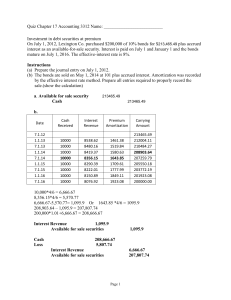

CHAPTER 19 – FA @ AMORTIZED COST BOND INVESTMENT ► FINANCIAL ASSET AT AMORTIZED COST A. The business model is to hold the financial asset in order to collect contractual cash flows on specified dates. B. The contractual cash flows are solely payments of principal and interest on the principal outstanding. FA@AC is only debt securities, there is no equity securities because equity securities has no specified dates and as well as interest. Pwede rin ang bonds sa FVPL at FVOCI, Bonds is a classic example of FA@AC kaya pwedeng tawaging Investment in Bonds. ► BONDS ╚ A formal unconditional promise made under seal to pay a specified sum of money at a determinable future date and make periodic interest payments at a state rate until the principal sum is paid. ╚ A bond is a contract of debt whereby one party called the issuer borrows fund from another party called the investor. ╚ A bond is a debt security because the bondholder is a creditor and the issuer is a debtor. May utangang nangyayari, contract of debt, merong maturity/due date. Other than the principal, nagbabayad ka din ng interest. ╚ A bond is evidenced by a certificate and the contractual agreement between the issuer and investor is contained in another document known as “bond indenture”. Sa certificate nakalagay yung Principal, Interest at Maturity date. Sa Indenture nakalagay yung mga agreements ng both parties. ╚ A bond is issued in small denomination of P100, P1,000, or P10,000 to enable more investors to purchase the bond issue. EXAMPLE: A P50,000,000 bond issue may be issued in denomination of P1,000, Thus, there share be 50,000 bonds with face of P1,000 each. ╚ An investor acquires a bond either as a temporary or permanent investment and derives regular income in the form of interest. ► KINDS OF BONDS 1. Term Bonds ╚ Bonds that mature on a single date. 2. Serial Bonds ╚ Those which have a series of maturity dates or those bonds which are payable in instalments. 3. Callable Bonds ╚ Those which may be called in or redeemed by the issuing entity prior to their date of maturity. Pwedeng bayaran ng issuer yung bonds, tatawagin nila para bayaran na kahit hindi pa umabot sa maturity date. 4. Convertible Bonds ╚ Those which give the bondholders the right to exchange their bonds for share capital of the issuing entity at any time prior to maturity. ► INTEREST PAYMENT DATE ╚ The interest on the bond investment is usually paid semiannually or every 6 months as follows: a. January 1 and July 1 b. February 1 and August 1 c. March 1 and September 1 d. April 1 and October 1 e. May 1 and November 1 f. June 1 and December 1 ╚ Of course there are certain bonds that pay interest annually or at the end of the bond year. Kapag nagbayad yung investor nang mas mataas face value that is Premium. Kapag nagbayad ng mas mababa yung investor that is Discount. ► CLASSIFICATION OF BOND INVESTMENT ╚ Bonds may be acquired as current or noncurrent investment depending on the business model of managing financial assets. ╚ Accordingly, bond investment are classified and accounted for as follows: a. Financial Asset held for Trading b. Financial Asset at Amortized Cost c. FA@FVOCI d. FA@FVPL or by irrevocable designation or by fair value option ► INITIAL MEASUREMENT ╚ Bond investments are recognized initially at fair value plus transaction costs that are directly attributable to the acquisition. (Fair Value + Transaction Costs) ╚ However, transaction costs attributable to the acquisition of bond investments held for trading at FVPL are expensed immediately. ► SUBSEQUENT MEASUREMENT ╚ Subsequent to initial recognition, bond investments are measured and accounted for as follows: a. At FVPL b. At Amortized cost c. At FVOCI On the part of the bondholder or the investor, discounts are treated as additional income or interest. Unti-untiing irerecognize ng investor yung discount through amortization, year by year. Kapag Premium naman, it is treated as a reduction of income. It is recognized same with the discount through amortization. ► ACCOUNTING OF BOND INVESTMENT ╚ Bonds may be acquired on interest date or between interest dates. ╚ When bonds are acquired on interest date, there is no accounting problem because the purchase price is initially recognized at acquisition cost. ╚ When bonds are acquired between interest dates, meaning the date of acquisition is not any one of the interest dates, the purchase price normally includes