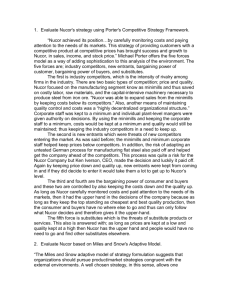

PORTER 5 FACTOR ANALYSIS Risk Legend: 5 -V High 4 - High 3- Medium 2- Low 1- V Low Rivalry among competitors Threat of Substitute # Threat of New entrants Remarks Risk 1 Barriers to Entry Huge barriers wrt Govt regulationin terms 2 of safety, land, quality and captial req 2 Economies of Scale Need to set up org at scale tocompete in market catering to big players. Any new entrant will find it difficult to scale up to Nucor's business level at entry level 2 3 Brand Loyalty Difficult to break brand loyalty as Nucor has a wide base of loyal customers eg it's a preferred supplier for GM 2 4 Capital Requirements Huge capital is required to compete at Nucor's level for any new entrant 1 5 Cumulative Experience This is very difficult to imbibe as Nucor had its share of success anf failure learning over a period of 45 yrs. Any new entrant will take ample time to accumulate industry and business exp 1 6 Government Policies Govt policies are not detrimental to set up 3 new industries. Infact states like Texas, New Jersey promote industry belts. Even financial insitutions provide monetary support for new entrants. 7 Access to Distribution Channels Nucor has established its own set of 2 distribution channels through its own subsidiaries. These distribution channels are located at prime locations near customer sites. All the company’s low-end steel products (50 percent of its total output) were distributed through steel service centers. Its high-end products (the other 50 percent) were sold directly to original equipment manufacturers (OEMs), fabricators, or end-use customers. 8 Switching Costs Customers are highly unlikely to switch to 2 any new entrant easily as Nucor products make a key component in customer's product and reliability and quality are of prime importance. Risk Value 15 Risk Threat of New Entrant 15 Bargain Power - Supplier 14 Bargain Power - Buyer 14 Threat of Substitute 11 Rivalry among competitors 23 Risk Threat of New Entrant 25 20 15 Rivalry among competitors 10 Bargain Power Supplier 5 0 Threat of Substitute Bargain Power Buyer Bargaining Power of Suppliers Remarks Risk Number of Suppliers Nucor has huge dependency on 3 suppliers for raw materials etc. Though there is not enough information on the number of suppliers and key suppliers/Tiers, steel industry usually relies on handfull of suppliers for pig.cast iron. Assuming Nucor has small number of suppliers they will have some level of bargaining power. However, this os offset as Nucor itself had acquired facility to convert scrap material to steel through mini-mills thereby reducing major dependency. Size of Suppliers There is no information on this aspect. 3 However, assuming that there will be a mix of suppliersboth Large (Tier I) and small (Tier II, Tier IIIs) they will definintely bring someimpact on bargaining power. This is offset with the long standing relationship of Nucor and established position in the industry. Uniqueness of each supplier's product This is dfficult to ascertain. However since Nucor has a wide range of products and has heterogeneous portflio the components would be supplied by unique suppliers. 3 Focal Company's ability to substitute Not much information here. However, 2 Nucor has the ability to replace suppliersbased on performance as it is driven by quality Switching Cost of Supplier This depends on multiple aspects: 3 i. Component for which supplier is being replaced, ii. whether that component is critical or generic, iii. whether that component plays the role at up-strem or down-stream in value chain iv. Relationship with supplier (longstanding/new) v.) Role of Supplier - Panorganization or limited to handful of subsidiaries/plants etc vi.) Whether losing this supplier will result is losing against competitor etc 14 Bargaining Power of Buyers Remarks Risk Number of Customers Nucor catered to multiple industries, 2 construction industry (60 percent), the automotive and appliance industries, (15 percent), and the oil and gas industries (15 percent), with the remaining 10 percent divided among miscellaneous users. So overall it'd a huge customer base. Since the number of customers were not few the colective bargaining power did not pose a serious challenge to Nucor Size of each customer order Nucor catered to some large organizations eg GM. These customers had their own purchasing targets and guidelinesfor suppliers which increased their barganing power. 3 Differences between competitors Since Nucor was involved in wide range 2 of industry segments the customers had their own set of requirements. Automotive didn't compete with construtionand construtction industry did not compete with home appliance indsutry etc. These buyers acted independently and had low influence in terms of bargaining. Price Sensitivity Nucor prodcuts were not directly 2 cosnumed by end products and hence they were not exposed to huge price sensitivity.The industry Nucor catered to had its own cycle of Price Highs and Lows. This is debatable as Nucor though 2 technologically superior in certain areas still had tough competitors like Bethelem, USX_US and LTV. Nucor customers were not much likely to replace it with customers asNucor enjoyed distinct advantages in certain product portfolios eg low-end steel for use in commercial appl and high end steel plate for automotive catalysts. Moreover, for certain segment, eg nonflat steel Nucor had no competition as Integrated Steel Companies were driven out by Nucor due to technical advancement and low costs. Buyer's ability to substitute Buyer's information availability How openly product information is 1 available to Nucor customers is not clearly known. However, steelindustry is verly unlike airline industry where prices are openly available over websites and products could be quickly bought. Switching Cost This is not clear though it depends how 2 customer assembly line, certification, integration, transportation, design costs wuld be impacted if a supplier is switched 14 Threat of substitute products Remarks Number of substitute products available There are few 2 substitutesa available in high end , high cost product segments. However, lower end steel segment was dominated by Nucor Buyer's propensity to substitute Nucor enjoyed a huge confience as a suppier within its customer eg it won BEST SUPPLIER award fromGM for straight 3 years. Risk 1 Rivalry among Exiting Competitors Number of Competitors Diversity of Competitors Relative price performance of substitute This depends upon which 2 segment the subsitution is done. For eg a substitute in Automtive Catalsyt Steel may impact overall vehicle cost as CC are usually costly Industry Concentration Perceived level of Product differentitation Nucor had a distinct differentiation of its product in certain categories eg reinforcement bars etc Industry growth Switching Costs This depends upon the 3 product and segment. Usually, the switching cost would not be higher for lower end products 3 Quality differences Brand Loyalty Barriers to Exit Switching Costs 11 Remarks Risk Direct competion with USX-US, Bethelem and LTV 4 Most of the competitors had 3 sameprodcut portfolio. Hower, Nucor had the advantage of the widest variety of prodcuts Nucor has market share of roughly 24.5% by volume in 2015 3 Average industry growth 2-4% 3 huge 2 Customers loyal to Nucor brand 2 due to quality and cost Huge barriers due to socioeconomic impact 4 Switching costs of csutomers between competitors is high 2 23