Agricultural Accounting: Biological Assets & Fair Value

advertisement

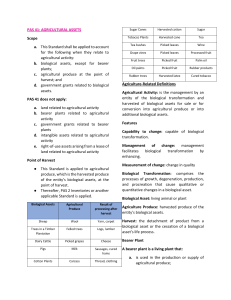

Government Accounting & Accounting for Non-Profit Organizations Zeus Vernon B. Millan Agriculture Chapter 8 Agricultural Activity Agricultural Activity is the management by an entity of the biological transformation and harvest of biological assets for sale, including exchange or non-exchange transactions, or for conversion into agricultural produce, or into additional biological assets. 1 Common Features of agricultural activities a. Capability to change b. Management of change c. Measurement of change 2 Definitions • Biological Asset – is a living animal or plant • Agricultural Produce – is the harvested product of the entity’s biological assets. 3 Biological Assets Agricultural produce Inventory Trees in a plantation forest Felled Trees Logs, Lumber Plants Harvested cane Sugar Dairy cattle Corn Corn Starch Sheep Cotton Clothing Pigs Milk Cheese Bushes Wool Yarn, Carpet Vines Carcass Ham Fruit trees Leaf Tea Grapes Wine Picked fruit Processed fruit 4 Measurement • Biological assets - initially and subsequently measured at fair value less costs to sell. Gain or loss arising from measurement are recognized in surplus or deficit. • Biological assets whose fair value cannot be reliably determined on initial recognition are initially measured at cost and subsequently measured at cost less accumulated depreciation and accumulated impairment losses. • Agricultural produce - initially measured at fair value less costs to sell at the point of harvest. 5 Determination of Fair value If there are more than one active markets, the entity shall use the price in the market expected to be used. 6 Determination of Fair value If there is no active market, the entity shall estimate the market price based on one of the following: • Most recent market transaction price • Market prices for similar assets with adjustment to reflect differences • Sector benchmarks • Present value of expected net cash flows from the asset. 7 Disclosures • Consumable and Bearer biological assets Consumable Biological Assets – are those that are to be harvested as agricultural produce or to be sold or distributed as biological assets. Bearer Biological Assets – are those that are self-generating and are used repeatedly for more than one year. • Mature and immature biological assets Mature Biological Assets – are those that have attained harvestable specifications or are able to sustain regular harvests. • The amount of change in fair value less costs to sell due to physical changes and due to price changes. 8 END