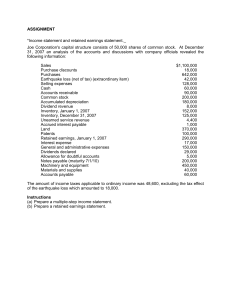

ASSIGNMENT #3 PROBLEMS (Provide a solution for every question) Mara Company provided the following data at year-end: Authorized share capital Unissued share capital Subscribed share capital Subscription Receivable Share Premium Retained earnings unappropriated Retained earnings appropriated Revaluation surplus Treasury shares, at cost 5,000,000 2,000,000 1,000,000 400,000 500,000 600,000 300,000 200,000 100,000 1. What total amount should be reported as shareholders’ equity? Authorized share capital 5,000,000 Unissued share capital ( 2,000,000) Subscribed share capital 1,000,000 Subscription Receivable (400,000) Share Premium 500,000 Retained earnings unappropriated 600,000 Retained earnings appropriated 300,000 Revaluation surplus 200,000 Treasury shares, at cost (100,000) Total shareholders’ equity P5,100,000 Glenn Company provided the following information at year-end: Preference share capital, P100 par 2,300,000 Share Premium – preference share 805,000 Ordinary share capital, P100 par 5,250,000 Share Premium – ordinary share 2,750,000 Subscribed ordinary share capital 50,000 Retained earnings 1,900,000 Note payable 4,000,000 Subscription receivable – ordinary share 400,000 2. What is the amount of legal capital? Preference share capital, P100 par Ordinary share capital, P100 par Subscribed ordinary share capital AMOUNT OF LEGAL CAPITAL 2,300,000 5,250,000 50,000 P7,600,000 Munn Company reported the following equity accounts: Preference share capital, par value P15 Share Premium – preference share Ordinary share capital, no par, P50 stated value 2,550,000 150,000 3,000,000 3. What is the number of issued and outstanding shares for each class? Preference share (2,550,000/par value P15) = 170.000 Ordinary share (3,000,000/P50) = 60,000 East Company issued 1,000 shares with P5 par to Howe as compensation for 1,000 hours of legal services performed. Howe usually bills P160 per hour for legal services. On that date of issuance, the share was trading on a public exchange at P140. 4. By what amount should the share premium account increase as a result of the transaction? 1,000 shares issued x P 140 = P 140,000 1,000 shares x P5 par value = 5,000 share premium account increase P 135, 000 Kalinga Company reported the following adjusted account balances at year-end: Share capital Share premium Treasury share, at cost Actuarial loss on defined benefit plan Retained earnings unappropriated Retained earnings appropriated Revaluation surplus 15,000,000 5,000,000 2,000,000 1,000,000 6,000,000 3,000,000 4,000,000 Cumulative translation adjustment – credit 1,500,000 5. What amount should be reported as shareholder’s equity at year-end? Share capital Share premium Treasury share, at cost Actuarial loss on defined benefit plan Retained earnings unappropriated Retained earnings appropriated Revaluation surplus Cumulative translation adjustment – credit Shareholder’s equity at year-end 15,000,000 5,000,000 (2,000,000) (1,000,000) 6,000,000 3,000,000 4,000,000 1,500,000 P 31,500,000