the accrued interest. ╚ That portion of the purchase price representing accrued interest should not be reported as part of the cost of investment but should be accounted for separately. ╚ In effect, in this case, two assets are acquired, namely the bonds and the accrued interest. On the date of acquisition, the accrued interest is charged either to accrued interest receivable or interest income. ╚ When accrued interest receivable is debited, upon receipt of the first semi-annual interest, the accrued interest receivable account is closed and interest income is credited for the excess. ╚ When interest income is debited, the receipt of the first semi-annual interest is credited entirely to interest income. ► ACCRUED INTEREST ON DATE OF ACQUISITION ╚ An entity acquired 12% bonds with face amount of P2,000,000 for P2,200,000 which includes accrued interest of P20,000. The bonds are held for “trading”. Trading Securities 2,180,000 Accrued Interest Receivable 20,000 Cash 2,200,000 ANOTHER APPROACH ╚ The accrued interest purchased or paid is charged to “interest income” instead of accrued interest receivable. ╚ Using the same example, the journal entry to record the acquisition of the bond investment is: Trading Securities 2,180,000 Interest Income 20,000 Cash 2,200,000 ╚ The subsequent collection of interest is simply credited to interest income. ╚ Thus, when the semi-annual interest of 120,000 is received, the journal entry is : Cash (.12 x 2,000,000 x 6/12) 120,000 Interest Income 120,000 ╚ The above approach is more convenient and will be followed for illustration. Illustration – Trading Securities ╚ April 1 Purchased P1,000,000 12% bonds at 96 plus accrued interest. Interest is payable January 1 and July 1. The bonds are held as trading investment. Trading Securities 960,000 Interest Income 30,000 Cash 990,000 Note that the accrued interest is for 3 months, from January 1 to April 1. (1,000,000 x .12 x 3/12) to get P30,000. (.96 x 1,000,000) to get P960,000. ╚ July 1 Received semi-annual interest: Cash 60,000 Interest Income 60,000 (.12 x 1,000,000 x 6/12) ╚ When the first semi-annual interest of P120,000 is received, the journal entry is: Cash 120,000 Accrued Interest Receivable 20,000 Interest Income 100,000 ╚ Oct. 31 Sold P600,000 face value bonds for 101 plus accrued interest. Sale Price (600,000 x 1.01) 606,000 Add: Accrued Interest (July 1 – Oct 31) (.12 x 600,000 x 4/12) 24,000 TOTAL CASH RECEIVED 630,000 Sale Price Less: Carrying amount of bonds sold (600K/1M or 6/10 x 960,000) GAIN ON SALE Cash ╚ Dec 31 576,000 30,000 630,000 Trading Securities Interest Income Gain on Sale of TS ╚ Dec 31 606,000 576,000 24,000 30,000 Recorded the accrued interest from July 1 to Dec. 31 on the remaining bonds of P400,000: Accrued Interest Receivable 24,000 Interest Income 24,000 (.12 x 400,000 x 6/12) The accrued interest on the P400,000 face amount is for 6 months from July 1 to December 31. The bonds are quoted at 120 at the end of the year. Changes in fair value of trading securities are recognized in profit or loss. Market Value (400,000 x 1.20) 480,000 Carrying amount of remaining bonds (960,000 – 576,000) (384,000) UNREALIZED GAIN 96,000 Trading Securities 96,000 Unrealized Gain – TS 96,000 When bond investment is held for “trading” or measured at FVPL, it is not necessary to amortize any premium or discount. ► INVESTMENT IN BONDS AT AMORTIZED COST ╚ A financial asset shall be measured at amortized cost if both of the following conditions are met: a. The business model is to hold the financial asset in order to collect contractual cash flows on specified dates. b. The contractual cash flows are solely payments of principal and interest on the principal amount outstanding. ╚ AMORTIZED COST Initial Recognition Amount Minus: Repayments (Applicable on Serial Bonds) Plus: Amortization of Discount Minus: Amortization of Premium Minus: Reduction for Impairment or Uncollectibility ╚ When bonds are acquired and classified as financial asset at amortized cost, the bond investments are classified as noncurrent investments. ► AMORTIZATION OF PREMIUM OR DISCOUNT ╚ Investment in bonds shall be measured subsequently at amortized cost. ╚ This means that any premium or discount on the acquisition of long-term investment in bonds must be amortized. ╚ Bond premium or discount is amortized over the life of the bonds. On the part of the bondholder, the life of the bonds is from the date of acquisition to the date