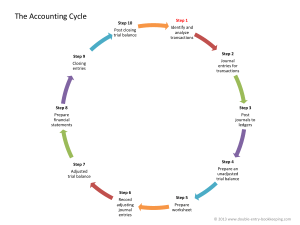

CLOSE-THE-BOOKS AUDIT WORK PROGRAM CLOSE-THE-BOOKS AUDIT WORK PROGRAM: SAMPLE 1 PROJECT TEAM: (LIST MEMBERS) Timing Date Comments Planning Fieldwork Report Issuance Time Audit Step Planning Conduct project planning, scope setting and auditee requests/coordination. Develop work programs and other reporting templates. Coordinate meetings with key process personnel. Review known best practices for initial benchmarking in the focus area. Collect and review online self-assessment forms (if applicable). Perform other planning and administrative duties. Fieldwork Obtain and review the policies and procedures for the closing process. Understand the organizational structure, scope of activities, and roles and responsibilities of personnel. Closing the Books Interview key accounting personnel. Determine if systems surrounding the closing process are fully integrated. Review current systems used (e.g., purchasing, AP, receiving, and consolidation). Determine if the company is complying with the close-the-books schedule as determined by management. Document personnel and processes for account reconciliation. Document processes and procedures for standard and nonstandard journal entries (JEs), including management review and approval. 2 Source: www.knowledgeleader.com Initial Index Time Audit Step Determine whether there is adequate segregation of duties within the account reconciliation process, journal posting and management review/approval. Agree on financial statements to the general ledger (GL) on a scope basis. Review intercompany reconciliation for accuracy and propriety (if applicable). Ensure that consolidating entries are eliminated (if applicable). Review cash flow statement preparation and supporting documentation. Clerically test financial statements for accuracy. Determine whether there are post-closing adjustments and review them for propriety. Obtain clarification from accounting personnel. Document the final management review process of financial statements. Process map the company’s close process. Determine whether there are internal control weaknesses within the close process and propose action items. Benchmark the company’s close process with other companies. Compare the company’s close process with known best practices. Conduct other meetings/interviews/discussions. Facilitate follow-up actions. Reporting Prepare a report on procedures, findings and recommendations. Total Project Effort Cost by Level Estimated Project Expenses Total Project Costs 3 Source: www.knowledgeleader.com Initial Index CLOSE-THE-BOOKS AUDIT WORK PROGRAM: SAMPLE 2 The close-the-books process is primarily concerned with ensuring compliance with Generally Accepted Accounting Principles (GAAP), including the timeliness of transaction recording. The processes and complexity of the accounting function will vary with the nature of the business being closed along with related financial reporting needs, such as SEC or regulatory requirements. Today, the Sarbanes-Oxley Act of 2002 and the related Public Company Accounting Oversight Board (PCAOB) Auditing Standard No. 2 require public companies to evaluate, certify and incorporate an additional public accountant attestation of the controls over financial reporting. Although this process involves significant effort and judgment by all parties involved, it forms the basis for an approach by any operational or financial audit team planning a review of the close-the-books process. GENERAL AUDIT PROCEDURES The following financial auditing procedures will provide a framework for approaching such a review. • Develop an understanding of the accounting applications and related processes and the chart of accounts (general ledger) structure. This step will help the team determine the level of complexity and risk involved in order to ensure that adequate resources and skills are applied to the review. • Identify and understand the significant risks related to the internal controls (manual, automated process, underlying IT controls) and the possibility of irregularities/error. SAS-99, also known as the fraud prevention and detection standard, requires that management performs a risk assessment and self-assessment based upon the risk and susceptibility to irregularities. Understanding these internal control risks will assist the team to tailor a work program to the organization under review. • Assess and redefine audit procedures based upon understanding the chart of accounts and accounting process (Step 1) and risk assessment (Step 2). The audit plan may consider a process flow of the closing and consolidation process (see Appendix A) and a related process narrative to ensure understanding. • Review and understand the closing schedule, including the cutoff and other accounting period-related limitations. The audit team may determine that certain cutoff-related testing, such as shipping concerning inventory and related payables, should be coordinated with period-end, etc. • Conduct fieldwork incorporating risk, audit planning and cutoff testing analysis. • Communicate audit results, as appropriate, during