21/9/2022

Lecture 5:

Financing & Valuation

Part 1

1

Learning Outcomes

To understand:

Valuing

What

businesses or project analysis;

is capital budgeting and the different methods:

Net

Present Value using WACC

Net

Present Value using Flow-to-equity (FTE) (Week 6)

Adjusted

Issues

Present Value (Week 7)

and considerations when using NPV (Week 7)

2

1

21/9/2022

Recall from Week 4

In order to value a project,

you require an appropriate

discount rate

The value of the new project

will add to overall equity value

of the business. You therefore

need to know the value of the

project.

You need a new COC, suitably

adjusted to the new gearing

level, to value the project

In order to calculate the new

COC, you need to know the

new MV of debt and equity

after the project’s acceptance

3

Capital Budgeting at its Simplest

The value of a business / project is in simple terms, the sum of the

present value of all its expected future cash flows:

𝐶𝐹

1 𝑟

Through this simple formula, we are simply trying to determine what the

business/project is worth today, given an appropriate discount rate

Recall that the discount rate ‘r’, reflects the expectations on a set of current

and future conditions – firm and/or market – that is taken into consideration

when valuing a firm/asset

By doing this, we are trying to decide whether this business/project will

add value to our firm

4

2

21/9/2022

Capital Budgeting at Its Simplest

The simplest – and most common – method of capital budgeting is the Net Present Value (NPV)

method

NPV expands the earlier definition to account for the initial outlay / cost of the investment:

𝐶𝐹

𝑁𝑃𝑉

𝐼𝑛𝑖𝑡𝑖𝑎𝑙 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑖𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡

1 𝑟

For example, ABC has a project that is expected to generate revenues of $100,000 per year

for 5 years. Investing in this project will require an initial outlay of $150,000. Assuming r = 5%,

the NPV of this project is:

100,000

100,000

100,000

100,000

$100,000

$150,000

1 0.05

1 0.05

1 0.05

1 0.05

1 0.05

= $282,947.67 (this is also known as Base-case NPV)

General rule of thumb:

If NPV > 0, then we accept the project

If NPV < 0, then we reject the project

5

Net Present Value using WACC (NPV-WACC)

Same as base-case NPV method

2 Differences

Use of Free Cash Flow (FCF)

Discounted using WACC

PV

FCF1

FCF2

FCFH

PVH

...

1

2

H

(1 r ) (1 r )

(1 r )

(1 r ) H

Horizon Value PVH

FCFH 1

wacc g

r = WACC

PV (free cash flows)

PV (horizon value)

𝑊𝐴𝐶𝐶

1

𝑇 𝑟

𝐷

𝑉

𝑟

𝐸

𝑉

NPV = PV – initial investment

6

3

21/9/2022

Net Present Value using WACC (NPV-WACC)

Some important points on NPV-WACC:

FCF

= cash company generates less cash outflows to support

operations and maintain capital assets

Excludes

non-cash expenses, interest payments and borrowings expenses

Includes

taxes, spending on equipment and assets, and changes in working

capital from the balance sheet (related to the project evaluated)

On

the use of WACC, there are two possible scenarios

Project

has no impact on company’s debt-equity ratio = fixed-debt

Project

impacts company debt-equity ratio = rebalancing required

7

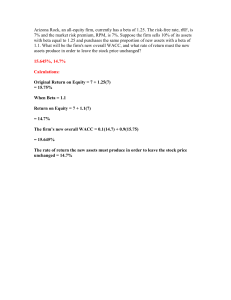

NPV-WACC Example – Fixed Debt

XYZ is considering diversifying its operations by setting up a manufacturing division to produce

medical masks. Its first potential project entails buying 2 machines for a total of RM600,000.

This will produce annual revenue of RM3 million, for 10 years. The cost of production is

expected to be 40% of the revenue and the depreciation is RM50,000 per year, using the

straight-line method. No inflation is considered in this case. After 10 years, this project will

be scrapped to zero value.

