr. Dela Cruz, assuming he registered as a VAT taxpayer at the start of the 2nd Quarter 2018? a. P432,000 c. P708,000 b. P312,000 d. P108,000 42. Assuming Mr. Dela Cruz is vat registered taxpayer instead of non-vat registered, how much is his business tax due for the 1st Quarter of 2020? a. P246,000 c. P696,000 b. P546,000 d. P396,000 43. Statement 1: Banks are subject to the VAT on its interest income. Statement 2: Resident international carriers are subject to the 0% VAT on its gross Philippine billings on flight originating from the Philippines to a foreign destination. a. Both statements are correct b. Both statements are not correct c. Only the first statement is correct d. Only the second statement is correct 44. In case of sale, barter or exchange of real property subject to vat, the term fair market value shall mean a. The fair market value as determined by the Commissioner of Internal Revenue (zonal value). b. The fair market value as shown in the schedule of values of the Provincial and City assessor (real property tax declaration). c. Whichever is higher between the zonal value and the value per real property tax declaration. d. Whichever is lower between the zonal value and the value per real property tax declaration 45. Philippine Catering Corporation (PCC) is a vat registered company which has been engaged in the catering business for the past 10 years. It has invested a substantial portion of its capital on flat wares, table linens, plates, chairs, catering equipment, and delivery vans. PCC sold its first delivery van, already 10 years old and idle to Northern Gravel and Sand Corporation (NGSC), a corporation engaged in the business of buying and selling gravel and sand. The selling price of the delivery van was way below its acquisition cost. The sale of delivery van by PCC to NGSC is: a. An unrelated transaction to PCC, hence, not subject to vat b. An isolated transaction which is not subject to vat. c. The sale is subject to vat being a transaction incidental to the catering business which is a vat registered activity of PCC. d. None of the above 46. G.I. Joe, an alien employee of the Asian Development Bank (ADB) who is retiring soon has offered to sell his car to you, which he imported tax-free for personal use. The privilege of exemption from tax is granted to qualified personal use under the ADB Charter, which is recognized by the tax authorities. If Pedro decide to purchase the car, the tax consequence shall be: a. Exempt from vat b. G.I. Joe is subject to vat c. Pedro is subject to vat d. Either G.I. Joe or Pedro is subject to vat, at the option of G.I. Joe 47. Commonwealth Management and Services Corporation (Comaserco) is a corporation duly organized and existing under the laws of the Philippines. It is an affiliate of of Philippine American Life Insurance Company (Philamlife), organized by the latter to perform collection, consultative and other technical services, including functioning as an internal auditor of Philamlife and its other affiliates. These services were performed on a “non-profit, reimbursement-of-cost only” by Comersco. The services performed by Comersco to Philamlife and other affiliates were subjected to vat by the BIR. Which of the following contentions of Comersco is correct? Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com) lOMoARcPSD|16874964 (I) Exempt from vat because the service was not considered “in the ordinary course of trade or business”. (II) Exempt from vat because Comersco was established only to ensure operational orderliness and administrative efficiency of Philamlife and its affiliates, and not in the sale of services. a. Ionly c. Either I or II b. II only d. Neither I nor II 48. Which of the following is exempt from vat? a. Services rendered by Pedro Construction Company, a contractor to the World Health Organization (WHO) in the renovation of its offices in Manila. WHO is an entity exempt from tax under international agreements to which the Philippines is a signatory. b. Sale of tractors and other agricultural implements by Magsasaka Corporation to local farmers. c. Sale of RTW by Ana’s boutique, a Filipina dress designer, in her dress shop and other outlets. d. Fees for lodging paid by students to Bahay-bahayan dormitory, a private entity operating a student dormitory (monthly fee, P2,500). 49. Statement 1: Facilitation expense shall be included in the determination of applicable input vat on importation. Statement 2: Presumptive input vat are creditable against output tax only if the taxpayer is allowed to avail for 0% vat on its export sales. a. Only statement 1 is correct b. Only statement 2 is correct c. Both statements are correct d. Both statements are incorrect 50. _______ is a merchant of stocks or securities, whether an individual, partnership, or corporation, with an established place of business, regularly engaged in the purchase of securites and their resale to customers. He buys securities and sells them to customers with a view to the gains and profits that may be derived therefrom. a. dealer in securities c. franchise grantees b. real estate dealer d. lending investor 51. Mabuhay Corporation is a pre-need company. Which of the following is statements is incorrect? a. A considered a dealer in securities subject to 12% vat on gross receipts. b. A considered a dealer in securities subject to 12% vat on gross income. c. Its gross income is computed as gross receipts (which consist of actual receipts of premium on contract price) minus contributions to the trust funds to be set up independently as mandated by the Securities and Exchange Commission. d. None of the above Receivable balances are all income related and are inclusive of VAT. Revenues and purchases are VAT exclusive. Capital goods are estimated to have a useful life of 10 years. 