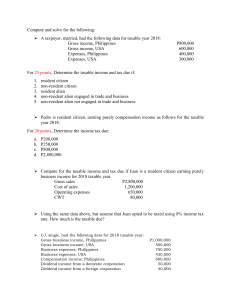

UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 3.1 Taxpayer and Tax base Classification of individual taxpayers 1. Citizens Resident citizens (RC) Non-resident citizens (NRC) means a Filipino citizen: Who establishes to the satisfaction of the Commissioner the fact of their physical presence abroad with a definite intention to reside therein; Who leaves the Philippines during the taxable year to reside abroad, either as immigrant or for employment on a permanent basis; Who works and derive income from abroad and whose employment thereat requires him to be physically present abroad most of the time during the taxable year Who is previously considered as a non-resident and who arrives in the Philippines at anytime during the taxable year to reside thereat permanently shall be considered non-resident for the taxable year in which he arrives in the Philippines with respect to his income derived from sources abroad until the date of his arrival; Who stays outside the Philippines more than 183 days. 2. Aliens Resident aliens (RA) – means an individual whose residence is within the Philippines and who is not a citizen thereof. Non-resident aliens (NRA) – means an individual whose residence is not within the Philippines and who is not a citizen thereof Engaged in trade of business within the Philippines (NRAETB) Not engaged in trade or business within the Philippines (NRANETB) Note: a) The term trade or business includes the performance of the functions of a public office b) The term trade, business or profession shall not include performance of services by the taxpayer as an employee c) A non-resident alien individual who shall come in the Philippines and stay therein for an aggregated period of more than 180 days during the calendar year shall be deemed a non-resident alien doing business in the Philippines. General Principles of Individual tax situs: Only resident citizens are taxable for income derived from sources within and without the Philippines. All other individual income taxpayers are taxable only for income derived from sources within the Philippines A seaman is considered as an OCW provided the following requirements are met: Receives compensation for services rendered abroad as a member of the complement of a vessel; and Such vessel is engaged exclusively in international trade Note: An overseas contract worker (OCF) is taxable only on income derived from sources within the Philippines Different individual income taxes: 1. Income tax – basic tax is at 5% to 32% (progressive tax rate) 2. Final tax on passive incomes (proportional tax rate) 3. Capital gains tax on capital gains Formula for Individual Income Tax: Gross income (excluding passive income & capital gains) xx Less Allowable deduction Net taxable income Less Tax rate Net income tax due Less Tax credit if any Tax payable or still tax due if any xx xx % xx xx xx Current progressive tax rates table: Over P10,000 30,000 70,000 140,000 250,000 500,000 But not over P10,000 30,000 70.000 140,000 250,000 500,000 - The tax shall be 5% P500 2,500 8,500 22,500 50,000 125,000 Plus 10% 15% 20% 25% 30% 32% Excess over P10,000 30,000 70,000 140,000 250,000 500,000 Allowable Deductions for Individuals 1) With gross compensation income derived from employer-employee relationship only Premium payments on health and/or hospitalization insurance Basic and additional personal exemption 2) Gross income from business or practice of profession Itemized deductions or optional standard deduction Premium payments on health and/or hospitalization insurance Basic and additional personal exemption Who cannot avail of deduction from gross income? 1) Non-resident aliens not engaged in trade or business in the Philippines 2) Resident Citizens who avail the 8% of Gross Income in computing tax income (Under the TRAIN) Premium payment on health and/or hospitalization insurance - It is an amount of premium on health and/or hospitalization paid by individual taxpayer for himself and members of his family during the taxable year. Requisites for Premium payments to be Deductible: 1) Insurance must have actually been taken 2) The amount of premium deductible does not exceed P2,400 per family or P200 per month during the taxable year 3) That said family has a gross income of not more than P250,000 for the taxable year 4) In case of married individual, only the spouse claiming additional exemption shall be entitled to this deduction. Who may avail of the Premium Payments? 1) Individual taxpayers earning purely compensation income during the year 2) Individual taxpayer earning business income or in practice of his profession whether availing of itemized or optional standard deductions during the year 3) Individual taxpayer earning both compensation and the business or practice of profession during the year Who may avail basic and additional personal exemption? 1) Only to individual resident citizen, non-resident citizen and resident alien (whether business or compensation income earners) 2) Non-resident alien engage in trade or business may be entitled to personal exemptions subject to reciprocity, i.e. the country of which he is a subject or citizen has an income tax laws and the income tax law of his country allows personal exemption to citizen of the Philippines not residing therein, bud deriving income there from and not to exceed the amount allowed in Philippine Tax Code. =================================================================================================== Page 1 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== What are basic and additional personal exemptions? 1) Basic personal exemption – The basic personal exemption is P50,000 exempt income of an individual whether single, head of the family or married individual (each married individuals) 4. Head of the family: Unmarried or legally separated person with one or both parents, or one or more brothers or sisters, or one or more legitimate, recognized natural or legally adopted children living with dependent upon the taxpayer for their chief support (chief support means more than one-half of the requirement for the support) 2) What are itemized deductions? 1. Ordinary and necessary expenses 2. Interests 3. Taxes 4. Losses 5. Bad debt 6. Depreciation of property 7. Depletion of oil, gas wells and mines 8. Charitable & other contributions 9. Research and development 10. Pension trust contributions of employees 11. Premium payments on health and/ hospitalizations insurance where such brother/sister or children are not more than 21 years of age, unmarried and not gainfully employed, or where such dependents regardless of age, are incapable of self-support because of mental or physical defect Additional personal exemption – The additional personal exemption is P25,000 exempt income of an individual for each of the qualified dependent children or senior citizen not exceeding four (4) in number. The proper claimant of the additional exemption in case of married individual is the husband being the head of the family, except, under the following cases: husband is unemployed husband is working abroad like an OFW or a seaman husband explicitly waived his right of the exemption in favor of his wife in the withholding exemption certificate husband is the guilty spouse in a legal separation (the innocent spouse may be categorized as Head of the Family (HF) plus additional personal exemption if court awards custody) husband purely in business while wife purely receiving compensation Qualified Dependent Child or children legitimate, illegitimate, legally adopted living with the taxpayer and dependent upon the taxpayer of chief support not exceeding 21 years old, unless incapable of self-support due to mental or physically defect unmarried and not gainfully employed become gainfully employed at the closed of such year. For any other event and for which there no specify rules applicable for the abovementioned, the status of the taxpayer at the end of the year shall determine his exemptions (strictly construed against the taxpayer. What is optional standard deductions? -In case of individual taxpayer’s OSD is a deduction equivalent to 40% of the gross receipts in lieu of Cost of Sales and itemized deductions. 3.1.2. Corporations Domestic Corporation (DC) – created or organized in the Philippines or under its laws 2. Foreign Corporation Resident foreign corporation (RFC) – created or organized other than Philippines laws; engaged in trade or business within the Philippines Non-resident foreign corporation (NRFC) – created or organized other than Philippine laws; not engaged in trade or business within the Philippines 3. Special Corporation 1. 1 2 3 4 Senior citizen any resident citizen of the Philippines at least sixty (60) years old, including those who have retired from both government officers and private enterprises, and has an income of not more than Sixty thousand peso (P60,000) per annum subject to the review of the National Economic Development Authority (NEDA) every three years. What are rules for a change of status? 1. If the taxpayer should marry or should have additional dependents during the taxable year, he may claim the corresponding exemption if full for such year. 2. If the taxpayer should die during the taxable year, his estate may claim his corresponding exemption as if he died at the close of such year 3. If the spouse or any dependent should marry or become 21 years of age, during the year or should become gainfully employed, the taxpayer may claim the exemption as if the spouse or dependent or dependent died or as if such dependent married, become 21 years of age or or 5 6 Private educational institutions & nonstock profit hospitals Resident international carriers Non-resident cinematographic film owner/lessor Non-resident owner/lessor of vessels Non-resident owner/lessor of aircrafts, machineries & equipment’s Offshore banking units SITUS TAX RATE TNI 10% Gross Philippine billings 2.5% Gross income Philippines0 25% Gross income from rentals, leases, charter fees, Philippines Gross income from rentals, leases, charter fees, Philippines Interest income from FC transactions 4.5% 7.5% 10% What is a corporation? It includes the following but not limited hereto: 1) Partnerships, no matter how created or organized 2) Joint-stock companies 3) Joint accounts 4) Associations 5) Insurance companies It excludes the following: 1) General professional partnership 2) Joint venue or consortium formed for the purpose of undertaking construction projects or engaging in petroleum, coal, geothermal and other energy operations pursuant to an operating or =================================================================================================== Page 2 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== consortium agreement under a service contract with the Government 3.1.3 Partnerships – is a business organization owned by 2 or more persons who contribute their industry or resources to a common fund for the purpose of dividing the profits among themselves. Type of partnership 1. Ordinary partnership or a business partnership – is one formed for profit, hence it is taxable as corporation. 2. General professional partnership (GPP) – is formed for the exercise of a common profession. A GPP is not treated as a corporation and is not a taxable entity; hence, exempt on its regular income. but the partners are taxable in their individual capacity with respect to their share in the income of the partnership. 3.1.4. Joint Ventures A joint ventures is a business undertaking for a particular purpose. It may be organized as a partnership or a corporation. 2 Types of joint ventures Exempt joint ventures Exempt joint ventures are those formed for the purpose of undertaking construction project, or engaging in petroleum, coal, geothermal and other energy operations, pursuant to an operating consortium agreement under a service contract with the Government. This type of joint venture is not treated as a corporation and is tax exempt on its regular income, but the venture are taxable to their share in the net income of the joint venture, similar to GPP. Taxable joint ventures All other joint ventures are taxable as a corporation 3.1.5. Estates and trusts Estate – refers to the mass of properties left by a deceased person. Estates under judicial settlement are treated as individual taxpayer and are taxable on the income of the properties left by the decedent Estate under extra judicial settlement are exempt entities. The income of the properties of the estate is taxable to the heirs. Trust – a right to the property, whether real or personal, held by one person for the benefit of another. A trust that is irrevocably designated by the grantor is treated as an individual taxpayer taxable on the income of the property held in trust. A revocable trust on the other hand, are not taxable entities. The income of properties held under revocable trust is taxable to the grantor. A Trust is a stipulation in favor of 3 rd persons. Under Art 1440 of the New Civil Code (NCC), a person who establishes a trust is called the trustor; one in whom confidence is reposed as regards to property for the benefit of another person is known as the trustee; and the person for whom benefit the trust has been created is referred to as the beneficiary. 3.1.6 Co-ownerships – is joint ownership of a property formed for the purpose of preserving the same and/or dividing its income. A co-ownership that is limited to property preservation or income collection is not a taxable entity and is exempt but the co-owners are taxable to their share on the income of the coowned property. A co-ownership that reinvests the income of the co-owned property to other income producing properties or ventures will be considered an unregistered partnership, hence taxable as a corporation. 3.1.7 Tax exempt individuals and organization a) Individual taxpayer – Both those who are working in the private and public sector being paid the statutory minimum wage as determine by the Tripartite Minimum Wage Board covering their basic, holiday, overtime, night differential and hazard pay shall be exempt from income tax and is not required to file income tax return. Note: Only commission and honorarium among others things are subject to income tax of a minimum wage earner. b) Corporation Corporation exempt from income taxation enumerated under Sec 30 of NIRC 1. Labor, agricultural or horticultural organization not organized principally for profit; 2. Mutual savings bank not having a capital stock represented by share, and cooperative bank without capital stock organized and operated for mutual purposes and without profit; 3. Beneficiary society, order or association, operating for the exclusive benefit of the members such as a fraternal organizations operating under the lodge system, or a mutual aid association or a nonstock corporation organized by employees providing for the payment of life, sickness, accident, or other benefits exclusively to the members of such society, order, or associations, or non-stock corporation or their dependents; 4. Cemetery Company owned and operated exclusively for the benefits of its members; 5. Non-stock corporation or association organized and operated exclusively for religious, charitable, scientific, athletic, or cultural purposes, or for the rehabilitation of veterans, no part of its net income or asset shall belongs to or inure to the benefit of any member, organizer, officer or any specific persons; 6. Business league, chamber of commerce, or board of trade not organized for profit and no part of the net income of which inure to the benefit of any private stockholder or individual; 7. Civic league or organizations not organized for profit but operated exclusively for the promotion of social welfare; 8. A non-stock and non-profit educational institution; 9. Government educational institution; 10. Farmers’ or other mutual typhoon or fire insurance company, mutual ditch or irrigation company, mutual or cooperative telephone company, or like organizations of a purely local character, the income of which consists solely of assessment, dues, and fees collected from members for the sole purposes of meeting its expenses and; 11. Farmers’, fruit growers’ or like association organized and operated as a sales agent for the purpose of marketing the products of its members and turning back to them the proceeds of sales, less the necessary selling =================================================================================================== Page 3 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== expenses on the basis of the quantity of produce finished by them. professional net income. Ordinary gain is taxable in full while ordinary loss is deductible in full. Note: Exemptions applies only to income derived from related activities. Any income derived from unrelated activities is subject to regular income tax. Effect of Situs on Dealings is Properties If the taxpayer is taxable on world income such as in the case of resident citizens and Domestic Corporation, the rules of dealings in properties apply to all properties regardless of location. If the taxpayer is taxable only on Philippine income, the rules of dealings in properties will be applied only to properties located in the Philippines. Government Owned & Controlled Corporations (GOCC’s) 1. General rule: These corporation are taxable as any other corporation. 2. Except the following: GSIS SSS PHIC PCSO 4. Regional or Area headquarters 1. If limited to supervision or communication activities – not subject to income tax 2. If it is operating headquarters – subject to a 10% of taxable income General principles of corporate tax situs: 1. Only Domestic Corporation are taxable for income derived from sources within and without the Philippines. 