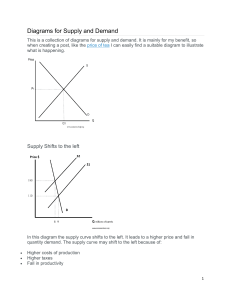

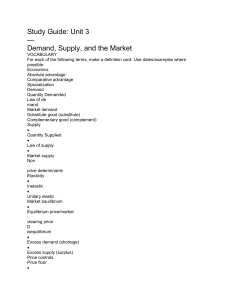

Week Two Reading Chapter 3 & 4 Wednesday, September 15, 2021 11:37 AM Chapter 3 - Demand, Supply, and Price 3.1 Demand • Quantity Demand - The amount of a good or service that consumers want to purchase during some time period - Desired quantity; the amount that consumers want to purchase when faced with a particular price of product, other product price, their incomes, their tastes etc. Total amount of product that consumers want to buy is influenced by the following variables: - Product's own price - Consumers' income - Prices of other products - Consumers' tastes - Population - Significant changes in weather • Quantity Demanded and Price - Alfred Marshall (1842-1924) called a fundamental relation the "law of demand" - lower the price, higher the quantity demanded; higher the price, lower the quantity demanded - When price goes up on a product, consumers decide to switch wholly or partly to other products. - As price goes down of the product, consumers will switch from other products whose prices have not fallen which increases demand. • Demand Schedules and Demand Curves - Demand Schedule - A table showing the relationship between quantity demanded and the price of a product, other things being equal - The Table above shows a hypothetical demand schedule For apples. It list the prices of the apples and the demand of the apple. As the price increases for the apple the demand decreases - A graph is another method to show quantity demanded and price. Price is the y axis while quantity is the x axis - Demand Curve - The graphical representation of the relationship between quantity demanded and the price of a product, other things being equal - The negative slope indicates the quantity demanded increases as price falls. - Demand - The entire relationship between the quantity of a product that buyers want to purchase and the price of that product, other things being equal • Shifts in the Demand Curve - Sometimes Demand can change on a product due to other factors - For example, In the table and the graph above, it shows the demand has increased. If the average household income increases that could mean that they have more money to spend on apples. Which causes the Demand curve shift to the right - If Demand shifts rightward , this is an increase in demand. But if Demand shifts leftward, this is a decrease in demand. 5 Causes of shifts in the demand curve 1. Consumers' Income - If average income rises, consumers desire more products. This means demand shifts to the right. Vice versa if income decreases. (demand shifts to the left) - Normal goods: Goods for which the quantity demanded increases when income rises - Inferior goods: Goods for which quantity demanded falls when income rises 2. Price of Other Goods - Substitute in consumption - Goods that can be used in place of another good to satisfy needs or desires - Example can be if price of apples goes down but the price of oranges remain fixed, then consumers will buy more apples as a substitute of oranges - Complements in consumption - Goods that send to be consumed together - Ex. Cars and gas, golf clubs and gold balls - Example can be if price of apples goes down but the price of oranges remain fixed, then consumers will buy more apples as a substitute of oranges - Complements in consumption - Goods that send to be consumed together - Ex. Cars and gas, golf clubs and gold balls 3. Consumers' Tastes - Consumers have different taste for products which can change demand - For example, shift from typewriters to computers 4. Population - Increase of population will mean more purchasing power. Therefore, demands for all the products can right and shift the curve to the right 5. Significant Changes in Weather - Demand for some products are affected by dramatic changes in the weather. - For ex. During winter, demand can increase for electricity, natural gas, and other energy sources used to heat homes. During summer, farmers' demand for water increases to water their crops - Movements Along the Curve Versus Shifts of the Whole Curve<Review* - Change in demand - A change in the quantity demanded at each possible price of the product, represented by a shift in the whole demand curve - Change in quantity demanded - A change in the specific quantity of the good demanded, represented by a change from one point on a demand curve to another point, either on the original demand curve or on a new one demand curve to another point, either on the original demand curve or on a new one 3.2 Supply • Quantity Supplied - The amount of a good or service that producers want to sell during some time period - Key Variables of quantity supplied of a product: - Products own price - Price of inputs - Technology - Government taxes or subsidies - Prices of other products - Significant changes in