52. How much is the correct output vat? c. P213,120 a. P216,000 b. P264,000 d. P240,000 53. How much is the total available input vat? c. P360,000 a. P86,400 b. P72,000 d. P370,000 54. How much is the deferred input tax as of March 31, 2018? a. P280,000 c. P283,200 b. P273,600 d. None 55. How much is the amount of input vat to be closed to expense or income. a. P26,000 closed to expense b. P22,000 closed to expense c. P4,400 closed to income d. P5,360 closed to income 56. Pilipinas Shell sold fuel to an international shipping carrier whose voyage is from a port in the Philippines directly to a foreign port without docking or stopping at any other port in the Philippines. What is the treatment of the transaction for VAT purposes? a. Exempt b. Zero-rated transaction c. Subject to 12% VAT d. Either “b” or “c” 57. When is the deadline for manual filing of the monthly VAT return? a. Ten (10) days from the end of the month b. Twenty (20) days from the end of the month c. Twenty-five (25) days from the end of the month d. Thirty (30) days from the end of the month 58. When is the deadline for manual filing of the quarterly VAT return? a. Ten (10) days from the end of the quarter b. Twenty (20) days from the end of the quarter c. Twenty-five (25) days from the end of the quarter d. Thirty (30) days from the end of the quarter 59. One of the following does not result to output tax: a. Domestic sale of goods b. Cash receipt on sale of services rendered in the Philippines c. Export sale of goods d. Cash receipt on sale of services rendered outside of the Philippines Use the following data for the next four (4) questions: The Wash Corporation, a VAT-registered company, is engaged in the laundry business. During the second quarter of 2018, the following information were made available: 60. The Value-added tax is not an/a: a. Direct tax b. Indirect tax c. Excise tax d. Ad-valorem tax Net revenues 2M Receivables from customers, April 1, 2018 448,000 Receivables from customers, June 30, 2018 672,000 Creditable VAT withheld 10,000 VAT purchases, other than capital goods 600,000 VAT purchases, capital goods (all in April 2018) 2.4M 61. Juan Dela Cruz is a Certified Public Accountant (CPA) who is currently employed as the Chief Financial Officer (CFO) of a large conglomerate. He regularly earns a total annual salary of P4,500,000 from his employment. In addition, he earns professional fees of P600,000 from his personal clients. The business tax liability of Juan shall be: a. 3% Other Percentage Tax Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com) lOMoARcPSD|16874964 b. c. d. 12% VAT Excise tax Amusement tax d. 62. A resident Filipino citizen (not a dealer in securities) sold shares of stocks of a domestic corporation that are listed and traded in the Philippine Stock Exchange. a. The sale is exempt from income tax but subject to the 6/10 of 1% stock transaction tax. b. The sale is subject to income tax computed at the graduated income tax rates of 20% to 35% on net taxable income. c. The sale is subject to the stock transaction tax and income tax. d. The sale is both exempt from the stock transaction tax and income tax. 63. Which of the following statements is incorrect? RA10378 provided for tax exemption of international carriers from: a. Income taxation on the basis of tax treaty or reciprocity. b. Vat on their carriage of passengers c. Percentage tax on their carriage of passengers d. Percentage tax on their carriage of goods. The donation is subject to graduated rates. 69. DMCI is a non-vat registered real estate dealer and lessor. If its monthly rental of residential units in 2019 taxable year exceeds P15,000 per unit, the same shall be subject to 12% vat a. True, regardless of the amount of annual gross receipts. b. True, only if the total annual gross receipts from rentals exceed P3,000,000. c. True, only if the total annual gross receipts from rentals and other operations exceed P3,000,000. d. False, DMCI is a non-vat registered entity. 70. Queenie Ripot operates a convenience store whose gross receipts during the taxable year was P3,500,000. She opted not to register under the VAT system. Statement 1: Her sales are subject to the 12% output VAT. Statement 2: She can claim input VAT credit arising from her purchases from VAT suppliers. a. Both statements are correct b. Both statements are not correct c. Only the first statement is correct d. Only the second statement is correct **end of exam** 64. Rentals of property, real or personal, received by bank and non-bank financial intermediaries performing quasibanking functions are: a. Subject to 12% vat b. Subject to gross receipts tax of 5% c. Subject to gross receipts tax of 7% d. Subject to 3% OPT if annual gross receipts do not exceed the vat threshold 65. Presumptive input VAT shall be available to the following, except: a. Sardines b. Tuna c. Milk d. Cooking oil 66. Statement 1: Banks are subject to the VAT on its interest income. Statement 2: Resident international carriers are subject to the 0% VAT on its gross Philippine billings on flight originating from the Philippines to a foreign destination. a. Both statements are correct. b. Both statements are incorrect. c. Only the first statement is correct. d. Only the second statement is correct. 67. Double taxation in its general sense means taxing the same subject twice during the same taxing period. In this sense, double taxation a. Violates substantive due process. b. Does not violate substantive due process. c. Violates the right to equal protection. d. Does not violate the right to equal protection. 68. Mr. Bill Morgan, a Canadian citizen but resident of El Nido, Palawan, donated in 2018 his car in Canada to his future daughter in-law who is to be married to his only son in Canada. His son and future daughter in law are both citizens and residents of Canada. What is the tax implication of the above donation? a. The donation is not subject to donor’s tax since the donee is a non-resident alien and the donated property is located in Canada. b. The donation is taxable, however, dowry exemption may be claimed as deduction. c. The donation is taxable at 6% in excess of P250,000 without any deduction for dowry. Downloaded by Kianne Marie De Torres (detorreskiannemarie06@gmail.com)