2. All other corporate income taxpayer are taxable for income derived from sources within the Philippines 3.2 GROSS INCOME 3.2.1. Inclusions in the gross income The term items of gross income or inclusions in gross income is a broad category pertaining to all items of income subject to taxation namely: 1) Gross income subject to final tax 2) Gross income subject to capital gain tax 3) Gross income subject to regular tax Exempted interest income from regular income taxation: Interest income earned by landowners in disposing their lands to their tenants in pursuant to the Comprehensive Agrarian Reform Law Imputed interest income 5. What is gross income subject to regular tax? – It means all income derived from whatever source, including but not limited to the following: 1. Compensation 2. Gross income from profession, trade of business 3. Gains from dealings in property a) dealings in ordinary assets b) dealings in capital assets other than domestic stocks and real properties 6. Royalties Royalties earned from sources within the Philippines are generally subject to final income tax, except when they are active by nature. Active royalty income and royalties earned from sources outside the Philippines are subject to regular income tax. 7. Dividends This pertains to dividends declared by foreign corporation such as cash, property and script dividends from foreign corporation are items of gross income subject to regular income tax. What is tax basis? – It refers to the cost, carrying amount or depreciated cost of an asset. The cost of an asset is the value forgone to acquire it. It is the purchase price or the fair value of consideration paid in acquiring the property. Tax treatment of ordinary gains and losses – ordinary gains are separate items of gross income subject to regular income tax, while ordinary losses are items of deductions from gross income in the determination of taxable business or Rents Rent income arises from leasing properties of any kind. It is a passive income but is not subject to final tax under the NIRC, hence is subject to regular income tax Special considerations on rent 1) Obligations of the lessor that are assumed by the lessee are additional rental income to the lessor 2) Advance rentals are a) Item of gross income upon receipt if Unrestricted Restricted to be applied in future years of upon the termination of the lease b) Not an item of gross income if It constitutes a loan It is a security deposit to guarantee payment or rent subject to contingency which may or may not happen 3) Leasehold improvements made by the lessee on the leased property are recognized by the lessor as income using the spread-out method or outright method. Determination of Gains or losses in dealings in property: Selling price xx Les Tax basis or adjusted s basis of the assets disposed xx Gain or loss xx What is Selling price? – It includes the amount realized from the sale and other disposition of property which shall include: the sum of money received and fair value of non-cash property received Interests Interest income refers interest income other than passive interest income subject to final tax. A taxable interest income must have been actually paid out of an agreement to pay interest, it cannot be imputed. Examples: interest income from lending activities to individuals and corporation by banks Interest income from bonds and promissory notes interest income from bank deposits abroad =================================================================================================== Page 4 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== Note: Dividends declared by domestic corporation are subject to 10% final tax if the recipient is an individual taxpayer and Dividends declared by domestic corporation are exempt if the recipient is a domestic or a resident foreign corporation Stock dividends is exempt from income tax but when the declaration confers to the recipient a different interest or right after the stock dividend declaration or when stocks dividends are subsequently redeemed such that it amounts to payment of cash dividends, the fair market value of the stock dividends received is taxable. 8. 9. Annuities The excess of annuity payments received by the recipient over premium paid is taxable income in the year of receipt. Prizes and winnings Prizes and winnings that are exempted from final tax are not items of gross income subject to regular income tax. Exempt prizes and winnings: a) Prizes received without effort to join a contest b) Prizes in athletic competition sanctioned by their respective national sports association c) Winnings from PCSO or lotto Rules of taxable prizes and winnings to individual taxpayer: Prizes Less than P10,000 More than P10,000 Winnings other than PCSO and Lotto Earned from Sources Within Abroad Regular tax Regular tax Final Tax Regular tax Final tax Regular tax 10. Pensions – this pertains to pensions and retirement benefits that fail to meet the exclusion criteria and hence subject to regular tax. 11. Partner’s share in the net income of the general professional partnership The partnership itself is not subject to regular income tax as they are merely viewed as passthrough entities. These entities do not pay tax on their regular income. However, the partners are the ones subject to regular tax on their share in the net income of the general professional partnership 3.2.2. EXCLUSIONS / EXEMPTIONS FROM GROSS INCOME a) Proceeds of life insurance exempt if the proceeds are retained by the insurer, the interest thereon is taxable. b) Return of insurance premium – the amount received by insured, as a return of premiums paid by him under life insurance, endowment, or annuity contracts, either during the term or at the maturity of the term mentioned in the contract or upon surrender of the contract. The amount received by the insured as a return of premium on any insurance contract is a return of capital, hence excluded from gross income. c) Gift, bequest or devise exempt income therefrom is taxable. Compensation for personal injuries or sickness, whether by suit or agreement Income exempt under treaty Retirement benefits, pensions, gratuities, etc. Requisites: d) e) f) In the service of the same employer for at least 10 years At least 50 years old must be availed of only once retirement plan must be approved by the BIR prior to implementation separation pay because of death, sickness, or other physical disability or for any cause beyond the control of the official or employee (e.g. retrenchment, redundancy or cessation of business) SSS benefits< retirement gratuities< pensions and other similar benefits received by citizens and aliens who come to reside permanently here from foreign sources private or public 3.2.3. INCOME FROM COMPENSATION Employer – Employee relationship Employer – refers to person to whom an individual performs any service, of whatever nature, as employee of such person. It is the person who has control over the payment of the employee. Employee – refers to any individual who is a recipient of wages. Elements of employer – employee relationship under the law 1) Selection and engagement of employees 2) Payment of wages 3) Power of dismissal 4) Power of control Type of employees as to function 1) Managerial employees 2) Supervisory employees 3) Rank and file employees The 1) 2) 3) following are not considered employees Consultant Directors Talents and Artists Type of employees as to taxability 1) Minimum wage earners – refers to a worker in the private sector who is paid the minimum wage or to an employee in the public sector with compensation income of no more than the statutory minimum wage (Salary 1 to 3) 2) Special employees – special aliens subject to the 15% final income tax on compensation income, such as those holding managerial or technical position in a Regional or area headquarters (RHQ) or Regional operating headquarters (ROHQ) 3) Regular employees – an employee subject to the regular progressive income tax Requirements to Filipinos Employed by RHQs and ROHQs: 1) Position and function test – the employee must be occupying and actually exercising a managerial or supervisory position 2) Compensation threshold test – the employee must have a gross annual taxable income of at least P975,000 3) Exclusivity test – employee is not a consultant or contractual personnel and is solely employed by RHQs or ROHQs. Gross compensation income – generally includes all remuneration received under an employer – employee relationship. Non-taxable or exempt Compensation =================================================================================================== Page 5 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 1) 2) 3) 4) Benefits excluded and/or exempted under the NIRC and special laws a) Remuneration received as incidents of employment Exempt retirement benefits under RA 7641, including exempt retirement gratuities to government official and employees Exempt termination benefits Benefits from the US Veterans Administration Social Security, retirement gratuities, pensions and similar benefits from foreign government agencies, and other institutions, private or public Benefits from SSS, under the SSS Act of 1954, as amended Benefits from GSIS, under the GSIS Act of 1937, as amended b) Employee mandatory contribution to GSIS, SSS, PhilHealth, HDMF and union dues c) Certain benefits of minimum wage earners d) De minimis benefits e) 13th month pay and other benefits not exceeding P82,000 (TRAIN P90,000) benefits exempt under treaty or international agreement benefits necessary to the trade, business or conduct of professional of the employer benefits for the convenience or advantage of the employer Exempt benefits of minimum wage earners 1) Basic minimum wages 2) Holiday pay 3) Overtime pay 4) Night shift differential pay 5) Hazard pay Note: A minimum wage earner must not have other items of taxable income aside from these benefits to be exempt. De Minimis Benefits – are facilities or privileges such as entertainment, medical services, or courtesy discounts on purchases that are of relatively small value and are furnished by the employer merely as a means of promoting health, goodwill, contentment or efficiency of his employees. De minimis benefits are petty fringe benefits and are exempt from income tax. De Minimis Benefits was restricted to mean only the following: a) Monetized unused vacation leave credits of private employees– not exceeding 10 days during the year b) Monetized unused vacation and sick leave credits of government official and employees c) Medical cash allowance to dependents of employees – not exceeding P750 per employee per semester of P125/month. d) Rice subsidy – P1,500 or 1 sack of 50-kg per month amounting to not more than P1,500 e) Uniform and clothing allowance – not exceeding P5,000 per annum f) Actual medical assistance – not exceeding P10,000 per annum g) Laundry allowance – not exceeding P300/ month h) Employee achievement award – monetary value not exceeding P10,000 i) Gifts given during Christmas – not exceeding P5,000 per employee j) Daily meals allowance – not exceeding 25% of the basis minimum wage Note: Hence, the following petty benefits are taxable de minimis benefits Excess de minimis over their limits Other benefits of relatively small value that are not included in the de minimis list. Treatment of taxable de minimis benefits 1) For rank and file employees – treated as compensation income as “other income” under 13th month pay and other benefits” 2) For managerial and supervisory employees – fringe benefit subject to final fringe benefits tax Classification of Gross Compensation Income 1) Regular compensation –fixed amount of remuneration 2) Supplemental compensation – other performance-based pay to employees with or without regard to the payroll period 3) 13th month pay and other benefits –not exceeding P82,000 is an exclusion from gross income ( under The Train Law this amount increases to P90,000). 3.2.4. Income from Business 1) Business income – arises from habitual engagement in any commercial activity involving regular sales of goods or services by an individual or a corporation. The income from business, legal or illegal, registered or unregistered is taxable 2) Professional income – the gross income from exercise of a profession or business gross income from the sales of service. 3.2.5. Passive income What is final tax? A tax imposes on passive income, also known as final income tax. 1. It is constituted as a full and final payment of the income tax due from the payee on a particular type of income subject to final withholding tax (FWT). The finality of the withholding tax is limited only to the payee’s income tax liability and does not extend to other taxes that may be imposed on said income. 2. The income subjected to final income tax is no longer subject to the net income tax; otherwise there would be a violation of prohibited double taxation. 3. The liability for the payment of the tax rests primarily on the payor as withholding agent. 4. The payee is not required to file an income tax return for the particular income subjected to FWT. 5. The rate of the final tax is multiplied to the gross income. Thus deductions and/or personal and additional exemptions are not allowed. What are passive incomes? – Income derived from sources within the Philippine such as: 1. Interest under the expanded foreign currency deposits system; 2. Interest, yields, or other monetary benefits from deposits, deposit substitutes, trust funds or similar agreement; 3. Royalties from intellectual creation (e.g. composition, authorship, literary works); 4. Prizes and winnings; 5. Dividends from Domestic Corporation or share of a partner in the distribution income of an ordinary partnership 3.2.6. Capital gains What are the 2 kinds of assets? 1) Ordinary assets – assets used in business such as =================================================================================================== Page 6 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== a) b) c) d) 2) Stock in trade of a taxpayer or other real property of a kind which properly be included in the inventory of the taxpayer if on hand at a close of the taxable year Real property held by the taxpayer primarily for sale to customers in the ordinary course of his trade or business Real property used in trade or business (i.e. buildings and/or improvements) of a character which is subject to the allowance for depreciation. Real property used in trade or business of the taxpayer 7) Interest payments must not be between related taxpayers 8) Interest must not be incurred to finance petroleum operation 9) In case of interest incurred in the acquisition of property, use in trade, business or profession, the same was not treated as a capital expenditures 10) The interest is not expressly disallowed by law to be deducted from gross income of the taxpayer. Deductible amount of interest expense: - The deductible amount of interest expense is the gross interest expense reduced by the following percentage of the interest income: Capital assets – any assets other than ordinary assets Effectivity Gains on dealings in properties: 1) Ordinary gains – arises from the sale, exchange and other disposition, including pacto de retro sales and other conditional sales, or ordinary assets. 2) Capital gain – arises from the sale, exchange and other disposition, including pacto de retro sales and other conditions sales of capital assets. Jan 1, 1998 Jan 1, 1999 Jan 1, 2000 Nov 1, 2005 Jan 1, 2009 Rationale of the deduction limit: - the limit is intended to recover the tax savings of taxpayers who are taking advantage of high regular tax savings created from interest expense and a lower final tax on deposit interest income. Taxation of gains on dealing in properties: Type of Gains Applicable taxation scheme Ordinary gains Regular income tax Capital gains General rule: Regular income tax Exception: Capital gains tax Optional treatment of interest expense: - Interest incurred in financing the acquisition of property used in trade or business may, at the option of the taxpayer, be claim as: 1) An outright deduction from gross income or 2) A capital expenditure claimable through depreciation Capital gains subject to capital gains tax: 1) Capital gains on the sale of domestic stock sold directly to buyer 2) Capital gains on the sale of real properties not used in business Other deductible interest expense 1) Interest from tax delinquency 2) Interest from scrip dividends What is a capital gains tax? – A tax imposed on sale of stock of a domestic corporation not listed and traded thru a local stock exchange, held as capital asset and sale of real property in the Philippine held as a capital asset. Examples of non-deductible interest: 1) Interest on personal loans 2) Interest incurred with a related party 3) Discounted interest applicable to future periods for individual taxpayers 4) Interest expense incurred to finance petroleum operations 5) Interest on preferred shares 6) Imputed interest How to compute capital gain tax of individual taxpayer? 