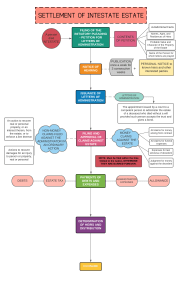

LECTURE 4: ESTATE TAXATION A transfer may be gratuitous or onerous. CONCEPT OF TRANSFER TAXATION Gratuitous Onerous 1. Donacion inter vivos (during lifetime) 1. Value-added Tax 2. Other Percentage Taxes 2. Donacion mortis causa (death) 3. Excise Taxes with applicable Documentary Stamp Tax I. Gratuitous Transfer: ESTATE TAX An estate tax is a tax on the right to transfer certain property at death and on certain transfers which are made by law equivalent to testamentary disposition (in contemplation of death). It is an excise tax (a tax impose upon the right or privilege), the object of which is the shifting of economic benefits and the enjoyment of the property from the deceased to the living. It accrues as of the time of death of the deceased. The taxpayer in estate taxation is the estate of the decedent represented by the administrator, executor or legal heirs. 1. Concept of Succession – a mode of acquisition by virtue of which the property, rights and obligations to the extent of the value of the inheritance, of a person are transmitted through his death to another or others by will or by operation of law. Will – is an act whereby a person is permitted with the formalities prescribed by law, to control to a certain degree the disposition of his estate, to take effect after his death. From the moment of death of the decedent, the rights to the succession are transmitted, and the possession of the hereditary property is deemed transmitted to the heir. Kinds of Will: a. Notarial or Ordinary Will – one which is executed in accordance with the formalities prescribed by Art. 804 to 808 of the New Civil Code. It is the will that is created for the testator by a third party, usually his lawyer, follows proper form, signed and dated in front of the required bumber of witnesses and acknowledged by the presence of a notary public. b. Holographic Will – is a written will which must be entirely written , dated and signed by the hand of the testator himself, without the necessity of any witnesses. c. Codicil – A supplement or addition to a will, made after the execution of a will and annexed to be taken as part thereof, by which any disposition made in the original will is explained, added or altered. 2. Elements of Succession Decedent – the person whose property is transmitted through succession, whether testamentary, intestate, or mixed. Heir – the person called to the succession either by the provision of a will or by operation of law. Estate – refers to all property, rights and obligations of a person which are not extinguished upon his death. 3. Kinds of Succession a. Testamentary – results from the designation of an heir, made in a will executed in the form prescribed by the law. The descedent may dispose his properties in his last will and testament in the manner he wants, however, he must reserve some for certain persons who are called by the law as compulsory heirs. Compulsory heirs are: i. Legitimate children and descendants, which include legally adopted children ii. In the absence of legitimate descendants, the legitimate parents or ascendants* iii. Surviving spouse iv. Illegitimate child, both natural and spurious *Note: Legitimate parents or ascendants can only inherit in the absence of legitimate children or descendants. Brothers and sisters of the decedent are not considered as compulsory heirs, thus they cannot inherit from the legitime of the decedent In the absence of compulsory heirs, the successors would be: i. Relatives up to 5th degree of consanguinity ii. If there were no relatives, the government shall inherit the whole estate. LECTURE 4: ESTATE TAXATION iii. If there is a will, the decedent may name other persons to inherit the free portion of the net distributable estate Kinds of Successors i. Legatee – an heir of personal property given by virtue of a will ii. Devisee – an heir of real property given by virtue of a will Under testamentary succession, properties left by the decedent are classified into: i. Legitime – portion of the testator’s property which could not be disposed freely because the law has reserved it for the compulsory heirs. ii. Free portion – part of the whole estate which the testator could dispose of freely through a written will irrespective of his relationship to the recepient. Executor (executrix) is the person nominated by the testator to carry out the directions and requests in the decedent’s will and to dispose his property according to the decedent’s testamentary provisions after his death. b. Legal Intestate Succession – transmission of properties where there is no will, or if there is a will, such is void or lost its validity, or nobody succeeds the will. In the intestate succession, the entire estate of the decedent is distributed to the heirs. The compulsory heirs in testamentary succession are also the heirs in intestate succession. However, intestate heirs include brothers and sisters, collateral relatives within the fifth degree of consanguinity and the