of maturity. ╚ Amortization is done through the interest income account. a. Amortization of Bond Discount: Investment in Bonds xxx Interest Income xxx b. Amortization of Bond Premium: Interest Income xxx Investment in Bonds xxx ╚ Amortization may be made on interest dates or at the end of the reporting period. It is more convenient to record amortization at the end of the reporting period. ► PHILOSOPHY ON AMORTIZATION ╚ The reason for amortization of bond premium or discount is to bring the carrying amount of the investment to face amount on the date of maturity. ╚ When the bonds are redeemed on the date of maturity, the entry will simply be a debit to cash and credit to investment in bonds at face value. ╚ The bondholder is a creditor and will collect on the date of maturity an amount equal only to the face amount of the bonds no more and no less. ╚ Such process of allocation, Bond Premium – deduction from the interest income Bond Discount – addition to interest income… …is what traditionally called amortization. ► ACQUISITION ON INTEREST DATE ╚ 2020 April 1 Purchased P1,000,000 face amount 12% bonds at 94. Bonds pay interest semi-annually April 1 to October 1 and mature on April 1, 2025. Investment in Bonds 940,000 Cash (1,000,000 x .94) 940,000 In as much as the acquisition is on interest date, April 1, there is no accrued interest involved. October 1 ╚ On the other hand, bond discount is a gain on the part of the bondholder because the bondholder paid less than what can be collected on the date of maturity. ╚ Such gain is not recognized outright but allocated over the life of the bonds to be added to the interest income derived from the bond investment. 60,000 60,000 Dec. 31 Adjustment for accrued interest for 3 months. Accrued Interest Receivable 30,000 Interest Income 30,000 (.12 x 1,000,000 x 3/12) Dec. 31 Amortization of the bond discount for 9 months from April 1 to Dec. 31, 2020. To simplify the illustration, the straight line method of amortization is used. Face Amount 1,000,000 Cost of Bonds (940,000) DISCOUNT 60,000 ╚ Conceptually, bond premium is a loss on the part of the bondholder because the bondholder paid more than what can be collected on the date of maturity. ╚ Such loss is not recognized outright but allocated over the life of the bonds to be offset against the interest income to be derived from the bond investment. Received semi-annual interest. Cash (.12 x 1,000,000 x 6/12) Interest Income Annual Amortization (60,000 / 5 yrs.) 12,000 Amortization for 9 months (12k x 9/12) Investment in Bonds Interest Income 9,000 9,000 9,000 ╚ 2021 January 1 April 1 October 1 Reversal of the adjustment for accrued interest on December 31, 2020. Interest Income 30,000 Accrued Interest Receivable 30,000 Received semi-annual interest. Cash 60,000 Interest Income 60,000 Received semi-annual interest. Cash 60,000 Interest Income 60,000 December 31 Adjustment for accrued interest for 3 months. Accrued Interest Receivable 30,000 Interest Income 30,000 Adjustment for amortization of bond discount for 1 year: Investment in Bonds 12,000 Interest Income 12,000 Note that during the life of the bonds, the investment account, after giving due recognition for discount amortization will appear as follows: INVESTMENT IN BONDS April 1, 2020 Cost 940,000 Balance, Apr. 1, 2025 1,000,000 Dec. 31, 2020 Amortization 9,000 Dec. 31, 2021 Amortization 12,000 Dec. 31, 2022 Amortization 12,000 Dec. 31, 2023 Amortization 12,000 Dec. 31, 2024 Amortization 12,000 April 1, 2025 Amortization 3,000 1,000,000 1,000,000 Observe that on the maturity date, April 1, 2025, the carrying amount of the investment is P1,000,000, an amount equal to the face amount of the bond. ╚ The redemption of the bonds may then be simply recorded. Cash 1,000,000 Investment in Bonds 1,000,000 ► ACQUISITION BETWEEN INTEREST DATES ╚ 2021 Feb. 1 Purchased 12% P1,000,000 face amount bonds at 105 plus accrued interest on February 1, 2021. Interest is payable semi-annually on April 1 and October 1. Bonds are dated April 1, 2020 and mature on April 1, 2025: Investment in Bonds 1,050,000 Interest Income 40,000 Cash 1,090,000 Cost (1,000,000 x 1.05) Accrued Interest from Oct. 1, 2020 to Feb 1, 2021 (.12 x 1,000,000 x 4/12) TOTAL CASH PAID 1,050,000 40,000 1,090,000 April 1 Received semi-annual interest: Cash (.12 x 1,000,000 x 6/12) 60,000 Interest Income 60,000 Oct. 1 Received semi-annual interest: Cash (.12 x 1,000,000 x 6/12) 60,000 Interest