1. On sale of shares of stock Not over P100,000 = 5% Excess of P100,000 =10% 2. On sale of real property Gross selling price or the current fair market value, whichever is higher = 6% 3. Gains from other capital assets = regular income tax 3.3 Deduction from gross income 3.3.1. Itemized deductions a) Ordinary and necessary expenses b) Interest Requisites on the deductibility of interest (RR132000): 1) There must be a valid indebtedness 2) The indebtedness must be that of the taxpayer 3) The indebtedness must be connected with the taxpayer’s trade, business or exercise of profession 4) Interest expense must have been paid or incurred during the taxable year 5) Interest must have stipulated in writing 6) Interest must legally due Percentag e 41% 39% 38% 42% 33% c) Taxes Taxes paid or incurred within the taxable year in connection with the taxpayer’s trade, business or exercise of profession shall be allowed as deduction, except: 1) Philippine income taxes , except fringe benefit tax Final income tax & stock transaction tax Capital gains tax Regular income tax 2) Foreign income, if claimed as tax credit 3) Estate tax and donor’s tax 4) Special assessment Other non-deductible taxes 1) Business tax VAT Other percentage tax 2) Surcharges or penalties on delinquent taxes Rationale of non-deductibility Income taxes are not costs of earning income but are impositions on net income accruing only after income is earned, hence not deductible. =================================================================================================== Page 7 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== Note: Foreign income tax is not a cost of earning income, however, it is allowed under the NIRC to be claimed as deduction if not claimed as tax credit. Special assessment is not a tax expense but is capitalized to the cost of the land. Bad debts refer to debt due to taxpayer which were actually ascertained to be worthless and were charged off within the taxable year. Requisites of claims for deduction of bad debt: 1) The debt must have been ascertain to be worthless 2) It must be charged off within the taxable year 3) It must be connected with the taxpayer’s profession, trade or business 4) The taxpayer must be under the accrual basis of accounting 5) It must not be incurred from related party Examples of deductible taxes: 1) Documentary stamp tax 2) Occupational tax 3) License tax 4) Fringe benefit tax 5) Local taxes, except special assessment 6) Community tax 7) Municipal tax 8) Foreign income tax, if not claimed as tax credit Note: The accounting bad debt expense called “estimated bad debt expense” is not deductible in taxation because it is a mere estimate rather than an actual loss. The deductible bad debt expense pertains to the write-off of uncollectible receivable after having been actually ascertained to be worthless. Only basic tax is deductible: - is allowed as deduction. Tax surcharges for late payments are avoidable and unnecessary expenses; hence, nondeductible. Moreover, allowing these as deduction will relax policy on tax collection. Note: Interest for late payment of tax is held deductible but as interest expense rather than as tax expense d) Losses Losses actually sustained during the taxable year and not compensated by insurance or other indemnity shall be allowed as deductions. Requisites for the deduction of losses: 1) It must be incurred in trade, profession or business of the taxpayer 2) It must pertain to property connected with trade, business or profession, if the loss arises from fires, storms, shipwrecks, or other casualties, or from robbery, theft or embezzlement (the loss must be an ordinary loss) 3) The loss must not be compensated by insurance or indemnity contract 4) A declaration of loss must have been filed by the taxpayer within 45 days from the date of discovery of the casualty or robbery, theft or embezzlement giving rise to the loss 5) The loss must not have been claimed as deduction for estate tax purposes in the estate tax return Types of losses 1) Ordinary loss 2) Capital loss Note: Losses from ordinary assets are deemed normal to the taxpayer’s trade, business or profession, hence, deductible in full. Losses on capital assets are deemed by law as unnecessary expenses, hence deductible only on the extent of capital gains. Examples of deductible ordinary losses 1) Loss on disposal or destruction of any ordinary assets 2) Loss due to voluntary removal of building incident to renewal or replacement 3) Permanent or irreversible loss in value of assets due to changes in business conditions only to the extend actually realized 4) Abandonment loss e) Examples of capital losses not deductible as bad debts: 1) Bad debt from personal receivable 2) Securities becoming worthless of taxpayers other than domestic banks and trust companies a substantial part of whose business is the receipts of deposits 3) Loss on capital investments in partnership, joint ventures or corporation Bad debt Subsequent recovery of bad debts – under the NIRC, the recovery of bad debts previously allowed as a deduction in the preceding years shall be included as part of the gross income in the year of recovery to the extent of the income tax benefit of said deduction. f) Depreciation – refers to the gradual exhaustion in the value of tangible business properties brought by the ordinary wear and tear through usage or obsolescence by the passing of time. It is a provision for the periodic return of the invested capital on the property throughout its useful life. There shall be allowed as a depreciation deduction a reasonable allowance for the exhaustion, wear and tear (including reasonable allowance for obsolescence) of property used in the trade or business. Depreciation method: 1) Straight line method 2) Declining balance method 3) Sum of the year digit method 4) Any other methods which may be prescribed by the Secretary of Finance upon recommendation of CIR Special rules on depreciation 1) Life tenancy to a property – in case of property held by one person for life with remainder to another person, the deduction shall be computed as if the life tenant were the absolute owner of the property and shall be allowed to the life tenant 2) Properties held in trust – in case of property held in trust, the allowable deduction shall be apportioned between the income beneficiaries and the trustees in accordance with the pertinent provisions of the instrument creating the trust, or in the absence of such provisions, on the basis of the trust income allowable to each. =================================================================================================== Page 8 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 3) 4) g) Revaluation on properties – the depreciation of an asset must be premised on its acquisition cost, and not on its reappraised value. Taxpayer using the revaluation model in accounting for items of property, plant and equipment under PAS 16 are not allowed to deduct the depreciation of the revalued surplus on the value of property as this is not a actual expense. 2) Rules on depreciation of passenger vehicles a) Substantiation of the purchase with sufficient evidence such as official receipts and other documents bearing the total purchase price including specific motor vehicle identification number of the vehicles b) Substantiation of the direct connection or relation of the vehicle to the development, operation, and/or conduct of the trade or business or profession of the taxpayer c) Only one vehicle for land transport is allowed for an official and employee and the value of which shall not exceed P2,400,000 d) No depreciation shall be allowed for yachts, helicopters, airplanes or aircrafts and land vehicle which exceeded the threshold, unless the main line of business is transport operation or lease of transportation equipment and the vehicle purchased are used in said operations Intangible exploration and development costs: 1) Intangible costs in petroleum operations include any incidental and necessary costs of drilling wells or preparing wells for petroleum production and which have no salvage value 2) Intangible costs in mining operations include the costs of diamond drilling, tunneling, and other improvements of a nature that is not subject to allowance for depreciation. Tax treatment of intangible exploration and development costs: 1) Before commercial production – capitalized as costs of the wasting asset 2) After commencement of commercial production, if incurred with: Non-producing wells or mines, deducted in the period paid or incurred Producing wells or mines, at the option of the taxpayer, either: Capitalized and amortized using the cost-depletion method or Deducted in the year paid or incurred Depletion Depletion expense is a provision for the periodic return of capital investments in wasting assets such as minerals, gas & oil. Stages of wasting assets activities 1) Exploration stage – it involves ascertaining the existence, location, extent or quality of any deposit or mineral. 2) Development stage – commences when deposits of ore or minerals are shown to exist in sufficient commercial quantity. 3) Commercial production – is the stage of actual extraction, processing and sale The expense Option on Non-producing Mines: After commercial production has commenced, exploration and development drilling expenses incurred on non-producing mines may be deducted outright but the deductible amount shall not exceed 25% of the net income from mining operations without the benefit of any tax incentives under existing laws. The unclaimed balance of the expense shall be carried forward to the succeeding years until fully deducted. Common rules for both mining and oil operation: Taxpayers engaged in wasting assets shall classify their expenditures into: 1) Cost of acquisition or improvement of tangible properties or 2) Intangible exploration, drilling and development costs Treatment of tangible development costs: - Tangible develop costs include the acquisition or improvement of tangible property which are of a character subject to the allowance for depreciation. This may include construction of mine-plant, roads, buildings, processing plants and installation of heavy equipment on-site. Treatment of tangible development costs: - tangible exploration and development drilling costs are capitalized and deducted through allowance for depreciation subject to the following rules: 1) Petroleum operations: Properties directly used in petroleum operations – the NIRC prescribes either straight line method or declining balance method at the option of the taxpayer. A shift from straight line method to declining balance method is allowed. The useful life shall be 10 years or such shorter life as may be permitted by the CIR. Properties not directly used in petroleum operation – the NIRC prescribed the straight line method on the basis of an estimated useful life of 5 years. Mining operations If the expected life of property used in mining is 10 years or less, the taxpayer can use the normal rate of depreciation. If the expected life is more than 10 years, the property can be depreciated over any number of years between 5 years and 10 years. Application of the matching rule: Taxpayers subject to on world income can deduct depreciation and depletion expense on properties wherever situated. Those taxable only on Philippine income are only allowed to claim depreciation and depletion on properties located within the Philippines. Charitable contributions Research & development Pensions h) i) j) 3.3.2. Items not deductions 1) Expenses non-deductible under the meaning of closed and completed transaction a) Decrease in value of properties or investment such as Decrease in value of securities such as stock or bonds Decrease in value of FOREX or FOREX denominated receivables Decrease in value of machineries, equipment and building brought by obsolescence b) Estimated future losses such as =================================================================================================== Page 9 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== Estimate loss on bad debts or uncollectible receivable Estimated loss on lawsuit not yet confirmed by a final judgment c) Loss on properties covered with insurance or indemnity contracts Expenses non-deductible under the matching principle a) Expense on exempt income Expenses incurred to finance the acquisition of a tax-exempt security Premiums paid for the life insurance of an officer where the taxpayer –business itself is the beneficiary Expense on EFCDU or OBU from foreign currency operation Expenses of non-profit organizations, government agencies and cooperative from their exempt operations cannot be deducted within the gross income subject to regular tax 2) b) Expenses on income subject to a special tax regime Expenses of new enterprises registered with the Tourism Infrastructure and Enterprises Zone Authority (TIEZA) under RA 9353 Expenses of enterprise registered PEZA under RA 7916 c) Business expenses of taxpayers subject to final income tax such as Non-resident alien, not engaged in trade or business Non-resident foreign corporations Expenses and taxes on income subject to final tax or capital gains tax Selling expenses of domestic stocks directly to buyer Selling expenses of real properties classified as capital assets Expenses of petroleum service subcontractors in supplying goods and services to petroleum service operators d) 3) e) Foreign business expenses of taxpayers taxable only on Philippine income such as Resident alien and non-resident alien engaged in trade or business in the Philippines Resident foreign corporation f) Loss of income not yet recognized in gross income Write-off of receivable under the cash basis of accounting Destruction of unharvested farm fruits or vegetables Death of animal offspring Expenses non-deductible under the lists of NIRC a) Personal, living or family expenses b) Amount paid out for new buildings or permanent, or betterment made to increase the value of any property or estate c) Any amount expended in restoring property or in making good the exhaustion thereof d) Premiums paid on any life insurance policy covering the life of any officer or employee, or any person financially interested in any trade or business carried on by the taxpayer, individual, or corporate, when the taxpayer is directly or indirectly a beneficiary under such policy 3.3.3. Optional standard deduction (OSD) Under the OSD, the allowable deduction of the taxpayer is simply presumed as a percentage of gross sales or receipt for individuals and gross income for corporations. There is no need to support every item of expenses. However, does not relieve the taxpayer of the responsibility to deduct withholding tax on income payments as required by the NIRC and the regulations. Who can claim OSD? OSD is a proxy to itemized deductions. As a rule, all taxpayers who are subject to tax on taxable net income can claim deductions, except the following: a) Non-resident alien engaged in trade or business (NRARTB) b) Taxpayers mandated to use itemized deductions Mandatory itemized deductions (RR2 – 2014) 1) Corporation mandated to use the itemized deduction a) Exempt GOCCs and non-stock non-profit corporation with no taxable income b) Those with income subject to special / preferential tax rates and c) Those with income subject to regular corporate income tax and special/preferential tax 2) Individual taxpayers mandated to use the itemized deduction: a) Exempt individuals under the NIRC and special laws with no other taxable income b) Those with income subject to special/preferential tax rates and c) Those with income subject to regular income tax special/preferential income tax Percentage of optional standard deduction: 1) Individual taxpayers – 40% of total sales/revenues/receipts/fees a) Those selling goods under the accrual basis – 40% of sales b) Those selling services under the cash basis – 40% of gross receipts c) Those selling services under the accrual basis – 40% of gross receipts 2) Corporate taxpayers – 40% of gross income Rules on determination of OSD for individual taxpayers 1) Gross Sales – it includes only sales contributory to income subject to regular tax. Since sales returns, allowances and discounts re not contributory to income, they must be deducted from the total recorded sales. In short, the tax concept of “gross sales” is the accounting concept of “net sales”. 2) Gross receipts – means amounts actually or constructively received during the taxable year. For sellers of services employing the accrual basis of accounting, the term “gross receipts” shall mean amounts earned as gross revenue during the taxable year. Optional Standard Deduction and NOLCO NOLCO cannot be claimed simultaneously with OSD because NOLCO is an item of deduction while OSD is a proxy of all itemized deductions. NOLCO is deemed included in the claimable OSD. Optional Standard Deduction and Net Capital Loss CarryOver OSD do not replace net capital loss carry-over of individual taxpayers. The net capital loss carry-over is used in the measurement of net capital gain which is an item of gross income. In other works, it is not an item of deduction. Hence, a net capital loss carry-over from the prior year can still be deducted against the net capital gain of the current year even if the taxpayer opted to deduct optional standard deduction for the current year. 3.3.4. Deductions allowed under special laws =================================================================================================== Page 10 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== Special allowable itemized deductions Special deductions are other items of deductions which may or may not partake the nature of an expense but is allowed by the NIRC or by special laws as deductions. Special deductions include deduction incentives to taxpayers in assisting and in complying with certain legal requirements. Special allowable Deductions: 1) Special expenses under the NIRC and special laws a) Income distribution from a taxable estate or trust b) Transfer to reserve fund and payments to policies and annuity contracts of insurance companies c) Dividend distribution of a Real Estate Investment Trust (REIT) under RA 9856 d) Transfer to reserves of funds of taxable cooperatives e) Discounts to senior citizens under RA 9257 Conditions for deductibility of sales discount to senior citizens: Only that portion of the gross sales exclusively used, consumed or enjoyed by the senior citizen shall be eligible for the deductible sales discount The gross selling price and the sales discount must be separately indicated in the official receipts or sales invoice by the establishment for the sale of goods or services to the senior citizen Only the actual amount of the discount granted or sales discount not exceeding 20% of the gross selling price can be deducted from gross income, net of VAT, if applicable. The discount can only be allowed as deduction from gross income for the same taxable year that the discount is granted The business establishment giving sales discount to qualified senior citizen is required to keep a separate and accurate records of sales, which shall include the name, TIN, ID. gross sales/receipts, discount granted, date of transaction and invoice number for every sale transaction to senior citizen f) Discounts to persons with disability under RA 9442 Similar to senior citizens, person with disability is entitled to 20% discount from certain establishments such as hotels, and similar lodging establishments, restaurant, sports, and recreation centers places of culture, leisure and amusement, drugstore on the purchase of medicine, medical and dental services in private facilities, and domestic air, sea, and land transport. 