state. Administrator (administratrix) is the person appointed by the court, in accordance with the governing statute, to administer and settle intestate estate and such testate estate as no competent executor designated by the testator. c. II. Mixed Succession – a transmission of properties, which is effected partly by will and partly by operation of law Formula in Computing Estate Tax 1. For married decedents (residents and citizens) Gross Estate Less: Allowable Deductions 1. Ordinary (ELITE) Net Estate before Special Deductions 2. Special Deductions Family Home Medical Expenses Standard deduction Benefits received under RA 4917 Share of the Surviving Spouse (1/2 of the net conjugal/community estate before special deductions) Net Taxable Estate Estate Tax Due Less: Estate Tax Credit Estate Tax Payable Exclusive Properties xx Conjugal/Community Properties xx Total (xx) xx (xx) xx (xx) xx xx (xx) (xx) (xx) (xx) (xx) xx xx (xx) xx As a general rule, obligations contracted during the marriage are presumed to have benefited the marriage, and are charges againts the community/conjugal property (e.g. funeral expenses, judicial expenses, claims against the estate). Vanishing deduction may be a dedcution against exclusive or community/conjugal property, depending on the classification of the property to which it is related, if exclusive or community/conjugal. A deduction, whether against exclusive or community/conjugal estate follows the classification of the property in the gross estate. If the property to which the deductioon is related is exclusive property in the gross estate, the deduction is against the exclusive gross estate. If the property to which the deductioon is related is community/conjugal property in the gross estate, the deduction is against the community/conjugal gross estate. LECTURE 4: ESTATE TAXATION 2. For single decedents III. Gross estate Less: Ordinary Deductions Special Deductions Net Taxable Estate xx (xx) (xx) xx Estate Tax Due Less: Estate Tax Credit Estate Tax Payable xx (xx) xx Gross Estate Residents and Citizens Non-Resident Aliens What are included? How to value? What are included? How to value? 1. ALL real properties wherever situated. The higher between the Fair Value or the Zonal Value. 1. Real properties located ONLY in the Philippines The higher between the Fair Value or the Zonal Value. Fair Value at the time of death 2. Personal properties located ONLY in the Philippines: Fair Value at the time of death 2. ALL properties situated: personal wherever a. Tangible b. Intangible 3. Whether real or personal property: a. In contemplation of death b. Transfer with retention or reservation of certain right c. Transfer under general power of appointment d. Revocable transfer In case of shares of stocks: a. If traded in the local stock exchange, the MEAN between the highest and lowest quotations. b. If not traded in the local stock exchange: i. Ordinary shares – book value ii. Preferred shares – par value a. If the transfer is a bona fide sale, no amount shall be included in the gross estate. b. If the transfer is a sale but for no or insufficient consideration, the difference between the FAIR VALUE at the time of death and the consideration received. c. If the transfer is a sale for no or insufficient consideration and the fair value at a. Tangible b. Intangible properties situated only in the Philippines unless exempted on the basis of reciprocity. The same as residents and citizens, however, only for properties situated within the Philippines. In case of shares of stocks, same as residents and citizens. Same valuation as in the case of residents and citizens. LECTURE 4: ESTATE TAXATION the time of death is LESS than the consideration received, no amount shall be included in the gross estate. 4. Proceeds of life insurance, included only if: a. Whether REVOCABLE or IRREVOCABLE, when the beneficiary is i. The estate of the deceased ii. His executor or iii. His administrato r b. The beneficiary is a third person, and the transfer is REVOCABLE IV. Amount of proceeds. Same treatment as in the case of residents and citizens, only if applicable. What intangible properties are considered as situated within the Philippines? 1. Franchise which must be exercisable in the Philippines; 2. Shares, obligations or bonds issued by domestic corporations; 3. Shares, obligations or bonds issued by any foreign corporation, 85% of business of which is in the Philippines; 4. Shares, obligations or bonds issued by any foreign corporation, if such shares, obligations or bonds have acquired business in the Philippines; 5. Shares or rights in any partnership, business or industry established in the Philippines. Exemptions and Exclusions from Gross Estate Under Section 85 and 86 of NIRC 1. Capital or exclusive property of the surviving spouse 2. Properties outside the Philippines of a non-resident alien decedent 3. Intangible personal property of a non-resident alien in the Philippines when the rule of reciprocity applies. Under Section 87 of NIRC 1. Merger of usufruct