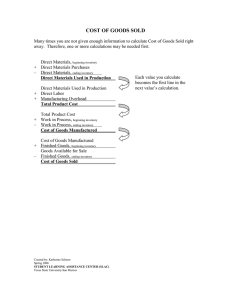

SHEENA MARIE C. SIRIOS BSMA3 E1-6 COST FLOW • Direct material- Direct material cost indicates the purchase price of raw material that is used in the manufacturing of the product. • Direct labor- These are the costs related to the payment of wages and salaries to workers who are involved directly in the production process. • Factory overheads- Involves all the direct production costs connected with the production of goods. It shall exclude direct labor and direct materials. E1-7 STATEMENT OF COST OF GOODS MANUFACTURED Direct Materials Material Inventory, beg. $25,000 Materials purchased 21,000 Materials available for use 46,000 Less: Materials inventory, end (22,000) Total materials used 24,000 Less: Indirect materials used (1,000) Direct materials used $23,000 Direct labor cost 18,000 Factory overhead 12,000 Total manufacturing costs 53,000 Work in process inventory, beg. 24,000 Total cost of work in process 77,000 Less: Work in process inventory, end (20,000) Cost of goods manufactured $57,000 COST OF GOODS SOLD Cost of goods manufactured $57,000 Finished goods inventory, beg 32,000 Less: finished goods inventory, end 30,000 Cost of goods sold $59,000 E1-9 DETERMINING MATERIALS, LABOR, AND COST OF GOODS SOLD A. Direct materials used $205,000 Direct materials, end 95,000 Less: Direct materials, beg Direct materials purchased (90,000) $210,000 B. Total manufacturing costs $675,000 Direct materials used (205,000) Factory overhead (175,000) Direct labor cost incurred $295,000 C. Cost of goods available for sale Less: Finished goods, end Cost of goods sold $775,000 (75,000) $700,000 D. Sales $900,000 Less: Cost of goods sold (700,000) Gross profit $200,000