Income 60,000 Dec. 31 Adjustment for accrued interest for 3 months from Oct. 1 to Dec. 31, 2021: Accrued Interest Receivable 30,000 Interest Income 30,000 (.12 x 1,000,000 x 3/12) Dec. 31 Adjustment for the amortization of the bond premium from February 1 to December 31, 2021 or 11 months using the straight line method of amortization. Interest Income (11 x 1,000) 11,000 Investment in Bonds 11,000 Life of Bonds = 02/01/21 to 04/01/25 50 months Monthly amortization (50,000 /50) 1,000 Yung 50,000 galing sa binayad ng bondholder na 1,050,000, kasi sobra ng 50,000 dapat ma-amortize yung sobra hanggang maging 1,000,000. Note that when bonds are acquired between interest dates, it is more convenient to compute monthly amortization rather than annual amortization. ╚ In succeeding years, similar entries will be prepared. If proper amortizations are made, the investment account will appear as follows: INVESTMENT IN BONDS Feb 1, 2021 1,050,000 Dec. 31, 2021 Amortization 11,000 Dec. 31, 2022 Amortization 12,000 Dec. 31, 2023 Amortization 12,000 Dec. 31, 2024 Amortization 12,000 April 1, 2025 Amortization 3,000 Balance April 1, 2025 1,000,000 1,050,000 1,050,000 Monthly amortization na 1,000 multiplied to 12 months to get 12,000 (12 x 1,000) ╚ Again on the date of maturity, when the bonds are redeemed by the issuing entity, the journal entry is: Cash 1,000,000 Investment in Bonds 1,000,000 ► SALE OF BONDS PRIOR TO MATURITY ╚ When investment in bonds is sold prior to the date of maturity, it is necessary to determine the carrying amount of the bond investment to be used as basis in computing gain or loss on the sale. ╚ In such case, amortization of the premium or discount should be recognized up to the date of sale. ╚ If the sale is between interest dates, the sale price normally includes the accrued interest. ╚ Accordingly, that portion of the sale price pertaining to the accrued interest should be credited to interest income. ╚ The difference between the sale price, after deducting the accrued interest, and the carrying amount of the bond investment represents the gain or loss on the sale of the investment. (Sale Price – Accrued Interest – Carrying amount = Gain/Loss) Illustration ╚ 2020 Aug. 1 Purchased 12% P1,000,000 face amount bonds for P1,075,000 including accrued interest. Interest is payable semi-annually May 1 and November 1. Bonds are dated May 1, 2020 and mature May 1, 2024. Total Cash Paid 1,075,000 Accrued Interest May 1 – 08/1/20 (.12 x 1,000,000 x 3/12) (30,000) COST OF BOND INVESTMENT 1,045,000 Investment in Bonds Interest Income Cash 1,045,000 30,000 1,075,000 Note that the cash payment of P1,075,000 includes accrued interest. The accrued interest purchased is not part of cost. Thus, the same is deducted from the cash paid. Nov. 1 Dec. 31 Received semi-annual interest: Cash (.12 x 1,000,000 x 6/12) 60,000 Interest Income 60,000 Adjustment for the accrued interest for 2 months from November 1 to December 31, 2020. Accrued Interest Receivable 20,000 Interest Income 20,000 (.12 x 1,000,000 x 2/12) Adjustment for the amortization of premium from August 1 to December 31, 2020 or 5 months. The straight line method of amortization is used. Life of Bonds Aug. 1, 2020 – May 1, 2024 45 months Monthly Amortization (45,000 / 45) 1,000 Interest Income (5 x 1,000) Investment in Bonds 5,000 5,000 ╚ SALE OF BONDS On February 1, 2022, the bonds were sold at 108 plus accrued interest. Sale Price (1,000,000 x 1.08) Add: Accrued Interest for 3 months from Nov. 1 2021 to February 1, 2022 (.12 x 1,000,000 x 3/12) TOTAL CASH RECEIVED 1,080,000 30,000 1,110,000 Original Cost Less: Amortization from Aug. 1 2020 to Feb. 1, 2022 or 18 months x 1,000 CARRYING AMOUNT OF BONDS 02/01/22 1,045,000 Sale Price (1,000,000 x 1.08) Carrying Amount Of Bonds 02/01/22 GAIN ON SALE 1,080,000 (1,027,000) 53,000 18,000 1,027,000 ╚ JOURNAL ENTRIES ON THE DATE OF SALE, FEBRUARY 1, 2022 a. To update the amortization of the premium up to the date of sale, February 1, 2022. Presumably, the last amortization was December 31, 2021. Investment Income (1 month x 1,000) 1,000 Investment in Bonds 1,000 b. To record the sale of bonds: Cash 1,110,000 Investment in Bonds Interest Income Gain on Sale of Bond Investment 1,027,000 30,000 53,000 ► CALLABLE BONDS ╚ Those which may be called in or redeemed by the issuing entity prior to their date of maturity. ╚ Usually, the call price or redemption price and the carrying amount of the bond investment