2) Deduction incentives under special laws a) Additional compensation expense for senior citizen employee under RA 9257. Under RA 9257, private establishments employing senior citizens shall be entitled to additional Conditions for deductibility of additional compensation: Employment shall have to continue for at least 6 months The annual taxable income of the senior citizen does not exceed the poverty level as determined by the NEDA b) Additional compensation expense for persons with disability under RA 7277 as amended by RA 9442. Private entities that employ persons who meet the required skills or qualification, either as regular employees, apprentice or learner, shall be entitled to an additional deduction, from their gross income, equivalent to 25% of the total amount paid as salaries and wages to disabled persons. Requisites for Deductibility: The entity present proof as certified by the DOLE that disabled persons are under their employ. The disabled employee is accredited with the DOLE and the DOH as to his disability, skills and qualification c) Cost of facilities improvements for persons with disability in accordance with RA 7277 as amended by RA 9442. Under RA 7277, private entities that improve or modify their physical facilities in order to provide reasonable accommodation for disabled persons shall also be entitled to an additional deduction from their income, equivalent to 50% of the direct costs of the improvements or modifications. d) Additional training expenses under the RA 8502 – Jewelry industry Development Act of 1998. Under RA 8502, and its implementing rules and regulations, a qualified jewelry enterprise duly registered and accredited with the Board of Investment (BOI) is entitled to an additional deduction from taxable income of 50% of the expenses incurred in training schemes approved by Technical Education and Skills Development Authority (TESDA). The same shall be deductible during the year the expenses were incurred. Conditions for deductibility: A qualified jewelry enterprise must submit to the BIR a certified true copy of its Certificate of Accreditation issued by BOI The training scheme must be approved and certified by TESDA e) Additional contribution expense under the Adopta School Program under RA 8525. Under this program, private entities are allowed to assist a public school to in particular aspect of educational program within an agreed period of time. The assistance maybe an aid, contribution or donation in cash or in kind but not limited to infrastructure, physical facilities, real estate property, training and skills development, learning support, reading materials, computer and science laboratories, health and nutrition packages, and assistive learning devices for students with special needs. Qualification of participating schools: Any government schools in all levels may participate in the program. Priorities shall be given to schools located in the poorest province, low income municipalities, and other local government units experiencing severe classroom shortages, insufficient budget, or having numerous poor but high performing learners. Qualification of Adopting Private Entity 1) It must have a credible track record 2) It must have been in existence for at least one year 3) It must not have been prosecuted and found guilty of engaging in illegal activities such as money laundering and other similar circumstances. Tax Deductible Incentive Contributions to the government in priority activities are deductible in full while those made in non-priority activities are deductible subject to limit. Aside from the usual regular deductible contribution expense, an adopting entity shall be allowed an additional deduction from gross income equivalent to 50% of the contribution of =================================================================================================== Page 11 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== the adopting entity for the “Adopt-A-SchoolProgram”. exchange that may otherwise be used for milk importation. Conditions for deductibility: 1) The deduction shall be availed of in the taxable year in which the expense is paid or incurred 2) The expense is substantiated with sufficient evidence, such as official receipts or delivery receipt and other adequate records The amount of expenses being claimed as deductions Direct connection or relation of the expenses to the adopting private entity’s participation in the “Adopt-a-SchoolProgram”. Proof or acknowledgement of receipt of the contributed or donated property by the recipient public school. 3) The application together with the approved MOA endorsed by the National Secretariat, shall be filed with the RDO having jurisdiction over the place of business of the adopting private entity, copy furnished the RDO having jurisdiction of the property, if the contribution is in the form of real property. Tax Deduction Incentives: The expenses incurred by a private health institution in complying with the rooming-in and breast-feeding practices, shall be deductible expenses for income tax purpose up to twice the actual amount incurred. Meaning, the cost of compliance shall be claimed as part of the regular itemized deduction and additional expense for the same amount shall be claimed under special itemized allowable deduction. Illustrative Problem: St Claire Medical Hospital, a private hospital, previously set up a milk storage facility and a milk bank. The total annual cost of the 2 facilities were as follows: Storage Milk Facility Bank Supplies P100,000 P120,000 Staff salaries 210,000 90,000 Maintenance 50,000 70,000 Total P360,000 P280,000 Less: Fees collected from patients 0 190,000 Excess Expense P360,000 P90,000 Procedure for availment. : 1) Memorandum of Agreement 2) Supporting evidence 3) Applying for Certificate of Tax Incentives and Tax Exemption and submit the following documents to the Secretariat: Duly authorized or approved MOA Duly notarized deed of donation Official receipts and other documents showing the actual value of the contribution or donation Certificate of Title and Tax declaration, if the donations is in the form of property Other adequate records showing direct connection or correlation of the expense being claimed as deduction to the adopting entity’s participation in the program Valuation of deductions (RR10-2003) 1) Cash assistance contribution or donations shall be based on the actual amount appearing in the official receipt issued by the done 2) Assistance other than money Personal property – acquisition cost of assistance or contributions Consumable goods – acquisition cost or value at date of donation whichever is lower Services – the value of service rendered by the donor and the service provider and the public school as fixed in the MOA or the actual expense incurred by the donor, whichever is lower Real property – fair value (higher of zonal value or assessed value) at the time of contribution or the depreciated cost of the property whichever is lower. f) Additional deductions for compliance to Roomingin and Breast-feeding practices under RA 7600 as amended by RA 10028. The purpose of RA 10028 is to encourage, protect and support the practice of breast-feeding which is believed to provide distinct benefits to the mother and the infant aside from saving the country’s valuable foreign Solution: The total regular itemized deduction is P450,000 (P360,000 + P90,000) The special itemized allowable deduction allowed as additional deduction is P450,000, same amount as the regular itemized deduction. Conditions for Deductibility 1) The deduction shall apply for the taxable period when the expense were incurred 2) All health or non-health facilities, establishments and institutions shall comply with the IRR of RA 10028 within 6 months after its approval 3) The facility, establishment or institution secure a “Working Mother-Baby-Friendly Certificate” from the Department of Health to be filed with the BIR Note: Government hospital cannot claim deductions since it is non-taxable However, government facilities, establishments and institutions will receive additional appropriation equivalent to the savings they may derive as a result of complying with RA 10028. g) Additional free legal assistance expense under RA 9999. Lawyers or professional partnership providing pro-bono legal services are given deduction incentives for their free legal services. Requirement for Availment: Lawyers or professional partnership rendering actual free legal services shall secure a certification from the Public Attorney’s Office (PAO), the DOJ or association accredited by the SC indicating that the said legal services to be provided are within the services defined by the SC, and that the agencies cannot provide the legal services to be provided by the legal counsel. Tax Deduction Incentive =================================================================================================== Page 12 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== The practicing lawyer or professional partnership shall be entitled to an allowable deduction from gross income equivalent to the amount that could have been collected for the actual performance of the actual free services rendered or up to 10% of gross income derived from the actual performance of the legal profession whichever is lower. For the purpose of this incentives, the free legal services must be exclusive of the 60-hour mandatory free legal assistance rendered to indigent clients as mandatorily required under the Rule on Mandatory Legal Aid Services for Practicing Lawyers. Computation of Special Free Legal Service Expenses (Whichever is Lower) Actual free services provided xx Compare Deduction Limit Gross receipts Xx Less: Direct cost of service Xx Gross income from operation xx x tax deductible incentive rate 10% xx Special “free legal service expense (lower figure) xx Computation of Net Income Gross receipts Les Direct cost s Gross income from operation Add Other gross income Total gross income Les Regular itemized s deduction Special free legal service expense Net income h) xx xx xx xx xx xx xx xx xx Additional productivity incentive bonus expense under RA 6971. Under the Productivity Incentive Acts of 1990 (RA 6971), a business enterprise which adopts a productivity incentive program is entitled to a special additional deduction equivalent to 50% of the total productivity bonuses given to employees under the program. In addition, business enterprises providing manpower training and special studies to rank and file employees as accredited by the TESDA are also entitled 50% additional deduction of the total grant for local training and special studies. However, the deduction incentive will not be allowed on bonuses accruing during the pendency of a strike or lockout arising from any violation of the productivity incentive program. 3.4 Accounting periods - it is the length of time over which income is measured and reported. Type of Accounting period: 1) Regular accounting period – 12 months in length Calendar year – starts from January 1 and ends December 31. This accounting period is available to both corporate taxpayers and individual taxpayer. Under the NIRC, the calendar year shall be used when the taxpayer’s annual accounting period is other than a fiscal period taxpayer has no annual accounting period taxpayer does not keep books taxpayer is an individual Fiscal year – a fiscal accounting period is any 12 month period that ends on any day other than December 31. The fiscal accounting period is available only to corporate income taxpayer 2) Short accounting period – less than 12 months Deadline of filing the income tax return: - Under the NIRC, the return is due for filing on the 15 th day of the four month following the close of the taxable year of the taxpayer. The regular tax due is payable upon filing of the income tax return. Instances of short accounting period: 1) Newly commence business – the accounting period covers the date of the start of the business until the designated year-end of the business. 2) Dissolution of business – the accounting period covers the start of the current year to the date of dissolution of the business. 3) Changes of accounting period by corporate taxpayers – the accounting period covers the start of the previous accounting period up to the designated yearend of the new accounting period. 4) Death of the taxpayer – the accounting periods covers the start of the calendar year until the death of the taxpayer. 5) Termination of the accounting period of the taxpayer by the CIR – the accounting period covers the start of the current year until the date of the termination of the accounting period. Note: The BIR approval is required in changing an accounting period, it is not automatic. 3.5 Accounting methods Types of accounting method: 1) The general methods a) Cash method – recognition of income and expense dependent on inflow or outflow of cash, e.g. rental income are realized from receipt not on when earned. b) Accrual method – under this method: Income, gains and profits are include in gross income when earned regardless whether received or not. Expense are allowed as deduction when it incurred, regardless whether paid or not 2) Installment and deferred payment method – under this method, gross income is recognized and reported in proportion to the collection from the installment sales. Installment method is available to the following taxpayers: a) Dealers of personal property b) Dealers of real properties, only if their initial payment do not exceed 25% of the selling price. c) Casual sale of non-dealers in property, real or personal, when their selling price exceeds P1,000 and their initial payment do not exceed 25% of the selling price Definition of terms: a) Initial payment – means total payments made by the buyer, in cash or property, in the taxable year the sale was made. The term “initial payment” means not only the down payment but it also includes the installment payment made in the year of sale. b) Selling price – means the entire amount for which the buyer is obligated to seller, it is computed as follows: Cash received and/or receivable Ad FMV of property received or d receivable Mortgage or any indebtedness assumed by the buyer Pxx xx Xx =================================================================================================== Page 13 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== Selling price c) Contract price – is the amount receivable in cash or other property from the buyer. It is usually the selling price in the absence of an agreement whereby the debtor assumes indebtedness on the property Deferred payment method: - is a variant of the accrual basis and is used in reporting income when a non-interest bearing is received as consideration in sale. Under this method, the gross income is computed based on the present value (discounted value) of a note receivable from the contract. The discount interest on the note is amortized (i.e. spread) as interest income over installment term. Note: The difference between the face value and the present value of the note, (is known as discount) will not be recognized in gross income at the date of sale but will be deferred and recognized as interest income The discount is amortized as interest income upon every collection on the balance of the note a. 3) Percentage of completion method – under this method, the estimated gross income from construction is reported based on the percentage of completion of the construction project. There are several methods of estimating project completion in practice but the output method based on engineering survey is prescribed by the NIRC. 4) Outright and spread-out method – under RR No. 2, the net income from leasehold improvements can be reported using either of the following method at the option of the taxpayer: a) Outright method – the lessor may report as income at the time when such buildings or improvements are completed the FMV of such buildings or improvements subject to the lease b) Spread-out method – the lessor may spread over the life of the lease the estimated depreciated value of such buildings or improvement at the termination of the lease and report as income for each year of the lease an aliquot part thereof. The depreciated value of the leasehold improvement is computed as follows: Excess useful life over lease term ÷ Useful life of the improvement Percentage x Cost of improvement Depreciated value 5) revenue district office where the taxpayer registered or required to register: An authorized agent bank Revenue Collection Officer Duly authorized city or municipal treasurer xx B. Electric filing & E-submission – the e-filling of tax returns including attachments in electronic format shall be made through the internet to the BIRs Large Taxpayer Service Division through the BIR website. Taxpayer under EFPS system shall e-pay their tax online through internet banking service. The account of the taxpayer will be auto-debited for the amount of taxes to be paid. C. D. Large taxpayers and non-large taxpayers Income tax credits E. Venue and time of filing of tax returns Where to file return? Legal residence – authorized agent bank; revenue district officer; collection agent of duly authorized treasurer Principal place of business With the office of the Commissioner When to file return? Under the NIRC, the return is due for filing on the 15th day of the 4th month following the close of the taxable year of the taxpayer. The regular tax due is payable upon filing of the ITR. First quarter – April of current year Second quarter – August 15 of current year Third quarter – November 15 of current year Final quarter – April 15 of the following year G. Modes of payment Cash Installment – when the tax due is in excess of P2,000, the taxpayer may elect to pay in 2 equal installment: 1st installment – April 15 2nd installment – on or before July 15 H. Use of tax tables xx xx % xx xx OLD Table Over P10,000 30,000 70,000 140,000 250,000 500,000 Crop year basis Farming income is commonly recognized using the cash basis or accrual basis, however, long-term crops or those that takes more than one year to harvest may be accounted for under the crop year basis. Under this method, farming income is recognized as the difference between the proceeds of harvest and expenses of the particular crop harvested. The expense of each crop is accumulated and deducted upon the harvest of the crop. Reconciliation of income under PFRS and income under tax accounting: 3.6 Tax return preparation and filing tax payments A. Manual filing – the traditional manual system of filing income tax return is by paper document where taxpayer fill-up BIR forms to report income, expenses or any declaration required to be filed with the Bureau. The income tax return shall be filed to the following, in descending order of priority, within the is But not over P30,000 70,000 140,000 250,000 500,000 P500 2,500 8,500 22,500 50,000 125,000 10% 15% 20% 25% 30% 32% Excess over P10,000 30,000 70,000 140,000 250,000 500,000 TRAIN TABLE Over P400,000 800,000 2,000,000 8,000,000 I. But not over P250,000 800,000 2,000,000 8,000,000 Excess over P30,000 130,000 490,000 2,410,000 25% 30% 32% 35% P400,000 800,000 2,000,000 8,000,000 Accomplishing of various income tax returns and forms 3.7 Withholding taxes A. Time of withholding – the final withholding tax, withholding tax on compensation and expanded withholding tax return shall be filed in triplicate by every withholding agent or payor who is either an =================================================================================================== Page 14 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== B. C. D. E. F. G. H. I. individual or corporation on or before the 10 th day of the month following the month in which withholding was made. The return shall be filed and the tax shall be paid with the authorized agent bank of the RDO having jurisdiction over the withholding agent’s place. Income payments subject to withholding Year-end withholding tax and requirements Venue and time of filing