Sixty per cent (60%) of the initial cost of the project will be financed by debt. The loan will be

irredeemable and carry an annual interest rate of 6%. The balance of finance will come from a

placement of new equity. It is assumed that there are no issue costs associated to this.

The manufacturing industry (for medical masks) has an average geared equity beta of 1.8 and

a debt-to-equity ratio of 1:5 by market values. XYZ’s current geared equity beta is 1.6 and

30% of its long-term capital is represented by debt that’s generally seen as risk-free. The riskfree rate is 2.5% a year and the expected return on an average market portfolio is 8%.

Corporation tax is set at 30% per annum.

8

4

21/9/2022

NPV-WACC Example – Fixed Debt

Lay down the facts:

Initial investment = RM600,000

Annual revenue = RM3,000,000 for 10 years

Cost of production = 40% of revenue

Depreciation = RM50,000

Project is financed 60/40 debt-equity

Cost of debt = 6% p.a.

Industry geared equity beta = 1.8

Industry debt-equity ratio = 1:5

XYZ equity beta = 1.6; 30% of long-term capital is risk-free

Risk-free rate = 2.5% p.a.

Market portfolio return = 8%

Tax = 30%

9

NPV-WACC Example – Fixed Debt

Start by calculating FCF

RM Calculation

Annual Revenue

Less: Cost of Production

(40%)

3,000,000

(1,200,000) 3,000,000 x 0.4

Profit before Tax

1,800,000

Less: Tax (30%)

(540,000) 1,800,000 x 0.3

FCF for 1 year

1,260,000

Assumption: The RM3,000,000 revenue is in cash

10

5

21/9/2022

NPV-WACC Example – Fixed Debt

We now need a few things, so let’s work backwards:

We

To

do so, we need Ke and Kd (Kd already provided)

We

To

need to calculate WACC

need to calculate Ke

do so, we need to calculate company beta

11

NPV-WACC Example – Fixed Debt

Step 1: Calculate Company Beta

𝛽

𝛽 ∗

𝐷

𝐷

𝐸

𝛽 ∗

𝐸

𝐷

𝐸

From the question:

Industry debt-equity ratio = 1:5

so we assume that XYZ has the same debt-equity ratio: D = 1, E = 5

XYZ’s equity beta = 1.6

XYZ’s debt beta = risk-free = 0

0

1

1

5

1.6

5

1

5

1.333

12

6

21/9/2022

NPV-WACC Example – Fixed Debt

Step 2: Calculate Cost of Equity

𝑘

𝑟

𝛽 𝑟

𝑟

From the question:

Rf = 2.5%

Rm = 8%

Company Beta (calculated earlier) = 1.333

Therefore, Ke

0.025

1.333 0.08

0.025

0.098315

9.83%

13

NPV-WACC Example – Fixed Debt

Step 3: Calculate WACC of the project

𝑊𝐴𝐶𝐶

1

𝑇 𝑘

𝐷

𝐷

𝐸

𝑘

𝐸

𝐷

𝐸

From the question:

T = 30%

Kd = 6%

Ke (calculated earlier) = 10.04%

Project is financed 60/40 debt-equity

Therefore, WACC:

1

0.3 0.06

0.6

0.098315

0.4

= 0.06453 = 6.453%

14

7

21/9/2022

NPV-WACC Example – Fixed Debt

Step 4: Calculate NPV. Since FCF is constant, we can use the

PV of Annuity Formula

1

1 𝑊𝐴𝐶𝐶

𝑁𝑃𝑉 𝐹𝐶𝐹

𝐼𝑛𝑖𝑡𝑖𝑎𝑙 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡

𝑊𝐴𝐶𝐶

FCF = RM1.26mn; WACC = 6.534%; Initial investment = RM0.6mn

Therefore:

𝑁𝑃𝑉

𝑅𝑀1.26𝑚

1

1

1.06453

0.06453

= RM8.478mn

𝑅𝑀0.6𝑚

15

NPV-WACC Example – Rebalanced D/E Ratio

ABC is considering diversifying its operations by setting up a manufacturing division to

produce medical masks. Its first potential project entails buying 2 machines for a total of

RM600,000. This will produce annual revenue of RM5 million, for 10 years. The cost of

production is expected to be 50% of the revenue and the depreciation is RM60,000 per

year, using the straight-line method. No inflation is considered in this case. After 10 years,

this project will be scrapped to zero value.

