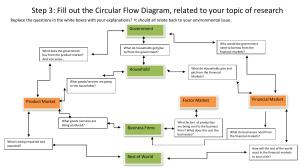

1. Difference between microeconomics and macroeconomics. 2. What is national income? National income means the value of goods and services produced by a country during a financial year. Thus, it is the net result of all economic activities of any country during a period of one year and is valued in terms of money. National income is an uncertain term and is often used interchangeably with the national dividend, national output, and national expenditure. We can understand this concept by understanding the national income definition. 3. What is economy growth and development? Generally economic development means development of economic condition of any country or area. It mainly refers to the long run or secular increase in per capita productivity. Economic development refers to increases in standard of living of a nation’s population associated with sustained growth from a simple, low-income economy to a modern, highincome economy. Economic Growth refers to an increase in the total amount of production and wealth in an economy. Economic growth means more output, while economic development implies both more output and changes in the technical and institutional arrangements by which it is produced and distributed. 4. What Is Per Capita Income? Per capita income is a measure of the amount of money earned per person in a nation or geographic region. Per capita income is used to determine the average per-person income for an area and to evaluate the standard of living and quality of life of the population. Per capita income for a nation is calculated by dividing the country's national income by its population. 5. Define the term ‘flow and stock’. Answer: Flow ‘Flow’ is a variable that is measured with reference to a period of time. Example: Flow of water in a river, income earned in a year, etc. Stock ‘Stock’ is a variable that is measured with reference to a particular point of time. Example: Water in a tank, wealth, bank balance on 31st March, etc. 6. The Classical Theory: The fundamental principle of the classical theory is that the economy is self‐regulating. Classical economists maintain that the economy is always capable of achieving the natural level of real GDP or output, which is the level of real GDP that is obtained when the economy's resources are fully employed. While circumstances arise from time to time that cause the economy to fall below or to exceed the natural level of real GDP, self‐adjustment mechanisms exist within the market system that work to bring the economy back to the natural level of real GDP. The classical doctrine—that the economy is always at or near the natural level of real GDP—is based on two firmly held beliefs: Say's Law and the belief that prices, wages, and interest rates are flexible. Say's Law. According to Say's Law, when an economy produces a certain level of real GDP, it also generates the income needed to purchase that level of real GDP. In other words, the economy is always capable of demanding all of the output that its workers and firms choose to produce. Hence, the economy is always capable of achieving the natural level of real GDP. 7. What Is Neoclassical Economics? Neoclassical economics is a broad theory that focuses on supply and demand as the driving forces behind the production, pricing, and consumption of goods and services. It emerged in around 1900 to compete with the earlier theories of classical economics. KEY TAKEAWAYS Classical economists assume that the most important factor in a product's price is its cost of production. Neoclassical economists argue that the consumer's perception of a product's value is the driving factor in its price. They call the difference between actual production costs and retail price the economic surplus. The term neoclassical economics was coined in 1900.1 Neoclassical economists believe that a consumer's first concern is to maximize personal satisfaction. Therefore, they make purchasing decisions based on their evaluations of the utility of a product or service. This theory coincides with rational behavior theory, which states that people act rationally when making economic decisions. For example, you desire to purchase designer apparel because of the attached brand label. Besides, the clothing production cost may be insignificant. Here, the perceived value of the brand label exceeded its input cost, creating an 'economic surplus. 8. What is Post-Keynesian Economics (PKE)? Post-Keynesian Economics (PKE) is a school of economic thought which builds upon John Maynard Keynes's and Michal Kalecki's argument that effective demand is the key determinant of economic performance. 9. What is Dynamic economics? In the real world, economic variables like population, capital, techniques of production, fashions, habits, etc. do not change at a constant rate. The rate of change is different at different times. According to Prof. Hicks, “Economic dynamics refers to that part of economic theory in which all quantities must be dated.” For example, the population of a country may increase at a rate of 2% in the first year; 3% in the second year and 5% in the third year, if the other economic variables change at unequal rates, the rate of output will also change at different times. In a dynamic state, there is uncertainty of every change. So, it is not possible to make correct predictions. 10. What is Keynes Budget? Keynesians believe that, because prices are somewhat rigid, fluctuations in any component of spending—consumption, investment, or government expenditures—cause output to change. If government spending increases, for example, and all other spending components remain constant, then output will increase. 11. What is financial Management System? A financial management system is the software and processes used to manage income, expenses, and assets in an organization. In addition to supporting daily financial operations, the purpose of a financial management system is to maximize profits and ensure long-term enterprise sustainability. They help finance teams: Streamline invoicing and bill collection Optimize daily, monthly, and yearly cash flow Maintain audit trails and comply with accounting regulations 12. What is budgetary system? The budget system of the United States Government provides the means by which the Government decides how much money to spend and what to spend it on, and how to raise the money it has decided to spend. 13. What is inductive? The inductive method involves collection of facts, drawing conclusions from them and testing the conclusions by other facts. 