on the date of redemption is recognized in profit or loss. ► CONVERTIBLE BONDS ╚ Those which give the bondholders the right to exchange their bonds for share capital of the issuing entity at any time prior to maturity. ╚ The existence of the conversion feature generally precludes classification of the convertible bonds as financial assets at amortized cost because that would be inconsistent with paying for the conversion feature, meaning the right to convert into equity shares before maturity. ╚ Accordingly, investment in convertible bonds can be classified as financial asset measured at fair value. ► SERIAL BONDS ╚ Those which have a series of maturity dates or those bonds which are payable in instalments. EXAMPLE: A P1,000,000 bond issued on January 1, 2020 may provide that the bond will mature as follows: December 31, 2020 200,000 December 31, 2021 200,000 December 31, 2022 200,000 December 31, 2023 200,000 December 31, 2024 200,000 ► TERM BONDS ╚ Those bonds that mature on a single date. ╚ Callable and convertible bonds can be classified as term bonds despite their special features. ► METHODS OF AMORTIZATION a. STRAIGHT LINE METHOD – provides for an equal amount of premium or discount amortization each accounting period. Straight Line Method – Discount Face Amount of Bonds Acquisition Cost on Jan. 1, 2020 Discount on the bonds Date of Bonds Date of Maturity Interest payable semi-annually on June 30 and December 31 2,000,000 1,850,000 150,000 January 1, 2020 January 1, 2023 12% ╚ Following the straight line method, the annual amortization of discount is simply computed by dividing the discount of P150,000 by the life of the bonds of 3 years or P50,000. (150,000 / 3 years) = 50,000 ╚ Schedule of annual amortization of the discount 2020 50,000 2021 50,000 2022 50,000 TOTAL BOND DISCOUNT 150,000 ╚ JOURNAL ENTRIES FOR 2020 1. Acquisition on January 1: Investment in Bonds Cash 1,850,000 1,850,000 2. Collection of semi-annual interest on June 30: Cash (.12 x P2,000,000 x 6/12) 120,000 Interest Income 120,000 3. Collection of semi-annual interest on December 31: Cash 120,000 Interest Income 120,000 4. Annual Amortization of discount: Investment in Bonds 50,000 Interest Income 50,000 Straight Line Method – Premium Face Amount of bonds 2,000,000 Acquisition Cost on January 1, 2020 2,200,000 Premium on the bonds 200,000 Date of Bonds January 1, 2020 Date of Maturity January 1, 2024 Interest payable annually on December 31 12% ╚ Following the straight line method, the annual amortization is simply computed by dividing the premium of P200,000 by the life of bonds of 4 years or P50,000. (200,000 / 4 years) = 50,000 ╚ Schedule of annual amortization of premium 2020 50,000 2021 50,000 2022 50,000 2023 50,000 TOTAL BOND PREMIUM 200,000 ╚ JOURNAL ENTRIES FOR 2020 1. Acquisition on January 1: Investment in Bonds Cash b. BOND OUTSTANDING METHOD – applicable to serial bonds and provides for a decreasing amount of amortization. Bond Outstanding Method – Discount Face amount of bonds 2,000,000 Acquisition cost on January 1, 2020 1,900,000 Discount on the bonds 100,000 Annual instalment on Dec. 31, 2020 and every December 31 thereafter 500,000 Date of bonds January 1, 2020 Interest payable semi-annually on June 30 and December 31 12% Year Bond Outstanding 2020 2,000,000 2021 1,500,000 2022 1,000,000 2023 500,000 5,000,000 Fraction 20/50 15/50 10/50 5/50 Discount Amortization 40,000 30,000 20,000 10,000 100,000 ╚ The bond outstanding is determined every bond year. Thus, the bond outstanding for 2020 is P2,000,000 and is decreased by the payment of P500,000 each year. 2,200,000 2,200,000 2. Collection of annual interest on December 31: Cash (.12 x 2,000,000) 240,000 Interest Income 240,000 3. Annual Amortization of the premium: Interest Income 50,000 Investment in Bonds 50,000 ╚ The fractions are developed from the bond outstanding column. ╚ The annual discount amortization is computed by multiplying the fractions by the amount of the discount. Thus, for 2020, 20/50 times P100,000 equals P40,000 and so on. ╚ JOURNAL ENTRIES 2020 Jan. 1 Investment in Bonds Cash 1,900,000 1,900,000 Jun. 30 Cash (.12 x 2,000,000 x 6/12) 120,000 Interest Income 120,000 Semi-annual interest Dec. 31 Cash Interest Income 120,000 120,000 Investment in Bonds 40,000 Interest Income 40,000 Amortization of discount for 2020 Cash Investment in Bond First Instalment 2021 Jun. 30 Dec. 31 500,000 500,000 Cash (.12 x 1,500,000 x 6/12) 90,000 