Sixty per cent (60%) of the initial cost of the project will be financed by debt. The loan

will be irredeemable and carry an annual interest rate of 5%. The balance of finance will

come from a placement of new equity. It is assumed that there are no issue costs

associated to this.

The manufacturing industry (for medical masks) has an average geared equity beta of 1.2

and a debt-to-equity ratio of 1:6 by market values. Frost’s current geared equity beta is

1.6 and 30% of its long-term capital is represented by debt that’s generally seen as riskfree. The risk-free rate is 4% a year and the expected return on an average market

portfolio is 10%. Corporation tax is set at 30% per annum.

16

8

21/9/2022

NPV-WACC Example – Rebalanced D/E Ratio

FCF = RM5,000,000 – 2,500,000 – 750,000 = RM1,750,000

See if you can figure it out!

In this question, we assume that the project is financially significant enough to alter ABC’s

capital structure and subsequently, WACC – which affects our NPV calculation

In order for ABC to maintain its current capital structure, it would have to rebalance it’s

D/E ratio

There are 4 steps to this:

Step 1: Unlever / ungear equity beta

𝛽

𝛽 ∗

𝐷

𝐷

𝐸

𝛽 ∗

𝐸

𝐷

𝐸

Step 2: Re-calculate the levered equity beta using new debt-equity ratio

𝐷

𝛽

𝛽

𝛽

𝛽

𝐸

Step 3: Recalculate cost of equity using new levered equity beta (use CAPM)

Step 4: Recalculate WACC (as normal)

17

NPV-WACC Example – Rebalanced D/E Ratio

𝛽

Step 1: Ungear equity beta

𝛽 ∗

𝛽 ∗

0

𝛽

1.6

Step 2: Re-calculate the levered equity beta using new debt-equity ratio

𝛽

𝛽

1.37

1.37

𝛽

1.37

0

.

.

3.425

Step 3: Step 3: Recalculate cost of equity using new levered equity beta

𝑘

𝑟

𝑘

0.04

𝛽 𝑟

𝑟

3.425 0.1

0.04

0.2455

24.55%

18

9

21/9/2022

NPV-WACC Example – Rebalanced D/E Ratio

Step 4: Re-calculate WACC

𝑊𝐴𝐶𝐶

1

𝑇 𝑘

𝑊𝐴𝐶𝐶

1

0.3 0.05 0.6

𝑘

0.2455 0.4

0.021

0.0982

0.1192

11.92%

Finally, Calculate NPV

𝑁𝑃𝑉

𝐹𝐶𝐹

𝑁𝑃𝑉

𝑅𝑀1.75𝑚

𝐼𝑛𝑖𝑡𝑖𝑎𝑙 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡

.

.

𝑅𝑀0.6𝑚

𝑅𝑀9.32𝑚

19

Net Present Value using WACC

Fixed‐Debt

Rebalanced

Step 1:

Calculate FCF

Step 2:

Calculate

Company Beta

Step 1: Calculate

FCF

Step 2: Ungear

Equity Beta

Step 4:

Calculate

WACC

Step 3:

Calculate Cost

of Equity

Step 4: Recalculate

Cost of Equity

using new Beta

Step 3: Recalculate

levered equity Beta

Step 5: Recalculate

WACC

Step 6: Calculate

NPV

Step 5:

Calculate NPV

20

10

0

0