weather - Number of suppliers • - Quantity Supplied and Price Price of a product and the quantity supplied are related positively Higher the product price, the more producers will supply The lower the price, the less its producers will supply • Supply Schedules and Supply Curves - Supply schedule - A table showing the relationship between quantity supplied and the price of a product, other things being equal - Supply Curve - The graphical representation of the relationship between quantity supplied and the price of a product, other things being equal - Supply: The entire relationship between the quantity of some good or service that producers wish to sell and the price of that product, other things being equal • Shifts in the Supply Curve - Supply: The entire relationship between the quantity of some good or service that producers wish to sell and the price of that product, other things being equal • Shifts in the Supply Curve - Shift at the supply curve means that at each price is a change in the quantity supplied - As you see in the graph above, the graph shifts to the right because the prices of the products have decreased. Therefore more quantity of the product - If the graph shifts to the left, that means the price of the product increase and thus, less quantity of the product. • 6 causes of shifts in supply curves 1. Price of inputs - Inputs are all things that a firm uses to make its products such as materials, labour, and machines - Higher the input, the less profit they make from making the product - Therefore, higher the price of the input, the less the firm will produce - This causes the supply curve to shift to the left; fall in the price of input make production more profitable and therefore shifts the supply curve to the right 2. Technology - Advancement of technology are causing increase in our ability to produce new products and services - Nanotech, 3D printing, robotics are examples of technologies that reduce the costs of producing existing goods - Technological innovation can decrease the production cost which increases profits - Therefore, technological change shifts the supply curve to the right 3. Government Taxes or Subsidies - Government put taxes on production of specific goods such as gasoline, - Technological innovation can decrease the production cost which increases profits - Therefore, technological change shifts the supply curve to the right 3. Government Taxes or Subsidies - Government put taxes on production of specific goods such as gasoline, cigarettes, and alcohol - These taxes make the production and sale of the goods less profitable and makes the supply curve shift to the left - Government also subsidize producer - which is they pay them a specific amount for each unit of good produced - subsidy increases the profitability of production and supply curve shifts to the right 4. Prices of Other Products - Changes of price of one product may lead to changes in the supply of other product because two products can be substitutes or complements 5. Significant Changes in the Weather - Can affect mostly agricultural products - For ex. Drought, excessive rain, or flooding can all massively reduce the supply of wheat 6. Number of Suppliers - Increase in the number of suppliers is to shift the supply curve to the right - Decrease will shift the supply curve to the left • Movements Along the Curve Versus Shifts of the Whole Curve - Change in Supply: The Change in the quantity supplied at each possible price of the product, represented by a shift in the whole supply curve - Change in quantity supplied: A change in the specific quantity supplied, represented by a change from one point on a supply curve to another point, either on the original supply curve or on a new one 3.3 The Determination of Price • The Concept of a Market - Market: Any situation in buyers and sellers can negotiate the exchange of 3.3 The Determination of Price • The Concept of a Market - Market: Any situation in buyers and sellers can negotiate the exchange of goods and services • Market Equilibrium - Equilibrium price is the intersection of demand and supply curves - Above the equilibrium is excess supply which means less demand and more apples available - Below the equilibrium is excess demand which means more demand but less apples available - Excess Demand: A situation in which, at the given price, quantity demanded exceeds quantity supplied - Excess Supply: A situation in which, at the given price, quantity supplied exceeds quantity demanded - Excess supply causes downward pressure of price - Demand causes upward pressure on price - Equilibrium Price: The price at which quantity demanded equals quantity supplied. Also called the market-clearing price - Disequilibrium price: A price at which quantity demanded does not equal quantity supplied - Disequilibrium: A situation in a market in which there is