in the owner of the naked title 2. Transmission or delivery of the inheritance or legacy of the fiduciary heir or legatee to the fideicommissary 3. Transmission from the first heir, legatee or donee in favor of another beneficiary, in accordance with the will of the predecessor 4. All bequests, devices, legacies or transfers to social welfare , cultural and charitable institutions, provided: i. No part of the net income of said institution inure to the benefit of any individual; ii. Not more than 30% of such transfers shall be used for administration purposes. Under Special Laws 1. Proceeds of life insurance and benefits received by members of the GSIS (RA 728) 2. Benefits received by members from SSS by reason of death (RA 1792) 3. Amounts received from Philippine and United States governments for war damages 4. Amounts received from United States Veterans Administration 5. Retirement benefits of officials/employees of a private firm (RA 4917), provided they are included in the gross estate. LECTURE 4: ESTATE TAXATION 6. Payments from the Philippines and US governments to the legal heirs of deceased of World War II Veterans and deceased civilian for supplies/services furnished to the US and Philippine Army (RA 136) V. Property Relationship Between Spouses Conjugal Partnership Absolute Community a. Gratuitous Exclusive Communal b. Onerous Exclusive Communal c. Exclusive Exclusive a. Gratuitous title Exclusive Exclusive b. Onerous Title Conjugal Communal c. Exclusive Exclusive d. In exchange of conjugal/ community property Conjugal Communal e. Fruits or income from EXCLUSIVE property Conjugal Exclusive f. Fruits or income from conjugal/ community property Conjugal Communal The highlighted rows are the differences between the two systems. Jewelries shall form part of the communal property (in case of absolute community). Rules in determining the property of relationship 1. Agreement on marriage settlement 2. If there was no prenuptial agreement and: i. The date of marriage took place before August 3, 1988, conjugal partnership of gains. ii. The date of marriage took place on or after August 3, 1988, absolute community of property. I. Property acquired BEFORE Marriage Where the spouse has a legitimate descendant from a previous marriage II. Property acquired DURING marriage VI. In exchange of EXCLUSIVE property Deductions Deductions from gross estate Residents and Citizens: ELITE + PP + VD + FH + STD + R + M + Share of the Surviving Spouse Nonresident Aliens: ELITE + PP + VD + Share of the Surviving Spouse 1. Expenses, losses, indebtedness and taxes (please see discussions below). a. If decedent was a citizen or resident alien, deduct all ELIT. b. If decedent was a non-resident alien, prorate ELITE as follows: Phil. Gross Estate World Estate x Total ELITE 2. Transfers for PUBLIC PURPOSE. These are bequests, legacies, devises or transfers for the use of the government of the Phil. or any political subdivision thereof, exclusively for public purpose. 3. Deduction for property previously taxed (VANISHING DEDUCTION). 4. The family home not exceeding P10,000,000. 5. Standard deduction for citizen or resident alien decedent only of P5,000,000. 6. Retirement benefits received by employees of private firms from private pension plan approved by the BIR under R.A. 4917. 7. Net share of the surviving spouse in the conjugal partnership property or community property as diminished by the expenses properly chargeable to such property shall be deducted from the estate. Expenses, losses, indebtedness, and taxes deductible from gross estate (ELIT) 1. Funeral expenses. Limit is 5% of the gross estate but not exceeding P200,000 (statutory maximum). 2. Judicial expenses for the testamentary or intestate proceedings. 3. Losses due to fire, storm, shipwreck, or other casualty. 4. Losses due to theft, robbery or embezzlement. LECTURE 4: ESTATE TAXATION 5. Claims of the decedent against insolvent persons, where the value of the decedent’s interest therein is included in the gross estate. 6. Claims against the estate, provided that the debt instrument was notarized at the time the indebtedness was incurred; and, if the loan was contracted within three years before the death of the decedent, a statement showing the disposition of the proceeds of the loan (or how the proceeds of the loan was used) must accompany the estate tax return. 7. Unpaid mortgage, where the value of the decedent’s interest, undiminished by the mortgage, is included in the gross estate. 8. Income tax on income prior to death of the decedent. 