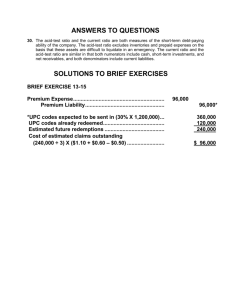

AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon Module 2: Premiums What are Premiums? Premiums are articles of value such as toys, dishes, silverware, and other goods given to customers as a result of past sales or sales promotion activities. In a marketing sales strategy to increase sales of products, entities offer premiums to customers in return for product labels, box tops, wrappers, and coupons. Accordingly, WHEN THE MERCHANDISE IS SOLD, an accounting liability for future distribution of the premium arises and should be given accounting recognition. Accounting Procedures: (1) When premiums (items to be given as prizes) are purchased: Premiums xxx Cash xxx (2) When the premiums are distributed to customers: Premium Expense xxx Premiums xxx (3) At the end of the year, if premiums are still outstanding: Premium Expense xxx Estimated Premium Liability xxx ILLUSTRATIONS ● ● ● An entity manufactures a certain product and sells it at P300 per unit. A soup bowl is offered to customers on the return of 5 wrappers plus a remittance of P10. The bowl costs P50 and it is estimated that 60% of the wrappers will be redeemed. The data for the first year concerning the premium plan are summarized below: Sales - 10,000 units at P300 each 3,000,000 Soup bowls purchased - 2,000 units at P50 each 100,000 Wrappers redeemed 4,000 Accounting Entries: (1) To record the sales: Cash Sales 3,000,000 3,000,000 AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon (2) To record the purchase of the premiums: Premiums - soup bowls 100,000 Cash 100,000 (3) To record the redemption of 4,000 wrappers: Cash (800*P10 redemption price) 8,000 Premium Expense (800*P40) 32,000 Premiums - soup bowls (8,000 + 32,000) 40,000 4,000 wrappers / 5 wrappers = 800 bowls to be distributed. 50 bowls - 10 redemption price = 40/bowl (4) To record the liability at the end of the 1st year: Premium Expense 16,000 Estimated Premium Liability 16,000 Wrappers to be redeemed (60% x 10,000 wrappers) 6,000 Less: Wrappers redeemed 4,000 Balance 2,000 Divide by bo. Of wrappers to redeem 5 Premiums to be distributed 400 Multiply by cost per bowl 40 Estimated liability 16,000 (5) At the end of the year, the accounts related to the premium plan are classified and presented in the financial statements as follows: Balance Sheet Current Asset: Premiums - soup bowls 60,000 Current Liability: Estimated Premium Liability 16,000 Income Statement Distribution (Selling) Cost Premium Expense 48,000 AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon WHAT ARE CASH REBATE PROGRAMS? It is another kind of premium program that promotes sales where a cash refund is given to the customer upon submission of certain documents as proof of purchase. Cash register receipts, bar codes, rebate coupons, and other proof of purchase often can be mailed to the manufacturer for cash rebates. Accounting Recognition Of Cash Rebates: ➔ Estimated amount of cash rebate should be recognized both as an EXPENSE AND AN ESTIMATED LIABILITY IN THE PERIOD OF SALE. ILLUSTRATION: ● ● ● ● An entity offered P500 cash rebate on a particular model of TV set. The customers must present a rebate coupon enclosed in every package sold plus the official receipt. Past experience indicates that 40% of the coupons will be redeemed. During the current year, the entity sold 4,000 TV sets and total payments to customers amounted to P450.000 Accounting Entries: (1) To recognize the cash rebate program: Rebate Expense 800,000 Estimated Rebate Liability 800,000 Rebate coupons issued 4,000 (TV set sold) Expected to be redeemed 40% (redemption experienced) Coupon rebates to be redeemed (4,000*40%) 1,600 Cash rebate per coupon 500 (cash rebate per TV set sold) Estimated rebate liability (1,600*500) 800,000 (2) To record payments to customer: Estimated Rebate Liability Cash 450,000 450,000 AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon What is the accounting treatment for Cash Discounts? Similarly, with the premium offer and cash rebates, an expense and an estimated liability for the expected cash discount shall be recognized in the period of sale. ILLUSTRATION: ● ● ● ● During the current year, an entity inserted in each package sold a coupon offering P300 off the purchase price of a particular brand of product when the coupon is presented to retailers. The retailers are reimbursed for the face amount of coupons plus 10% for handling. Previous experience indicates that 30% of coupons will be redeemed. During the current year, the entity issued coupons with face amount of P5,000,000 and total payments to retailers amounted to P1,100,000. Accounting Entries: (1) To recognize the cash discount coupon offer: Cash Discount Coupon Expense Estimated Discount Coupon Liability 1,650,000 1,650,000 Discount coupon issued at face amount 5,000,000 Estimated redemption based on experienced 30% Face amount of coupons to be redeemed 1,500,000 Multiply by (100% redemption + 10% handling) 110% Total coupon liability 1,650,000 (2) To record payments to retailers: Estimated Discount Coupon Liability Cash Estimated Coupon Liability at the end of the year 1,100,000 1,100,000 550,000 (1,650,000 - 1,100,000) What is CUSTOMER LOYALTY PROGRAM (Credit Points Award System)? Designed to reward customers for past purchases by providing them with incentives to make further purchases. Supports marketing strategy of building brand loyalty, retain valuable customers