of withholding tax returns Venue and time of payment Modes of payment Time of payment Use of tax tables and rates Use of various withholding tax returns and forms 3.8 Compliance requirement A. Administrative requirements B. Attachments to the income tax returns, including CPA certificate per NIRC requirements C. Keeping of books of accounts and records, including report of inventories D. Prescriptive period of maintain books of accounts and other accounting periods 4. C an American singer was engaged to sing for one week at the Western Philippine Plaza after which she returned to USA. for income tax purposes she shall be classified as a. Resident alien b. Non-resident alien engaged in trade or business c. Non-resident alien not engaged in trade or business d. Resident citizen 5. Situs of taxation is world/global taxation? a. Resident citizen b. Resident alien c. Non-resident citizen d. Non-resident alien 6. It is important to know the source of income for tax purposes (i.e from within and without the Philippines) because a. Some individuals and corporate taxpayers are taxed on their worldwide income while others are taxable only upon income from sources within the Philippines b. The Philippines imposes income tax only on income from sources within c. Some individual taxpayers are citizens while others are aliens d. Export sales are not subject to income tax 7. An exemption allowed to a taxpayer who has qualified legitimate illegitimate, or legally adopted children a. Additional exemption b. Special additional personal exemption c. Optional standard deduction d. Basic personal exemption 8. The following except one may claim personal exemption a. Non-resident alien not engaged in trade or business b. Non-resident alien engaged in trade or business c. Resident alien d. Citizens 9. Which of the following taxpayers whose personal exemption is subject to the law on reciprocity under the Tax Code? a. Non-resident citizen with respect to his income derived from outside the Philippines b. Non-resident alien who shall come to the Philippine and stay herein for an aggregate period of more than 180 days during any calendar year c. Resident alien deriving income from a foreign country d. Non-resident alien not engaged in trade or business in the Philippines whose country allows personal exemption to Filipinos who are not residing but are deriving income from said country 10. Under the Tax Code who of the spouses is the proper claimant of the additional exemption in respect to any of the dependent children? a. The husband if his income is higher than the income of the wife b. The spouse who has the bigger income c. The husband d. The wife who has the bigger income MULTIPLE CHOICE PROBLEMS. Select the correct answer for each item by writing the letter of your choice on the answer sheet. Submit necessary solution to support your answer if needed. NO SOLUTION WILL BE MARK INCORRECT! A. INDIVIDUAL TAXATION 1. 2. 3. One of them is not considered non-resident citizen a. A citizen of the Philippines who establishes to the satisfaction of the Commissioner the fact of this physical presence abroad with a definite intention reside therein b. A citizen of the Philippines who leaves the Philippines during the taxable year to reside abroad either as an immigrant or for employment on permanent basis c. A citizen of the Philippines who works and derives income from abroad and whose employment thereat requires him to be physically present abroad most of the time during the taxable year d. A citizen of the Philippines who went on a business trip abroad and stayed there in most of the time during the taxable year A non-resident citizen arrived in the Philippines on July 1, 2000 to reside here permanently after working as nurse in the United States of America for many years Which of the following statements is correct with respect to Ms. A’s classification for income tax purposes? a. She shall be classified as non-resident citizen for the year 2000 with respect to her income derived from sources abroad from January 1, 2000 until the date of her arrival in the Philippines b. She shall be classified as non-resident citizen for the whole year of 2000 c. She shall be classified as resident citizen for the whole year of 2000 d. She shall be classified as neither resident non-resident citizen for the year 2000 B an Expert Physicist was hired by a Philippines corporation to assist in its organization and operation for which he had to stay in the Philippines for an indefinite period. His coming to the Philippines was for a definite purpose which in its nature would require an extended stay and to that end makes his home temporarily in the Philippines. The American management expert intends to leave the Philippines as soon as his job is finished For income tax purposes, the American management expert shall be classified as a. Resident alien b. Non-resident alien engaged in trade or business c. Non-resident alien not engaged in trade or business d. Resident citizen 11. Mr. H and Mrs. W married couple had the following data in year? Only Mr. H has gainful employment earning gross income. Two dependents a legitimate son 21 years old and daughter 19 years old but newly-wed. The personal and additional exemption of the couple a. H – P100, 000; W – P50, 000 b. H – P100, 000; W – P0 c. H – P50, 000; W – P50,000 =================================================================================================== Page 15 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== d. H – P50, 000; W – P0 12. One of the following is not a head of the family for income tax purposes a. Widower supporting his mother in law 50 years old b. Unmarried taxpayer supporting his mother 50 years old c. Married but legally separated taxpayer supporting a legitimate child 6 years old d. Legally separated taxpayer supporting a brother 22 years old physically incapacitated 13. A taxpayer single has the following dependents who live with him a. Jimy brother 23 years old taking up Engineering course b. Dea sister married c. Jomen adopted child gainfully employed d. . Generally non-resident aliens not engaged in trade or business are subject to 25% final tax on their gross income in the Philippines a. True, true b. True, false c. False, false d. False, true 19. “Global system of income taxation” means a. All types of income except those subject to final tax are aggregated to arrive at gross income b. Separate graduated rates are imposed on different types of income c. Capital gains are excluded in determining gross income d. Compensation income and business/professional income are taxed at different place in the world 20. For income tax purposes the taxpayer can claim: Basic personal exemption Additional exemption a. P50, 000 Zero b. P50, 000 P8, 000 c. P100, 000 Zero d. P50, 000 P25, 000 Which of the following income of an individual taxpayer is subject to final tax? a. P10, 000 prize in Manila won by a resident citizen b. Dividend received by a resident citizen from a resident corporation c. Share in the net income of a general professional partnership received by a resident alien d. Dividend received by a non-resident alien from a domestic corporation 14. The taxpayer is a married non-resident alien engaged in business in the Philippines with two (2) qualified dependent children. His country gives a non-resident Filipino with income there from a basic personal exemption of P4, 000. He is entitled to total personal exemptions of a. P54, 000 b. P32, 000 c. P28, 000 d. P48, 000 21. Interest received by non-resident individuals from a depository bank under the expanded foreign currency deposit system is exempt from tax Passive income received by a resident citizen from resources outside the Philippines shall be generally subject to Section 24 (A) and not to final tax a. True, true b. True, false c. False, false d. False, true 15. 22. One of the following is not qualified as dependent for income tax purposes a. Illegitimate child 16 years old living in the United States due to his studies b. Senior citizen not related to the taxpayer with a yearly income of P60, 000 living with and taken care of by the taxpayer c. Legitimate child 21 years old with a monthly income of P2, 000 living with the taxpayer in Manila d. Brother 24 years old incapable of self-support because of physical disability 16. Life insurance premiums paid by an individual taxpayer is deductible from gross income for an maximum amount of P2, 400 provided the family’s gross income for the year does not exceed P250, 000 The premium on health and/ or hospitalization insurance is deductible by the spouse who claimed the additional exemption in case of married taxpayer a. True, true b. True, false c. False, false d. False, true 17. Which of the following will change the status of the taxpayer? a. Marriage of a dependent within the taxable year b. Dependent becoming 21 years old during the year c. Dependent gaining employment during the year d. Marriage of taxpayer himself during the year 18. Filipinos as well as alien employees of regional or area headquarters established in the Philippines by multinational companies shall be subject to final tax of 15% of gross compensation income in the Philippines A non-resident alien driving income from Philippines sources claims that he is entitled to personal exemptions. Which of the following is not a condition for the allowance of personal exemptions to said non-resident citizen? a. That he has stayed in the Philippines for an aggregate period of more than 180 days b. That his country has an income tax law that allows personal exemptions to Filipinos not residing therein c. That he has filed a true and accurate return of his total income from all sources within the Philippines d. That he is married to a Filipina 23. Which of the following statements is incorrect? a. To be subject to final tax passive income must be from Philippines sources b. Passive income earned outside of the Philippines is not subject to final tax but subject to Section 24(A) Net Income Tax\ c. An income which is subject to final tax is excluded from the computation of income subject to Section 24 (A) Net Income Tax d. An income which is subject to creditable withholding tax is excluded in the computation of income subject to Section 24(A) 24. Proceeds of sale of real property classified as principal residence and capital asset are exempt from the 6% capital gains tax if used to build or buy a new principal residence within 18 months from the date of sale or disposition Gain from sale of real property classified as capital asset to the Government may be taxed under Section 24 (A) or capital gains tax at the option of the individual taxpayer a. True, true b. True, false c. False, false d. False, true =================================================================================================== Page 16 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 25. One of the following is not a deposit substitute a. Bankers acceptance b. Promissory notes c. Repurchase agreements d. Debt instruments issued for interbank call loans with maturity of not more than 5 days to cover deficiency in reserves against deposit liabilities 26. Which of the following statements is incorrect? a. A prize of P10, 000 is subject to 20% final b. Wining from Philippine Charity Sweepstakes are exempt from income tax c. Royalties on books literary works and musical composition are subject to 10% final withholding tax d. Interest income from long term deposit is exempt from income tax 27. 1st statement - Cash and or property dividends received from domestic corporation by a non-resident alien not engaged in trade of business are subject to 25% final tax 2nd statement - Share of an individual in the distributable net income after tax of a general professional partnership is subject to final tax a. True, true b. True, false c. False, false d. False, true 33. F sold his residential house to Ms. P for P5M. Its FMV when he inherited it was P6M although its presents FMV is P8M The tax on the above transaction is a. P360,000 CGT b. P480,000 CGT c. P30% donors tax d. VAT 34. Continuing #33 but assuming the residential house is located abroad the capital gains tax is; a. P360,000 b. P480,000 c. P120,000 d. P0 35. G bought a plot of land with a cash payment of P2, 000, 000 and a purchase money mortgage of P2, 500, 000. In addition G paid P10, 000 for title insurance policy. G’s basis in this land is a. P2,000,000 b. P2,010,000 c. P4,500,000 d. P4,510,000 36. H an accrual – basis taxpayer owns a building which was rented to M under a 10 – year lease expiring August 31, 2016. On January 2, 2013 M paid P30, 000 as consideration for cancelling the lease. On November 7, 2013, H leased the building to P under a 5 – year lease. P paid HP 10,000 rent for 2 months November and December and an additional P5, 000 for the last month’s rent. What amount of rent income should H report in its 2013 income tax return? a. P10,000 b. P15,000 c. P40,000 d. P45,000 28. 1st statement – Non-resident individual taxpayer are also subject to 7.5% final tax on their income from expanded foreign currency deposit 2nd statement – there can be a 6% capital gains tax on sale of a real property in USA a. True, true b. True, false c. False, false d. False, true 29. Which is covered by gross income taxation? a. Resident alien b. NRA – ETB without Reciprocity Law c. NRA – not ETB d. Not resident citizen 30. Which is governed by Hybrid gross income taxation? a. A resident Filipino with compensation income only b. NRA – ETB with the benefit of reciprocity law c. A non resident citizen with the business income only d. A resident citizen who is considered a mixed income earner 31. E Resident Filipino taxpayer single supporting three minor (illegitimate) children one of them living abroad showed the following data for taxable year 2000 Salary from ABC Co. (net of P40, 000 Withholding tax) P350,000 Professional fee from various schools (net of 10% withholding tax) 135,000 Expenses incurred practice of profession (Living expenses including tuitions fees of children 25% thereof) 80,000 Health and or hospitalization insurance Premium paid 5,000 How much personal exemption may Mr. E claim? a. P25,000 b. P50,000 c. P75,000 d. P100,000 32. How much is Mr. E taxable income? a. P380,000 b. P355,000 c. P350,000 d. P330,000 37. The a. b. c. d. following are subject to Net Income Taxation except Resident Citizen Domestic Corporation Non Resident Citizen engaged in business Non Resident Corporation 38. Mr L a cemetery lot dealer sold real properties to different buyers as follows; Selling Price Cost House & Lot P2,000,000 P1,250,000 Farm Lot P 800,000 P 300,000 Cemetery Lot P 45,000 P 20,000 The house and lot were sold to acquire a condominium unit for Mr. L new principal place of residence. What is Mr. L capital gains tax? a. P170,700 b. P168,000 c. P 48,000 d. P 50,700 39. In June 2005 J received a piece of land fairly valued at P1, 000, 000 from his wealthy best friend as a birthday gift. Since J had no use of the said donated land he immediately sold it to G for only P500, 000. What is the total tax liability of J? a. P 30,000 b. P 60,000 c. P210,000 d. P360,000 40. Mr. S an individual calendar year taxpayer purchased 100 shares of Core Co. Common stock for P15, 000 on December 15, 2015 and an additional 100 shares for P13, 000 on December 30, 2015. On January 3, 2016 S sold the shares purchased on December 15, 2015 for P13, 000. What amount of loss from the sale of core’s stock is deductible on Mr. S 2015 and 2016 income tax returns? =================================================================================================== Page 17 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== a. b. c. d. 2015 P0 P0 P1,000 P2,000 2016 P0 P2,000 P1,000 P0 41. Mr. O received the following in December Thirteenth month pay 15,000 Christmas bonus 15,000 Monetized vacation leave for 5 days 10,000 The taxable compensation income to Jose is a. P40,000 b. P0 c. P25,000 d. P20,000 42. Lessor had the following information for the given taxable year Cost of Leasehold improvement P1,000,000 Annual rent 100,000 The estimate life of leasehold improvement is 50 years. The term of the lease is 40 years. At the end of the twentieth (20th) year the lease was terminated for valid causes done by the lessee What is the taxable income to be reported by the lessor at the end of the 20th year? a. P100,000 b. P125,000 c. P605,000 d. P700,000 c. d. 47. Mr. C a widower has two sons by his previous marriage. C lives with Mrs. J who is legally married to Mr. J. They have a child name Jill. The children are all minors and not gainfully employed. How much personal exemption can Mr. C claim? a. P 50,000 b. P 75,000 c. P100,000 d. P125,000 48. 45. 1st statement – In case of an individual taxpayer and the income tax on the annual return exceeds two thousand pesos such tax may be paid in two equal instalments 2nd statement – if an individual’s annual income tax is paid in instalment. First payment shall be made when the return is files and the rest shall be paid on or before July 15 following the close of the year a. True, false b. True, true c. False, true d. False, false 46. Mr. A a non resident alien stockholder received a dividend income of P300, 000 in 2016 from a foreign corporation doing business in the Philippines. The gross income of the foreign corporation from within and without the Philippines for three years preceding 2016 are as follows Source of 2013 2014 2015 income From P16,000,000 P12,000,000 P14,000,000 within the Philippines From 18,000,000 14,000,000 16,000,000 without the Philippines How much of the dividend income received by Mr. A is considered income from sources within the Philippines? a. b. Zero P150,000 A privilege granted to a taxpayer to deduct or set off against Phil. Income tax the income war profits and excess profits taxes that he has paid or has accrued to a foreign country a. Tax exemption b. Tax deduction c. Tax consolidation d. Tax credit 49. A married to M had the following during the taxable year Gross Income From the practice of profession P700,000 Rental income of their conjugal 300,000 property Allowable deductions For the practice of profession 520,000 For the property rented to tenants 140,000 The taxable income before exemptions of Mr. A is a. P340,000 b. P180,000 c. P260,000 d. P170,000 43. What is the allowable deduction of lessee on the 20th year? a. P600,000 b. P625,000 c. P100,000 d. P500,000 44. The following individuals are required to file an income tax return except a. non-resident alien engaged in trade or business b. non-resident alien not engaged in trade or business c. resident citizen d. non-resident citizen P300,000 P270,000 50. K sold for P10 M her Baguio rest house with a FMV of P12 M to buy a new principal residence. If K utilized P8 M of the proceeds of the sale in acquiring a new principal residence the capital gains tax payable is a. P720,000 b. P600,000 c. P144,000 d. P120,000 51. Which of the following is not correct? a. An individual citizen of the Phils. Who is working and deriving income from abroad as an overseas contract worker is taxable only on income from sources within the Phils b. A seaman who is a citizen of the Phils. and who receives compensation for services rendered abroad as a member of the complement of a vessel engaged exclusively in international trade shall be treated as an overseas contract worker c. An alien individual is taxable only on income derived from sources within the Phils d. A citizen of the Phils. is taxable on income derived from sources within and without the Phils 52. Optional standard deduction is allowed to except a. Non-resident alien engaged in business b. Non-resident alien not engaged in business c. Resident alien d. General professional partnership 53. 