excess demand or excess supply • - Changes in Market Equilibrium Four possible shifts: Increase in demand (Rightward shift in the demand curve) Decrease in demand (a Leftward shift in the demand curve) Increase in supply (A rightward shift in the supply curve) Decrease in supply (A leftward shift in the supply curve) - Increase in demand (Rightward shift in the demand curve) Decrease in demand (a Leftward shift in the demand curve) Increase in supply (A rightward shift in the supply curve) Decrease in supply (A leftward shift in the supply curve) - Comparative statics: The derivation of predictions by analyzing the effect of a change in a single exogenous variable on the equilibrium - Endogenous variables (Equilibrium price and quantity) - Exogenous variable (The variables whose changes cause shifts in the demand and supply curves) - Effects of the four possible curve shifts: 1. An increase in demand causes an increase In both the equilibrium price and the equilibrium quantity exchanged 2. A decrease in demand causes a decrease in both the equilibrium price and the equilibrium quantity exchanged 3. An increase in supply causes a decreases in the equilibrium price and increase equilibrium quantity exchanged 4. A decrease in supply causes an increase in equilibrium price and a decrease in the equilibrium quantity exchanged Reasons of the shifts: 1. An increase in Demand (Demand curve shifts to the Right) - Creates a shortage at the initial equilibrium price, unsatisfied buyers bid up the price - Rise in price causes larger quantity supplied 2. A Decrease in demand (The demand curve shifts to the left) - Decrease in demand creates surplus at the initial equilibrium price, unsuccessful buyers bid the price down - Less of the product supplied and offered for sale 3. An Increase in supply (Supply curve shifts to the right) - Increase in supply creates surplus at the initial equilibrium price, 2. A Decrease in demand (The demand curve shifts to the left) - Decrease in demand creates surplus at the initial equilibrium price, unsuccessful buyers bid the price down - Less of the product supplied and offered for sale 3. An Increase in supply (Supply curve shifts to the right) - Increase in supply creates surplus at the initial equilibrium price, unsuccessful suppliers force the price down 4. Decrease in supply (The Supply curve shifts to the left) - Decrease in supply creates shortage at the initial equilibrium price that causes the price to be bid up Chapter 4 - Elasticity 4.1 Price Elasticity of Demand - Demand is said to be elastic when quantity demanded is quite responsive to changes in price - When quantity demanded is relatively unresponsive to changes in price, demand is said to be inelastic - In part (i), it shows that demand is relatively elastic because when the price goes up, the demand decreases at a faster rate which in other words it is responsive to price changes - In part (ii), it shows that demand is relatively inelastic because when the price goes up, the demand decreases at a slower rate which means that demand is not responsive to price change • The Measurement of Price Elasticity responsive to price changes - In part (ii), it shows that demand is relatively inelastic because when the price goes up, the demand decreases at a slower rate which means that demand is not responsive to price change • The Measurement of Price Elasticity - When we want to deal with different initial price-quantity equilibria, we need to decide whether we are interested in absolute or percentage changes - The table above shows that cheese is more elastic and coffee machines is least elastic. This is because there is a higher change in demand when the price of cheese is reduced by $2 and for coffee, there is a lower change in demand when the price of coffee is reduced by $2 - Price of elasticity of demand: A measure of the responsiveness of quantity demanded to a change in the product's own price - - The equation above is used to calculate price of elasticity of demand • The Use of Average Price and Quantity in Computing Elasticity - Table above is an example on how to calculate demand elasticities - How to Calculate the percentage decrease in price & percentage increase in quantity: (Refer to Table 4-2) - "Triangle" Q is the change in quantity demanded that occurs because of the change in price - "Triangle" P is the change in price itself - Calculation: • Interpreting Numerical Elasticities - Extreme cases: Elasticity is zero when a change in price leads to no change in quantity demanded. Another extreme, when a very small change in price leads to an enormous change in quantity demanded, elasticity is very large in number. Inelastic demand: Following a given percentage change in price, there is a • Interpreting Numerical Elasticities - Extreme cases: Elasticity is zero when a change in price leads to no change in