9. Property taxes which have accrued prior to death of decedent. REQUISITES for deduction of losses in Nos. 3 and 4 above a. The loss is not compensated by insurance or otherwise. b. The loss is not claimed as a deduction in the estate income tax return. c. The loss must occur not later than the last day for payment of the estate tax. (The last day for payment of the estate tax is 6 months from the decedent’s death). PROPERTY PREVIOUSLY TAXED (VANISHING DEDUCTION) 1. Purpose - to minimize the effects of a double tax on the same property within a short period of time. 2. Conditions for allowance: a. There is a property forming a part of the gross estate of the present decedent situated in the Philippines; b. The present decedent acquired the property by inheritance or donation within 5 years prior to his death; c. The property subject to vanishing deduction can be identified as the one received from the prior decedent, or from the donor, or can be identified as having been acquired in exchange for the property so received; d. The property acquired formed part of the gross estate of the prior decedent, or of the taxable gift of the donor; e. The estate tax on the prior transfer or the gift tax on the gift must have been paid; and f. The estate of the prior decedent has not previously availed of the vanishing deduction. 3. Percentage of vanishing deduction - the rate depends on the interval between the death of present decedent and death of prior decedent (if the property was acquired by inheritance) or death of present decedent and date of gift (if the property was acquired by donation), as follows: More than Not more than Percentage xxx 1 years 100% 1 years 2 years 80% 2 years 3 years 60% 3 years 4 years 40% 4 years 5 years 20% 5 years Xxx Xxx 4. Procedures in computing vanishing deduction a. Determine the initial value by comparing the FMV of the property used in computing the first transfer tax paid with the FMV of the property in the present decedent. The lower of the two is the initial value. b. From the initial value taken, deduct any mortgage or lien on the property previously taxed which was paid by the present decedent prior to his death, where such mortgage or lien was a deduction from the gross estate of the prior decedent or gross gift of the donor. This is the initial basis. c. The initial value taken, as reduced by Step (b), shall be further reduced by prorated deductions for expenses, losses, indebtedness, taxes (ELIT) and transfers for public purpose (PP) only, allocable to the property previously taxed as follows: Initial basis x Deductions = Portion deductible Gross estate This is the final basis. d. Determine the time interval between the death of present decedent and death of prior decedent (if the property was acquired by inheritance) or death of present decedent and date of gift (if the property was acquired by donation) to find the applicable percentage of vanishing deduction. LECTURE 4: ESTATE TAXATION e. Multiply the final basis by the percentage of vanishing deduction to arrive at the VANISHING DEDUCTION. The FAMILY HOME 1. Defined - The family home is the dwelling house where a person and his family reside, and the land on which it is situated. 2. Value included in the gross estate. The current fair market value or zonal value of the family home, whichever is higher, shall be included in the gross estate of decedent. 3. Valuation date. The family home shall be valued as of the date of death. 4. Conditions for allowance of deduction: a. Decedent must have died on or after July 28, 1992. b. The total value of the family home must be included in the gross estate of the decedent. c. The family home must be the actual residence of decedent and his family at the time of death, as certified by the Barangay Captain of the locality where the family home is situated. d. Deduction cannot exceed the fair market value or zonal value of the family home as included in the gross estate but not exceeding P10,000,000. e. It is a deduction from common properties or separate properties of the decedent, as the case maybe. Tax credit for estate tax paid to a foreign country 1. 2. Who can claim? Only citizen or resident alien decedent. Amount Deductible, whichever is lower: a. Actual estate tax paid abroad b. Limit 2. Limitations on tax credit: a. Only one country is involved Net estate (per Foreign Country) Total net estate x Philippine estate tax b. Two or more foreign countries are involved Limit 1: per country Net estate (per Foreign Country) Total net estate x Philippine estate tax x Philippine estate tax Limit 2: Total Foreign Country Net estate (all Foreign Countries) Total net estate VII. Compliance Requirements a. Notice of death shall be given when the value of the gross estate exceeds P 20,000 b. The executor, administrator or any of the legal heirs shall file the notice of death within 2 months after the decedent’s death or within 2 months after the executor or administrator has qualified. c. The estate tax return shall be filed within 6 months after the decedent’s death, but may be extended to not exceeding 30 days if authorized by the BIR Commissioner. d. When the estate tax return shows a gross value exceeding P 2,000,000, it shall be supported with a statement duly certified by a CPA. e. The payment of estate tax shall be made at the time the return is filed. However, the CIR may allow an extension of until 5 years if settled judicially or 2 years if settled extra-judicially. LECTURE 4: ESTATE TAXATION