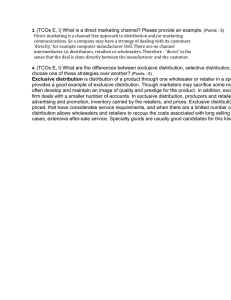

ESTATE TAX: Gross Estate of Married Decedents

Gross estate of married decedents:

1. The decedent’s exclusive property

2. The common property of the spouses

Exclusive

GROSS ESTATE

Less: Deductions

xxx

Conjugal/Communal

xxx

Total

xxx

*Separate or common properties depends on the property regime agreed upon before marriage

in their “Prenuptial Agreement”

BASIC RULE:

1. Common property presumption rule – properties of spouses are presumed common

properties unless proven to be exclusive properties of either of the spouses

2. Consistent classification rule – Sale or exchange of properties do not alter their classification.

Properties acquired using separate properties are separate properties, while properties

acquired using common properties are common properties. One exception under ACP

3. Accruals in value or gains on sale of properties – increases in value or gains on the sale of

properties are subject to the rules of the property regime agreed upon by the spouses

Common types of property regimes:

1. Absolute separation of property (ASP) – All properties of spouses are separate properties

except those which they may acquire jointly.

2. Conjugal partnership of gains (CGP) – All properties before marriage are exclusive. All

properties that accrue as fruit of their individual or joint labor and fruit of their properties

during marriage will be common properties of the spouses.

Properties before marriage

Properties derived during marriage:

- From fruits income or gains

Classification

Exclusive

Common

*Fruits does not follow principal. During marriage,

fruits of separate properties are still common. In other

words, all fruits derived during marriage are common

-

From gratuitous acquisitions:

a. For one of the spouse

b. For both of them

a. Exclusive

b. Common

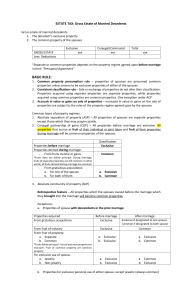

3. Absolute community of property (ACP)

Retrospective feature – All properties which the spouses owned before the marriage which

they brought into the marriage will become common properties

Exceptions:

a. Properties of spouse with descendants in the prior marriage

Properties acquired

From gratuitous acquisitions

From fruit of industry

From fruit of property:

a. Separate

b. Common

Before marriage

Exclusive

Exclusive

a. Exclusive

b. Exclusive

After marriage

Exclusive if designated to one spouse.

Common if designated to both spouse

Common

a. Exclusive

b. Common

*Fruits follow principal. Fruit of exclusive property are

exclusive. Fruit of common property are common

property

For exclusive use of spouse:

a. Jewelry

b. Non-jewelry

a. Exclusive

b. Exclusive

a. Common

b. Exclusive

b. Properties for exclusive personal use of either spouse, except jewelry (always common)

Prospective feature – all properties which the spouses may acquire during the marriage from

their separate or joint labor or industry are common properties

Exceptions:

a. Gratuitous acquisition received by either spouses (if designated for both = common)

b. Fruits of exclusive property

c. Properties acquired for exclusive personal use of either of spouse, except jewelry

Properties acquired

From gratuitous acquisition

Before marriage

Common

After marriage

From fruit of industry

From fruit of property

a. Separate property

Common

Common

a. Common

a. Exclusive

b. Common

b. Common

Exclusive if designated to one spouse.

Common if designated to both spouse

*Gratuitous

acquisitions

of

properties during marriage is a

separate property, fruit of

separate property is separate

property. Fruits follow principal

b. Common property

For exclusive personal use of

either spouse

a. Jewelry

b. Non-jewelry

a. Common

b. Exclusive

a. Common

b. Exclusive

Note:

1. A jewelry acquired through gratuitous acquisition during marriage is exclusive property

because it is a gratuitous acquisition regardless of the property acquired and a jewelry

acquired using exclusive property, e.g. jewelry acquired using cash donated during

marriage, is still exclusive

0

0