1st statement – the fact that an individual’s name is signed to a filed return shall be prima facie evidence for all purposes that the return was actually signed by him 2nd statement – if a taxpayer is unable to make his return the return may be made by his guardian or representative the latter assuming the responsibilities of making the return and incurring penalties if the same was erroneous a. True, false =================================================================================================== Page 18 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== b. c. d. True, true False, true False, false 54. 1st statement – an individual may employee either calendar year or fiscal year as basis for filing its annual income tax return 2nd statement – the return of any individual shall be filed on or before the 15th day of April of each year covering income for the preceding year a. True, false b. True, true c. False, true d. False, false 55. Z is a Filipino immigrant living in the United States for more than 10 years. He is retired and he came back to the Philippines as a balikbayan. Every time he comes to the Philippines he stays here for about a month. He regularly receives a pension from his former employer in the United States amounting to US$1,000 a month. While in the Philippines with his pension pay from his former employer he purchased three condominium units in Makati which he is renting out for P15, 000 a month each. Does the US$1,000 pension become taxable because he is now in the Philippines? a. Yes income received in the Philippines by non-resident citizens is taxable b. Yes income received in the Philippines or abroad by non-resident citizens is taxable c. No income earned abroad by non-resident citizens are no longer taxable in the Philippines d. No the pension is exempt from taxation being one of the exclusions from gross income 56. 57. K sold for P10 M her Baguio rest house with a FMV of P12 M to buy a new principal residence. If K utilized P8 M of the proceeds of the sale in acquiring a new principal residence the capital gains tax payable is a. P720,000 b. P600,000 c. P144,000 d. P120,000 Skylar sold his bachelor’s pad for P1,200,000 to acquire a two bedroom loft at Princeville condominium for P3,200,000 with a fair market value of P3,500,000. How much is the capital gains tax? a. P 72,000 b. P192,000 c. P210,000 d. Zero 58. In the preceding number a sale of principal residence to purchase a new principal residence shall be exempt from tax if done a. Once every 10 years and reported to BIR within 18 months from sale b. Once every 18 years and reported to BIR within 10 months from sale c. One every 10 years and reported to BIR within 2 months from sale d. Once every 10 years and reported to BIR within 1 month from sale 59. Dondon and Helena were legally separated. They had six minor children all qualified to be claimed as additional exemptions for income tax purposes. The court awarded custody of two of the children to Dondon and three to Helena with Dondon directed to provide full financial support for them as well. The court awarded the 6 th child to Dondon’s father with Dondon also providing full financial support. Assuming that only Dondon’s gainfully employed while Helena is not for how many children could Dondon claim additional exemptions when he files his income tax return? a. b. c. d. Six children Five children Three children Two children 60. Keynard Inc. A Philippines corporation sold through the local stock exchange 10,000 PLDT share that it bought 2 years ago. Keynard sold the shares for P2 million and realized a net gain of P2, 000,000. How shall it pay tax on the transaction? a. It shall declare a P2 million gross income in its income tax return deducting its cost of acquisitions an expense b. It shall report the P200,000 in its corporate income tax return adjusted by the holding period c. It shall pay 5% tax on the first P100,000 of the P200,000 and 10% tax on the remaining P100,000 d. It shall pay a tax of one half of 1% of the P2 million gross sales 61. Which theory in taxation states that without taxes a government would be paralyzed for lack of power to activate and operate it resulting in its deduction? a. Power to destroy theory b. Lifeblood theory c. Sumptuary theory d. Symbiotic doctrine 62. The payor of passive income subject to final tax is required to withhold the tax from the payment due the recipient. The withholding of the tax has the effect of a. A final settlement of the tax liability on the income b. A credit from the recipient’s income tax liability c. Consummating the transaction resulting in an income d. A deduction in the recipients income tax return 63. Guidant Resources Corporation a corporation registered in Norway has a 50MW electric power plant in San Jose Batangas. Aside from Guidant’s income from its power plant which among the following is considered as part of its income from sources within the Philippines? a. Gains from the sale to an Ilocos Norte power plant of generator bought from the United States b. Interest earned on its dollar deposits in a Philippine bank under the Expanded Foreign Currency Deposit System c. Dividends from a two year old Norwegian subsidiary with operations in Zambia but derives 60% of its gross income from the Philippines d. Royalties from the use in Brazil of generator sets designed in the Philippines by its engineers 64. Anktryd Inc. Bought a parcel of land in 2015 for P7 million as part of its inventory of real properties. In 2016 it sold the lad for P12 million which was its zonal valuation. In the same year it incurred a loss of P6 million for selling another parcel of land in its inventory. These were the only transactions it had in its real estate business. Which of the following is the applicable tax treatment? a. Anktryd shall be subject to a tax of 6% of 12 million b. Anktryd could deduct its P6 million loss from its P5 million gain c. Anktryd’s gain of P5 million on shall be subject to the holding period d. Anktryd’s P6 million loss could not be deducted from its P5 million gain 65. Aplets Corporation is registered under the laws of the Virgin Islands. It has extensive operations in Southeast Asia. In the Philippines its products are imported and sold at a mark-up by its exclusive distributor Kim’s Trading Inc. The BIR complied a record of all the imports of Kim from Aplets and imposed a tax on Aplets net income derived from its exports to Kim. Is the BIR correct? =================================================================================================== Page 19 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== a. b. c. d. 66. Yes Aplets is a non-resident foreign corporation engaged in trade or business in the Philippines No the tax should have been computed on the basis of gross revenues and not net income ‘ No Aplets is a non-resident foreign corporation not engaged in trade or business in the Philippines Yes Aplets is doing business in the Philippines through its exclusive distributor Kim’s Trading Inc. Passive income includes income derived from an activity in which the earner does not have any substantial participation. This type of income is a. Usually subject to a final tax b. Exempt from income taxation c. Taxable only if earned by a citizen d. Included in the income tax return 67. In 2016, Juliet UIbod earned P500,000 as income from her beauty parlor and received P250,000 as Christmas gift from her spinter aunt. She had no other receipts from the year. She spent purposes her gross income for 2016 is a. P750,000 b. P500,000 c. P350,000 d. P600,000 68. Federico a Filipino citizen migrated to the United States some six years ago and got a permanent resident status or green card. He should pay his Philippine income taxes on a. The gains derived from the sale in California U.S.A of jewelry he purchased in the Philippines b. The proceeds he received from a Philippine insurance company as the sole beneficiary of life insurance taken by his father who died recently c. The gains derived from the sale in the New York Stock Exchange of shares of stock in PLDT a Philippine corporation d. Dividends received from a two year old foreign corporation whose gross income was derived solely from Philippine sources 69. An example of a tax where the concept of progressivity finds application is the a. Income tax on individuals b. Excise tax on petroleum products c. Value added tax on certain articles d. Amusement tax on boxing exhibitions 70. Income is considered realized for tax purpose when a. It is recognized as revenue under accounting standards even if the law does not do so b. The taxpayer retires from the business without approval from the BIR c. The tax payer has been paid and has received in cash or near cash the taxable income d. The earning process is complete or virtually complete and an exchange has taken place 71. Which among the following taxpayers is required to use only the calendar year for tax purpose a. Partnership exclusively for the design of government infrastructure projects considered as practice of civil engineering b. Joint stock company formed for the purpose of undertaking construction projects c. Business partnership engaged in energy operations under a service contract with the government d. Joint account (cuentas en participation) engaged in the trading of mineral ores 72. In March 2016, Tonette who is found of jewelries bought a diamond ring for P750,000, a bracelet for P250,000, a necklace for P500,000 and a brooch for P500,000. Tonette derives income from the exercise of her profession as a licensed CPA. In October 2016, tonette sild her diamond ring, bracelet and necklace for only P1.25 million incurring a loss of P250, 000. She used the P1.25 million to buy a solo diamond ring in November 2016 which she sold for P1.5 million in September 2017. Which among the following describes the tax implications arising from the above transactions? a. Tonette may deduct his 2016 loss from her 2016 professional income b. Tonette may carry over and deduct her 2016 loss only from her 2017 gain c. Tonette may carry over and deduct her 2016 loss from her 2017 professional income as well as from her gain d. Tonette may not deduct her 2016 loss from both her 2016 loss from both her 2017 professional income and her gain 73. Anion Inc. received a notice of assessment and a letter from BIR demanding the payment of P3 million pesos in deficiency income taxes for the taxable year 2015. The financial statements of the company show that it has been suffering financial reverses from the year 2016 up to present. Its asset position shows that it could pay only P500, 000 which it offered as a compromise to the BIR. Which among the following may the BIR require to enable it to enter into a compromise with Anion Inc.? a. Anion must show it has faithfully paid taxes before 2016 b. Anion must promise to pay its deficiency when financially able c. Anion must waive its right to the secrecy of its bank deposits d. Anion must immediately deposit the P500,000 with the BIR 74. Levox Corporation wanted to donate P5 million as prize money for the world professional billiard championship to be held in the Philippines. Since the Billiard sports Confederation of the Philippines does not recognize the event if was held under the auspices of the International Professional Billiards Association Inc. Is Levox subject to the donor’s tax on its donation? a. No so long as the donated money goes directly to the winners and not through the association b. Yes since the national sports association for billiards does not sanction the event c. No because it is donated as prize for an international competition under the billiards association d. Yes but only that part that exceeds the first P100,000 of total Levox donations for the calendar year 75. The excess of allowable deductions over gross income of the business in a taxable year is known as a. Net operating loss b. Ordinary loss c. Net deductible loss d. NOLCO B. CORPORATION TAXATION 76. For purposes of computing the MCIT which will not form part of cost of goods sold for traders a. Invoice cost b. Import duties c. Freight d. Wharfage 77. Based on the preceding number nut the taxpayer is a manufacturer which will not form part of cost of goods sold? a. Raw materials used b. Direct labor & overhead c. Freight & insurance d. Import duties =================================================================================================== Page 20 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 78. based on No. 76 but the taxpayer is a seller of services which will not form part of cost of services? a. Salaries & supplies b. Employee benefits c. Depreciation & rental expenses d. Interest expense 79. Statement 1: The MCIT is only effective in the 5 th year following the year in which the corporation commenced its business Statement 2: non-resident corporations are also covered by MICT a. True, true b. False, false, c. False, true d. True, false 80. Non-Resident Corporations need not file any income tax returns. Tax EXEMPT Corporations are also required to file an ITR for administrative purposes only a. True, true b. False, false, c. False, true d. True, false 81. To record MCIT the account deferred charges MCIT is a. Debited b. Credited c. Memo entry only d. No entry required 82. To record application of excess MCIT vs. NORMAL income tax what account is credited a. Income tax payable b. Cash in bank c. Retained earnings d. Deferred charges MCIT 83. To record expired portion of MCIT what account is debited a. Retained earnings b. Income tax payable c. Deferred charges MCIT d. Provision for income tax 84. One of the following is not accepted basis of relief from the MCIT a. Prolonged labor dispute b. Force majeure problems c. Legitimate business reverse d. Law suits filed by the company 85. Which is not a characteristics of corporate income tax a. Progressive tax b. Direct tax c. General x d. Natural tax 86. 1st statement: Non stock non – profit corporation are tax exempt from their income from all operations 2nd statement: Interoperate dividends are tax exempt if the recipient is a foreign corporation a. True, true b. False, false, c. False, true d. True, false 87. Which of the following corporation may not file a income tax return? a. Domestic Corporation b. Resident Corporation c. Non-Resident Corporation d. Special Corporation 88. Which is governed by gross income taxation a. Domestic corporation b. c. d. Resident corporation Non-resident corporation Educational institutions 89. One of the following corporations cannot claim tax credit for foreign taxes paid abroad a. Private educational Institutions b. Resident International Carriers c. Investment companies d. Domestic Hospitals 90. 1st statement: Foreign income tax may be treated by a corporate taxpayer as tax credit but not as deduction from gross income 2nd statement: Being a holding company is conclusive evidence of improper accumulation of profit’ a. True, true b. False, false c. True, false d. False, true 91. The improperly accumulated earning tax shall not apply to the following except a. Insurance companies b. Corporations formerly registered with PEZA c. Publicly held corporations d. Bank & Non-Bank Financial Intermediaries 92. 1st statement: Domestic corporation not falling number under the definition of closely held corporations are considered publicly held corporations 2nd statement: A closely Corporation under the Corporation Code are the same a. True, true b. False, false c. False, true d. True, false 93. It is the reasonable a test used in determining the reasonable needs of a business to justify the accumulation of earnings which will exempt the corporation from paying IAE a. Urgency test b. Reasonable need test c. Immediacy test d. Excise tax 94. The a. b. c. d. IAE tax is essentially a General tax Property tax Regulatory or penalty tax Excise tax 95. 1st Statement: MCIT shall apply to all corporations 2nd statement: IAET shall apply only to Domestic Corporation a. True, true b. True, false c. False, false d. False true 96. A domestic corporation provided the following data Gross sales Sales returns Cost of goods sold Busines s expense s 13 P2,040,00 0 40,000 14 2,800,00 0 100,000 15 3,000,00 0 16 4,000,00 0 1,000,000 700,000 1,500,00 0 1,500,00 0 950,000 210,000 1,200,00 0 1,200,00 0 =================================================================================================== Page 21 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== The income tax due after tax credit if any for taxable year 2015 is a. P15,000 b. P40,000 c. P60,000 d. P90,000 97. Income derived by a depository bank under the expanded foreign currency deposit system from foreign currency transactions with local commercial banks shall be subject to a final tax rate of a. Seven and one half percent (7 ½%) b. Twenty percent (20%) c. Ten percent (10%) d. Five percent (5%) 98. The following corporations are except from the Minimum Corporate Income Tax except a. Non-profit hospitals b. Proprietary educational institutions c. Non-stock non-profit educational institutions d. Resident corporations 99. Which of the following is not exempted from improperly accumulated earnings tax? a. Publicly – held corporations b. Bank and other non-bank financial intermediaries c. Insurance companies d. Resident corporation 100. 