the review to confirm findings. Generate Tier II testing as required and develop recommendations for final report closing meetings. The internal audit team should incorporate additional considerations into the close-the-books process, such as management’s process for making estimates, accounting treatments and other financial reporting decisions. Many adjustments or reclassifications may be required to ensure that financial statements are fairly presented in conformance with GAAP. These processes will probably include eliminating entries for intercompany accounts, translation of currencies, or other special matters like contingent liabilities for legal issues or business closings. OTHER CONSIDERATIONS The general ledger and closing of the books will include significant application systems and network support that allows for an automated close. Often, subledger systems, such as inventory, payroll and cash management, will update the general ledger through the close process. These updates may or may not be integrated and various spreadsheets are usually used to perform extended analysis to derive at closing entries. Every organization follows a similar, although usually highly customized, process for closing the books. Audit teams should develop an understanding of this process by listening carefully to those that both supervise and perform the process. Pay particular attention to the application systems utilized and the manual review controls since these are often inherently risky and may present internal control issues or significant opportunities for improvement. 4 Source: www.knowledgeleader.com Segregation of duties should be evaluated to ensure the separation of processes to authorize, record, transact (book) and hold the custody of assets. In organizations with limited resources, some individuals may have access to perform incompatible duties that create serious control concerns. For example, some supervisors are responsible for reviewing the work of others and have access to system functionality to book transactions that they may be responsible for approving. In some cases, additional downstream detective or preventive controls may be included to ensure that the risk of error or irregularity is minimal. Internal audit may consider the use of computer-assisted auditing techniques such as ACL to review transactions from the general ledger system database. MANAGEMENT CONTROLS It is the responsibility of management to ensure that the control environment is both established and monitored to ensure personnel, processes and related results are under proper supervision. A few considerations for audit teams include: • Management documents and clearly communicates the objectives/standards for the close process. This may include communicating disciplinary action for untimely or inaccurate results and provisions for handling exceptions, unethical behavior or instances that may require approval or review by management personnel. • Management articulates the performance expectations related to the closing process and ties these to performance/compensation reviews. • Management documents job descriptions for positions with closing responsibilities, including the specific competency requirements (e.g., required educational background, prior work experience and past accomplishments) and details of tasks to be performed. • Management clearly defines and communicates responsibilities and delegations of authority for executing closing procedures and achieving objectives. • Management demonstrates its support for the development of necessary information systems by the commitment of appropriate human and financial resources. PROJECT TEAM: (LIST MEMBERS) Timing Date Comments Planning Fieldwork Report Issuance Time Audit Step Planning A. Audit Objective: Develop an understanding of the close-the-books (general ledger) process. Conduct project planning, scope setting and auditee requests/coordination. Note: Request this information before starting fieldwork to evaluate, agree upon the scope and determine testing with management. 5 Source: www.knowledgeleader.com Initial Index Time Audit Step Review the policies and procedures related to the close-the-books general ledger processing. Coordinate meetings with key process personnel. Review known best practices for initial benchmarking in the focus area. Develop a narrative describing the roles, responsibilities and processes for initiating, reconciling, calculating (amortization, capitalization, estimations), authorizing and recording related general ledger accounts. Determine the related IT applications and spreadsheet analysis tools that both interface and manually “feed” the close-the-books process. Consider related CAATs analysis and application or database controls for the scope of the review. Fieldwork B. Audit Objective: Understand and document the process of close the books or general ledger maintenance and accounting controls. Obtain and review the policies and procedures for the closing process. Understand the organizational structure, scope of activities, and roles and responsibilities of