Interest Income 90,000 Semi-annual interest Cash Intererst Income 90,000 90,000 Investment in Bonds 30,000 Interest Income 30,000 Amortization for 2021 Cash Investment in Bonds Second instalment 500,000 500,000 Bond Outstanding Method – Premium Face amount of bonds 4,000,000 Acquisition cost on Jan. 1, 2020 4,200,000 Premium on the bonds 200,000 Annual instalment on Dec. 31, 2020 and Every December 31 thereafter 1,000,000 Date of bonds Jan.1, 2020 Interest payable annually on December 31 12% ╚ ANNUAL AMORTIZATION OF PREMIUM Year Bond Outstanding Fraction Premium Amortization 2020 4,000,000 4/10 80,000 2021 3,000,000 3/10 60,000 2022 2,000,000 2/10 40,000 2023 1,000,000 1/10 20,000 10,000,000 200,000 ╚ The bond outstanding for 2020 is P4,000,000 and this is reduced by P1,000,000 each year. ╚ JOURNAL ENTRIES FOR 2020 Jan. 1 Investment in Bonds Cash Dec. 31 4,200,000 4,200,000 Cash (.12 x 4,000,000) 480,000 Interest Income 480,000 Annual Interest Interest Income 80,000 Investment in Bonds 80,000 Amortization for 2020 Cash 1,000,000 Investment in Bonds 1,000,000 First Instalment c. EFFECTIVE INTEREST METHOD – “interest method”/scientific method. It provides for an increasing amount of amortization. ╚ Bond investments shall be classified as financial assets measured at amortized cost using the effective interest method. ╚ This means that any discount or premium must be amortized using the effective interest method. ╚ The straight line method and bond outstanding method are acceptable only when the computation will result in periodic interest income that is not materially different from the amount that would be computed using the effective interest method. PROBLEMS – CHAPTER 19 ► 19 – 1 ╚ At the beginning of current year, Icon Company acquired bonds with face amount of P4,000,000 at a cost of P3,761,000. The bonds are held for trading. ╚ Bonds pay interest of 12% semi-annually on January 1 and July 1 and mature after 4 years. ╚ The bonds have an effective yield of 14% and are quoted at 105 at year end. Required: Prepare journal entries for the current year. Jan 1 Trading Securities Cash 3,761,000 3,761,000 July 1 Cash (.12 x 4,000,000 x 6/12) Interest Income 240,000 240,000 Dec. 31 Accrued Interest Receivable 240,000 Interest Income 240,000 (.12 x 4,000,000 x 6/12) Market Value (4,000,000 x 1.05) 4,200,000 Carrying amount of Bonds 3,761,000 UNREALIZED GAIN 439,000 Trading Securities Unrealized Gain – TS 439,000 439,000 ╚ Mature Company carried out the following transactions in bond investments held for trading during the current year. Aug. 1 Purchased 5,000, P1,000, 12% bonds of Acme Company at 104 plus accrued interest of P150,000. The bonds pay interest semi-annually on May 1 and November 1. Aug. 31 Purchased 2,000, P1,000, 12% bonds of Avco Company at 98 plus accrued interest. Semi-annual payment of interest, June 30 and December 31. Dec. 1 Dec. 31 The following quotations were obtained: Acme Bonds 98 Avco Bonds 99 Required: a. Prepare journal entries to record the transactions. b. Present the investments on December 31. A. JOURNAL ENTRIES Aug. 1 Trading Securities (5,000 x P1,000 x 1.04) Interest Income Cash Aug. 31 Nov. 1 ► 19 – 2 Sold 2,000 of the Acme bonds at 102 plus accrued interest. Dec. 1 5,200,000 150,000 5,350,000 Trading Securitirs (2,000 x P1,000 x .98) 1,960,000 Interest Income (.12 x 2,000,000 x 2/12) 40,000 Cash Cash (.12 x 5,000,000 x 6/12) Interest Income Sale Price (2,000,000 x 1.02) 2,000,000 300,000 300,000 2,040,000 Add: Accrued Interest from Nov. 1 to Dec. 1 (.12 x 2,000,000 x 1/12) TOTAL CASH RECEIVED 20,000 2,060,000 Sale Price Less: Carrying Amount of bonds sold (2M/5M x 5,200,000) LOSS ON SALE Cash 2,060,000 Loss on Sale of TS 40,000 Trading Securities Interest Income Dec. 31 Acme Bonds Avco Bonds 2,080,000 (40,000) 2,080,000 20,000 Accrued Interest Receivable 60,000 Interest Income 60,000 (.12 x 3,000,000 x 2/12) 3,000,000 remaining Acme Nov. 1 to Dec. 31 Cash (.12 x 2,000,000 x 6/12) Interest Income 120,000 120,000 Unrealized Loss – TS Trading Securities 160,000 160,000 CARRYING AMOUNT 3,120,000 (5,200,000 – 2,080,000) 1,960,000 (2,000,000 x .98) 5,080,000 MARKET 2,940,000 (3,000,000 x .98) 1,980,000 (2,000,000 x .99) 4,920,000 B. INVESTMENTS Current Assets: Trading Securities at FV ► 19 – 3 2,040,000 G/L (180,000) 20,000 (160,000) ╚ Bullish Company had the following transactions in bond investment held as trading for the current year. Mar. 1 Purchased 