and increase sales volume. AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon How does CUSTOMER LOYALTY PROGRAM work? When a customer buys goods or services, AWARD CREDITS or "POINTS" are given. Customer can redeem the "points" by granting the customer free or discounted goods or services. Customers may be required to accumulate a specified number of award credits or points before redemption. MEASUREMENT OF AWARD CREDITS OR POINTS Accounted for as a "SEPARATE COMPONENT OF THE INITIAL SALE TRANSACTION." Accounted as "FUTURE DELIVERY OF GOODS OR SERVICES." IFRS 15, Par 74 provides that an entity shall allocate the transaction price to each performance obligation identified in a contract on a relative stand-alone selling price basis. The fair value of the consideration received with respect to the initial sale shall be allocated between the award credits and the sale based on relative stand-alone selling price. The stand-alone selling price is the PRICE AT WHICH AN ENTITY WOULD SELL A PROMISED GOOD OR SERVICE SEPARATELY TO A CUSTOMER. RECOGNITION The consideration allocated to the award credits is INITIALLY recognized as DEFERRED REVENUE and SUBSEQUENTLY recognized as REVENUE WHEN the AWARD CREDITS are REDEEMED. The amount of revenue recognized shall be based on the number of award credits that have been redeemed relative to the total number expected to be redeemed. The estimated redemption rate is assessed each period. Changes in the total number expected to be redeemed do not affect the total consideration for the award credits. The changes in the total number of award credits expected to be redeemed shall be reflected in the amount of revenue recognized in the current and future periods. periods. The calculation of the revenue to be recognized in any one period is made on a "cumulative bases" in order to reflect the changes in the estimate. ILLUSTRATION 1 ➔ A grocery retailer operates a customer loyalty program. ➔ The grocery grants program members loyalty points when they spend a specified amount on groceries. ➔ Program members can redeem the points for further groceries. The points have no expiry date. ➔ The sales during 2020 amounted to P9,000,000 based on stand-alone selling price. ➔ During 2020, the customers earned 10,000 points. ➔ Management expects that 80% or 8,000 of these points will be redeemed. ➔ The stand-alone selling price of each loyalty point is estimated at P100. ➔ On December 31, 2020, 4,000 points have been redeemed in exchange for groceries. ➔ In 2021, the management revised expectations and now expects that 90% or 9,000 points will be redeemed altogether. ➔ During 2021, the entity redeemed 4,100 points. In 2022, a further 900 points are redeemed. ➔ Management continues to expect that only 9,000 points will ever be redeemed, meaning, no more points will be redeemed after 2022. AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon COMPUTATIONS: ALLOCATION OF TRANSACTION PRICE Product Sales 9,000,000 Points-stand-alone selling price (10,000 * 100) 1,000,000 Total 10,000,000 ALLOCATION OF SALES Product Sales (9,000,000/10,000,000*9,000,000) 8,100,000 Points (1,000,000/10,000,000*9,000,000 900,000 Total Transaction Price 9,000,000 Accounting Entries: (1) Initial sale in 2020: Cash 9,00,000 Sales 8,100,000 Unearned Revenue - Points 900,000 (2) Redemption of 4,000 points in 2020: Unearned Revenue - Points Sales Revenue to be recognized in 2020: 450,000 450,000 4,000 / 8,000 * 900,000 = 450,000 (3) Redemption for 4,100 points in 2021: Unearned Revenue - Points Sales 360,000 360,000 Points redeemed in 2020: 4,000 Points redeemed in 2021: 4,100 Tota points redeemed to Dec. 31, 2021 8,100 Cumulative Revenue on Dec. 31, 2021 (8,100 / 9,000 * 900,000) 810,000 Revenue recognized in 2020 (450,000) Revenue recognized in 2021 360,000 AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon (4) Redemption of 900 points in 2022: Unearned Revenue - Points 90,000 Sales 90,000 Points redeemed in 2020: 4,000 Points redeemed in 2021: 4,100 Points redeemed in 2022: 900 Total points redeemed to Dec. 31, 2021 9,000 Cumulative Revenue on Dec. 31, 2022 (9,000 / 9,000 * 900,000) 900,000 Revenue recognized in 2021 (810,000) Revenue recognized in 2022 90,000 ILLUSTRATION 2 - 3rd Party Operates Loyalty Program ➔ A retailer of electrical goods participates in a customer loyalty program operated by an airline. ➔ The retailer grants program members one air travel point for every P1,000 spent on electrical goods. ➔ Program members can redeem the points for travel with the airline subject to availability. The entity pays the airline P60 for each point. ➔ During the current year, the entity sold electrical goods for consideration totaling P4,500,000 based on a stand-alone selling price and granted 5,000 points with a stand-alone selling price of P100 for each point. SOLUTION: SELLING PRICE FRACTION ALLOCATION 4,500,000 0.90 4,050,000 500,000 0.10 450,000 Product Sales Points (5,000 * 100) 5,000,000 Revenue from points 450,000 Payments for Airline (5,000 * 60) (300,000) Net revenue from points 150,000 ● ● The entity has fulfilled its obligation by granting the points. Therefore, revenue from points is recognized when the electrical goods are sold. 4,500,000 AE 16: INTERMEDIATE ACCOUNTING 2 A.L Pericon Accounting Entries: (1) To record initial sale: Cash 4,500,000 Sales 4,050,000 Revenue from points 450,000 (2) To record payment to the airline: Loyalty Program expense Cash 300,000 300,000