101. Amos Corp. Had P600,000 in compensation expense for book purposes in 2016. Included in this amount was a P50, 000 accrual for 2016 non shareholder bonuses Amos paid the actual 2016 bonus for P60,000 on march 1, 2017. In its 2016 tax return what amount should Amos deduct as compensation expense? a. P600,000 b. P610,000 c. P550,000 d. P540,000 What was Kelly’s taxable income for the year ended December 31, 2016? a. P170,000 b. P330,000 c. P345,000 d. P380,000 104. A DOMESTIC CO. Provide the following data Gross income Net income 102. In 2016 Cable Corp. A calendar year corporation contributed P80, 000 to a qualified charitable organization. Cable’s 2016 net income was P820, 000. In 2016 what amount can Cable deduct as charitable contributions? a. P80,000 b. P45,000 c. P41,000 d. P51,000 103. For the year ended December 31, 2016 Kelly Corp. Had net income per books of P300, 000 before taxes. Included in the net income were the following items Dividend income from an unaffiliated domestic taxable corporation Bad debt expense (represents the increase in the allowance for doubtful account) P50,000 80,000 2016 1,500,000 100,000 250,000 What income tax due for the taxable year 2015 is a. P80,000 b. P72,000 c. P32,000 d. P40,000 105. Assuming the same problem in No.29. the income tax due for the taxable year 2016 is a. P75,000 b. P65,000 c. P30,000 d. P40,000 106. Assuming the same problem No. 29. However the domestic corporation is a proprietary educational institution. The income tax due for 2016 is a. P75,000 b. P25,000 c. P32,000 d. P40,000 107. Williams a domestic corporation had the following data Taxable year 2015 2016 Aragorn Inc had the following items of income and expenses Gross Receipts P500,000 Cos of salary of personnel 250,000 Directly engaged in business Dividends received 25,000 The dividends were received from a domestic corporation. The general and administrative expenses include cost of utilized facilities cost of supplies of P25, 0000 and P15, 000, respectively. What amount should be reporter as gross income for minimum corporate income tax purpose? a. P210,000 b. P235,000 c. P250,000 d. P275,000 2015 2,00,000 The a. b. c. d. Gross income Deductions 1,000,000 980,000 1,100,000 500,000 income tax payable in 2015 is P20,000 P0 P380,000 P100,000 108. Assuming the same problem No. 32 the taxable income in 2016 is a. P380,000 b. P0 c. 100,000 d. P50,000 109. Assuming the same problem in No. 32 the income tax payable in 2016 is a. P153,600 b. P144,000 c. P114,600 d. P 94,600 110. The following person’s signature must appear in the corporation income tax return except a. President b. Vice president c. Treasurer d. External auditor 111. Resident international Philippine billing at a. 2 ½% b. 5% c. 7 ½% d. 10% carriers are taxed on gross =================================================================================================== Page 22 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 112. Non-resident lessors of aircraft machineries and other equipment are taxed on gross rentals, charter and other fees at a. 2 ½% b. 4 ½% c. 7 ½% d. 10% 113. Non-resident owner or lessor of vessels chartered by Philippine nationals are taxed on gross rentals lease or fees at a. 2 ½% b. 4 ½% c. 7 ½% d. 10% 114. 1st statement – A resident corporation is allowed to deduct depreciation expense regardless of the property’s location 2nd statement – A private educational institution may at its option elect either to deduct capital expenditures during the taxable year or to deduct allowance for depreciation thereof a. True, false b. True, true c. False, true d. False, false 115. 116. 117. ABC Corporation sold a real property in Malolos Bulacan to XYZ Corporation. The property has been classified as residential and with a zonal valuation of P1, 000 per square meter. The capital gains tax was paid based on the zonal value. The Revenue District Officer (RDO) however, refused to issue the Central Authorizing Registration for the reason that based on his ocular inspection the property should have a higher zonal valuation determined by the Commissioner of Internal Revenue because the area is already a commercial area. Accordingly, the RDO wanted to make a recompilation of the taxes due by using the fair market value appearing in nearby bank’s valuation list which is practically double the existing zonal value. What values must the RDO use as the basis for determining the capital gains tax? a. Fair Market Values or Zonal Values whichever is higher b. Fair Market Values or Gross Selling Price whichever is higher c. Fair Market Values or Assessed Values whichever is higher d. Fair Market Values or Bank’s Valuation whichever is higher In connection with the preceding number the RDO also wanted to assess a donor’s tax on the difference between the selling price based on the zonal value and the fair market value appearing in a nearby bank’s valuation list, should the difference in the supposed taxable value be legally subject to donor’s tax? a. Yes taxable value is difference between the selling price and fair market value at the time of transfer b. Yes taxable value is the difference between the zonal values and selling price c. No there was no transfer for insufficient consideration of immovable are not subject to donor’s tax d. No there was a valid perfect and consummated contract of sale and not donation Weber Realty Company which owns a three hectare land in Antipolo entered into a Joint Venture Agreement (JVA) with Prime Development Company for the development of said parcel of land. Weber Realty as owner of the land contributed the land to the Joint Venture and Prime Development agreed to develop the same into a residential subdivision and construct residential house thereon. They agreed they would dive the lots between them. Does the JVA entered into by and between Weber and Prime create a separate taxable entry? a. b. c. d. Yes JVA is a taxable corporation Yes JVA is a taxable partnership No JVA is exempt from taxation No JVA is a mere conduit 118. Based on the preceding questions are the allocation and distribution of the saleable lots to Weber and Prime subject to income tax and to expanded withholding tax? a. Yes allocation and distribution saleable lots are taxable income subject to withholding tax b. Yes allocation and distribution saleable lots are part of the gross income and not subject to expanded withholding tax c. No allocation and distribution saleable lots are exempt income in the likings of interoperate dividends d. No allocation and distribution of saleable lots of a joint venture engaged in construction projects are exempt from income tax 119. Is the sale by Weber or Prime of their respective shares in the saleable lots to third parties subject to income tax and to expanded withholding tax? a. Yes the sale by Weber or Prime of their respective shares in the saleable lots to third parties are part of the gross income of a taxable corporation and not subject to withholding tax b. Yes the sale by Weber or Prime of their respective shares in the saleable lots to third parties are not part of the gross income but subject to expanded withholding tax c. Yes the sales by Weber or Prime of their respective shares in the saleable lots to third parties are both subject to income tax to expanded withholding tax d. No the sales by Weber or Prime of their respective shares in the saleable lots to third parties are exempt from income tax 120. Taxable on income within and without the Philippines? a. Residential International Carrier b. Non-residential cinematographic film makers c. Non-stock non-profit hospitals d. Non-resident owners or lessors of vessels C. TAXATION ON PARTNERSHIP, ESTATE & TRUST 121. Mr. D and Ms. W are partners in a Partnership which realized a gross income of P800, 000 with a corresponding P350, 000 expenses in the year 2014. Mr. D is married with 2 qualified dependent children he earned P400, 000 in his own business incurring P230, 000 a allowable expenses while Ms. W had P450, 000 and P250, 000 gross income and expenses respectively. they share profits and losses as follows 4:6 If the partnership is a GPP the taxable income of Mr. D subject to 5 – 32% is a. P122,000 b. P180,000 c. P250,000 d. P320,000 122. And a. b. c. d. taxable income of Ms. W subject to 5 – 32% is P180,000 P270,000 P420,000 P470,000 123. If the partnership is an Ordinary Partnership its tax due is a. P135,000 b. P148,000 c. P153,000 d. P108,000 124. And the total tax liability of Mr. D is a. P12,240 b. P18,900 =================================================================================================== Page 23 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 125. 126. 127. 128. 129. 130. 131. 132. 133. c. d. P50,000 P32,500 The a. b. c. d. total tax liability of MS. w is P 32,500 P 18,360 P101,000 P 31,140 Samuel and John are co-owner by virtue of a property given to them by their father. The co – ownership had a gross rental income of P500, 000 (gross of 5% tax) and expenses related to rental activity of P200, 000 but 10% is now deductible for the year. Samuel and John share in the profits at 75% and 25% respectively. Samuel withdrew P50, 000 from the co – ownership net income for the year John did not withdraw any amount. Samuel and John are both single The income tax the co- ownership a. P102,400 b. P76,800 c. P80,000 d. P0 The a. b. c. d. taxable income of Samuel is P320,000 P190,000 P80,000 P0 Suppose Sam & John did not divide but instead invested the P320,000 profit in another business venture where are they earned a net income after deductions of P450,000 the tax due of the co- ownership is a. P102,400 b. P76,800 c. P135,000 d. P0 1st statement – a CPA and a Dentist mat form GPP or an ordinary partnership 2nd statement – Partnership and Corporation have separate juridical personalities distinct from the owners a. true, false b. false, false c. false, true d. true, true 1st statement – the share of the partnership in the gross income of the GPP is added to his own gross income 2nd statement – the share of the partner in the net income of a GPP is also considered passive income a. true, true b. false, false c. false, true d. true, false 1st statement – GPP’s may claim the 10% OSD 2nd statement – a GGPP may be organized for p[profit also a. true, true b. false, false c. false, true d. true, false 1st statement – Co – ownership and partnership are the same as to taxability 2nd statement - corporation and ordinary partnerships are the same as to taxability a. true, true b. false, false c. false, true d. true, false 1st statement – a GPP has no separate juridical personality since it is tax exempt 2nd statement – corporations partnership but not GPP a. true, true b. false, false c. false, true d. true, false may form a taxable 134. 1st statement – the term taxpayer means any person subject to income tax including estates & trusts 2nd statement - the income tax imposed upon individuals shall also apply to the income of estate or of any property held in trust a. true, true b. false, false c. false, true d. true, false 135. 1st statement – only estates earning income under judicial administration are subject to income tax 2nd statement – in income taxation of estate the judiciary or the trust or has the personal liability to pay the tax in all cases a. true, true b. false, false c. false, true d. true, false 136. 1st statement – the estate is still the taxpayer after administration or its settlement 2nd statement – the trust is the taxpayer if the income is to be accumulated for the trustor or grantor a. true, true b. false, false c. false, true d. true, false 137. All of the following are non-taxable trusts except one a. revocable whose trusts b. trusts whose income are reserved for the grantee c. pension trusts created under conditions laid down by law d. trusts whose income are to be accumulated for the trustor or grantor 138. The share in the profits of a partnership in a general professional partnership is regarded as received by him and thus taxable although not yet distributed. The principle is known as a. actual receipt of income b. advance reporting of income c. accrual method of accounting d. constructive receipt of income 139. Fusion of two corporation for a specific undertaking a. merger b. consolidation c. joint- account d. joint – venture 140. An a. b. c. d. indivisible thing own by at least two individuals joint – account co – ownership partnership sociedad anominas D. 1. GROSS INCOME DEDUCTIONS One of the following does not form part of gross income a. interest b. royalties c. annuities d. gift bequest and devises 2. In computing allowable deduction for purposes of income taxation: 1st statement – interest expense in connection with the taxpayer’s business shall be reduced by an amount equal =================================================================================================== Page 24 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== to thirty eight percent (33%) of interest income subject to final tax. 2nd statement – interest incurred to acquire property used in trade shall only be allowed to be treated as a capital expenditure a. true, false b. true, true c. false, true d. false, false 3. 4. 5. 6. 7. Patricia was injured in a vehicular accident in 2012. he incurred and paid medical expenses of P10, 000 and legal fees of P5, 000 during that year. in 2016, he recovered P35, 000 as settlement form the insurance company which insured the car owned by the other party involved in the accident. from the above payments and transactions the amount of income taxable to Patricia in 2016 is a. P20,000 b. P25,000 c. P35,000 d. P0 One a. b. c. d. of the following is not excluded from gross income amounts received by insured as return of premium life insurance proceeds compensation for injuries as sickness share in the net income of a general professional partnership To be allowed as a valid deduction charitable and other contribution must not exceed a. 5% of taxable income after charitable contribution income of individuals b. 10% of taxable income after charitable contribution in case of individuals c. 5% of taxable income before charitable of contribution in case of individuals d. 10% of taxable income before charitable contribution in case of individuals Premium paid for health and hospitalization insurance shall be allowed as a deduction a. the amount claimed does not exceed two thousand five hundred pesos (P2,500) per year b. must be claimed by each spouse separately c. gross income of the family does not exceed two hundred fifty thousand pesos (P250,00) d. the amounts of premium payment claimed is not exceeding two hundred fifty pesos (P250) a month 1st statement – the term quasi – banking activities means borrowing funds from twenty or more persons at any one time through the issuance endorsement or acceptance of debt instruments of any kind other than deposits. 2nd statement – interest in government debt securities are exempt income a. true, false b. true, true c. false, true d. false, false 8. In the case of sale of land under the agrarian reform law 1st statement – interest earned by the owner/seller is exempt income 2nd statement – capital gain in the sale of the lad is taxable income a. true, false b. true, true c. false, true d. false, false\ 9. In computing net income no deduction shall any case be allowed in respect to except a. personal living or family expenses b. c. d. any amount paid out for new buildings or for permanent improvements or betterment made to increase the value of any property or estate any amount expended in restoring property or in making good the exhausted thereof which an allowance is or has been made premiums paid on any life insurance policy covering the life of any officer or employee when the immediate family members of such employees are directly the beneficiary 10. Losses from wash sales of stock or securities shall not be deductible except a. the taxpayer is a dealer of securities or stock and made in the course of business of such dealer b. the share of stock sold and then required or repurchased are identical stock or securities c. the shares of stock sold and then reacquired within a period beginning thirty (30) days before the date of such sale or disposition d. the shares of stock sold and then reacquired within a period ending thirty (30) days after such sale or disposition 11. 