quantity demanded. Another extreme, when a very small change in price leads to an enormous change in quantity demanded, elasticity is very large in number. - Inelastic demand: Following a given percentage change in price, there is a smaller percentage change in quantity demanded; elasticity is less than 1 - Elastic demand: Following a given percentage change in price, there is a greater percentage change in quantity demanded; elasticity is greater than 1 - If price rises by 10 percent and quantity demanded falls by exactly 10 percent, we say that demand is unit elastic - Demand curve does not have a constant elasticity, even though it does have a constant slope 4.2 Price Elasticity of Supply - Price of Elasticity of supply: A measure of responsiveness of quantity supplied to a change in the product's own price - Formula: - Increase in price causes an increase in quantity supplied - In the table above, Supply elasticity is computed using average price and average quantity supplied - Even though the graph has constant slope, the measure of supply elasticity may be different at different places - When ns > 1, supply is said to be elastic - When ns < 1, supply is said to be inelastic - Special cases: - If supply curve is vertical, quantity supplied does not change as price changes. Therefore, the elasticity is 0 - A horizontal supply curve has an infinite elasticity of supply: • Ease of Substitution - If supply curve is vertical, quantity supplied does not change as price changes. Therefore, the elasticity is 0 - A horizontal supply curve has an infinite elasticity of supply: • Ease of Substitution - Substitution can vary in production as well as in consumption. - Depends on how easy it is for producers to shift from the production of other products to the one whose price has risen - Ex. If a factory that produces snowmobiles can easy produce jet skis, then the supply of each product will be more elastic than if the factory cannot substitute the products. • Short Run and Long Run - Difficult to change quantity supplied in response to a price increase in matter of weeks or months but can be easy to do so over the years - The short run supply curve shows the immediate response of quantity supplied to a change in price given producers current capacity to produce the good. - The long-run supply for a product is more elastic than the short run supply. For ex. Oil production because if oil fields is discovered, wells drilled, and pipelines are built over the years not months. 4.3 Elasticity Matters for Excise Taxes (REVIEW THIS) - Excise tax: A tax on the sale of a particular product. For ex. Cigarettes, alcohol, or gasoline - Tax incidence: The location of the burden of a tax - that is, the identity of the ultimate bearer of the tax. - Burden of an excise tax is distributed between consumers and sellers in a manner that depends on the relative elasticities of supply and demand - After the imposition of an excise tax, the difference between the consumer and seller prices is equal to the tax. In the new equilibrium, the quantity exchanged is less than what occurred without the tax. - When demand is inelastic relative to supply, consumers bear most of the burden of excise taxes. When supply is inelastic relative to demand, producers bear most of the burden 4.4 Other Demand Elasticities (REVIEW SECTION) • Income Elasticity of Demand - Income elasticity of demand: A measure of the responsiveness of quantity demanded to a change in income - Normal Goods: A good for which quantity demanded rises as income rises-its income elasticity is positive - Inferior Goods: A good for which quantity demanded falls as income rises - its income elasticity is negative • Income Inelastic - If income elasticity is positive but less than one, we say the demand for this good is income inelastic • Income Elastic income elasticity is negative • Income Inelastic - If income elasticity is positive but less than one, we say the demand for this good is income inelastic • Income Elastic - If income elasticity is positive and greater than one, we say the demand for this good is income elastic • Luxuries Versus Necessities - Necessities: Products for which the income elasticity of demand is positive but less than one - Luxuries: Products for which the income elasticity of demand is positive and greater than one - The more necessary an item is in the consumption pattern of consumers, the lower is its income elasticity • Inferior Goods - Inferior goods have a negative income elasticity because an increase in income actually leads to a reduction in quantity demanded • Cross Elasticity of Demand - Cross elasticity of demand: A measure of the responsiveness of the quantity of one product demanded to changes in the price of another product - The positive or negative signs of cross elasticities tell us whether products are substitutes or complements