2,000, P1,000, 12% bonds of Long Company at 93 excluding accrued interest. Interest is payable on February 1 and August 1. Apr. 1 Purchased 4,000, P1,000, 12% bonds of National Corporation at 95 plus accrued interest. Interest is payable March 1 and September 1. Oct. 1 Sold 1,000 of the National bonds at 105 excluding accrued interest. Dec. 1 Sold all of the Long bonds at 100 plus accrued interest. Dec. 31 The market value of the National bonds is 90. Required: a. Prepare journal entries to record the transactions including receipt and accrued interest. b. Statement presentation of the bond investment on Dec. 31. A. JOURNAL ENTRIES Mar. 1 Trading Securities (2,000 x P1,000 x .93) Interest Income (.12 x 2,000,000 x 1/12) Cash Apr. 1 4,920,000 Aug. 1 Trading Securities (4,000 x P1,000 x .95) Interest Income (.12 x 4,000,000 x 1/12) Cash Cash (.12 x 2,000,000 x 6/12) 1,860,000 20,000 1,880,000 3,800,000 40,000 3,840,000 120,000 Interest Income Sept. 1 Oct. 1 120,000 Cash (.12 x 4,000,000 x 6/12) Interest Income 240,000 240,000 Sale Price (1,000,000 x 1.05) Add: Accrued Interest from Sept. 1 to Oct. 1 (.12 x 1M x 1/12) TOTAL CASH RECEIVED 10,000 1,060,000 1,060,000 Trading Securities Interest Income Gain on Sale of TS Dec. 1 950,000 10,000 100,000 Sale Price (2,000,000 x 1.0) Add: Accrued Interest from Aug. 1 To Dec. 1 (.12 x 2M x 4/12) TOTAL CASH RECEIVED Dec. 31 Accrued Interest Receivable 2,850,000 (150,000) Unrealized Loss – TS (National) 150,000 Trading Securities 150,000 B. STATEMENT PRESENTATION Current Asset: Trading securities at FV 2,700,000 ► 19 – 4 ╚ On July 1, 2020, Bearish Company purchased as trading investment a P2,000,000 face amount 8% bond for P2,200,000 plus accrued interest and commission of P50,000. The bond pays interest annually on December 31. ╚ On December 31, 2020, the bond investment was quoted at 95. On March 31, 2021, the entity sold the bond investment for P2,100,000 plus accrued interest. Required: Prepare journal entries for 2020 and 2021. 80,000 2,080,000 2,080,000 Trading Securities Interest Income Gain on Sale of TS 2,700,000 2,000,000 Sale Price 2,000,000 Less: Carrying amount of bonds sold 1,860,000 GAIN ON SALE 140,000 Cash Market Value (3,000,000 x .90) Carrying Amount of remaining bonds (3,800,000 – 950,000) UNREALIZED LOSS 1,050,000 Sale Price 1,050,000 Less: Carrying Amount of bonds sold (1/4 x 3,800,000) 950,000 GAIN ON SALE 100,000 Cash Interest Income 120,000 (.12 x 3,000,000 x 4/12) 1,860,000 80,000 140,000 120,000 2020 July 1 Trading Securities Commission Expense Interest Income (.08 x 2M x 6/12) Cash 2,200,000 50,000 80,000 2,330,000 Dec. 31 Cash (.08 x 2,000,000) 160,000 Interest Income 160,000 Market Value (2,000,000 x .95) 1,900,000 Carrying amount of bonds UNREALIZED LOSS Unrealized Loss – TS Trading Securities 2021 March 31 Cash Trading Securities Interest Income Gain on Sale of TS 2,200,000 (300,000) 300,000 300,000 Dec. 31 2,140,000 1,900,000 40,000 200,000 Sale Price 2,100,000 Add: Accrued Interest from Dec. 31 To March 31 (.08 x 2M X 3/12) 40,000 TOTAL CASH RECEIVED 2,140,000 Sale Price Less: Carrying Amount of Bonds (2,000,000 x .95) GAIN ON SALE Oct. 1 2,100,000 1,900,000 200,000 2021 Jan. 1 July 1 Dec. 31 ► 19 – 5 ╚ On October 1, 2020, Yost Company purchased 4,000 of the P1,000 face amount, 10% bonds of Pell Company for P4,400,000 which included accrued interest of P100,000. ╚ The bonds which mature on January 1, 2027, pay interest semi-annually on January 1 and July 1. ╚ The entity used straight line method of amortization and appropriately recorded the bonds as financial asset at amortized cost. Required: Prepare journal entries for 2020 and 2021. 2020 ► 19 – 6 Investment in Bonds Interest Income Cash 4,300,000 100,000 4,400,000 Accrued Interest Receivable 200,000 Interest Income (.10 x 4M x 6/12) 200,000 Life of Bonds = Oct 1, 2020 to Jan. 1, 2027 Monthly Amortization (300,000 / 75) 75 months 4,000 Interest Income (3 x 4,000) Investment in Bonds 12,000 Cash 12,000 200,000 Accrued Interest Income Cash (.10 x 4,000,000 x 6/12) Interest Income 200,000 Accrued Interest Income Interest Income 200,000 Interest Income (12 x 4,000) Investment in Bonds 48,000 200,000 200,000 200,000 48,000 ╚ Manda Company acquired P6,000,000 of Landoil 12% bonds on May 1, 2020 at 94 plus accrued interest to be held as financial asset at amortized cost. Aug. 1 Dec. 31 ╚ The bonds pay interest semi-annually on February 1 and August 1, and mature on February 1, 2024. ╚ The fiscal period for Manda Company is the calendar period. Amortization is done following the straight line method. ╚ On May 1, 2022, Manda Company sold all the bonds at 105 plus accrued interest. Required: Prepare journal entries for 2020, 2021, and 2022. 