1st statement – the allowable deduction for pension payments to employees will only apply to those pension plan that is funded 2nd statement – the pension trust deduction I composed of the past service cost and the year present service cost a. true, false b. true, true c. false, true d. false, false 12. SFI Inc. (SFI) has been in business for the past 10 years. For the year 2004, it decided to establish a pension fund for its employees. the pertinent data of the fund are us follows; Past service cost (lump sum payment) Present service cost P1,000,000 100,000 How much allowable deduction for pension cost SFI could claim? a. P1,000,000 b. P1,100,000 c. P 200,000 d. P 100,000 13. Assuming the same facts in number 12 the allowable deduction of SFI for pension after 10 years a. P1,000,000 b. P1,100,000 c. P200,000 d. P100,000 14. Mr. R was retired by his employer corporation and paid P1, 000,000 as a retirement gratuity without any deduction for withholding tax. The corporation became bankrupt the following year. Can the BIR subject the P1, 000,000 retirement gratuity to income tax? 1st answer – yes if the retirement gratuity was paid based on a reasonable pension where Mr. R was 50 years old and has served the corporation for more than 10 years 2nd answer – no if Mr. R was forced by the corporation to retire beyond Mr. R’s control a. both answer are wrong b. both answer are correct c. 1st answer is correct 2nd answer is wrong d. 1st answer is wrong 2nd answer is correct 15. The widow of your best friend has just been paid P1, 000,000 on account of the life insurance of the decreased =================================================================================================== Page 25 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== husband. she asks you whether she declare the amount the amount for income tax purpose or the estate tax purposes 1st advice – the proceeds of life insurance paid to the beneficiary upon the death of the insured are exempt income tax and need not be declared for income tax purposes 2nd advice – the proceeds of life insurance would have to be declared for estate tax purposes if the designation of the beneficiary was irrevocable otherwise it need not be declared a. both advices are correct b. 1st advice correct; 2nd advice wrong c. both advices are wrong d. 1st advice wrong and 2nd advice correct 16. ABC Corporation took two key men insurance on the life of its President Mr. X. In one policy the beneficiary is the corporation to compensate it for its expected loss in case of death of its president. the other policy designates Mr. X’s wife as its irrevocable beneficiary Question 1: are the insurance premiums paid by X corporation in both policies deductible? Question 2: will the insurance proceeds be treated as income subject to tax by the corporation and by the wife? a. yes to 1st and 2nd questions b. yes to both questions c. no to 1st questions and yes to 2nd question d. no to both questions 17. A worked for a manufacturing firm but due to business reverses, the firm offered a voluntary redundancy program in order to reduce overhead expenses. Under the program an employee who offered to resign would be given separation pay equivalent to his 3 months basic salary for every year of service. a accepted the offer and received P800,000 as separation pay under the program. After all the employees who accepted the offer were paid the firm found its overhead still excessive. Hence it adopted another program where various unprofitable departments were closed. As a result B was separated from the service B also received P800, 000 as separation pay. at the time of separation both A and B have rendered at least 10 years of service but A was 55 years old while B was only 45 years old as a result a. both amounts are exempt from income tax b. both amounts are subject to income tax c. only Mr. A is subject to income tax d. only Mr. B is subject to income tax 18. Which of the following expenses is deductible from gross income? a. contribution to a newspaper fund for needy families when such newspaper organizes a drive solely for charitable purposes b. premiums paid by the self-employed employer for the life insurance of his employees c. contribution to the construction of a chapel of a university that declares dividends to its stockholders d. donation of prizes and awards to athletes in local and international competitions and sanctioned by their respective sport associations 19. Cash dividends received by a NON RESIDENT corporation from a domestic corporation is a. exempt from income tax b. subject to final tax c. part of taxable income d. party exempt partly taxable 20. Cash dividends received by a domestic corporation from a domestic corporation is a. exempt from income tax b. subject to final tax c. part of taxable income d. partly exempt partly taxable 21. Shares obligations or bonds issued by a foreign corporation shall be considered as intangible personal property situated in the Phil’s if, how many percent of its business is located in the Phil’s? a. 33% b. 50% c. 75% d. 85% 22. If a friend inquires whether or not the cost of educational assistance to the employee and / or his dependents which are borne by the employer be taxable. What will your answer be? 1st answer – a scholarship grant to the employee by the employer shall not be treated as taxable fringe benefits if the education or study involved is directly connected with the employer’s trade business or profession and there is a written contract between them that the employee is under obligation to remain in the employ of the employer for s period of time that they have mutually agreed upon 2nd answer – the cost of educational assistance extended by an employer to the dependents of an employee shall be treated as taxable fringe benefits of the employee unless the assistance was provided through a competitive scheme under the scholarship program of the company a. both answer are correct b. both answer are wrong c. only the first answer is correct d. only the second answer is correct 23. As regards taxable year one of the following statements is not correct? a. the taxable year is the accounting period b. the taxable year maybe less than 12 months c. the taxable year of a sole proprietorship business maybe fiscal or calendar year d. the taxable year of a domestic corporation maybe fiscal or calendar year 24. Which of the following taxes may be deducted from gross income a. special Assessment b. transfer tax c. documentary stamp tax d. income tax 25. All of the following taxpayers are not entitled to tax credit except a. resident citizen with income only from the Phils b. resident citizen with income only from abroad c. resident alien with income from within and without the Phils d. non-resident citizens with income from within and without the Phils 26. A operates a retail store and owns the following properties. which of the following is capital assets in the hand of A a. building which houses the retail store b. fixture used in the retail store c. inventory on hand at the end of the year d. trade accounts receivable 27. A bought from XYZ Corp. 1,000 shares of stock Ninety days thereafter the corporation was adjudged bankrupt and its stock was worthless. the lose of A for income tax purposes is a. wagering loss b. short term capital loss c. long term capital loss d. non – deductible loss for income tax purposes 28. Any amounts subsequently received on account of a bad debt previously charged off and allowed as a deduction =================================================================================================== Page 26 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== from gross income for prior years must be included in gross income for the taxable year in which received. this is a. end result doctrine b. destination of income test c. severance theory d. equitable doctrine of tax benefit b. c. d. 29. Which of the following statements on tax exemptions is not correct a. when an electric light and power franchise holder is exempt under its franchise from property tax on its poles wires and transformers its exemption does not extend to the VAT of its importation of said articles b. where a taxpayer receives as payment for the land expropriated by the government tax exempt bonds such tax exempt bonds should be included in the total price to determine correct taxable profit therefrom c. the salaries of the justices of the Supreme Court are exempt from income tax d. exemption granted to cooperatives does not extend to be members thereof in the sale of their products 30. A was selected as the most outstanding teacher in her region. Her name was submitted by the school principal without her knowledge. she received a trophy and a cash award of P15, 000 a. taxable income b. subject to final tax c. exempt from income tax d. partly taxable partly exempt 31. This will not result to a taxable gain or loss a. the sale by a corporation of its shares of stock from the unissued stock over its par or stated value b. the sale by a corporation of its treasury stock over its cost or other basis of acquisition c. the purchase and retirement by a corporation of its bonds at a price less than the issue price or face value d. the issuance by a corporation of its bonds at a premium 32. Which of the following does not represent compensation income? a. honorarium as a guest speaker b. emergency leave pay c. vacation and sick leave pay d. gratuitous condonation of obligation 33. One of the following is not subject to final tax a. interest on savings deposit b. royalties c. prizes amounting to more than P10,000 d. professional fees paid to individuals 34. Gain on sale of domestic shares of stock in New York is a. Income within the Phils b. Income without the Phils c. Income party within and without d. Exempt from income tax 35. Noel Santos is a very bright computer science graduate. He was hired by Hewlett Packard. To entice him to accept the offer the arrangement that part of his compensation would be an insurance policy with a face value of P20 Million. The parents of Noels are made the benefices of the insurance policy. will the proceeds of the insurance form part of the income of the parents of Noel and be subject to income tax? a. yes the proceeds of the insurance form part of the gross income of the parents of Noel and be subject to income tax yes the proceeds of the insurance form part of the income of the parent of Noel and be subject to final withholding tax no, the proceeds of the life insurance do not form part of the gross income being exclusion therefrom no the proceeds of the insurance do not form part of the gross income of the parents of Noel being irrevocable beneficiaries 36. Pursuant to the preceding question can the company deduct from its gross income the amount of the premium? a. yes the premium may be deducted from the company’s gross income for it is an ordinary and necessary expense b. yes the premium may be deducted from the company’s gross income if the intended beneficiaries are the immediate family members of Noel Insured c. no the premium may not be deducted from the company’s gross income because the company was not made the beneficiary of the insurance proceeds d. no the premium may not be deducted from the company’s gross income because it is not ordinary and necessary expenses of the business 37. What are requisites of the business expense to be deductible except? a. ordinary and necessary b. paid or incurred within the taxable year c. substantiated with official receipts d. must be reasonable 38. The following are examples of non – taxable compensation for injuries except a. actual damages for injuries suffered b. compensatory damages for unrealized profits c. moral damages for grief anxiety and physical sufferings d. exemplary damages 39. What would be the allowable deduction for P8, 000 contribution made by a resident citizen to a religious organization from his P70,000 net income after contribution? a. P8,000 b. P7,000 c. P7,800 d. P3,500 40. A bought a condominium unit under installment basis to be used as his office in the practice of his profession and paying P10, 000 monthly. for income tax purposes the P10,000 monthly payment shall be a. treated as business rental, hence deductible b. treated as capital expenditure, hence not deductible c. treated as depreciation expense hence deductible d. treated as ordinary business expense 41. A domestic corporation made a borrowing from ABC bank thereby incurring a business connected interest expense of P60, 000 for taxable year 2016. During the same year the corporation earned an interest income subject to final tax in the amount of P100,000. the deductible interest is a. P27,000 b. P33,000 c. P60,000 d. P0 42. In a year ABC Corp paid total premiums of P1, 000 for the life insurance policy of the vice president where the beneficiary is the corporation. At the end of the year ABC received dividend of P100 because of the policy. the =================================================================================================== Page 27 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== corporation should indicate a claim for a deduction for life insurance premium of a. P1,000 b. P 900 c. P1,100 d. Zero 43. A dependent senior citizen will allow an individual resident citizen taxpayer a. to be classified as single b. to be promoted to a head of a family c. to be promoted to a head of a family and claim one additional exemption d. answer not given 44. Mr. A resident alien adopted a child in USA Mr. A personal exemptions is a. P 50,000 b. P 75,000 c. P100,000 d. none of the above 45. Mr. resident citizen send his child to USA for the latter’s high school studies Mr. B personal exemption is a. P 50,000 b. P 75,000 c. P100,000 d. none of the above E. CAPITAL GAINS / FRINGE BENEFITS /OTHERS 46. Calendar year is Tax payer is a citizen of the Philippines who is single Capital gain on sale of bonds held for P45,000 2 months Capital gain on sale directly to buyer 120,000 of shares of domestic corporation held for 16 months Capital loss on sale of family car held 80,000 for 5 years Capital loss on sale of land in the 60,000 Philippines held for 3 years on a selling price of P800,000 Net capital loss in 2005 (net taxable 20,000 income of the year was P30,000) The a. b. c. d. net capital gain in 2016 was P50,000 P5,000 zero some other amount 47. Nutrition Chippy Corporation gives all its employees (rank and file supervisors and managers) one sack of rice every month valued at P800 per sack. During an audit investigation made by the Bureau of Internal Revenue (BIR) the BIR assessed the company for failure to withhold the corresponding withholding tax on the amount equivalent to the one sack of rice received by all the employees contending that the sack of rice is considered as additional fringe benefit for the supervisors and managers. Therefore the value of the one sack of rice every month should be considered as part of the compensation of the rank and file subject to tax. For the supervisors and managers, the employers should be the one assessed pursuant to Section 33 (a) of the NIRC. Is there a legal basis for the assessment made by the BIR? a. yes benefits received by rank and file are subject to compensation tax b. yes benefits received by supervisory employees and managerial employees are subject to fringe benefit tax c. no the benefit is a De minimis benefit exempt from income tax d. no the benefit is for the convenience of the employer thus exempt 48. Which among the following fringe benefits is taxable? a. those benefits which are given to rank and file employees b. contributions of the employer for the benefit of the employee to retirement, insurance and hospitalization benefit plans c. benefits given to supervisory employees under a collective bargaining agreement d. de minimis benefits 49. 1st statement – monetized unused vacation leave credits not exceeding 10 days is an exempt de minimis benefit 2nd statement – daily meal allowance for overtime work not exceeding twenty five (25%) percent of the basic minimum wage is exempt fringe benefit a. true, false b. true, true c. false, true d. false, false 50. 1st statement – laundry allowance not exceeding P300 per month is exempt de minimis benefit 2nd statement – medical cash allowance to dependents of employees not exceeding P750 per employee per semester or one hundred twenty five pesos (P125) per month is exempt de minimis benefit a. true, false b. true, true c. false, true d. false, false 51. 1st statement – flowers fruits and books or other similar token items given to employees under certain circumstances are exempt de minimis benefits 2nd statement – gifts given during Christmas and major anniversary celebrations not exceeding P5, 000 per employee per annum is exempt de minimis benefit a. true, false b. true, true c. false, true d. false, false 52. 1st statement – rice subsidiary of one thousand peso or one sack of 50 kg. Rice per month amounting to not more than one thousand five hundred pesos is an exempt de minimis benefit 2nd statement – employee achievement awards e.g for length of service or safety achievement which must be in the form of a tangible personal property other than cash or gift certificate with an annual monetary value not exceeding ten thousand pesos received by an employee under an established written plan which does not discriminate in favor of highly paid employees is an exempt de minimis benefit a. true, false b. true, true c. false, true d. false, false 53. 1st statement – uniforms and clothing allowance not exceeding four thousand pesos per annum is an exempt de minimis benefit 2nd statement – actual medical benefits not exceeding P10, 000 per annum is an exempt de minimis benefit a. true, false b. true, true c. false, true d. false, false 54. In case of foreign travel of employees for the purpose of attending business meeting or conventions: 1st statement – such travel expenses shall not be treated as taxable fringe benefits regardless of its amount =================================================================================================== Page 28 of 29 UNIVERSITY OF PERPETUAL HELP SYSTEM DALTA CALAMBA CAMPUS, BRGY. PACIANO RIZAL, CALAMBA CITY, LAGUNA, PHILIPPINES TAXATION EDMUND E. HILARIO, CPA, MBA CHAPTER 3.0 – Income Taxation (16 items) 2 ND SEMESTER 2019 – 2020 ================================================================================================== 2nd statement – the cost of economy and business class airplane ticket shall not be subject to the fringe benefit tax. However 30 percent of the cost of first class airplane ticket shall be subject to the fringe benefit tax a. true, false b. true, true c. false, true d. false, false 55. On August 12, 2016 A sold a land held as capital assets for P2 M with a FMV of P1.8 M. A acquired the land for P1 M and at the time of sale the property was subject to a mortgage of P1.3 M. payments shall be; P100, 000 on the date of sale and the balance shall be paid in equal monthly instalments. the capital gain tax for 2016 is a. P120,000 b. P 24,000 c. P 36,000 d. P 48,000 for calendar year. in addition Becky Corp. had the following capital gains and losses during 2018 Short term capital gain Short term capital loss Long term capital gain Long term capital loss P8,500 (4,000) 1,500 (3,500) Becky Corp. did not realize any other capital gains or losses since it began operations. What is Becky’s total taxable income? a. P36,250 b. P38,500 c. P39,500 d. P40,500 56. How much is the allowable deduction from business income of a domestic corporation which granted and paid P340, 000 fringe benefits to its key officer in 2016? a. P500,000 b. P160,000 c. P340,000 d. none of the above 57. In the year, Cadena de Amor Corporation gave the following fringe benefits to its employees To managerial employees To rank and file employees P1,020,000 5,000,000 The allowable deduction from the gross income of the corporation for the fringe benefits given to employees is a. P2,000,000 b. P1,500,000 c. P6,320,000 d. P7,000,000 58. The tax payer other than a corporation may elect to pay the income tax due in two equal installments if the tax due is a. more than P100 b. more than P1,000 c. more than P2,000 d. more than P5,000 59. The a. b. c. d. tax reform Act of 1997 took effect on January 1, 1997 January 1, 1998 December 11, 1997 July 28, 1997 60. A feature of ordinary gains as distinguished from the capital gains a. gains from sale of assets not stock in trade b. may or may not be taxable in full c. sources are capital assets d. no holding period 61. On capital gains tax on real property which of the following statement is not correct? a. the tax should be paid if in one lump sum within 30 days from the date of the sale b. the installment payment of the tax should be made within 30 days from receipt of each installment payment on the selling price c. the tax may be paid in installment if the initial payment does not exceed 25% of the contract price d. the initial payment maybe more than down payment 62. Becky Corp. a calendar year corporation realized taxable income of P36, 000 from its regular business operations =================================================================================================== Page 29 of 29