14. What is deductive? Deductive reasoning is used extensively in economics as we apply theory to a particular case or instance. For example, any supply and demand analysis you do is the application of generally accepted principles about demand and about supply; therefore, you are engaging in deductive logic. 15. Why economics is the queen of social science? Economics is the queen of social science. It is the study of house society uses its limited. It is concerned with production distribution and consumption of goods and services. It examines how various factors affect the society the use of goods and services, the involvement of individuals, businessmen, and government. 16. Production system i. Agro LED production system: The Agro LED production system is an economic system in which the production and distribution of goods and services are organized around the use of LED technology. This system is characterized by the use of LED lights to grow crops, the use of LED lighting to improve the efficiency of manufacturing processes, and the use of LED lighting to provide lighting for homes and businesses. The Agro LED production system is based on the premise that LED technology can be used to improve the efficiency of agriculture, manufacturing, and lighting. 17. Importance of macroeconomics. a) Understand working of macroeconomic: What is true and valid in case of individual may not be valid for the economy as a whole. What is true for individual and true for the whole economy. b) Nature of macro issues: it explains causes of macro problems and help to solve them. It is easy to find individual problem but difficult to find macro problems. c) Accelerating economic growth: it provide us knowledge and techniques as to how to achieve self-sustained economic growth. d) Understanding business cycles: annual planning program, and other development planning is not possible without knowledge of macroeconomic. e) Forming government macroeconomic policies: with the knowledge of macroeconomic; governments can formulate proper policies to tackle them. f) Individual decision making: the understanding about the working of the economy as whole helps the individuals to take better decisions. g) Importance in business: it also helps a good deal to businesses or their managers who are faced with various decision making problems. h) Foreign trade control: export, import, balance of payments, exchange rates are highly influenced by the macroeconomic activities of country i) Proper planning: annual planning program, and other development planning is not possible without knowledge of macroeconomic. j) Budget formation: it provides information and effective budget formulation is not possible without proper analysis of macro economic. 18. Types of economic system. Socialism – Command economic system A command economic system is often referred to as a socialist or communist system. Under this structure, power is centralised either to the government or a sole ruler. In turn, they decide the rules of the game and command how economic interactions take place. Economic decisions such as what goods to produce, how much to produce, and its price are decided upon by central powers. So it’s up to them to decide whether it is socially optimal to make iPhones or PlayStations, or whether it’s best to divert these resources to house building or agriculture. Under a command economic system, central powers own the means of production, so can, therefore, shift it to where they see fit. For instance, if the nation’s central powers want to start making more steel, they may move workers from a construction site and transfer them to a steel factory. Moving workers may be necessary in order to fulfill long-term economic plans created by central planners. These long-term plans are a key part of command economies – such as the five-year plans adopted in the Soviet Union. In order to organise an economy from the top-down, clear and concise information needs to be passed through the chain of command – which is why a plan is necessary for everyone to understand their role. Whilst planning can be effective, the issue with such command systems is slow and sluggish to change to economic trends. Where people are wanting more of Product A, central powers produce more of Product B. Examples include North Korea, Cuba, and the former Soviet Union. Capitalism – Market economic system A capitalist economic system is where the means of production is owned and controlled by private enterprise rather than the government. Instead of government dictating what goods and services should be produced, these are driven by supply and demand mechanisms. When consumers demand goods, it sends a signal to businesses for them to produce more. Equally, when demand for goods falls, it sends a signal to businesses to produce less. This in turn forces the business to offer new products that consumers may desire instead. Under this form of economic system, government involvement is almost non-existent – other than enforcing law and legal contracts. Instead, the economy is regulated by the fluctuations in supply and demand, as well as other factors such as brand trust and competition. 19. Surplus economic unit and depreciate: For example, surplus units are defined as economic units whose income exceeds spending on goods and services. Conversely, deficit units are those economic units whose spending on goods and services is in excess of their income. 20. What Is Political Economy? Political economy is an interdisciplinary branch of the social sciences that focuses on the interrelationships among individuals, governments, and public policy. 21. What Is Full Employment? Full employment is an economic situation in which all available labor resources are being used in the most efficient way possible. Full employment embodies the highest amount of skilled and unskilled labor that can be employed within an economy at any given time. What Is Unemployment? The term unemployment refers to a situation where a person actively searches for employment but is unable to find work. Unemployment is considered to be a key measure of the health of the economy. 22. What Is Fiscal Policy? Fiscal policy refers to the use of government spending and tax policies to influence economic conditions, especially macroeconomic conditions. These include aggregate demand for goods and services, employment, inflation, and economic growth. During a recession, the government may lower tax rates or increase spending to encourage demand and spur economic activity. Conversely, to combat inflation, it may raise rates or cut spending to cool down the economy. What Is Monetary Policy? Monetary policy is a set of tools used by a nation's central bank to control the overall money supply and promote economic growth and employ strategies such as revising interest rates and changing bank reserve requirements. 