2020 May 1 Aug. 1 Dec. 31 2022 Jan. 1 Feb. 1 360,000 Accrued Interest Receivable (.12 x 6,000,000 x 5/12) 300,000 Interest Income 300,000 Investment in Bonds (12 x 8,000) 96,000 Interest Income 96,000 Interest Income 300,000 Accrued Interest Receivable 300,000 Cash (.12 x 6,000,000 x 6/12) Interest Income 360,000 360,000 5,820,000 Cash (.12 x 6,000,000 x 6/12) Interest Income 360,000 Sale Price (6,000,000 x 1.05) 6,300,000 Add: Accrued Interest from Feb. 1 to May 1 (.12 x 6,000,000 x 3/12) 180,000 TOTAL CASH RECEIVED 6,480,000 5,640,000 300,000 Original Cost Less: Amortization from May 1, 2020 to May 1, 2022 (24 months x 8,000) CA OF BONDS MAY 1, 2022 Sale Price Carrying amount of bonds May 1, 2022 GAIN ON SALE 6,300,000 (5,832,000) 468,000 May. 1 Investment in Bonds (4 x 8,000) Interest Income 360,000 Accrued Interest Receivable (.12 x 6,000,000 x 5/12) 300,000 Interest Income Investment in Bonds (8 x 8,000) Interest Income Feb. 1 360,000 Investment in Bonds (6,000,000 x .94) 5,640,000 Interest Income (.12 x 6,000,000 x 3/12) 180,000 Cash Life of bonds = May 1, 2020 to Feb. 1, 2024 45 months Monthly Amortization (360,000 / 45) 8,000 2021 Jan. 1 Cash (.12 x 6,000,000 x 6/12) Interest Income 64,000 64,000 Cash Interest Income 300,000 Accrued Interest Receivable 300,000 Cash (.12 x 6,000,000 x 6/12) Interest Income 360,000 360,000 ► 19 – 7 6,480,000 Investment in Bonds Interest Income Gain on Sale of Bonds 32,000 32,000 192,000 5,832,000 5,832,000 180,000 468,000 ╚ On January 1, 2020, Flexible Company acquired for P1,150,000 the entire P1,000,000 12% bond issue of another entity to be held as financial asset at amortized cost. ╚ Bonds of P200,000 mature at annual interval beginning December 31, 2020. Interest is payable semi-annually on June 30 and December 31. Required: a. Prepare a schedule of amortization following the bond outstanding method. b. Prepare journal entries for the current year. A. SCHEDULE OF AMORTIZATION YEAR BOND OUTSTANDING 2020 2021 2022 2023 2024 FRACTION 1,000,000 800,000 600,000 400,000 200,000 3,000,000 B. JOURNAL ENTRIES Jan. 1 Investment in Bonds Cash 10/30 8/30 6/30 4/30 2/30 1,150,000 60,000 Dec. 31 Cash 60,000 60,000 Interest Income ► 19 – 8 ╚ The date of the bonds is February 1, 2020 and the interest is payable semi-annually on February 1 and August 1. ╚ The bonds mature annually at the rate of P1,000,000 on February 1, 2020 and every February 1 thereafter. Required: a. Prepare a schedule of amortization following the bond outstanding method. b. Prepare journal entries for 2020 and 2021. A. SCHEDULE OF AMORTIZATION YEAR 10/01/20 02/01/21 02/01/21 02/01/22 02/01/22 02/01/23 60,000 MONTH OUTSTANDIN G 4 months PESO MONTH FRACTION DISCOUNT AMORTIZATION – BOND OUTSTANDI NG 3,000,000 12,000,000 12/48 75,000 – 2,000,000 12 months 24,000,000 24/48 150,000 – 1,000,000 12 months 12,000,000 12/48 75,000 48,000,000 1,150,000 June 30 Cash (.12 x 1,000,000 x 6/12) Interest Income Interest Income Investment in Bonds PREMIUM AMORTIZATION 50,000 40,000 30,000 20,000 10,000 150,000 ╚ On October 1, 2020, Complex Company purchased a 12% P3,000,000 face amount bond issue for P2,700,000 excluding accrued interest to be held as financial asset at amortized cost. B. JOURNAL ENTRIES 2020 Oct. 1 Investment in Bonds 2,700,000 Interest Income (.12 X 3,000,000 x 2/12) 60,000 Cash 50,000 50,000 Dec. 31 Accrued Interest Receivable 150,000 300,000 2,760,000 Interest Income (.12 x 3,000,000 x 5/12) Investment in Bonds 56,250 Interest Income (75,000 x 3 / 4) Oct 1 to Dec 31 = 3 months 2021 Jan. 1 Feb. 1 150,000 Cash (.12 x 3,000,000 x 6/12) 180,000 Interest Income 180,000 1,000,000 Investment in Bonds Dec. 31 56,250 Interest Income 150,000 Accrued Interest Income Cash Aug. 1 150,000 1,000,000 Cash (.12 x 2,000,000 x 6/12) 120,000 Interest Income 120,000 Note that every interest payment date the face amount changes from 3,000,000 , it becomes 2,000,000 because the 1,000,000 matured last Feb. 1, 2021 Accrued Interest Receivable Interest Income 150,000 150,000 Jan. 1 to Feb. 1 2021 (75,000 x 1 / 4) Feb. 1 to Dec. 31 2021 (150,000 x 11/12) TOTAL AMORTIZATION FOR 2021 18,750 137,500 156,250 Investment in Bonds Interest Income 156,250 156,250