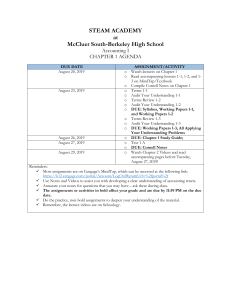

Chapter 12 The Statement of Cash Flows © 2019 Cengage. All rights reserved. Cash Flows and Accrual Accounting • • Statement of cash flows complements an accrualbased income statement by providing information on a company’s cash flows from operating, investing, and financing activities External parties have an interest in a company’s cash flows: – Stockholders – Creditors © 2019to Cengage. All rights reserved. Introduction Cost management Exhibit 12.1—Cash Flows and Net Income for Four Companies (all amounts in millions of dollars) © 2019 Cengage. All rights reserved. Purpose of the Statement of Cash Flows • • • Summarizes an entity’s cash receipts and cash payments during the period from operating, investing activities, and financing activities Reports the changes in cash over a period of time and explains those changes Assess company’s performance on a cash basis © 2019to Cengage. All rights reserved. Introduction Cost management Cash Equivalents • • • • • Readily convertible to a known amount of cash Maturity date of three months or less Less degree of risk in terms of price changes Combined with cash on a statement of cash flows Examples: commercial paper, money market funds, and Treasury bills © 2019to Cengage. All rights reserved. Introduction Cost management Operating Activities • • Activities concerned with the acquisition and sale of products and services Examples: – – – – Collection of customer accounts Payment to suppliers for inventory Payment of wages Payment of taxes © 2019to Cengage. All rights reserved. Introduction Cost management Investing Activities • • Activities concerned with the acquisition and disposal of long-term assets Examples: – – – – Capital expenditures Purchase of another company Sale of plant and equipment Sale of another company © 2019to Cengage. All rights reserved. Introduction Cost management Financing Activities • • Activities concerned with the raising and repaying of funds in the form of debt and equity Examples: – – – – – – – Issuance of capital stock Issuance of bonds Issuance of bank note Repurchase of stock Retirement of bonds Repayment of notes Payment of dividends © 2019to Cengage. All rights reserved. Introduction Cost management Exhibit 12.2—Format for the Statement of Cash Flows © 2019 Cengage. All rights reserved. Exhibit 12.3—Classification of Items on the Statement of Cash Flows © 2019 Cengage. All rights reserved. Noncash Investing and Financing Activities (1 of 2) • Assume that at the end of the year, Wolk Corp. issues capital stock to an inventor in return for the exclusive rights to a patent. Although the patent has no ready market value, the stock could have been sold on the open market for $25,000 © 2019 Cengage. All rights reserved. Noncash Investing and Financing Activities (2 of 2) • Assume Wolk sells stock on the open market for $25,000 and then pays this amount in cash to the inventor for the rights to the patent © 2019 Cengage. All rights reserved. Two Methods of Reporting Cash Flow from Operating Activities • Direct method – Reports major classes of cash receipts and cash payments • Indirect method – Net income is adjusted for the effects of accruals and deferrals • Net cash provided by Operating Activities is the same under both methods © 2019to Cengage. All rights reserved. Introduction Cost management Exhibit 12.4—Boulder Company’s Income Statement © 2019 Cengage. All rights reserved. Exhibit 12.5—Boulder Company’s Balance Sheet © 2019 Cengage. All rights reserved. Exhibit 12.6—Statement of Cash Flows Using the Direct Method © 2019 Cengage. All rights reserved. Exhibit 12.7—Statement of Cash Flows Using the Indirect Method © 2019 Cengage. All rights reserved. Accounting Equation and the Statement of Cash Flows © 2019 Cengage. All rights reserved. Summary of Various Possibilities for Inflows (+) and Outflows (−) of Cash © 2019 Cengage. All rights reserved. Master T-Account Approach—Direct Method • Step1: Set up three master T accounts • Step 2: determine cash flows from operating activities • Step 3: determine cash flows from investing activities • Step 4: determine cash flows from financing activities © 2019 Cengage. All rights reserved. Exhibit 12.8—Julian Corp.’s Income Statement © 2019 Cengage. All rights reserved. Cash Flows from Operating Activities—Sales Revenue and Accounts Receivable © 2019 Cengage. All rights reserved. Exhibit 12.10—Master T Account for Cash Flows from Operating Activities © 2019 Cengage. All rights reserved. Exhibit 12.11—Conversion of Income Statement Items to Cash Basis © 2019 Cengage. All rights reserved. Exhibit 12.12—Master T Account for Cash Flows from Investing Activities © 2019 Cengage. All rights reserved. Exhibit 12.13—Master T Account for Cash Flows from Financing Activities © 2019 Cengage. All rights reserved. Exhibit 12.14—Completed Statement of Cash Flows (1 of 2) © 2019 Cengage. All rights reserved. Exhibit 12.14—Completed Statement of Cash Flows (2 of 2) © 2019 Cengage. All rights reserved. Master T-Account Approach—Indirect Method © 2019 Cengage. All rights reserved. Exhibit 12.15—Indirect Method for Reporting Cash Flows from Operating Activities © 2019 Cengage. All rights reserved. Summary of Adjustments to Net Income under the Indirect Method Additions to Net Income Deductions from Net Income Decrease in accounts receivable Increase in accounts receivable Decrease in inventory Increase in inventory Decrease in prepayments Increase in prepayments Increase in accounts payable Decrease in accounts payable Increase in accrued liabilities Decrease in accrued liabilities Losses on sales of long-term assets Gains on sales of long-term assets Losses on retirements of bonds Gains on retirements of bonds Depreciation, amortization, and depletion © 2019 Cengage. All rights reserved. Comparison of the Indirect and Direct Methods • The direct method – Provides valuable information in evaluating a company’s operating efficiency – Reveals too much to competitors by telling them the amount of cash receipts and cash and payments from operations • The indirect method – Focuses attention on the differences between income on an accrual basis and a cash basis – Should separately disclose two important cash payments—income taxes paid and interest paid © 2019to Cengage. All rights reserved. Introduction Cost management Cash Flow Adequacy • Measures a company’s ability to meet future debt obligations after paying taxes and interest costs and making capital expenditures Cash Flow Adequacy Cash Flow from OPerating Activities Capital Expenditures Average Amount ofDebt Maturing over Next Five Years © 2019to Cengage. All rights reserved. Introduction Cost management Work-Sheet Approach—Indirect Method (1 of 7) © 2019 Cengage. All rights reserved. Work-Sheet Approach—Indirect Method (2 of 7) © 2019 Cengage. All rights reserved. Work-Sheet Approach—Indirect Method (3 of 7) © 2019 Cengage. All rights reserved. Work-Sheet Approach—Indirect Method (4 of 7) © 2019 Cengage. All rights reserved. Work-Sheet Approach—Indirect Method (5 of 7) © 2019 Cengage. All rights reserved. Work-Sheet Approach—Indirect Method (6 of 7) © 2019 Cengage. All rights reserved. Work-Sheet Approach—Indirect Method (7 of 7) © 2019 Cengage. All rights reserved.