23. Business Cycles: refer to fluctuations in output and employment with alternating periods of boom and recession, business fluctuation over time period. https://docs.google.com/presentation/d/1GsVGh9M61_n0u8vy_SY7D5l7Y2o49R_/edit#slide=id.p4 24. What Is Inflation? Inflation is a rise in prices, which can be translated as the decline of purchasing power over time. The rate at which purchasing power drops can be reflected in the average price increase of a basket of selected goods and services over some period of time. The rise in prices, which is often expressed as a percentage, means that a unit of currency effectively buys less than it did in prior periods. Inflation can be contrasted with deflation, which occurs when prices decline and purchasing power increases. What Is Deflation? Deflation is a general decline in prices for goods and services, typically associated with a contraction in the supply of money and credit in the economy. During deflation, the purchasing power of currency rises over time. 25. GDP and GNP What Is Gross Domestic Product (GDP)? Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country’s economic health. What Is Gross National Product (GNP)? Gross national product (GNP) is an estimate of the total value of all the final products and services turned out in a given period by the means of production owned by a country's residents. 26. NNP and NDP What Is Net National Product (NNP)? Net national product (NNP) is the monetary value of finished goods and services produced by a country's citizens, overseas and domestically, in a given period.1 It is the equivalent of gross national product (GNP), the total value of a nation's annual output, minus the amount of GNP required to purchase new goods to maintain existing stock, otherwise known as depreciation. What Is Net Domestic Product (NDP)? Net domestic product (NDP) is an annual measure of the economic output of a nation that is calculated by subtracting depreciation from gross domestic product (GDP). 27. What Is Personal Income? Personal income refers to all income collectively received by all individuals or households in a country. Personal income includes compensation from a number of sources, including salaries, wages, and bonuses received from employment or self-employment, dividends and distributions received from investments, rental receipts from real estate investments, and profit sharing from businesses.1 What Is Disposable Income? Disposable income, also known as disposable personal income (DPI), is the amount of money that an individual or household has to spend or save after income taxes have been deducted. 28. NI AT MARKET PRICE AND FACTOR COST https://enotesworld.com/relationship-between-concepts-of-national-income-at-marketprice-and-factor-cost/ 29. Difference between security market line and capital market line 30. What is development cap? The development gap refers to the widening gap between the richest (most developed) and poorest (least developed) countries of the world. Development in this sense can be referred to as either economic development where the county has an increase in wealth, or human development where quality of life is improved for the people who live there. 31. Ultimate objective of macroeconomics 32. What Is the Circular Flow Model? The circular flow model demonstrates how money moves through society. Money flows from producers to workers as wages and flows back to producers as payment for products. a. Household Sector: Households provide factor services to firms, government and foreign sector. In return, it receives factor payments. Households also receive transfer payments from the government and the foreign sector. Households spend their income on: (i) Payment for goods and services purchased from firms; (ii) Tax payments to government; (iii) Payments for imports. b. Firms: Firms receive revenue from households, government and the foreign sector for sale of their goods and services. Firms also receive subsidies from the government. Firm makes payments for: (i) Factor services to households; (ii) Taxes to the government; (iii) Imports to the foreign sector. c. Government: Government receives revenue from firms, households and the foreign sector for sale of goods and services, taxes, fees, etc. Government makes factor payments to households and also spends money on transfer payments and subsidies. d. Foreign Sector: Foreign sector receives revenue from firms, households and government for export of goods and services. It makes payments for import of goods and services from firms and the government. It also makes payment for the factor services to the households. The savings of households, firms and the government sector get accumulated in the financial market. Financial market invests money by lending out money to households, firms and the government. The inflows of money in the financial market are equal to outflows of money. It makes the circular flow of income complete and continuous. https://www.yourarticlelibrary.com/macro-economics/circular-flow-of-income-in-afour-sector-economy/30259 33. Effective demand chart 34. Theory of income and employment 35. What is the Gini Coefficient? The Gini coefficient (Gini index or Gini ratio) is a statistical measure of economic inequality in a population. The coefficient measures the dispersion of income or distribution of wealth among the members of a population. 36. What is MPC? MPC is the ratio of change in consumption to change in income. Cha 37. Comparison of economic system Comparative Economic Systems is the sub-classification of economics dealing with the comparative study of different systems of economic organization, such as capitalism, socialism, feudalism and the mixed economy. income. 38. What Is Financial Economics? Financial economics is a branch of economics that analyzes the use and distribution of resources in markets. Financial decisions must often take into account future events, whether those be related to individual stocks, portfolios, or the market as a whole. KEY TAKEAWAYS Financial economics analyzes the use and distribution of resources in markets. It employs economic theory to evaluate how time, risk, opportunity costs, and information can create incentives or disincentives for a particular decision. Financial economics often involves the creation of sophisticated models to test the variables affecting a particular decision.