personnel. Understand the structure of the chart of accounts, related application interfaces and consolidation processes. Closing the Books Interview key accounting personnel. Determine if systems surrounding the closing process are fully integrated. Review current systems used (e.g., payroll, purchasing, AP, receiving, consolidation). Determine if the company is complying with the close-the-books schedule as determined by management. Note: A comprehensive close checklist of all close activities should be maintained and updated. The checklist may be organized by task and clearly identifies the responsible groups/individuals, interdependencies and deadlines. Document personnel and processes for account reconciliation. Document processes and procedures for standard and nonstandard JEs, including management review and approval. Process map the company’s close process. Determine whether there is adequate segregation of duties within the account reconciliation process, journal posting and management review/approval. Agree on financial statements to the GL on a scope basis. 6 Source: www.knowledgeleader.com Initial Index Time Audit Step Review intercompany reconciliations for accuracy and propriety (if applicable). Ensure that consolidating entries are eliminated (if applicable). Review cash flow statement preparation and supporting documentation. Clerically test financial statements for accuracy. Perform account reconciliations and analysis prior to closing the books. Determine whether there are post-closing adjustments and review them for propriety. Obtain clarification from accounting personnel. Document the final management review process of financial statements. Verify that the closing schedule is followed. Determine whether there are internal control weaknesses within the close process and propose action items. Benchmark the company’s close process with other companies. Compare the company’s close process with known best practices. All JEs are reviewed and approved by the manager. The supervisor reviews the input of exchange rates and backup documentation. The local accounting manager reviews and posts U.S. GAAP entries. Standard entries are used for consolidation processes to eliminate and reclassify intercompany activity. Transactions in systems are set up in U.S. GAAP. The consolidation policy and schedule are followed. The corporate accounting manager verifies that all entities are entered and complete. If additional JEs are made at entities (after uploading), entity data will turn to “obsolete” status (in the system) and must be uploaded again. Utilize elimination checklists. 7 Source: www.knowledgeleader.com Initial Index Time Audit Step Consolidation Consolidation checklists are maintained and reviewed by assigned personnel to ensure that all business units have been included. Eliminations are reviewed by the consolidation controller. Excel spreadsheets or similar working documents are used to compile financial results in U.S. GAAP, including the following (if applicable): • Consolidations and consolidating adjustments (if there are more than one entity/set of books) • Adjustments from local GAAP to U.S. GAAP • Other adjustments not recorded in local books but affecting U.S. books Financial analysis is performed on global results. Entities using systems are all on the same system. Entries in the GL and consolidation modules are reviewed and reconciled throughout the close process to ensure that the two agree. Nonsystem users have a preset mapping macro, which is used to upload trial balances to consolidated books. Discuss foreign currency translation processes and review account balances, as appropriate. Other Coordinate with the external auditor and obtain copies of any known concerns, passed adjustments, management recommendation letters, process memos or documentation. (Obtain in advance – consider meeting with the external audit manager on-site.) Reporting Prepare reports on procedures, findings and recommendations. 8 Source: www.knowledgeleader.com Initial Index Days 1 - 4 Period End Accounting/ finance staff perform periodend closing tasks. Accounting/ finance staff analyze the results. Accounting/ prepare journal entries. Journal entries are reviewed for reasonableness and should include backup and manager signatures. Were JEs approved? Balance sheet and income statements. Journal entries are posted in the system. Yes U.S. GAAP entries are posted by the accounting manager. Issues are resolved with the appropriate manager. Run a reevaluation. Run a translation. Day 4 This day is the official journal entry cutoff. No Hold closing meetings. Yes Backup j entries submitted corpo accoun mana No No Day 5 Run financial reports. Were JEs approved by a manager? No The period-close schedule is followed and managed by the corporate accounting manager. The corporate accounting manager reviews JEs for support and appropriate signoff. Journal entries are reviewed by the appropriate manager. Appendix finance A staff Each manager confirms that the area is completed and closed. Was the area complete and disclosed? Yes Closed Yes Was the close schedule completed?