")

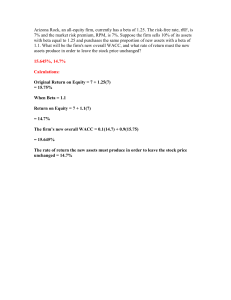

Case 1: Marriott Corporation Submitted on October 7, 2019 1. Estimate asset betas for the lodging, restaurant, and contract service divisions. We estimate asset betas of Lodging and Restaurant division by using the asset beta of comparable company. Since there is some extreme value in the betas of comparable company, we choose to use median of their beta instead of the average. The table below shows the value of each factor and their source Factor Source Value 𝜷𝒂𝒔𝒔𝒆𝒕(𝑳𝒐𝒅𝒈𝒊𝒏𝒈 𝒅𝒊𝒗𝒊𝒔𝒊𝒐𝒏) Comparable company’s asset beta 0.32 𝜷𝒂𝒔𝒔𝒆𝒕(𝑹𝒆𝒔𝒕𝒂𝒖𝒓𝒂𝒏𝒕 𝒅𝒊𝒗𝒊𝒔𝒊𝒐𝒏) Comparable company’s asset beta 0.68 Since the asset beta for the company is the weighted average of each division’s beta. We can derive the asset beta for contract division. The formula to calculate asset beta by equity beta is below: 𝛽45567 = 𝐸 𝐷 × 𝛽6<=>7? + × 𝛽B6C7 𝑉 𝑉 And we assume that 𝛽B6C7 = 0. Factor 𝛽45567(EFGH4I?) Asset proportion of lodging division Asset proportion of Source Derived from 𝛽6<=>7?(EFGH4I?) provided by the case Derived from the proportion of identifiable asset (Exhibit 2) Derived from the proportion of 1 Value 0.39 61% 12% restaurant division identifiable asset (Exhibit 2) Asset proportion of Derived from the proportion of contract division identifiable asset (Exhibit 2) 𝜷𝒂𝒔𝒔𝒆𝒕(𝑪𝒐𝒏𝒕𝒓𝒂𝒄𝒕) Calculated by method mentioned before 27 % 0.41 2. Calculate equity betas for each of the three divisions using their respective target leverage ratios. As we already have the asset beta, we can calculate equity beat by the formula below, as we assume 𝛽B6C7 = 0 𝛽6<=>7? = 𝛽45567 ∗ 𝑉 𝐸 Factor Source Lodging Restaurant Contract Debt percentage Table A of Case 74% 42% 40% Equity percentage Table A of Case 26% 58% 60% 𝜷𝒆𝒒𝒖𝒊𝒕𝒚 Calculate by formula above 1.23 1.13 0.71 3. Using the asset betas and equity betas in Questions 1 and 2, calculate the all equity opportunity cost of capital (ra ) for each of the divisions as well as the cost of equity (re ) for each of the divisions at their respective target leverage ratios. For each division, compare the ra and the re . Why are the re’s larger than the ra’s ? Marriott used the Capital Asset Pricing Model (CAPM) to estimate the cost of equity: 2 Expected return = Risk-free rate + equity beta*[Risk premium] As stated in the case, lodging assets like hotels, had long useful lives, so we choose the 30-year government bond rate of 8.95% (see in Table B)as the riskfree rate for lodging division; as for the restaurant and contract services divisions, we use shorterterm government bond of 6.90% as the riskfree rate, because those assets had shorter useful lives. Market risk premium can be obtained from Exhibit 5: We prefer the arithmetic average, because CAPM is a single-period model and arithmetic mean is better at estimating the average risk premium for the next year. So the Spread between S&P 500 Composite Returns and LongTerm U.S. Government Bond Returns from 1926 to 1987(which is 7.43%) can be used as the risk premium of the lodging division, while Spread between S&P 500 Composite Returns and Short-Term Treasury Bill Returns from 1926 to 1987(which is 8.47%) can be used as the risk premium of the restaurant and contract divisions. Factor Lodging Restaurant Contract rf 8.95% 6.90% 6.90% β(equity) 1.23 1.13 0.71 rm-rf 7.43% 8.47% 8.47% re 18.08% 16.45% 12.88% Marriott measured the opportunity cost of capital using the weighted average cost of capital (WACC): 3 Ra=WACC = (1-t)rd (D/V) + re (E/V) The tax rate can be calculated by (income tax)/ (income before tax) in 1987, the data is given in Exhibit 1: Period Income before income tax Income tax Tax rate 1987 398.90 175.90 0.44 Target D/V and E/V and the cost of debt, which is calculated by adding specific risk premium to the riskfree rate are shown in the Table A: Rd= riskfree rate + Debt Rate Premium above Government Calculation for all equity opportunity cost of capital (ra) Factor Lodging Restaurant Contract 1-t 0.56 0.56 0.56 D/V 0.74 0.42 0.40 E/V 0.26 0.58 0.60 rf 8.95% 6.90% 6.90% Credit Spread 1.10% 1.80% 1.40% rd 10.05% 8.70% 8.30% ra 8.86% 11.59% 9.58% The reason why re’ are larger than the ra’s is that the equity holder often takes more risk than the creditors, so re is usually higher than rd. Mathematically, according to the formula of WACC: ra=(1-t)*rd*(D/V) + re*(E/V) ≤ (1-t)*re*(D/V)+re*(E/V)=re-t*re*D/V ≤ re 4 4.If Marriott used a single cost of capital for evaluating investment projects for all lines of business, what would happen to the company over time. We use the formula mentioned in the case to calculate Marriott’s WACC. (The tax rate is been calculated by income tax/ income before tax): WACC = (1 − t)r (D/V) + r (E/V). As stated in the case, Marriott used the cost of long-term debt for its Lodging cost-of-capital calculation and short-term one for the other two divisions.Therefore, we choose corresponding rates to do the evaluation. Marriott’s three divisions are from different business area and have totally different leverage ratios. If Marriott used a single cost of capital(𝑊𝐴𝐶𝐶RFGH4I? = 9.9%) for evaluating all its divisions, proper investment opportunities could be rejected while improper ones be accepted. An investment opportunity which will yield a positive NPV for Lodging division(𝑊𝐴𝐶𝐶VFBW>IW = 8.86%) could be rejected. While at the same time, projects resulting in a negative NPV and reduced cash flow in restaurant division (𝑊𝐴𝐶𝐶Z6574=[4I7 = 11.59%)could be accepted. Over time, Lodging and Contract Service divisions would have to take improperly high risk, while restaurant division would suffer a loss. This will terribly harm Marriott’s performance and destroy the interest of shareholders. 5